CHAPTER 14 Statement of Cash Flows

Prob. 14–2B (Concluded)

Balance Balance

Account Title Dec. 31, 2013 Dec. 31, 2014

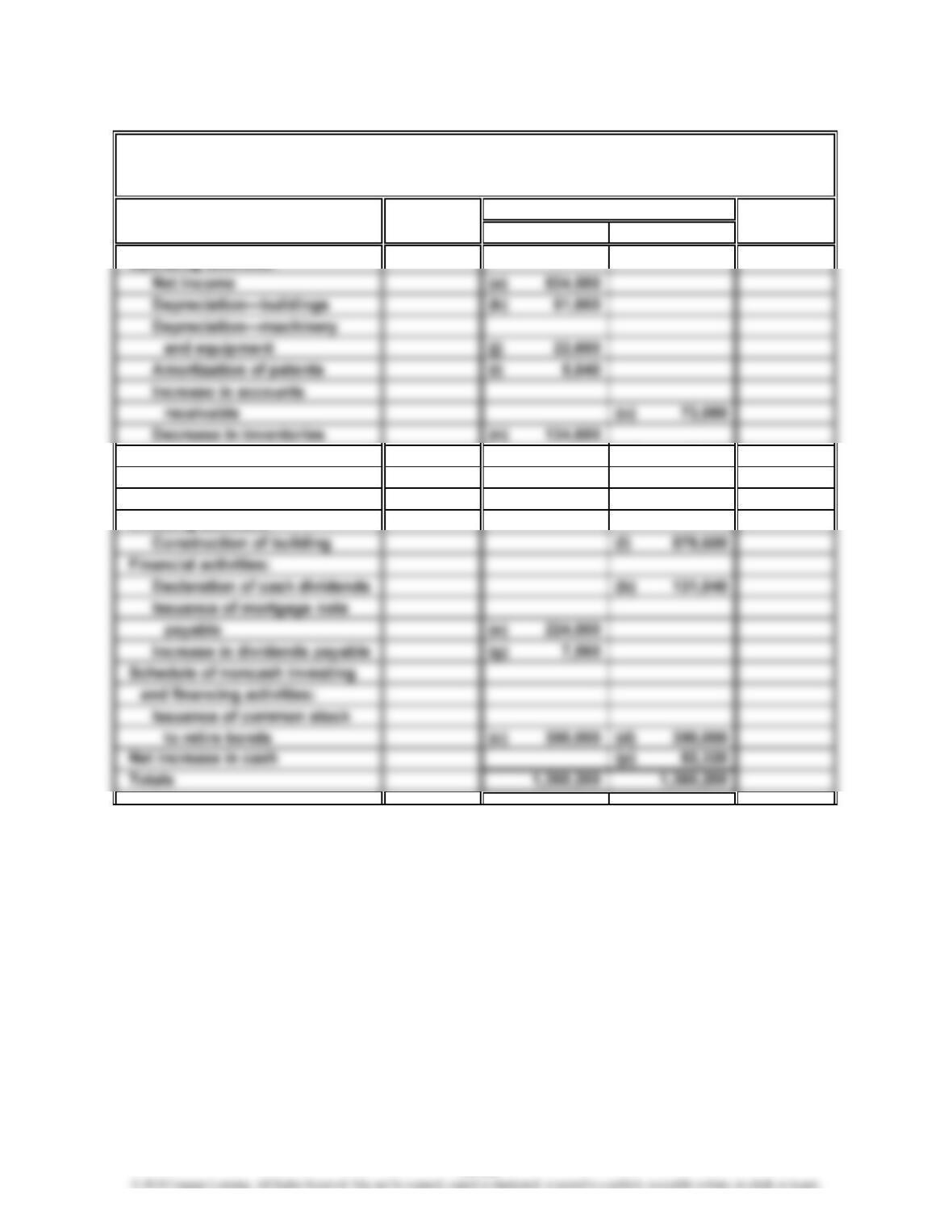

Operating activities:

Increase in prepaid expenses (m) 6,440

Decrease in accounts payable (h) 89,600

Decrease in salaries payable (f) 8,120

Investing activities:

Debit Credit

HARRIS INDUSTRIES INC.

Spreadsheet (Work Sheet) for Statement of Cash Flows

For the Year Ended December 31, 2014

Transactions

14-34

CHAPTER 14 Statement of Cash Flows

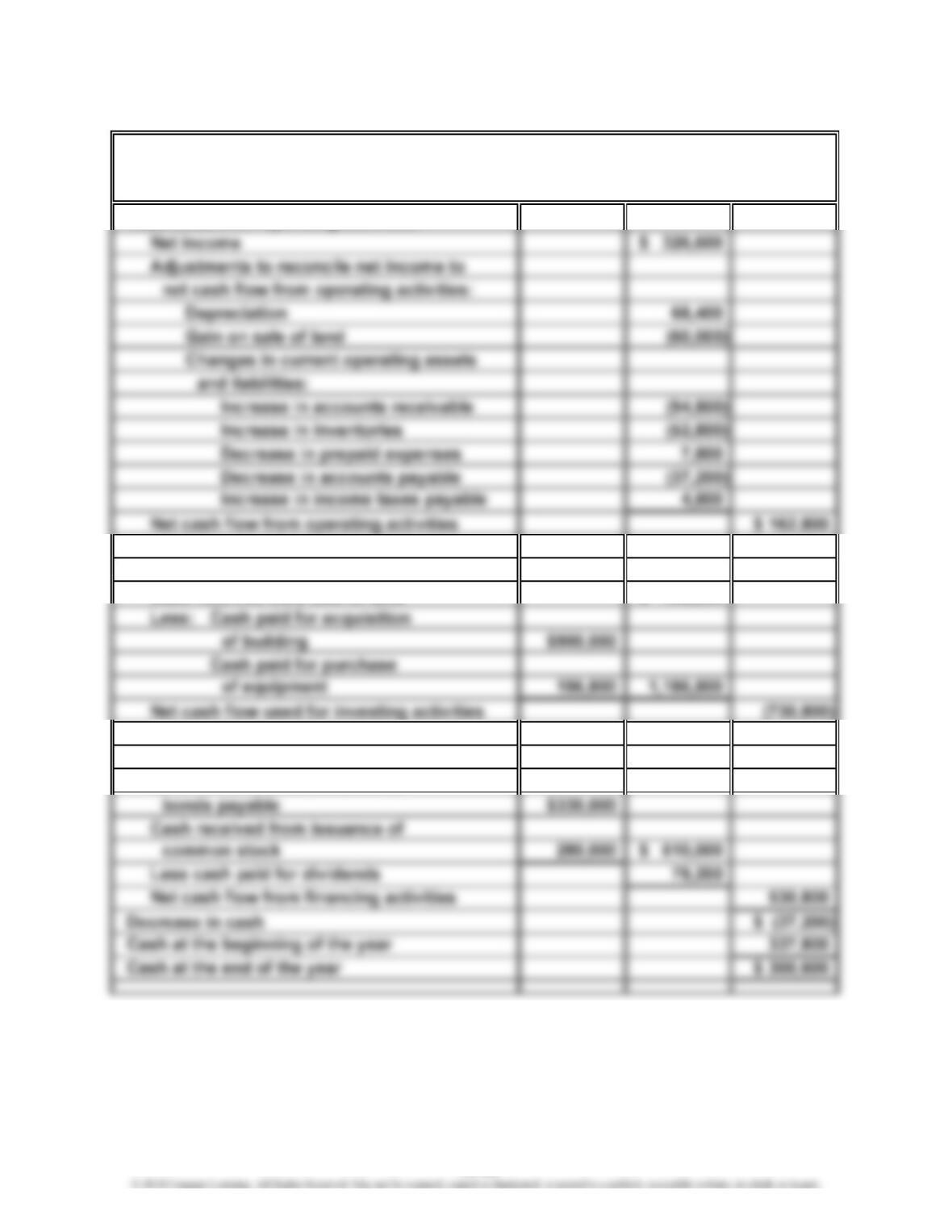

Prob. 14–3B

Cash flows from operating activities:

Cash flows from investing activities:

Cash received from sale of land $ 456,000

Cash flows from financing activities:

Cash received from issuance of

For the Year Ended December 31, 2014

COULSON INC.

Statement of Cash Flows

14-35

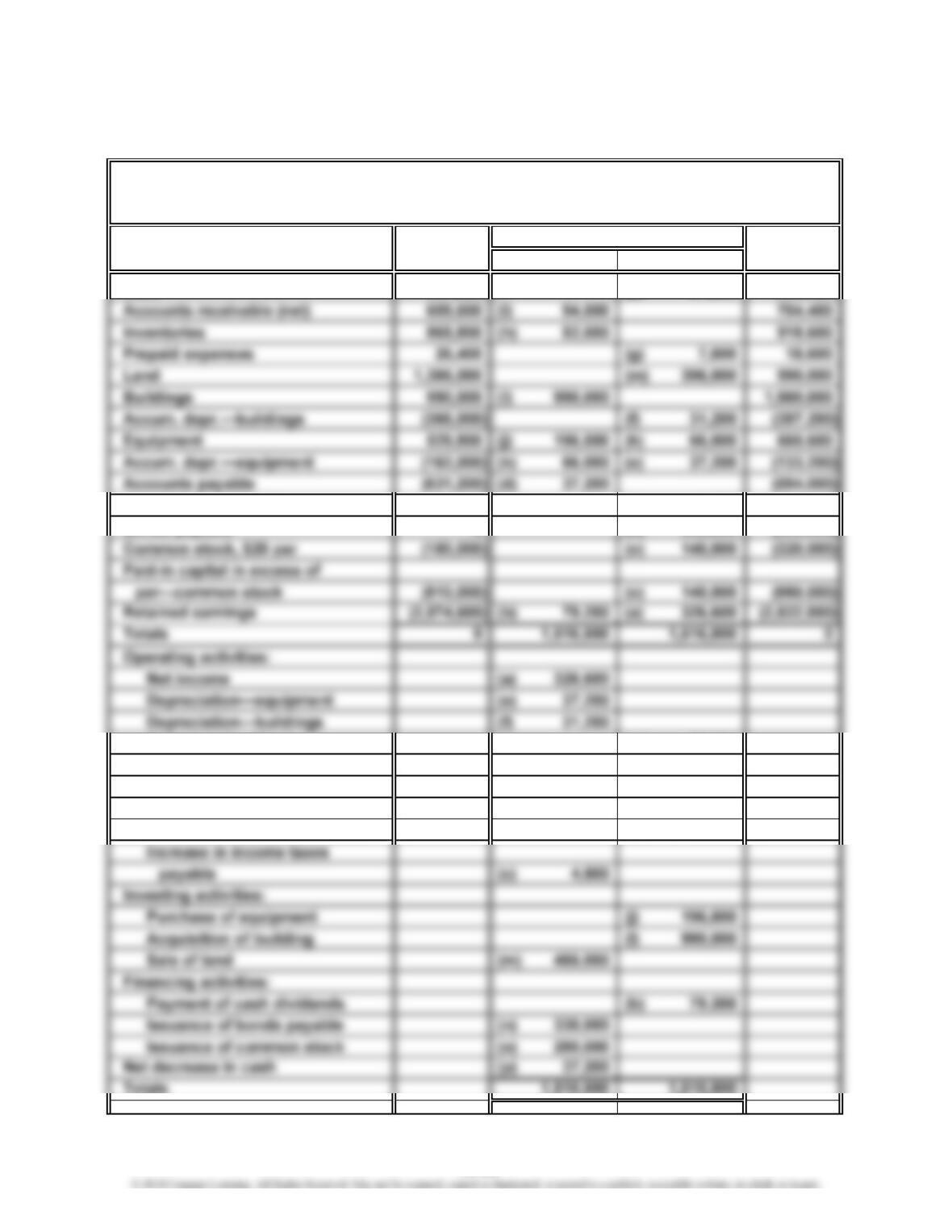

CHAPTER 14 Statement of Cash Flows

Prob. 14–3B (Concluded)

(Optional)

Balance Balance

Account Title Dec. 31, 2013 Dec. 31, 2014

Cash 337,800 (p) 37,200 300,600

Income taxes payable (21,600) (c) 4,800 (26,400)

Bonds payable 0 (n) 330,000 (330,000)

Gain on sale of land (m) 60,000

Increase in accts. receivable (i) 94,800

Increase in inventories (h) 52,800

Decrease in prepaid expenses (g) 7,800

Decrease in accounts payable (d) 37,200

Debit Credit

COULSON INC.

Spreadsheet (Work Sheet) for Statement of Cash Flows

For the Year Ended December 31, 2014

Transactions

14-36

CHAPTER 14 Statement of Cash Flows

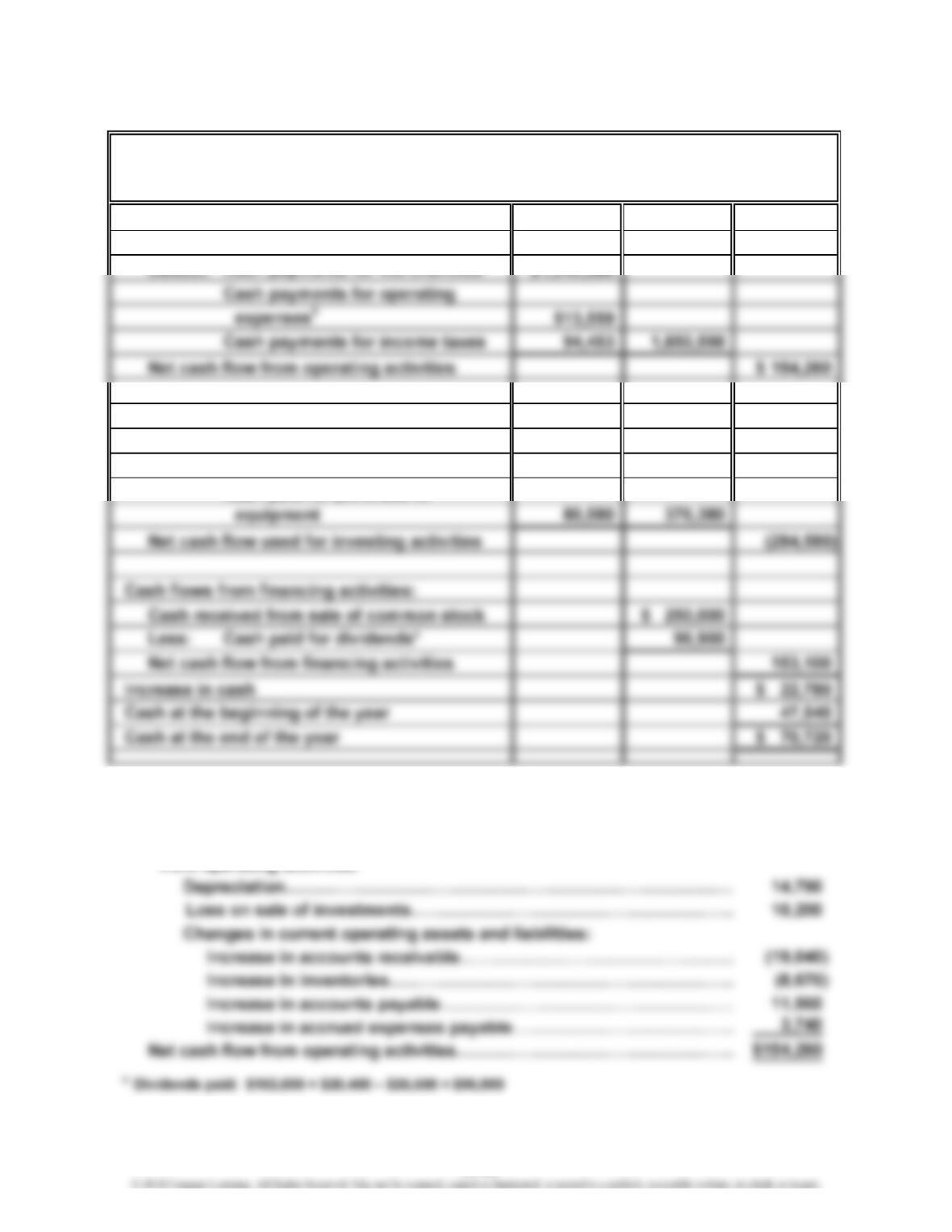

Prob. 14–4B

Cash flows from operating activities:

Cash flows from investing activities:

Cash received from sale of investments $ 588,000

Less: Cash paid for land $ 960,000

Cash paid for equipment 240,000 1,200,000

Net cash flow used for investing activities (612,000)

Cash flows from financing activities:

Reconciliation of Net Income with Cash Flows from Operating Activities:

Net income……………………………………………………………………………

…

$ 558,960

Adjustments to reconcile net income to net cash flow

from operating activities:

For the Year Ended December 31, 2014

MARTINEZ INC.

Statement of Cash Flows

14-37

CHAPTER 14 Statement of Cash Flows

Prob. 14–4B (Concluded)

Computations:

1. Sales………………………………………………………………………………… $4,512,000

2. Cost of merchandise sold………………………………………………………

…

$2,352,000

3. Operating expenses other than depreciation………………………………

…

$1,344,840

14-38

CHAPTER 14 Statement of Cash Flows

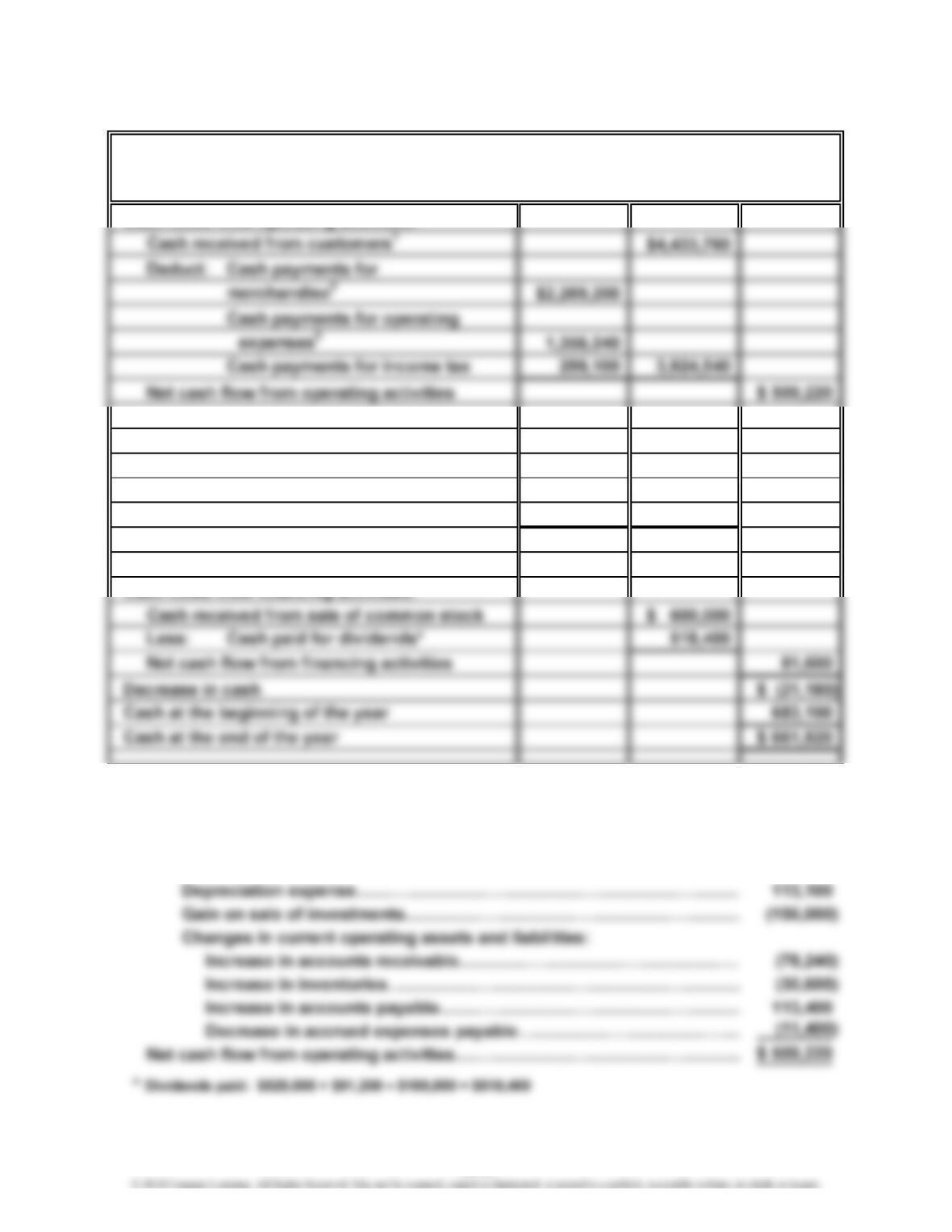

Prob. 14–5B

Cash flows from operating activities:

Cash received from customers1$2,004,858

Cash flows from investing activities:

Cash received from sale of investments $ 91,800

Less: Cash paid for purchase of land $ 295,800

Cash paid for purchase of

Reconciliation of Net Income with Cash Flows from Operating Activities:

Net income……………………………………………………………………………

…

$141,680

Adjustments to reconcile net income to net cash flow

from operating activities:

For the Year Ended December 31, 2014

MERRICK EQUIPMENT CO.

Statement of Cash Flows

14-39

CHAPTER 14 Statement of Cash Flows

Prob. 14–5B (Concluded)

Computations:

1. Sales…………………………………………………………………………………

…

$2,023,898

2. Cost of merchandise sold………………………………………………………

…

$1,245,476

3. Operating expenses other than depreciation………………………………

…

$ 517,299

14-40

…

CHAPTER 14 Statement of Cash Flows

CP 14–1

Although this situation might seem harmless at first, it is actually a violation of

generally accepted accounting principles. The operating cash flow per share figure

should not be shown on the face of the income statement. The income statement is

CP 14–2

Start-up companies are unique in that they frequently will have negative retained

earnings and operating cash flows. The negative retained earnings are often due to

losses from high start-up expenses. The negative operating cash flows are typical

because growth requires cash. Growth must be financed with cash before the cash

CASES & PROJECTS

14-41

CP 14–3

a. 1. Normal practice for determining the amount of cash flows from operating

activities during the year is to begin with the reported net income. This net

income must ordinarily be adjusted upward and/or downward to determine the

2. Generally accepted accounting principles require that significant transactions

affecting future cash flows should be reported in a separate schedule to the

3. The $180,000 cash received from the sale of the investments is reported in the

Cash Flows from Investing Activities section. Since the net income included a

4. The balance sheets for the last two years will indicate the increase in cash but

will not indicate the firm’s activities in meeting its financial obligations, paying

dividends, and maintaining and expanding operating capacity. Such information,

as provided by the statement of cash flows, assists creditors in assessing the

CP 14–4

The senior vice president is very focused on profitability but has been bleeding cash.

The increase in accounts receivable and inventory is striking. Apparently, the new

credit card campaign has found many new customers, since the accounts receivable is

growing. Unfortunately, it appears as though the new campaign has done a poor job of

14-43

CHAPTER 14 Statement of Cash Flows

CP 14–5

a. and b.

Recent statements of cash flows for Johnson & Johnson and JetBlue Airways

Johnson & Johnson

Johnson & Johnson (J&J) is a powerful generator of cash flows from operating

activities, with almost $14.3 billion in cash flow from operations. This is enough to

JetBlue Airways Corp.

JetBlue is weaker than J&J. JetBlue had cash flows from operating activities of

14-44

CHAPTER 14 Statement of Cash Flows

CP 14–5 (Continued)

In Millions For Period Ended December 31, 2011 12/31/11

CASH FLOWS FROM OPERATING ACTIVITIES:

Net earnings $ 9,672

Adjustments to reconcile net earnings to cash flows:

Depreciation and amortization of property and intangibles 3,158

CASH FLOWS FROM INVESTING ACTIVITIES:

Additions to property, plant and equipment $ (2,893)

CASH FLOWS FROM FINANCING ACTIVITIES:

Dividends to shareholders $ (6,156)

Repurchase of common stock (2,525)

Proceeds from short-term debt 9,729

Retirement of short-term debt (11,200)

Consolidated Statements of Cash Flows

JOHNSON & JOHNSON

14-45

CHAPTER 14 Statement of Cash Flows

CP 14–5 (Concluded)

In Millions For Period Ended December 31, 2011 12/31/11

Cash Flow from Operating Activities:

Changes in certain operating assets and liabilities:

Decrease (increase) in receivables (10)

Cash Flow from Investing Activities:

Capital expenditures, including purchase deposits on flight equipment $(525)

Net decrease in short-term investments 24

Cash Flow from Financing Activities:

Proceeds from:

Issuance of common stock $ 10

Repayment of:

Long-term debt and capital lease obligations (238)

JETBLUE AIRWAYS CORP.

Consolidated Statements of Cash Flows

14-46