CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

Prob. 28–2A (FIN MAN); Prob. 14–2A (MAN) (Concluded)

Cost makeup of Procedure 2:

Labor (55%) ………………………………………………

$170,500

Materials (25%) …………………………………………

Overhead (20%) ………………………………………..

$310,000

3.

Current total cost of production (P1 + P2) ………..

$930,000

Less target total cost of production…………………

(900,000)

P2 materials cost savings needed …………………..

$ 30,000

Current P2 overhead materials

$ 37,200

Less P2 overhead materials cost

Maximum new cost of P2 overhead

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

Prob. 28–3A (FIN MAN); Prob. 14–3A (MAN)

1. The data show that while the online customer survey score increased (from 8.5 to

9.2), the company’s market share decreased (from 12.3% to 10.5%). This does not

2. Three possible reasons for the unsupported relationship between the online

customer survey score and market share are as follows:

Reason 1: Satisfying the customer has no effect on increasing market share.

3. Reasons 1 and 2 do not seem logical. Customer satisfaction (Reason 1) should lead

to an increase in customers, sales, and market share. Likewise, market share

(Reason 2) is a direct measure of increasing market share. This leaves as the most

likely reason that the online customer survey rating (Reason 3) is a poor metric for

increasing market share. These findings are summarized as follows:

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

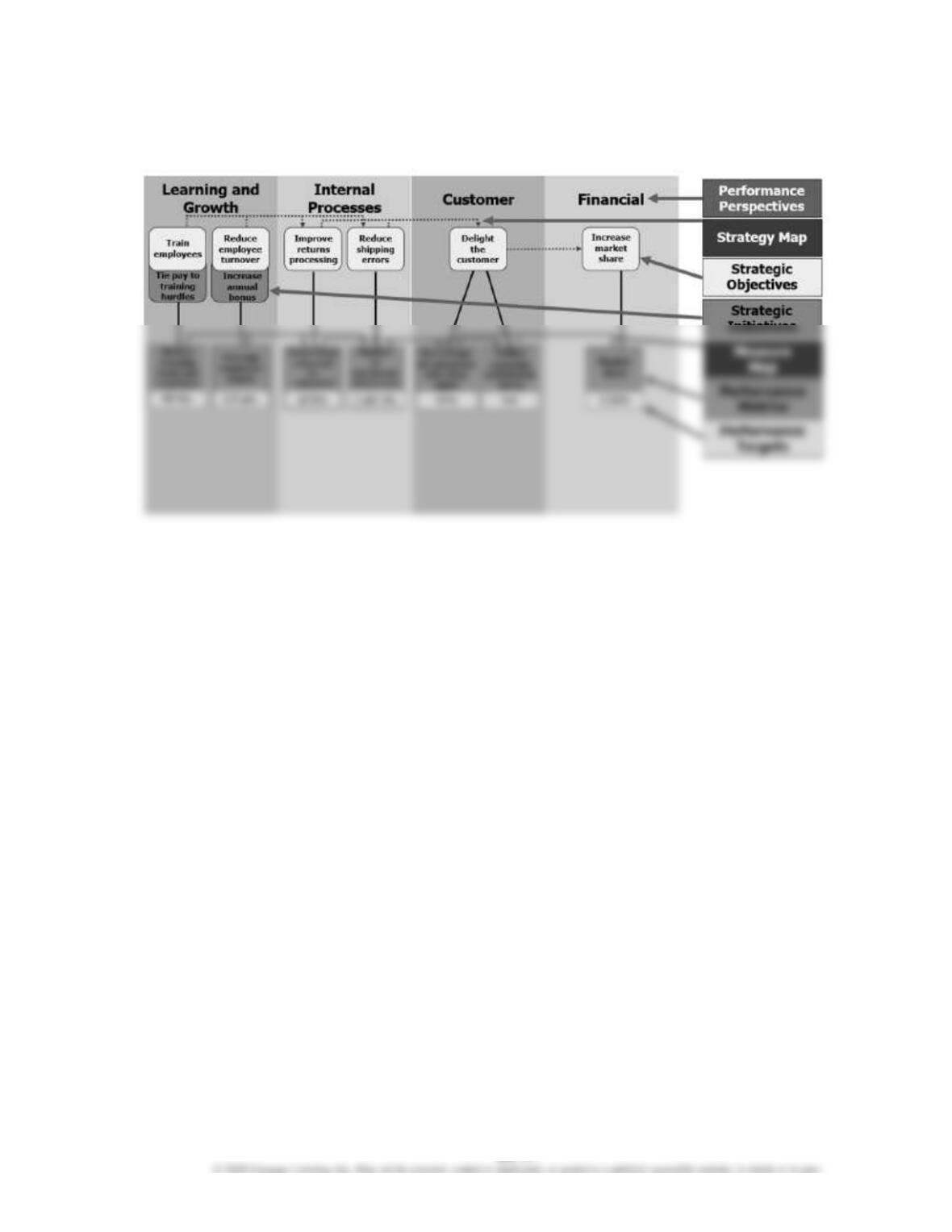

Prob. 28–1B (FIN MAN); Prob. 14–1B (MAN)

1.–3.

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

Prob. 28–2B (FIN MAN); Prob. 14–2B (MAN)

1.

Target gross profit percentage …………………..

30% of sales

Total cost of production percentage …………..

70% of sales

Total sales ……………………………………………….

$600,000

Total cost of production percentage ………….

× 70%

Target cost of production ………………………….

$420,000

P1 = 2(P2) = (2 × $140,000) = $280,000

Cost makeup of Procedure 1:

Labor (40%) …………………………………………

$112,000

Materials (45%) ……………………………………

126,000

Overhead (15%) …………………………………..

42,000

Total …………………………………………………..

$280,000

Cost makeup of Procedure 2:

Labor (60%) …………………………………………

Materials (30%) ……………………………………

Overhead (10%) …………………………………..

Total …………………………………………………..

$140,000

2.

Labor cost of Procedure 1 …………………………

$114,000

Labor cost = 40% of P1, so

P1 = $114,000 ÷ 40% =

$285,000

Procedure 1 cost twice as much

Cost makeup of Procedure 1:

Labor (40%) …………………………………………

$114,000

Materials (45%) ……………………………………

Overhead (15%) …………………………………..

Total ……………………………………………………

$285,000

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

Prob. 28–2B (FIN MAN); Prob. 14–2B (MAN) (Concluded)

Cost makeup of Procedure 2:

Labor (60%) ……………………………………………..

$ 85,500

Materials (30%) …………………………………………

42,750

Overhead (10%) ………………………………………..

14,250

Total …………………………..…………………………...

$142,500

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

Prob. 28–3B (FIN MAN); Prob. 14–3B (MAN)

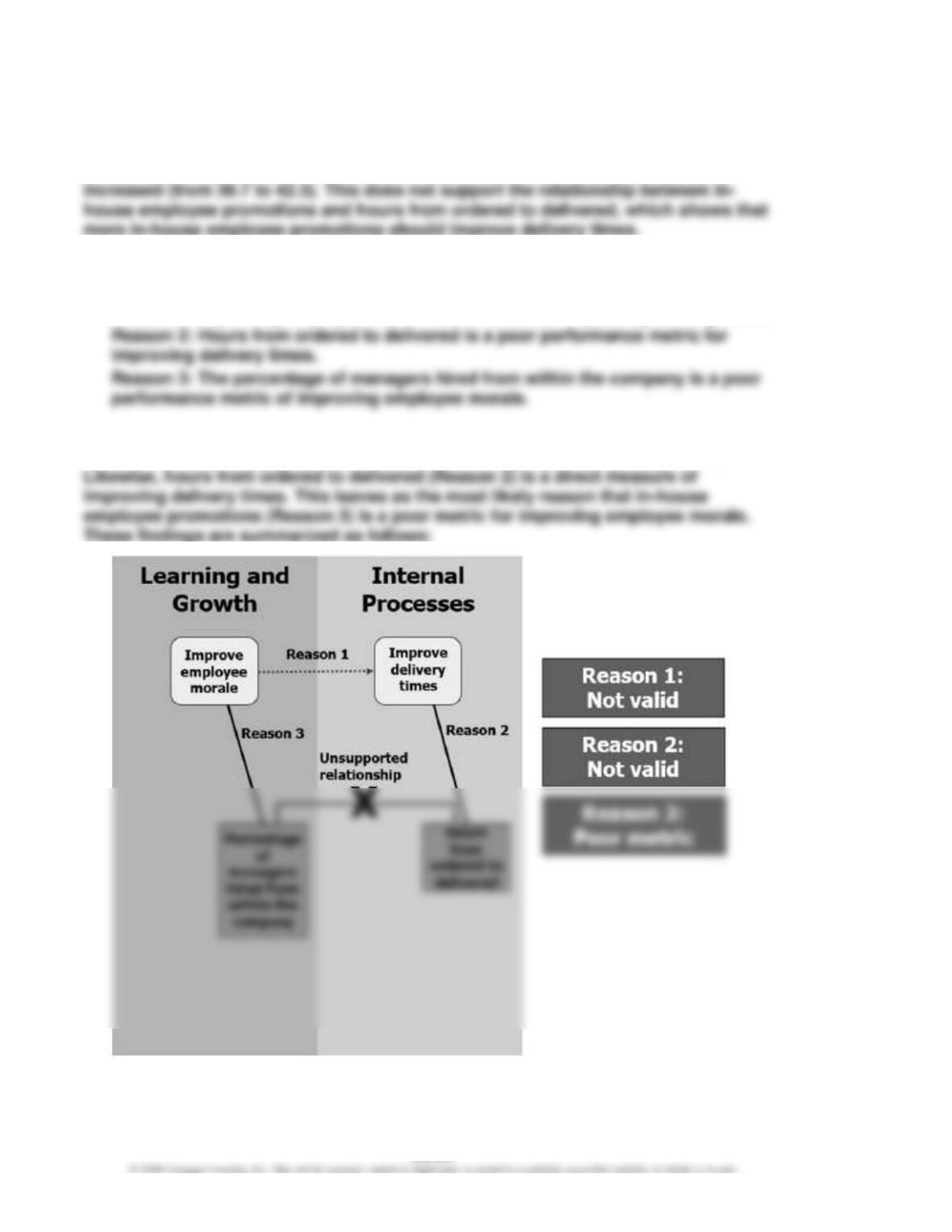

1. The statistics show that while the percentage of management hired from within the

company increased (from 7% to 10%), the hours from ordered to delivered also

2. Three possible reasons for the unsupported relationship between in-house

employee promotions and hours from ordered to delivered are the following:

Reason 1: Improving employee morale has no effect on improving delivery times.

3. Reasons 1 and 2 do not seem logical. Higher employee morale (Reason 1) should

lead to improved employee performance, and thereby improved delivery times.

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

MAKE A DECISION

MAD 28–1 (FIN MAN); MAD 14–1 (MAN)

a.

Lifetime cost to replace each HID fixture with LED ………………………….

$ 500

Number of fixtures ………………………………………………………………………..

× 700

Investment cost ……………………………………………………………………………

$350,000

b.

HID kilowatt-hour consumption per fixture ……………………………………..

0.5*

LED kilowatt-hour consumption per fixture …………………………………….

*

500 watts ÷ 1,000 watts = 0.5 kilowatt

**

300 watts ÷ 1,000 watts = 0.3 kilowatt

c.

Annual net cash flow savings from installing LED …………………………..

$ 46,200

Present value factor for an annuity of $1 at 8% for 15 periods ………….

Present value of annual savings (rounded) …………………………………….

Amount to be invested ………………………………………………………………….

(350,000)

Net present value ………………………………………………………………………….

MAD 28–2 (FIN MAN); MAD 14–2 (MAN)

a. Both CSR initiatives best fit under the internal processes performance perspective.

b.

Replacing old fans initiative:

Cost of each new fan ……………………………………………………………….

$ 750

Cost of replacing each old fan with new fan ………………………………

100

Number of units ………………………………………………………………………

Initial investment cost ……………………………………………………………..

Replacing ATVs initiative:

Cost of new electric-powered ATV per unit ………………………………..

Number of units (ATVs) ……………………………………………………………

Total cost of replacing each old fan with new fan ………………………

$ 850

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

MAD 28–2 (FIN MAN); MAD 14–2 (MAN) (Concluded)

c.

Replacing old fans initiative:

Old fan kilowatt-hour consumption per unit……………………………….

0.8*

Kilowatt-hour savings per unit ………………………………………………….

Number of operating hours per day …………………………………………..

Number of operating days per year …………………………………………..

Number of units ……………………………………………………………………….

Kilowatt-hour savings per year …………………………………………………

Metered utility rate per kwh ………………………………………………………

Annual utility cost savings ……………………………………………………….

New fan kilowatt-hour consumption per unit ……………………………..

(0.5)**

* 800 watts ÷ 1,000 watts = 0.8 kilowatt

** 500 watts ÷ 1,000 watts = 0.5 kilowatt

Replacing ATVs initiative:

Fuel, repair, other cost savings per ATV per hour of use ……………

$ 1.70

Number of operating days per year per ATV ………………………………

Annual cost savings per ATV ……………………………………………………

Number of ATVs ………………………………………………………………………

d. Replacing old fans initiative:

Initial Investment Cost

Annual Utility Cost Savings

=

Years before Initiative Pays Off Initial

Investment Cost

$68,000

$3,456

=

19.68

Years before Initiative Pays Off Initial

10.46

e. The initiative to replace old fans with new energy-efficient fans should be

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

MAD 28–3 (FIN MAN); MAD 14–3 (MAN)

a. Recycling and reuse of production materials:

Variable savings

$ 0.15

per lb. of recycled material

Recycled material required to pay back initial cost: $5,000 ÷ $0.05 = 100,000 lbs.

The company will make up its added initial cost by the time it recycles 100,000 lbs.

of materials, and then every pound recycled after that will result in net savings of

$0.05 per lb. Based on this analysis, and because it can carry on this activity

indefinitely, Green Manufacturing should implement this activity because it will lead

to savings in the long run.

Adding solar panels as a source of power:

Variable savings

$33,000

per year

Variable cost

(1,000)

per year

Variable profit

$32,000

per year

Years until initial cost is paid back: $700,000 ÷ $32,000 = 21.875 years

The company will make up its added initial cost in 21.875 years, and then every

Replacing assembly room light fixtures with natural light:

Variable savings

$ 220

per month

Variable cost

(180)

per month

Variable profit

$ 40

per month

Years until initial cost is paid back: $120,000 ÷ $40 = 3,000 months

3,000 ÷ 12 = 250 years

b.

CSR Activity

Performance Metric

Recycle and reuse production

Pounds of material recycled

materials

Add solar panels as a source

Utility costs

Replace assembly room light

Utility costs

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

TAKE IT FURTHER

TIF 28–1 (FIN MAN); TIF 14–1 (MAN)

a. The motivated reasoning and surrogation biases can both have large negative

effects on the use of the balanced scorecard, even to the point that the balanced

scorecard becomes useless. Consider motivated reasoning: When a manager

motivated to evaluate his or her product positively ignores substantially negative

b. Some possible suggestions for avoiding or mitigating the motivated reasoning

bias:

1. Be aware of the tendency and incentive you have to be motivated to see

things favorably for yourself.

making a decision.

Some possible suggestions for avoiding or mitigating the surrogation bias:

1. Always act ethically and honestly. Ask yourself if you would feel

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

TIF 28–2 (FIN MAN); TIF 14–2 (MAN)

a. The online client review and client growth percentage metrics likely relate to a

strategic objective to satisfy and increase clients. The market share and profit

margin metrics likely relate to a strategic objective to increase profits.

b.

New clients during the month

7

Lost clients during the month

Increase in clients

3

Total clients at the beginning of last month

Client growth percentage last month

target met

c.

Number of 5-star reviews

55 × 5 =

275

Number of 4-star reviews

10 × 4 =

40

Number of 3-star reviews

3 × 3 =

9

Number of 1-star reviews

1 × 1 =

Sum total of stars

327

Total number of reviews

Number of 2-star reviews

1 × 2 =

2

not met

d. Possible strategic initiatives for the strategic objective to satisfy clients:

• Implement additional training course on serving and interacting with clients

• Invite clients to provide additional feedback through a brief online survey

• Have the company owner send a personal apology to any clients providing

a review of 2 stars or less, and offer them some kind of compensation; also

ask for their feedback regarding what caused them dissatisfaction

TIF 28–3 (FIN MAN); TIF 14–3 (MAN)

a.

Performance Perspective

Possible Strategic Objective(s)

Financial

Increase profits

Customer

Maintain current customers

b.

Possible Strategic Objective

Possible Performance Metric(s)

Increase profits

Gross profit

Maintain current customers

Number of lost customers

Cut production costs

Variable production costs

Decrease production times

Production process times

Recruit and train quality employees

Employee wages/salaries

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

TIF 28–3 (FIN MAN); TIF 14–3 (MAN) (Concluded)

c. High-quality employees would be expected to decrease production times and cut

production costs. Lower production costs would directly increase profits.

Decreased production times would likely satisfy and maintain current customers,

which would also contribute to increased profits.

TIF 28–4 (FIN MAN); TIF 14–4 (MAN)

People care about what is on the financial statements because of what these

statements communicate about the health and success of the firm. People do not care

CHAPTER 28 (FIN MAN); CHAPTER 14 (MAN) The Balanced Scorecard and Corporate Social Responsibility

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. d. The balanced scorecard is not based on scientific management theory but is a

flexible means of translating a company’s strategy into a comprehensive set

of performance measures.

2. a. The four perspectives of the balanced scorecard include options b, c, and d

plus the customer perspective. Competitor business strategies are not

included.