Problem 14-2, Concluded

(4) The capital of the original partnership plus the contribution of the new partner would total

(5) The contribution of $66,000 represents a 30% interest in a partnership with a total value of

$220,000. Therefore, the value traceable to the original partnership must be $154,000

(6) After the contribution of $70,000 the total capital of the new partnership would be $185,000

(7) The $25,000 understatement in value of the recognized assets is traceable to the original

partners and total partnership capital would increase to $140,000 ($115,000 plus $25,000).

Dividing the $140,000 by 70% (the original partners’ interest in the new partnership) would

(8) The $25,000 understatement in value of the recognized assets is traceable to the original

partners and total partnership capital would increase to $140,000 ($115,000 plus $25,000).

(9) Adjusting the partnership for the $30,000 understatement in value would increase B’s capi-

tal to $39,000 ($30,000 + 30% times $30,000). If B is paid $51,000 for their interest, this

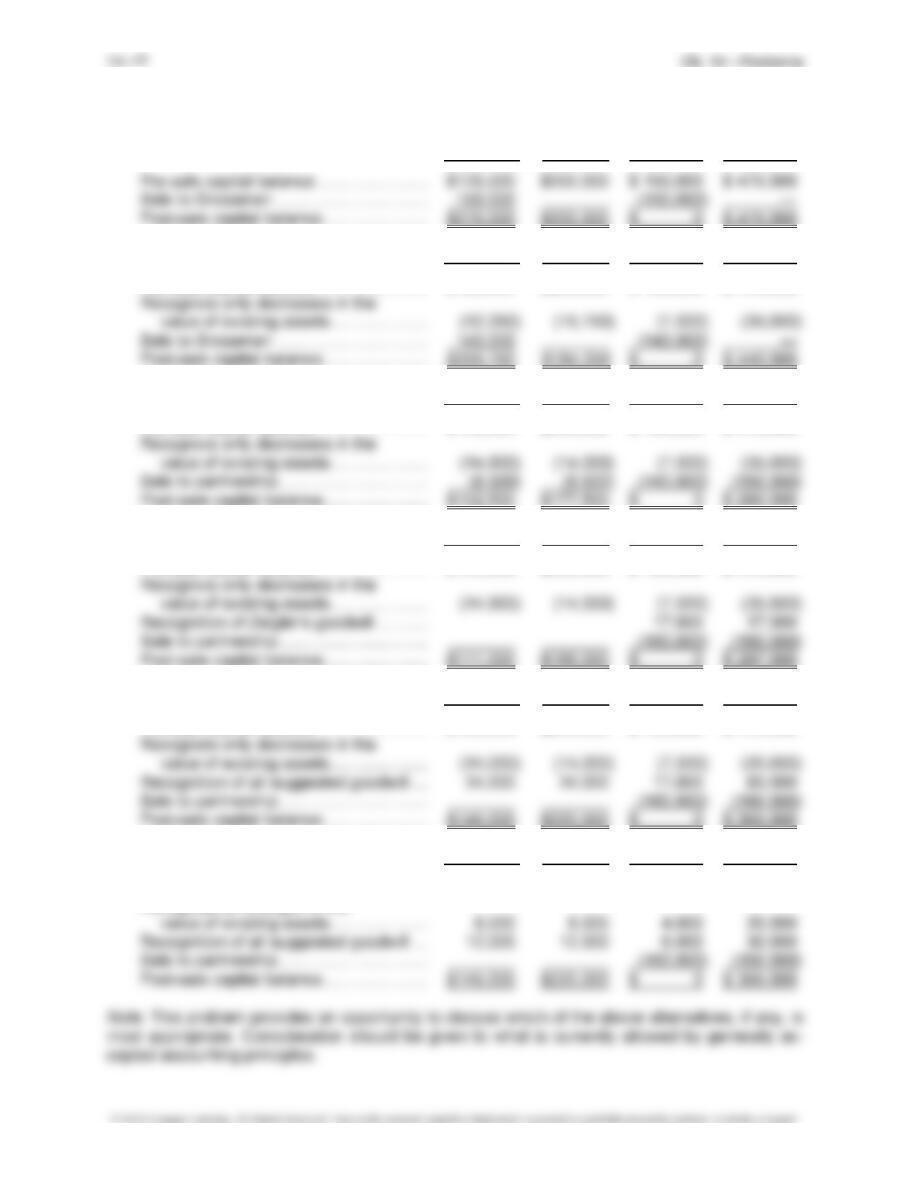

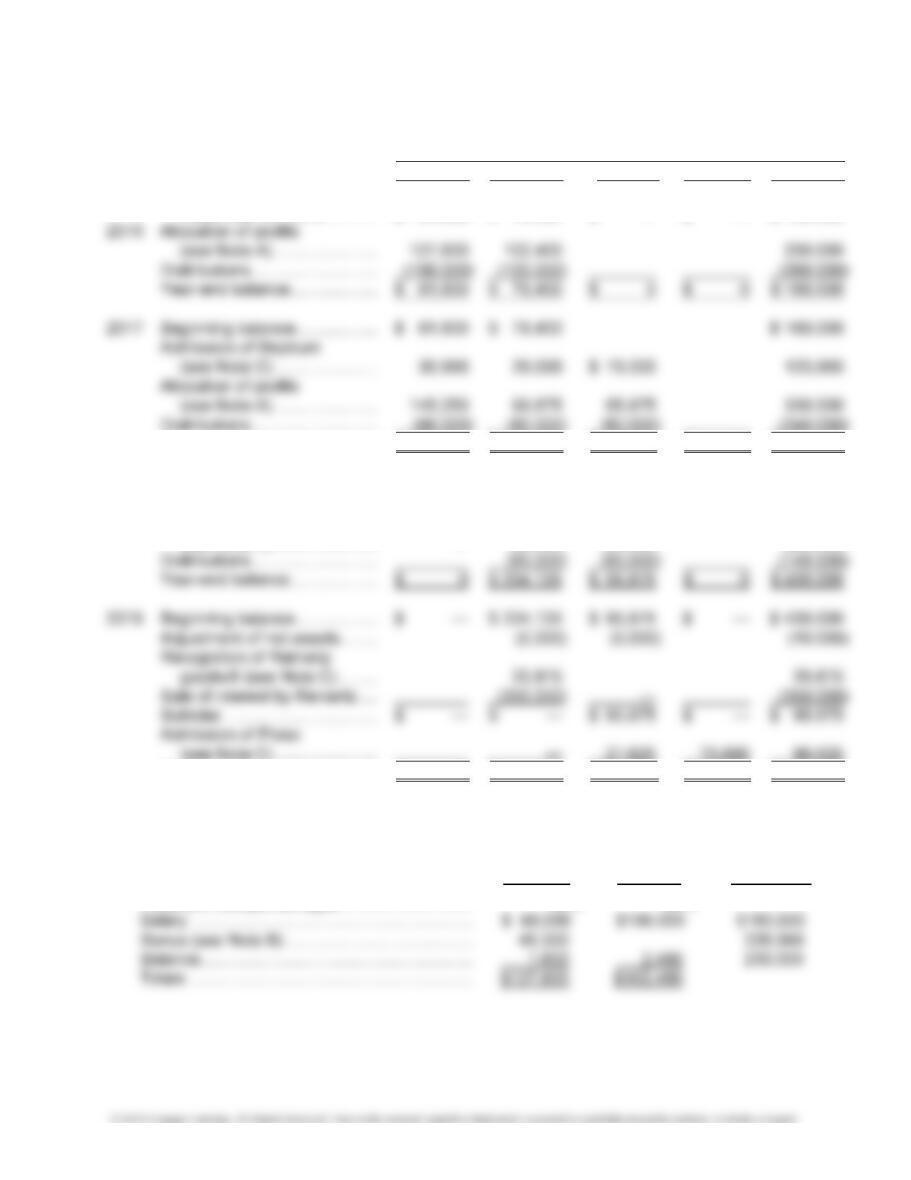

PROBLEM 14-3

(1) Grossman Casper Ziegler Total

(2) Grossman Casper Ziegler Total

Pre-sale capital balance …………………… $125,000 $200,000 $ 150,000 $ 475,000

(3) Grossman Casper Ziegler Total

Pre-sale capital balance …………………… $125,000 $200,000 $ 150,000 $ 475,000

(4) Grossman Casper Ziegler Total

Pre-sale capital balance …………………… $125,000 $200,000 $ 150,000 $ 475,000

(5) Grossman Casper Ziegler Total

Pre-sale capital balance …………………… $125,000 $200,000 $ 150,000 $ 475,000

(6) Grossman Casper Ziegler Total

Pre-sale capital balance …………………… $125,000 $200,000 $ 150,000 $ 475,000

Recognize all changes in the

PROBLEM 14-4

(1) Capital Balances

Davis

Murray Clay Rayburn Total

Balances as of

December 31, 2013 ……………. $ 50,000 $ 80,000 $ 70,000

Distribution of Clay’s 2013 bonus

(see Schedule A) ……………….. (36,000)

Admission of Rayburn (see

Schedule B) ………………………. (3,300) (3,300) (3,300) $ 68,900

Distribution of Clay’s 2014 bonus

(see Schedule A) ……………….. (6,000)

Distribution of 2014 other income

(see Schedule A; 80% ×

(see Schedule A) ……………….. 0 0 0 0

Allocation of 2016 income* (see

Schedule A) ………………………. 0 40,948 40,948 28,104

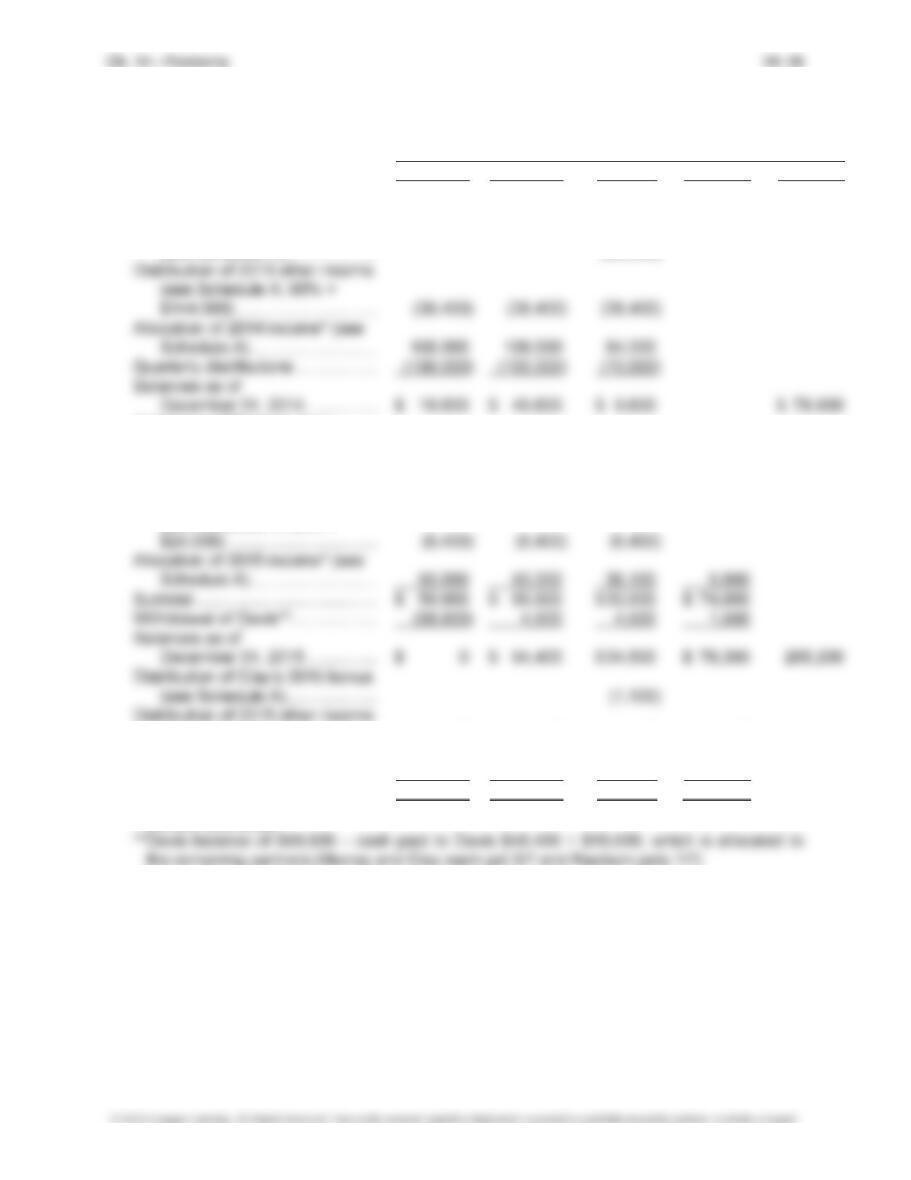

Balances as of June 30, 2016 …… $ 0 $ 135,348 $ 74,348 $104,404 314,100

*Not yet distributed

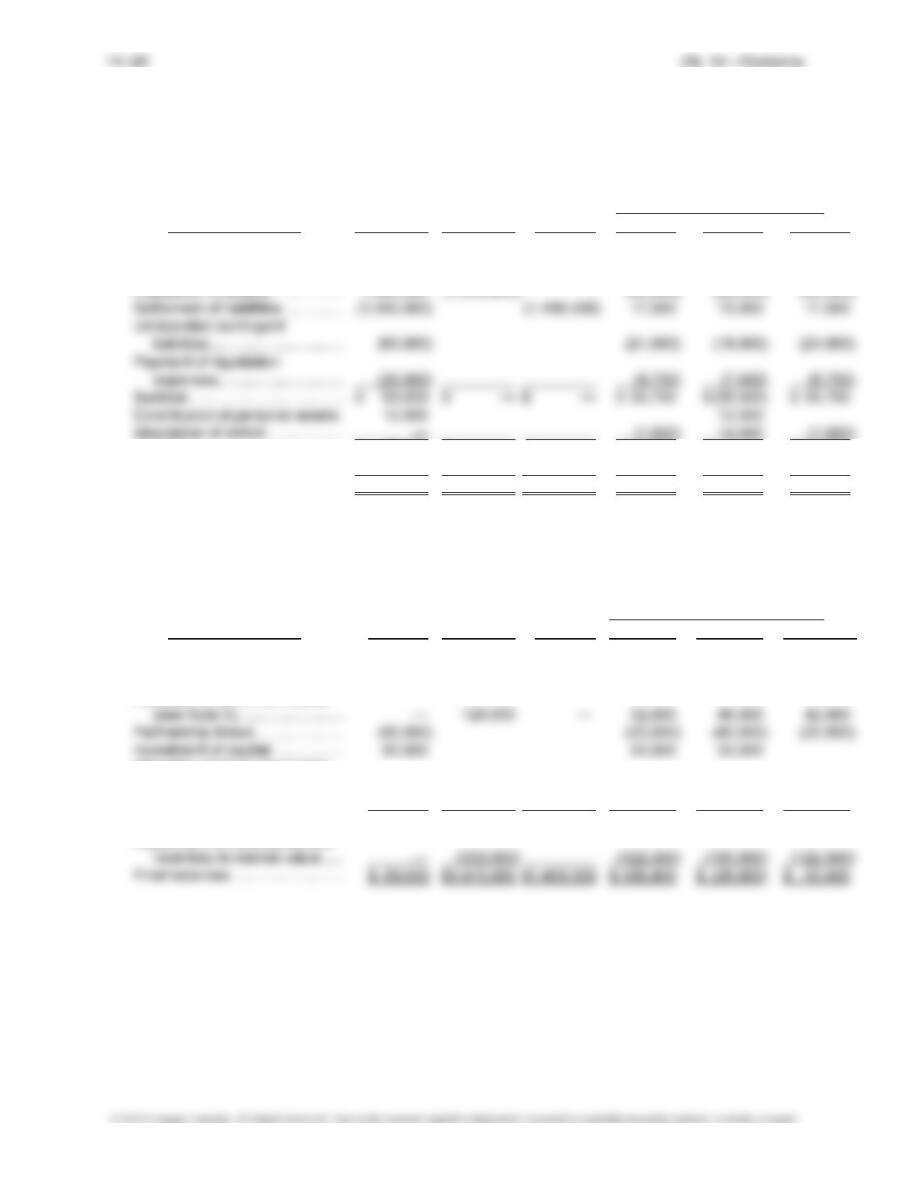

14–19 Ch. 14—Problems

Problem 14-4, Continued

Schedule A

Allocation of Profits and Losses

Cumulative

2013 Income Davis Murray Clay Rayburn Total

Profit and loss percentages … 33.3% 33.3% 33.3%

Salaries …………………………… $100,000 $100,000 $ 70,000 $270,000

2014 Income

Salaries …………………………… $100,000 $100,000 $70,000 270,000

Bonus (see Note B) …………… 6,000 276,000

Remaining profits ……………… 8,000 8,000 8,000 300,000

Total ……………………………….. $108,000 $108,000 $84,000

2015 Income

Salaries …………………………… $50,000 $50,000 $35,000 $ 0 135,000

Interest ……………………………. 5,900 140,900

Bonus (see Note C) …………… 1,100 142,000

Remaining profits ……………… 0 0 0 142,000

Note B: Bonus = 20% (Net Income – Salaries)

Bonus = 20% ($300,000 – $270,000)

Bonus = 20% ($30,000)

Bonus = $6,000

Note C: Bonus = 20% (Net Income – Salaries)

Problem 14-4, Concluded

Schedule B

Changes in Partnership Interests

Admission of Rayburn:

Total capital of previous partners ………………………………………………….. $ 78,800

Investment of Rayburn ………………………………………………………………… 59,000

(2) Distribution of Available Cash on September 15, 2016

Cash

Liabilities Murray Clay Rayburn

Available cash (see Schedule C) …… $ 277,000

Payment of liabilities ……………………. (84,000) $84,000

Payment to partners (see Note D) …. (183,000) $112,908 $1,908 $68,184

Total ………………………………………….. $ 10,000 $84,000 $112,908 $1,908 $68,184

Schedule C

Partial Liquidation Schedule

Noncash Loan from Capital Balances

Cash

Assets Liabilities Murray Murray Clay Rayburn

Balances at June 30, 2016 ….. $ 15,000 $433,100 $84,000 $50,000 $135,348 $74,348 $104,404

August 1 sale of assets ………. 180,000 (220,000) (16,000) (16,000) (8,000)

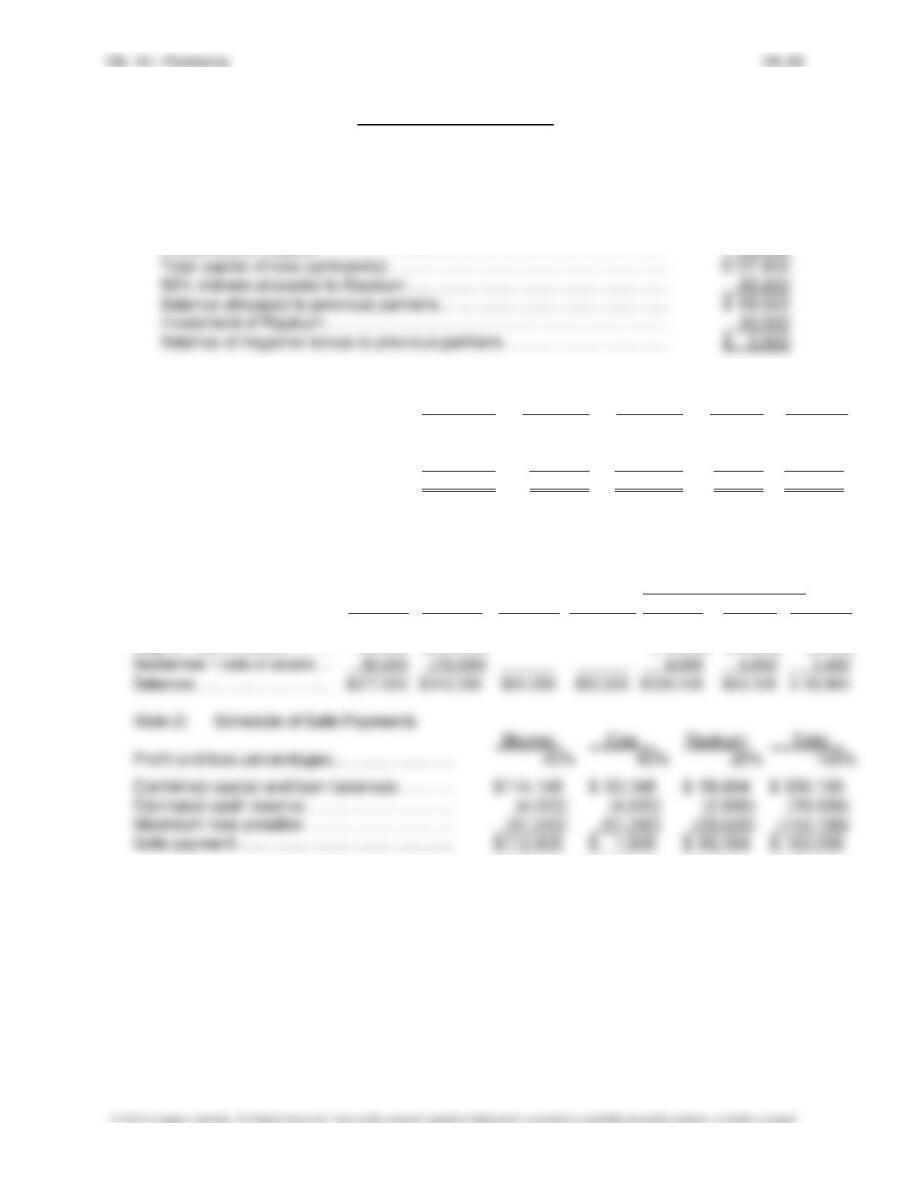

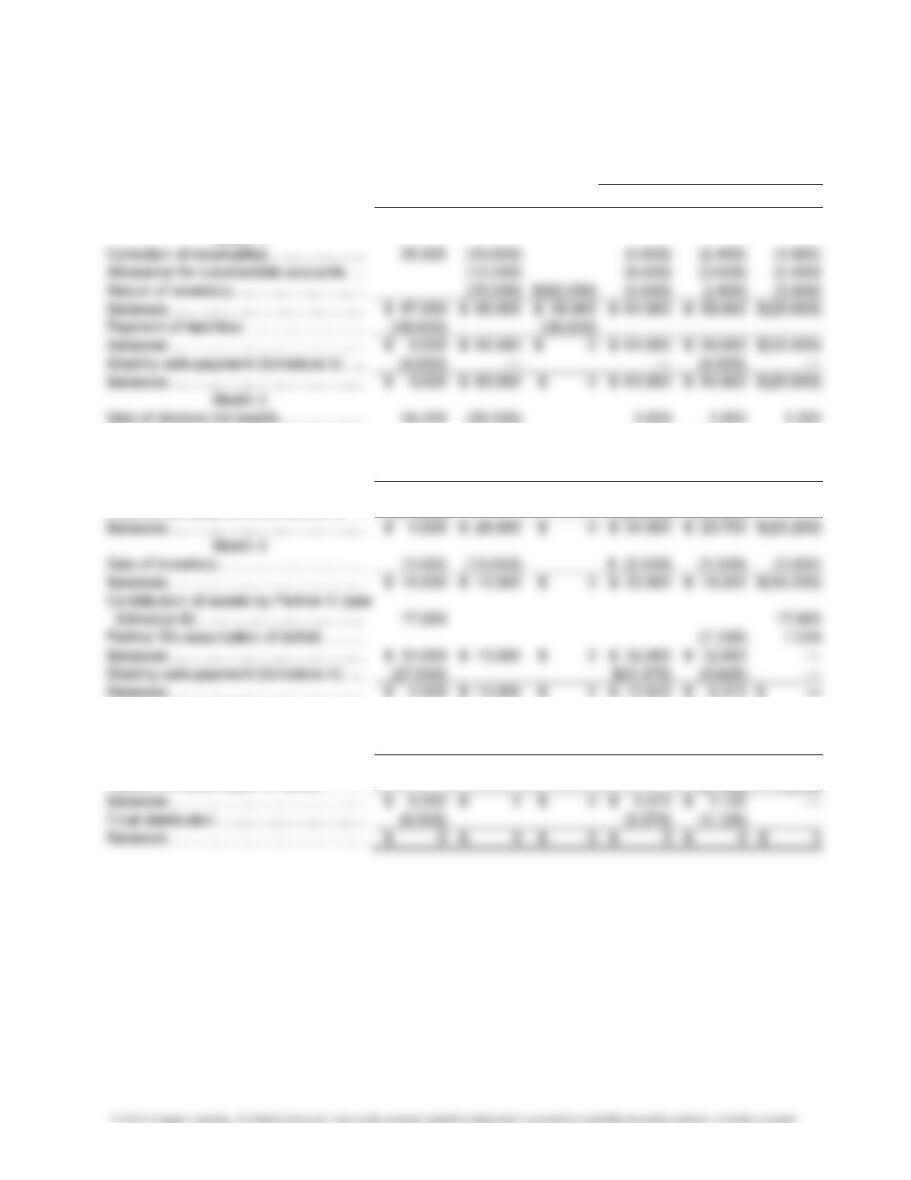

PROBLEM 14-5

If the partnership is liquidated, Jacobs’ capital balance and resulting distribution will be as follows:

Noncash Combined Loan and Capital Balances

Cash

Assets Liabilities Jacobs Williams Harrington

Profit and loss percentages ……………….. 30% 30% 40%

Beginning balances …………………………… $ (15,000) $ 322,000 $ 160,000 $ 52,000 $ 65,000 $ 30,000

Discovery of liabilities ………………………… 12,000 (3,600) (3,600) (4,800)

Sale of assets ………………………………….. 232,000 (322,000) (27,000) (27,000) (36,000)

Payment of liabilities …………………………. (172,000) (172,000)

If the offer by Williams is accepted, the amount received by Jacobs will be determined as follows:

Noncash Combined Loan and Capital Balances

Cash

Assets Liabilities Jacobs Williams Harrington

Profit and loss percentages ……………….. 30% 30% 40%

Problem 14-5, Concluded

Payment due Jacobs:

Capital balance ………………………………………….. $ 31,000

Percent to be paid ………………………………………. 50%

Total payment ……………………………………………. $ 15,500

Less down payment ……………………………………. (3,100)

Remaining balance …………………………………….. $ 12,400

14–23 Ch. 14—Problems

PROBLEM 14-6

Capital Balances

Murphy

Reinartz Hepburn Pioso Total

Balance as of

December 31, 2015 ……….. $ 54,000 $ 76,000 $ — $ — $ 130,000

Year-end balance ………………. $ 176,850 $ 117,275 $ 75,875 $ 0 $ 370,000

2018 Beginning balance ……………… $ 176,850 $ 117,275 $ 75,875 $ — $ 370,000

Sale of interest to Reinartz ….. (176,850) 176,850 —

Allocation of profits

(see Note A) ………………….. — 100,000 100,000 200,000

Ending balance …………………. $ 0 $ 0 $112,500 $ 75,000 $ 187,500

Note A:

Cumulative

2016 Allocation Profit Murphy

Reinartz Total

Profit and loss percentages ……………………….. 40% 60%

Problem 14-6, Concluded

Cumulative

2017 Allocation Murphy Reinartz Hepburn Total

Profit and loss percentages .. 30% 45% 25%

Salary …………………………….. $ 80,000 $100,000 $70,000 $250,000

Partner Income Income Bonus

Murphy 20% $230,000 $46,000

2017 Bonus

Percent of

Partner Income Income Bonus

Note C: Admission of Hepburn: If Hepburn paid $70,000 for a 25% interest in capital, this

would suggest that the new partnership had a value of $280,000. This value exceeds

the capital of the old partnership ($160,000) plus the investment of the new partner

($70,000). Therefore, goodwill of $50,000 [$280,000 – ($160,000 + $70,000)] is tra-

ceable to the original partnership. The goodwill is allocated to the original partners per

their profit percentages.

Admission of Pioso: If Pioso paid $75,000 for a 40% interest in capital, this would

suggest that the new partnership had a value of $187,500. This value exceeds the

capital of the old partnership ($90,875) plus the investment of the new partner

PROBLEM 14-7

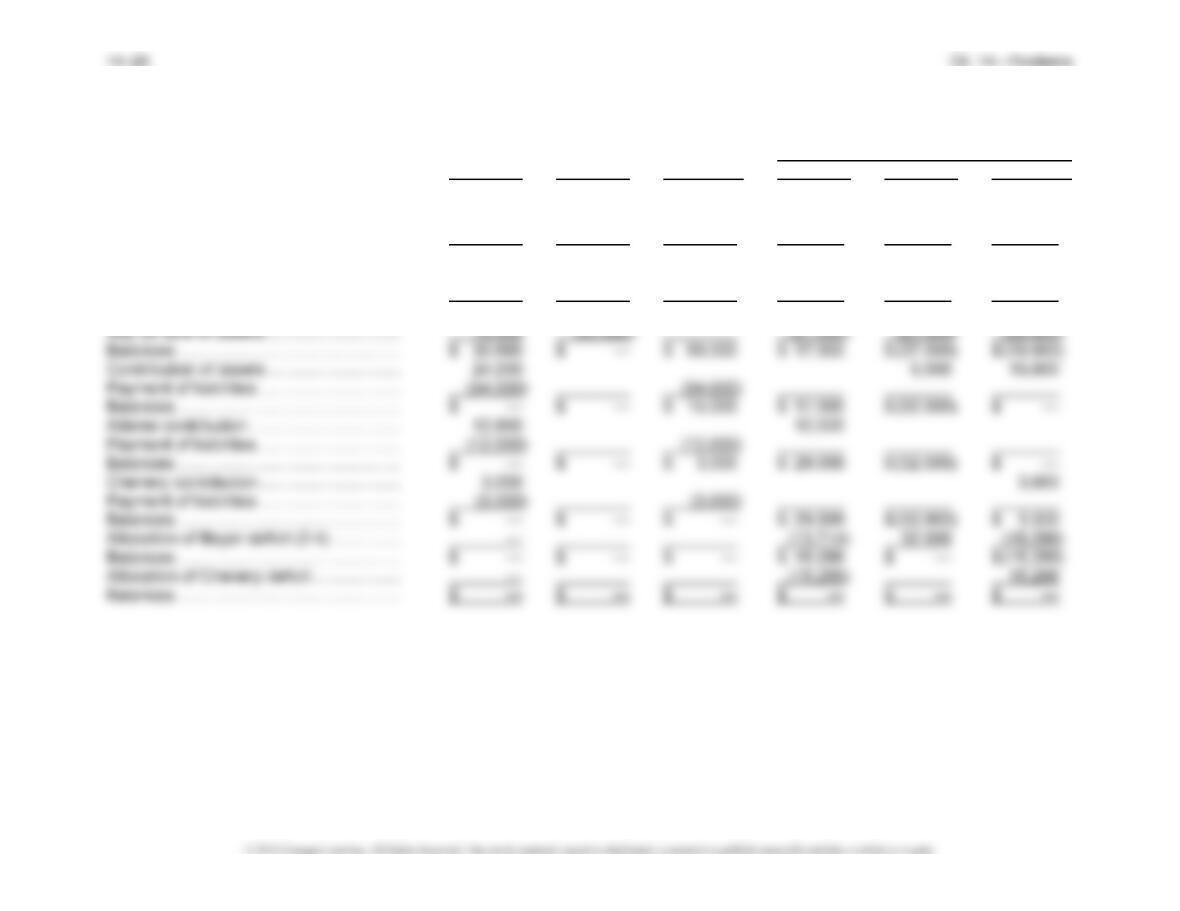

If the partnership were liquidated on March 31, 2016, Klaproth would receive $48,750, determined as

follows:

Noncash Partner’s Capital Balances

Event/Circumstance Cash Assets Liabilities Klaproth Stone Jackson

Profit and loss percentages ……. 35% 30% 35%

Beginning balances ………………. $ 120,000 $1,500,000 $1,400,000 $110,000 $ 20,000 $ 90,000

Subtotal ……………………………….. $ 77,500 $ — $ — $ 48,750 $ — $ 28,750

Final payment to partners ………. (77,500) — — (48,750) — (28,750)

Final balances ………………………. $ — $ — $ — $ — $ — $ —

If Klaproth continued in the partnership until March 31, 2018, he would receive draws of $20,000 and

a final payment of $117,040 (110% of final capital balance of $106,400) less an investment of

$50,000, determined as follows:

Noncash Partner’s Capital Balances

Event/Circumstance Cash Assets Liabilities Klaproth Stone Jackson

Profit and loss percentages ……. 35% 30% 35%

Beginning balances ………………. $120,000 $1,500,000 $1,400,000 $ 110,000 $ 20,000 $ 90,000

Allocation of 2016 net income

Allocation of 2017 net income

(see Note B) …………………….. — 200,000 56,900 62,200 80,900

Partnership draws …………………. (60,000) — (40,000) (20,000)

Subtotal ……………………………….. $ 60,000 $1,820,000 $1,400,000 $ 228,900 $ 78,200 $ 172,900

Adjustment of receivables and

Problem 14-7, Concluded

Note A:

Cumulative

Allocation of 2016 income: Klaproth Stone Jackson Total

Profit and loss percentages ……. 35% 30% 35%

Salary ………………………………….. $100,000 $130,000 $ 90,000 $320,000

Bonus as a percent of sales ……. 30,000 — 50,000 400,000

14–27 Ch. 14—Problems

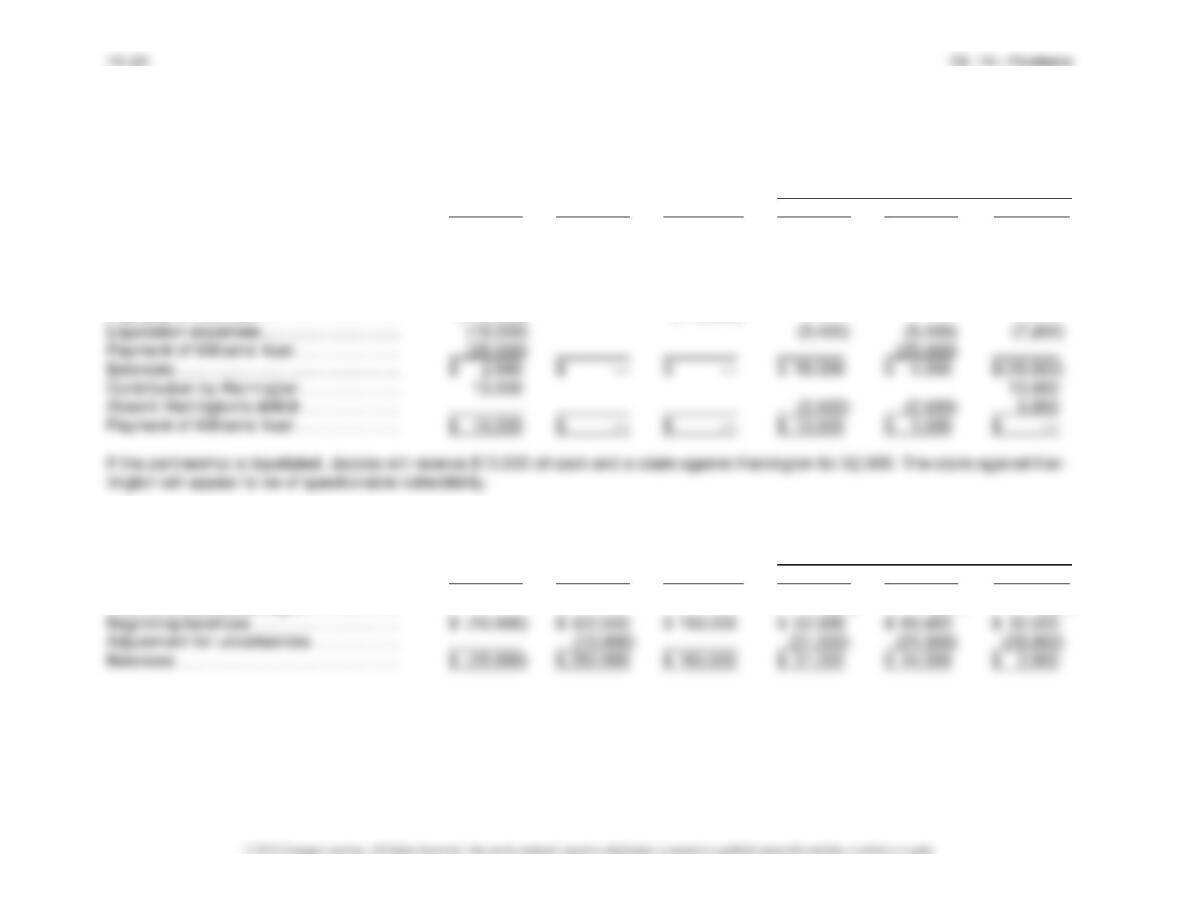

PROBLEM 14-8

Noncash Combined Capital and Loans

Cash Assets Liabilities Partner A Partner B Partner C

Beginning balances …………………………. $ 12,000 $210,000 $100,000 $ 75,000 $ 67,000 $(20,000)

Month 1

Satisfaction of Partner B note payable .. (15,000) 5,000 (22,000) 2,000

Customer sale ………………………………… 16,000 (14,000) 1,000 600 400

Payment of liquidation expenses ………. (6,000) (3,000) (1,800) (1,200)

Balances………………………………………… $ 49,000 $ 28,000 $ 0 $ 67,000 $ 33,200 $(23,200)

Monthly safe payment (Schedule A) …. (45,000) (32,500) (12,500) —

Month 4

Sale of remaining assets ………………….. 7,000 (13,000) (3,000) $ (1,800) (1,200)

Payment of liquidation expenses ………. (4,500) (2,250) $ (1,350) $(900)

Balances………………………………………… $ 6,500 $ 0 $ 0 $ 5,375 $ 3,225 $ (2,100)

Partner B’s assumption of deficit ……….. (2,100) 2,100

Problem 14-8, Concluded

Schedule A

Schedule of Safe Payments

Partner A Partner B Partner C Total

Profit and loss percentages………………………….. 50% 30% 20% 100%

Safe payment …………………………………………….. $ 0 $ 4,000 $ 0 $ 4,000

Month 2

Combined capital and loan balances …………….. $ 67,000 $ 33,200 $(23,200) $ 77,000

Estimated liquidation expenses and/or

adjustment to minimum cash balance ………… (2,000) (1,200) (800) (4,000)

Maximum loss possible ……………………………….. (6,500) (3,900) (2,600) (13,000)

Balances……………………………………………………. $ 23,500 $ 6,900 $ (3,400) $ 27,000

Allocation of debit capital balances ……………….. (2,125) (1,275) 3,400 —

Safe payment …………………………………………….. $ 21,375 $ 5,625 $ 0 $ 27,000

Schedule B

PROBLEM 14-9

Other Partner’s Capital Balance

Cash

Assets Liabilities Adams Beyer Chenery

Profit and loss percentages ……………….. 30% 30% 40%

Beginning balances …………………………… $ 25,000 $ 240,000 $ 200,000 $ 50,000 $ (10,000) $ 25,000

June 30 sale of assets ………………………. 120,000 (160,000) (12,000) (12,000) (16,000)

Balances …………………………………………. $ 145,000 $ 80,000 $ 200,000 $ 38,000 $ (22,000) $ 9,000

Contribution of assets ……………………….. 6,000 6,000

Payment of liabilities …………………………. (131,000) (131,000)

Balances …………………………………………. $ 20,000 $ 80,000 $ 69,000 $ 38,000 $ (16,000) $ 9,000

Problem 14-9, Concluded

Allocation of Adams’ personal assets:

Personal liabilities …………………………………………………………… $22,500 60%

Unsatisfied partnership creditors ………………………………………. 15,000 40

Total claims against personal assets …………………………………. $37,500 100%