CHAPTER 14

UNDERSTANDING THE ISSUES

1. A major concern is that the value used as a

existing partnership’s net assets. Existing

capital balances most often do not reflect

30% interest by paying 30% of the existing

partnership’s capital will not result in the in-

However, the incoming partner’s capital

balance of $30,000 will only represent a

2. The first step would be to determine the fair

value of the net assets of the original part-

been recognized. Once the fair value of the

net assets (e.g., $400,000) has been

suggested value of the new partnership

entity ($400,000 ÷ 80% = $500,000). The

partnership and that of the original partner-

3. Several guidelines govern the process of

liquidating a partnership. First, all assets

ception to this priority involves the doctrine

of right of offset. Third, every attempt

say, all distributions should be based

on the conservative assumptions that re-

4. If a fellow partner has a deficit capital

balance, it is possible that other partners

will have to absorb that deficit partner’s

during the liquidation process, it is hoped

that the deficit will be eliminated. If the

creditors and that those creditors will attach

to the personal assets of individual part-

14–2

with personal wealth could end up having

to contribute additional assets to the part-

14–3 Ch. 14—Exercises

EXERCISES

(1)

Inventory ……………………………………………………………………….. 58,000

Accounts Receivable …………………………………………………. 18,000

(2) If the $56,000 of goodwill proved to be worthless, Warner would be charged 35% of

$56,000, or $19,600. However, the real harm to Warner would be that of having paid more

EXERCISE 14-2

Date:

To: My client

From: Student, CPA

Re: Issues involving goodwill and the liquidation of a partnership

With respect to the questions you had regarding the above referenced matter, please consider

the following responses which correspond to your questions (1) through (7).

(1) It is correct that a corporation cannot record goodwill unless it has been purchased through

the acquisition of another company. However, in the case of a partnership, when a new

Exercise 14-2, Concluded

(2) The goodwill method involves recording goodwill and/or the appreciation on net assets and

results in measuring net assets at amounts that are more in line with economic market val-

(3) The capital of a partner is the last claim against assets to be satisfied given the liquidation

of a partnership. Technically, the claims are satisfied in the following order: amounts owed

(4) Unsatisfied partnership liabilities could attach to any one or more partners that had person-

al assets. Obviously, the unsatisfied creditors would seek out those partners that have the

(5) Given the above response, it would be better to have a corporation own the office building

and thereby shelter it from being directly included in your personal assets. This does not

(6) Per the response to item (3) above, a loan to the partnership would have a higher priority in

liquidation than a capital investment. However, loans typically have a rate of return that is

(7) In theory, the sales price should not differ between what is offered by the partnership and

that offered by an individual partner. In that case, the key factor would be which party has

EXERCISE 14-3

(1) A sale by Freeman to another individual, as compared to a sale to the partnership, would

(2) The $125,000 paid to Freeman relative to their capital balance of $80,000 represents a bo-

nus of $45,000 that is allocated between the remaining partners according to their propor-

(3) The $45,000 over excess over Freeman’s capital balance represents two things: 1) Free-

(4) Once again, the $45,000 over excess over Freeman’s capital balance represents two

things: 1) Freeman’s share of the appreciation in value of the recorded net assets and 2)

Freeman’s share of the total entity goodwill. If the partnership is going to recognize goodwill

(5) Given the movement toward recognizing net assets at fair value, the method set forth in (4)

(6) If the current method were to be retained, it is imperative that the method for determining

“average capital” be clearly set forth. Is it a simple or a weighted average? What impact do

draws and loans have on the calculation, etc. Using just capital as a basis for allocation

EXERCISE 14-4

(1) The note payable has a market value greater than the book value that will reduce the net

asset value of the partnership by $15,000. However, the assets whose market values differ

(2) If the value of Petersen’s interest before consideration of goodwill is $104,500 as set forth

(3) Both Jacobsen and Olsen would be acquiring equal interests in the net asset values asso-

ciated with Petersen’s interest; therefore, one would expect them to value these assets at

(4) Based on the $104,500 value in item (1) above, a half interest in that would be $52,250.

Therefore, selling a half interest for $60,000 suggests that $7,750 represents Petersen’s

(5) In either case, Petersen should sell his interest for the same price. However, the ability for

him to collect the sales price may be a factor. The partnership itself may have a greater

ability to pay the sales price. The partnership may have a greater ability to borrow the ne-

14–7 Ch. 14—Exercises

EXERCISE 14-5

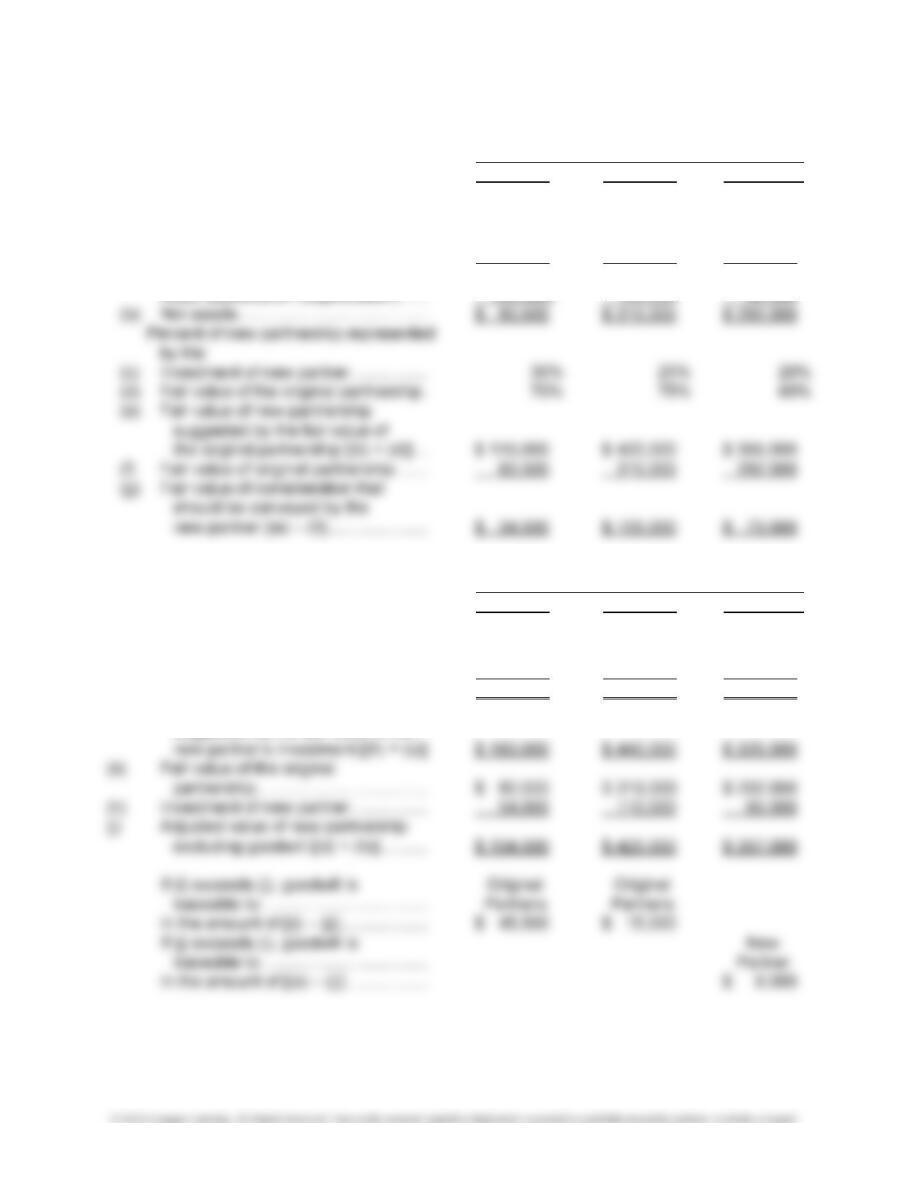

(1) Partnership

A B C

Fair market value of original partnership:

Assets at book value ……………………. $ 500,000 $ 600,000 $ 800,000

Liabilities at book value and fair

market value …………………………….. (369,500) (410,000) (558,000)

(a) Book value of original partnership ….. $ 130,500 $ 190,000 $ 242,000

(2) Partnership

A B C

Amount of consideration to be conveyed:

Value of land ………………………………. $ 50,000 $ 50,000 $ 50,000

Value of cash ……………………………… 4,000 60,000 15,000

(h) Total consideration ………………………. $ 54,000 $ 110,000 $ 65,000

(i) Fair value of new partnership

suggested by the fair value of the

Exercise 14-5, Concluded

Proof:

(a) Book value of original partnership ….. $130,500 $190,000 $242,000

Asset appreciation (depreciation) …… (50,000) 125,000 50,000

Goodwill traceable to original

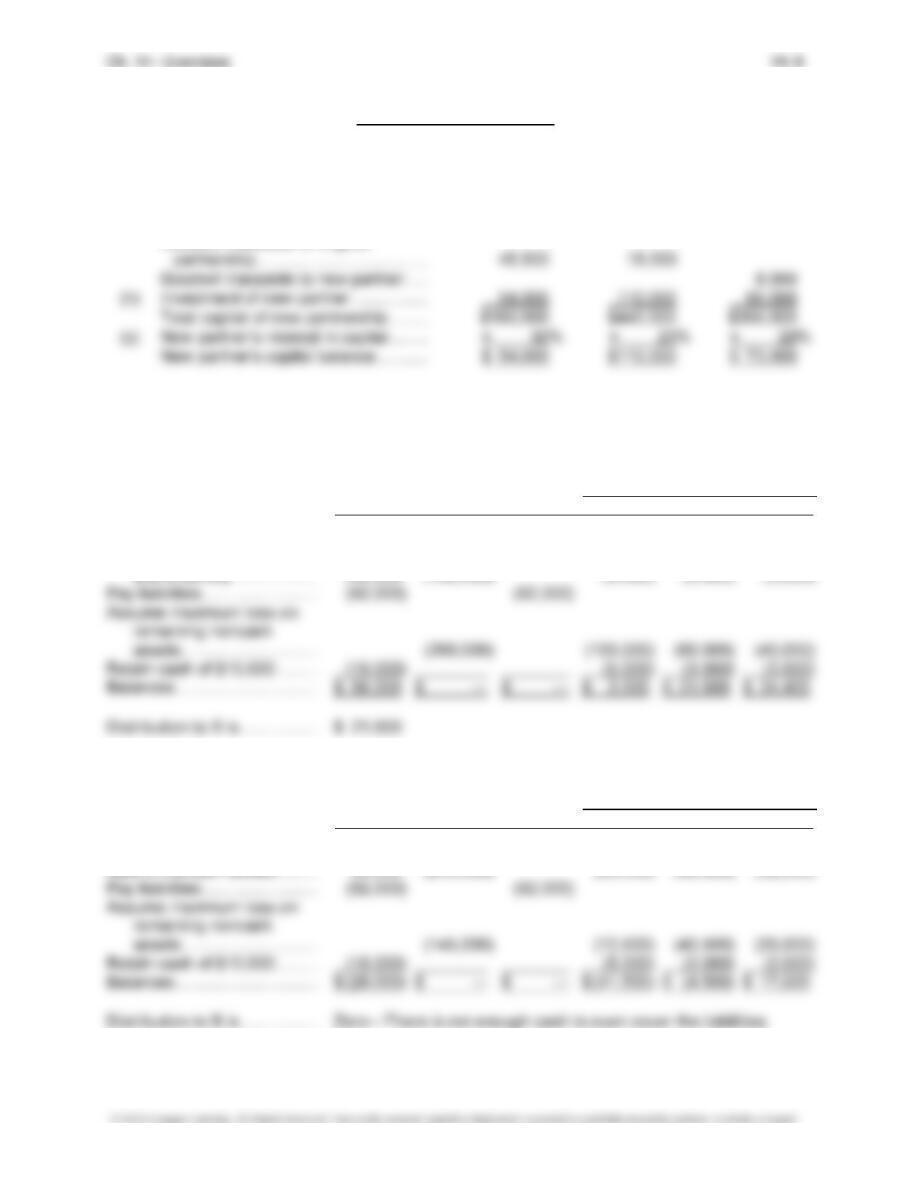

EXERCISE 14-6

1. Combined Capital

Noncash and Loan Balances

Cash Assets Liabilities A (50%) B (30%) C (20%)

Beginning balance ……………. $ 20,000 $ 358,000 $ 92,000 $116,000 $ 90,000 $ 80,000

Liquidation of receivables

2. Combined Capital

Noncash and Loan Balances

Cash Assets Liabilities A (50%) B (30%) C (20%)

Beginning balance ……………. $ 20,000 $ 358,000 $ 92,000 $116,000 $ 90,000 $ 80,000

Exercise 14-6, Concluded

3. Combined Capital

Noncash and Loan Balances

Cash Assets Liabilities A (50%) B (30%) C (20%)

Beginning balance ……………. $ 20,000 $ 358,000 $ 92,000 $116,000 $ 90,000 $ 80,000

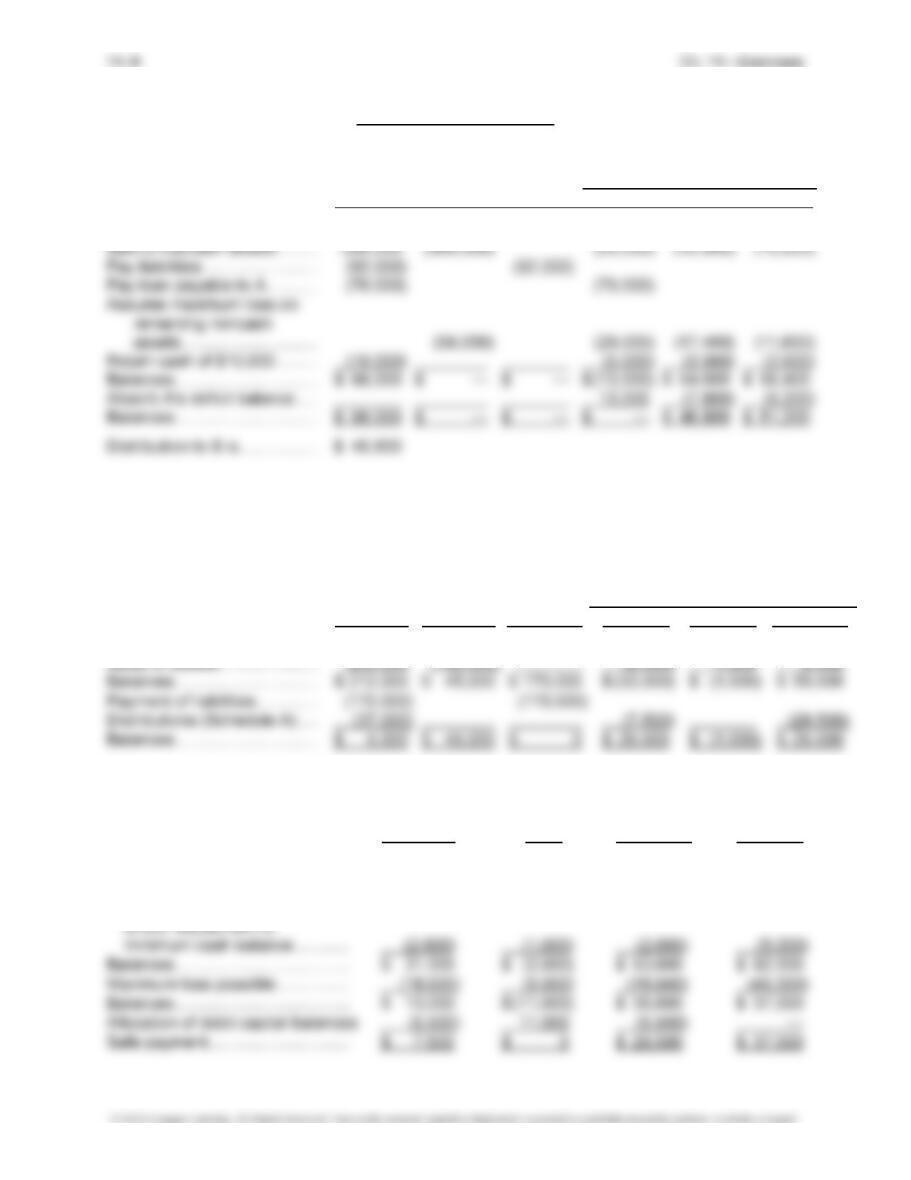

EXERCISE 14-7

1. None of the available cash would be available to Boyd.

Noncash Combined Capital and Loans

Cash

Assets Liabilities Adams Boyd Chambers

Beginning balances …………… $ 12,000 $ 255,000 $ 170,000 $ 25,000 $(5,000) $ 47,000

Schedule A

Schedule of Safe Payments

Adams

Boyd Chambers Total

Profit and loss percentages ……… 40% 20% 40% 100%

Combined capital and loan balances $ 33,000 $ (1,000) $55,000 $ 87,000

Estimated liquidation expenses

Exercise 14-7, Concluded

2. $6,000 of the available cash would be available to Boyd.

Noncash Combined Capital and Loans

Cash

Assets Liabilities Adams Boyd Chambers

3. Boyd would be liable to Adams for $10,000.

Noncash Combined Capital and Loans

Cash

Assets Liabilities Adams Boyd Chambers

Beginning balances …………… $ 12,000 $ 255,000 $ 170,000 $ 25,000 $(5,000) $ 47,000

Sales of assets …………………. 150,000 (255,000) (30,000) (15,000) (30,000)

Balances …………………………. $ 162,000 $ 0 $ 170,000 $ (5,000) $ (20,000) $ 17,000

4. Boyd would need a final capital balance of $16,000 represented by their personal deficit of

$16,000. Therefore, their share of the gain on the sale of assets would have to be $21,000

so that after offsetting their $5,000 deficit capital balance, they would have a final balance of

$16,000. Therefore the assets would have to be sold for $330,000 ($225,000 + ($21,000 di-

vided by 20%).

Noncash Combined Capital and Loans

Cash

Assets Liabilities Adams Boyd Chambers

EXERCISE 14-8

(1) Allocation of typical profits under the original partnership’s agreement:

Cumulative

A

B C Total

Salaries …………………………… $30,000 $30,000 $40,000 $100,000

Bonus to A* ……………………… 12,000 112,000

Remaining profits ……………… 10,000 4,000 6,000 132,000

Total ……………………………….. $52,000 $34,000 $46,000

Allocation of new partnership profits necessary to satisfy Bower:

Cumulative

A

B C D Total

Salaries ………………………………… $30,000 $30,000 $40,000 $30,000 $130,000

Remaining profits* …………………. 42,000 14,000 42,000 42,000 270,000

(2) The fair value of the net assets of the original partnership is $56,000 ($530,000 –

$474,000). If Dawson acquires a 30% interest in the capital of the partnership, this would

(3) If the partnership were liquidated as described, Bower would receive additional cash of

$88,200, determined as follows:

Noncash Offset Capital Balances

Cash

Assets Liabilities Arnold Bower Chambers

Beginning balances ……. $ 0 $ 680,000 $ 430,000 $ 50,000 $140,000 $ 60,000

Recognition of liability …. 4,000 (2,000) (800) (1,200)

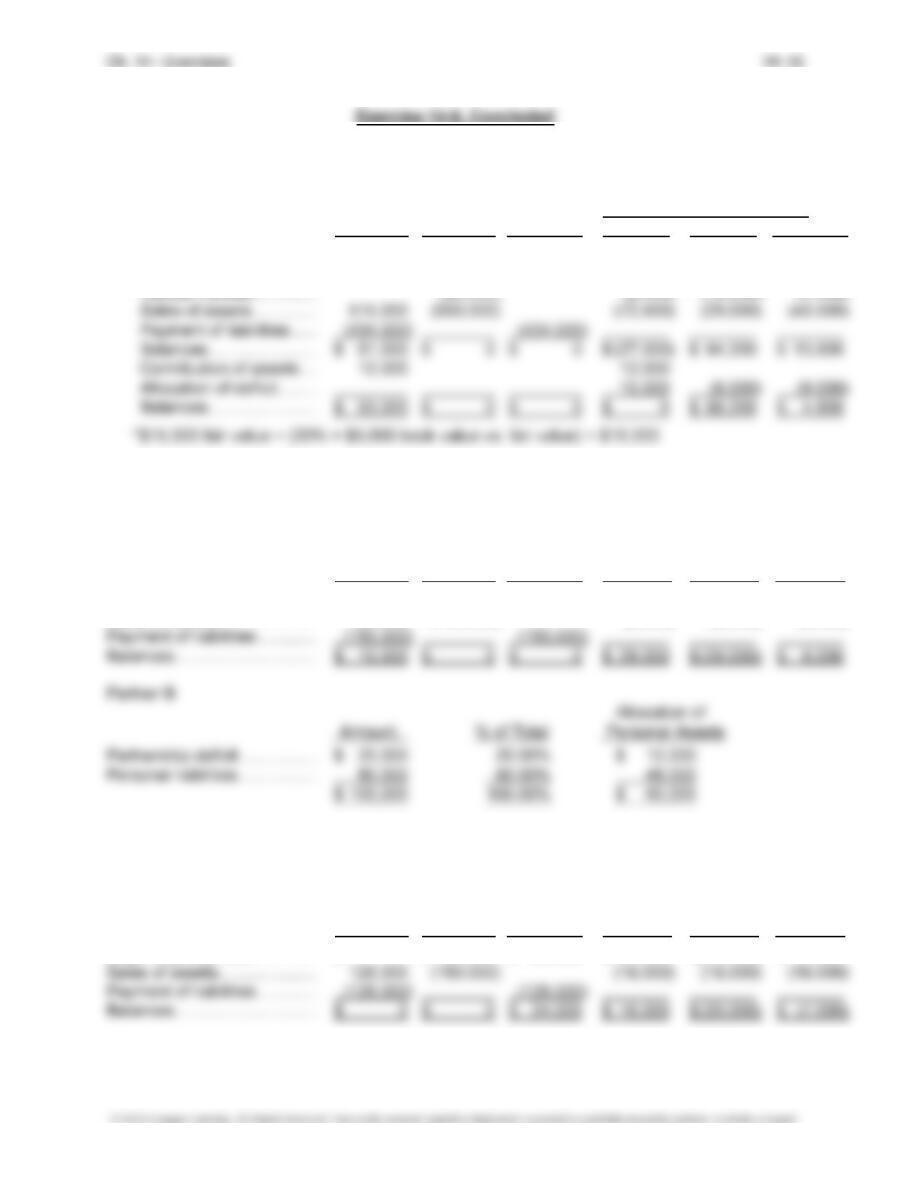

EXERCISE 14-9

1. Partner B could contribute $12,000 determined as follows:

Other

Cash

Assets Liabilities Partner A Partner B Partner C

Beginning balances …………… $ — $ 180,000 $ 150,000 $ 34,000 $(15,000) $ 11,000

Sales of assets …………………. 165,000 (180,000) (5,000) (5,000) (5,000)

2. After Partner A contributes $22,500 toward the $24,000 of remaining partnership liabilities,

Partner C would contribute the remaining $1,500 since they have net personal assets of

$8,000. Determined as follows:

Other

Cash

Assets Liabilities Partner A Partner B Partner C

Beginning balances …………… $ — $ 180,000 $ 150,000 $ 34,000 $(15,000) $ 11,000

Exercise 14-9, Concluded

Partner A

Allocation of

Amount

% of Total Personal Assets

Partnership creditors …………. $ 24,000 37.50% $ 22,500

3. The amounts contributed by Partners B and C are adequate to satisfy the remaining part-

nership creditors. Therefore, Partner A would not need to contribute any additional funds to

the partnership.

Other

Cash

Assets Liabilities Partner A Partner B Partner C

Beginning balances …………… $ — $ 180,000 $ 150,000 $ 34,000 $(15,000) $ 11,000

Sales of assets …………………. 135,000 (180,000) (15,000) (15,000) (15,000)

Payment of liabilities …………. (135,000) (135,000)

Partner B

Allocation of

Amount

% of Total Personal Assets

Partnership deficit …………….. $ 30,000 33.33% $ 15,000

Personal liabilities …………….. 60,000 66.67% 30,000

4. Partner A would first have to absorb the remaining deficit balances of Partners B and C

leaving Partner A with a final capital balance of $3,200. This $3,200 is all that the personal

Ch. 14—Problems 14–14

PROBLEMS

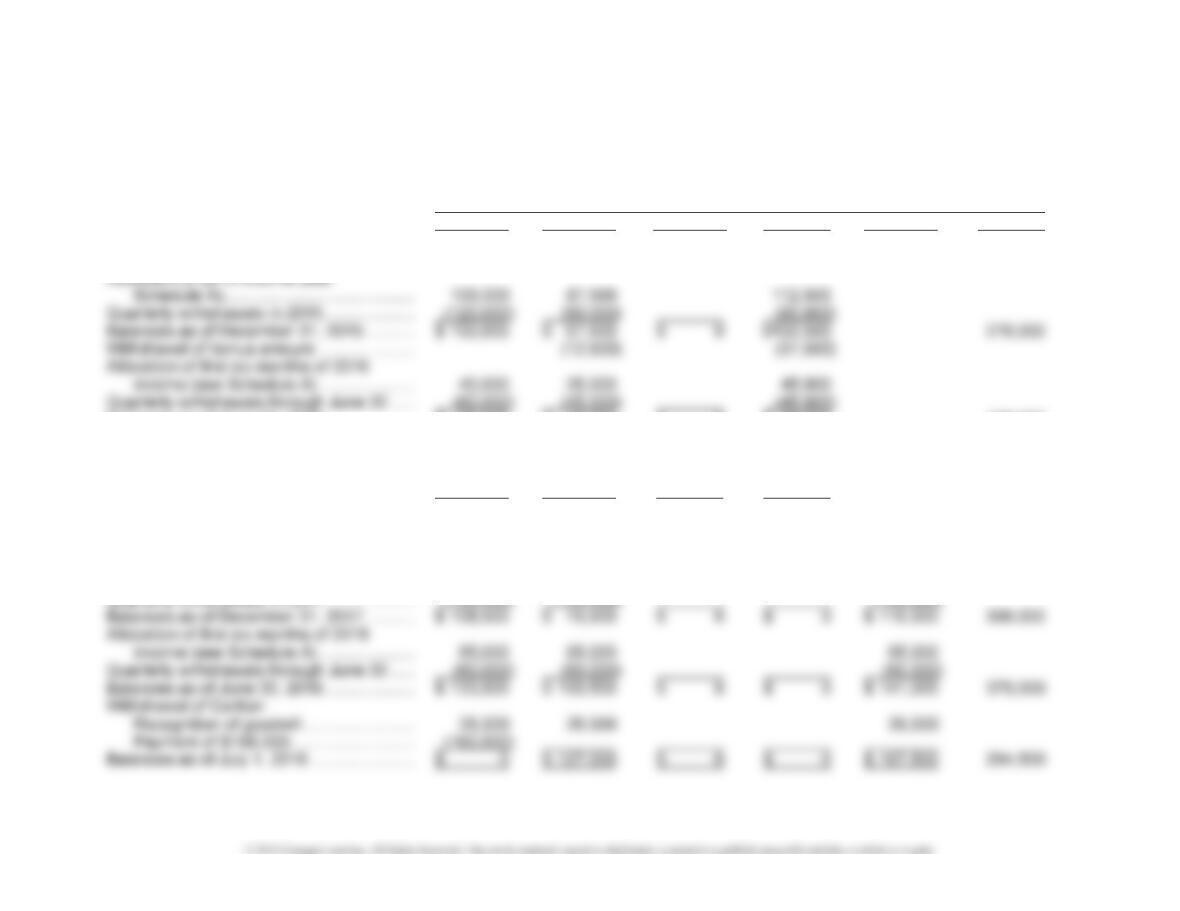

PROBLEM 14-1

Capital Balances

Carlton Weber Stansbury Laidlaw Wilson Total

Balances as of December 31, 2014 …….. $ 120,000 $ 70,000 $ 80,000 $270,000

Withdrawal of Stansbury ………………………. (80,000) $ 80,000

Balances as of June 30, 2016 ……………….. $ 80,000 $ 45,000 $ 0 $ 65,000 190,000

Acquisition of Laidlaw’s interest …………….. (8,000) (6,000) (65,000)

Allocation of second six months of

2016 income (see Schedule A) ………… 36,500 36,500

Quarterly withdrawals through December 31 (20,000) (20,000)

Balances as of December 31, 2016 ……….. $ 88,500 $ 55,500 $ 0 $ 0 144,000

Admit Wilson to partnership

($144,000/60% = $240,000) ……………. $ 96,000

Allocation of 2017 income (see

Schedule A)…………………………………… 140,000 140,000 140,000

14–15 Ch. 14—Problems

Problem 14-1, Concluded

Schedule A—Allocation of Net Income

Carlton

Weber Laidlaw Wilson Total

2015 Salary ………………………………. $120,000 $ 90,000 $ 90,000 $300,000

Bonus (Note A) ………………….. 12,500 37,500 50,000

Subtotal ……………………………. $120,000 $102,500 $127,500 $350,000

2nd 6 mos.

2016 Per profit and loss

percentages …………………. $ 36,500 $ 36,500 $ 73,000

2017 Per profit and loss

percentages …………………. 140,000 140,000 $140,000 420,000

1st 6 mos.

PROBLEM 14-2

(1) Partner B’s capital balance will now be 80% of $30,000 or $24,000.

(2) The understatement of $25,000 is traceable to the original partnership and the total part-

ners’ capital would increase $25,000 to a revised total of $140,000. The $140,000 would

(3) The overstatement of $25,000 is traceable to the original partnership and the total partners’