Operating Activities 403

E. An increase in this percentage would indicate that a company is hav-

ing greater difficulty collecting its receivables. A rapid increase might

suggest that a company’s customers are facing financial difficulties

P13-5 Computation of Manufacturing Inventory Costs:

Raw materials inventory:

Beginning balance $ 850,000

Materials purchased during the year 3,550,000

Materials used in production (3,720,000)

404 Chapter 13

P13-6

Part of the

cost of goods

manufactured,

or expense?

Materials,

labor, or

overhead?

a. Salaries of sales office staff

expense

—

b. Electric utilities for the factory area

cost of goods

overhead

c. Office supplies

expense

—

d. Paint and miscellaneous plastic

l. Insurance on the factory

cost of goods

overhead

m. Insurance on the administrative

offices

expense

—

magazines

expense

—

expense

—

p. Rental of storage facilities for ma-

terials

cost of goods

overhead

n. Advertising in trade

ished goods

expense

—

*Depends on how significant they are.

With regard to manufacturing costs, it is relatively easy to distinguish

among materials and labor on the one hand, and factory overhead on the

P13-7 A. “Raw materials and parts” are the physical components that will be-

come part of the firm’s finished products. “Work in process” is costs

cost of goods

e. Depreciation on factory equipment

cost of goods

overhead

expense

—

cost of goods

overhead

cost of goods

materials

j. Plastic sheets used for table tops

cost of goods

materials

assemblers

cost of goods

Operating Activities 405

of partially completed products, including purchased parts, labor, and

overhead. “Finished goods” is costs of completed but unsold goods,

406 Chapter 13

P13-8 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

1

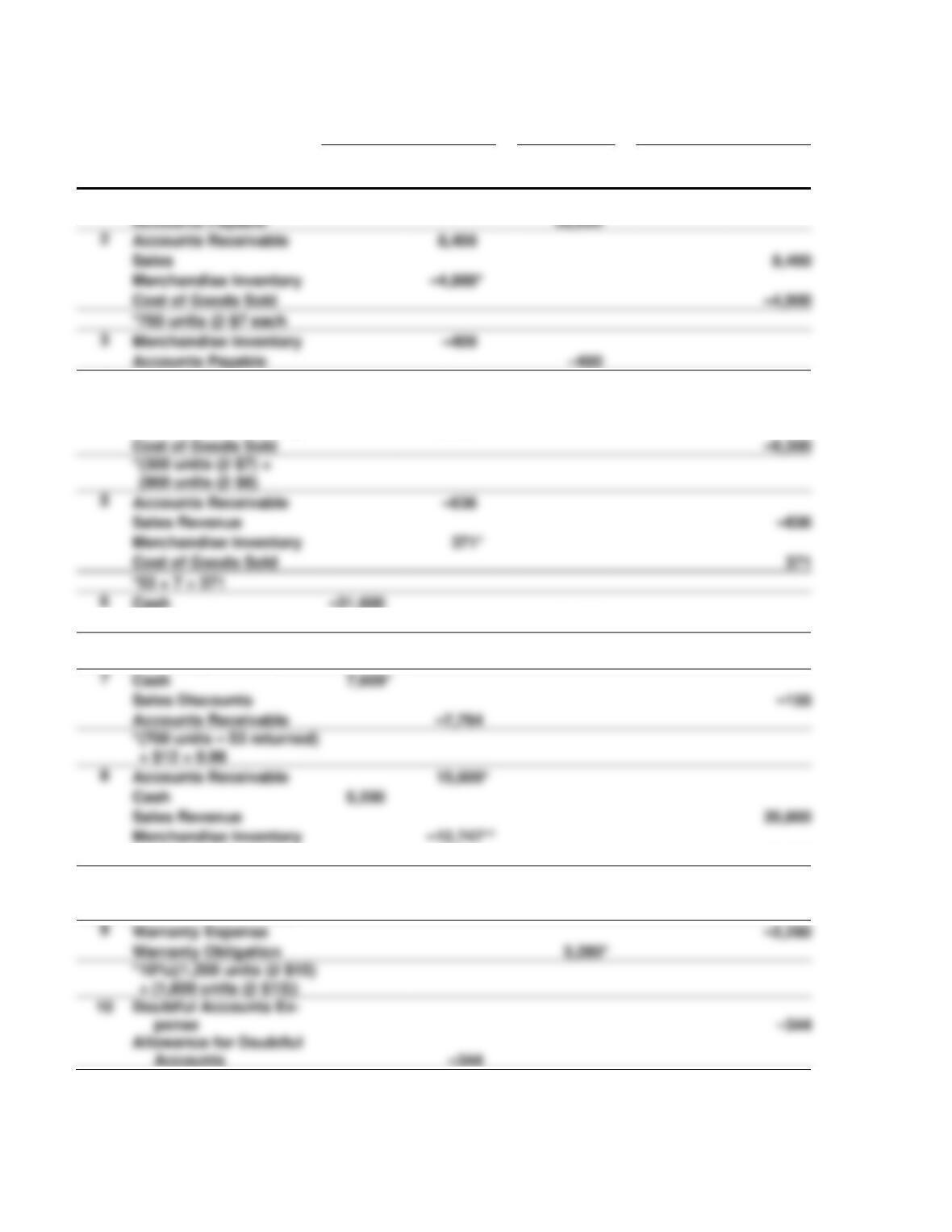

Merchandise Inventory

32,000

4

Cash

12,000

Sales

12,000

Merchandise Inventory

–9,300*

Cost of Goods Sold

(900 units @ $8)

5

Accounts Receivable

Sales Revenue

Merchandise Inventory

Cost of Goods Sold

*53 × 7 = 371

Cash

–31,600

Accounts Payable

–31,600*

*$32,000 – $400 goods

previously returned

7

Cash

Sales Discounts

Accounts Receivable

8

Accounts Receivable

Cash

Sales Revenue

20,800

Merchandise Inventory

Cost of Goods Sold

–12,747

* (1,600 units @ $13) ×

75%

** (53 × 7) + (1,547 × 8)

9

Warranty Expense

Warranty Obligation

Accounts Payable

Accounts Receivable

Sales

Merchandise Inventory

–4,900*

Cost of Goods Sold

*700 units @ $7 each

3

Merchandise Inventory

Accounts Payable

Operating Activities 407

B. Culture Music Company

Income Statement

Month of October

Net Sales ($8,400 + $12,000 + $20,800 − $636 − $155) $40,409

C. −$616

Cost of goods sold under: Sale #1 Sale #2 Return Sale #3 Total

FIFO $4,900 $9,300 ($371) $12,747 $26,576

408 Chapter 13

P13-9 A.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

1

Accounts Receivable

–9,000

Sales Returns

–9,000

Merchandise Inventory

6,300a

Cost of Goods Sold

6,300

a Based on a 30% gross profit ($9,000 × 70% = $6,300 cost of goods sold)

B. $248,440

Schedule:

Net sales $ 1,835,7001

Total operating expenses 987,060

Operating income $ 248,440

1 [$1,855,000 − ($9,000 + $10,300 sales returns)]

2

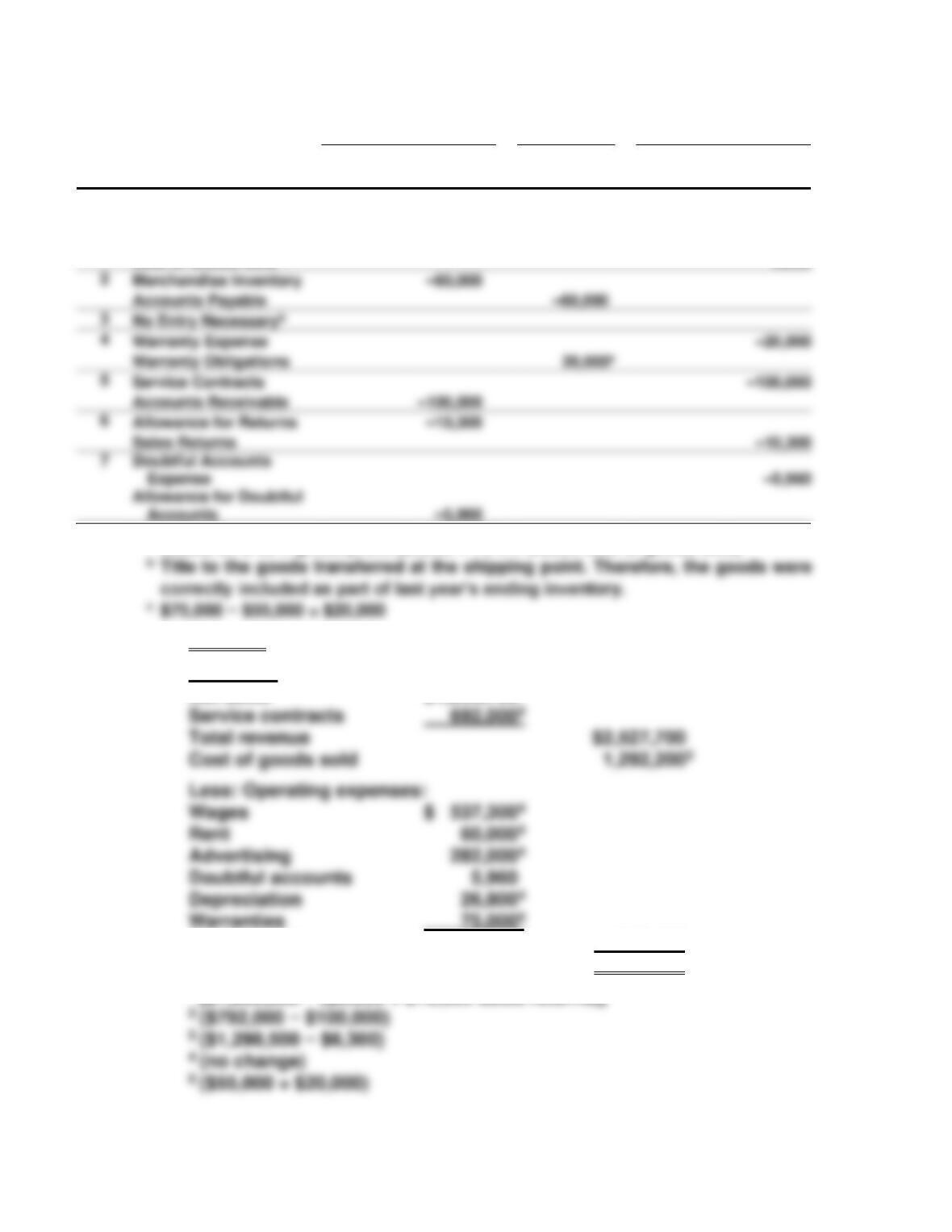

Merchandise Inventory

Accounts Payable

4

Warranty Expense

Warranty Obligations

5

Service Contracts

Accounts Receivable

Allowance for Returns

Sales Returns

–5,960

–5,960

Operating Activities 409

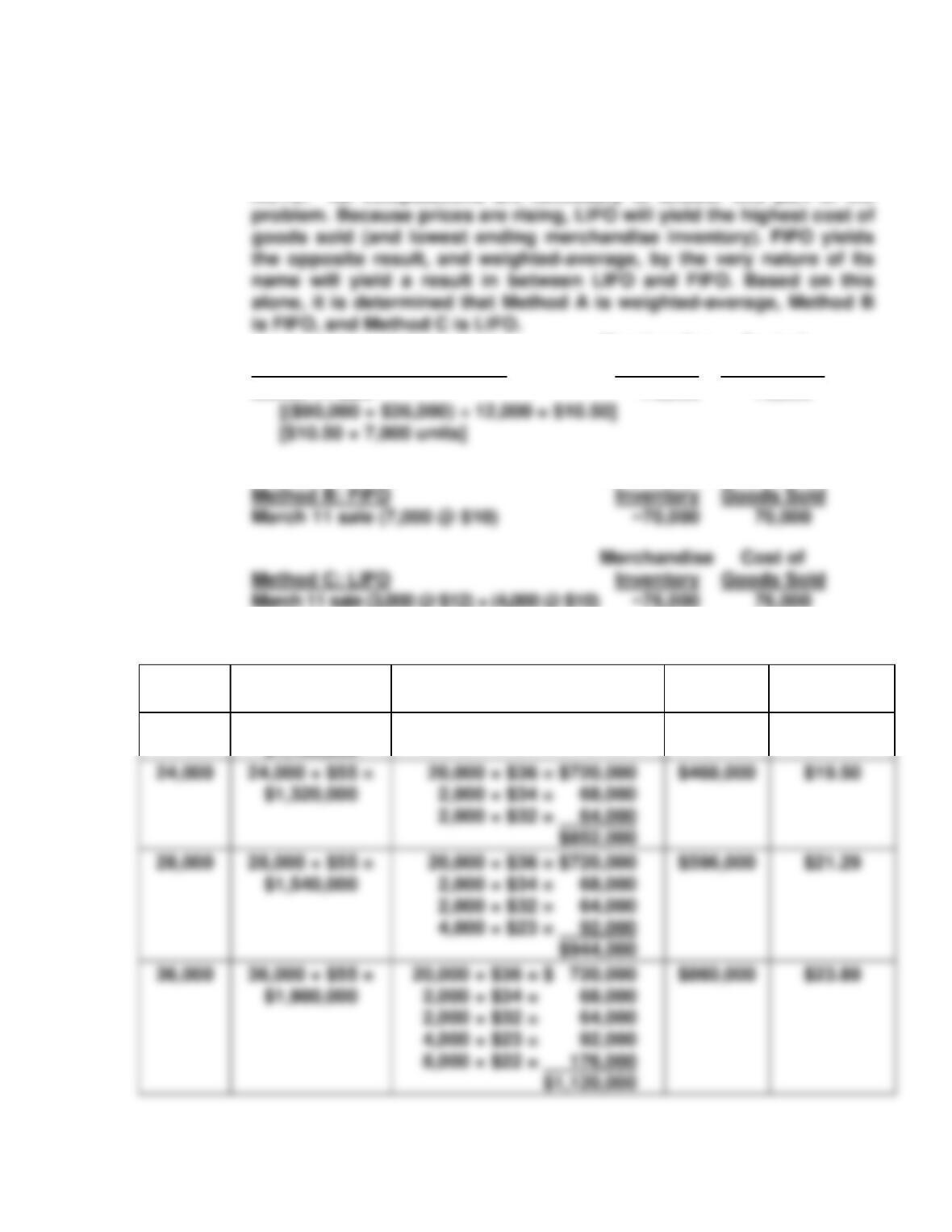

P13-10 A. Method A = Weighted-average

Method B = FIFO

Method C = LIFO

NOTE: No computations are necessary to answer this part of the

Merchandise Cost of

B. Method A: Weighted average Inventory Goods Sold

March 11 sale −73,500 73,500

Merchandise Cost of

P13-11 A.

Units

Sold

Revenue

Cost of Goods Sold

Gross

Profit

Gross Profit

per Unit

20,000

20,000 × $55 =

$1,100,000

20,000 × $36 = $720,000

$380,000

$19.00

410 Chapter 13

B. To minimize the effect of taxes: produce 36,000 units

If Rousseau produced 36,000 units during the current year, it would

To maximize the effect of taxes: produce 20,000 units

By producing only 20,000 units, Rousseau would be forced to sell off

C. Gross profit can be adjusted by controlling the number of units pro-

duced during the current year. The more units produced (up to

P13-12 A. Current Alternate

Methods Methods

Sales revenue $ 12,000,000 $ 12,000,000

Cost of goods sold 3,500,000 4,300,000

Net income $ 3,010,000 $ 2,100,000

B. The only cash flow effect of the choice in accounting methods is the

Operating Activities 411

P13-13 A. Sold = 5,200 units

Ending inventory = 900 units

B. Perpetual Periodic

Cost of Goods Sold $63,800 $65,400

Ending inventory $10,600 $ 9,000

Proof of perpetual system amounts (cost is determined separately for

each sale):

$10,600

Proof of periodic system amounts (cost is determined only at the end

of year):

Cost of goods sold: Under LIFO, the cost of goods sold is the cost of

the 5,200 units most recently purchased

C. Net income when the perpetual method is used would be:

Sales Revenue $ 85,000

412 Chapter 13

Net income when the periodic method is used would be:

For the two methods, net income differs by $1,600 and is lower if the

periodic method is used. This happens because when determining

D. Advantages of the perpetual method are that more timely information

is available. Also, if there are any inventory losses during the year,

Operating Activities 413

P13-14 Lawson Company

Income Statement

For the Year Ended December 31, 2007

(In millions)

Sales revenue $ 318.6

Gain on sale of securities 7.4

Income from continuing operations before taxes 46.7

Provision for income taxes (35%) 16.3

Income from continuing operations 30.4

Discontinued operations (net of tax effect of $4.3) (8.0)

P13-15 A. The gross profit on product sales is $806 million ($3,355 − $2,549). On

industries engaged in sales of similar products or services.

B. A “provision for restructuring” is the estimated cost of a plan that

414 Chapter 13

C. Yes, moving interest expense below would have made income from

operations positive in 2008 and 2007, but not in 2006.

F. Income from operations probably assists more in assessing the fu-

ture of the company. The discontinued operations have nothing to do

with the future of the company; the accounting change is a one-time

event.

G. The discontinued segment and the change in accounting principle are

the relationship between income and tax for this company.

P13-16 A. Pelican Enterprises

Income Statement (In thousands)

Year Ended June 30, 2007

Sales revenue $ 6,930

Service revenue 3,382

Income tax expense (30%) 1,077

Income before extraordinary item 2,513

Extraordinary gain on extinguishment of debt,

net of $12 tax 28

Net income $ 2,541

Operating Activities 415

Earnings per share:

B. No. The closing entries have not been made because the revenue and

D. Each of these stops along the income statement reports additional in-

formation that would not be available if all the information were just

added together and a single number reported. When you start com-

bining items and netting them against each other, eventually all you

416 Chapter 13

P13-17 A. B.

Minimum Maximum

Net Income Net Income

Sales revenue $13,680,000 $13,680,000

Cost of goods sold1 3,930,000 3,710,000

Cumulative effect of accounting

change net of tax savings of $374,000 (726,000) 0

Net income (loss) $ (609,378) $ 1,463,126

Earnings per share:

Income before cumulative effect

2Doubtful accounts expense:

Maximum expense — 4% × $10 million = $400,000

Minimum expense — 3% × $10 million = $300,000

3Depreciation expense:

Maximum Double-declining balance over minimum life

Operating Activities 417

C. The results of parts (a) and (b) suggest that one must be very careful

when comparing the net incomes of two or more companies. The

numbers (and comparisons) may be meaningless unless one is aware

of the different accounting choices that were made in obtaining the

P13-18 a. Merchandise was sold to customers at a price of $18,000. The cost to

the seller of the merchandise sold was $14,600.

b. Merchandise the company had purchased on credit for $33,000 was

returned to the supplier.

c. Cash was received from a customer in payment on account. The custom–

418 Chapter 13

P13-19 A. This disclosure reveals that Half Moon Inc. has an investment in the

common stock of Able Company and that the size of the investment is

B. This disclosure reveals that Half Moon controls Baker Company.

Usually this means that Half Moon owns a majority of Baker’s com-

mon stock. Further, this disclosure reveals that Half Moon does not

C. Projected benefit obligation: The amount of pension benefits earned

by employees as of the balance sheet date.

promised and the assets set aside to fund them.

D. Service cost: The amount of pension benefits that employees have

earned during the current fiscal period.

P13-20 The Book Wermz

Inventory of Webster’s Dictionary

August 31, 2007

FIFO Basis

Cost of Goods Sold

Ending Inventory

Date Purchased

Units

Available

Cost per Unit

Units

Cost

Units

Cost

12-Apr-07

245

$27.00

245

$ 6,615.00

0

—

360

360

0

—

842

$43,999.00

LIFO Basis

Cost of Goods Sold

Ending Inventory

Date Purchased

Units

Available

Cost per Unit

Units

Cost

Units

Cost

12-Apr-07

245

$27.00

87

$ 2,349.00

158

$4,266.00

360

360

$44,789.00

158

$4,266.00

Tax Savings from LIFO

LIFO Cost $ 44,789.00

If 545 units were purchased in April and the May purchase cost $31.00 per unit:

FIFO Basis

Cost of Goods Sold

Ending Inventory

Date Purchased

Units

Available

Cost per Unit

Units

Cost

Units

Cost

12-Apr-07

545

$27.00

545

$14,715.00

360

360

11,160.00

542

17,344.00

458

$43,219.00

458

(continued)

420 Chapter 13

LIFO Basis

Cost of Goods Sold

Ending Inventory

Date Purchased

Units

Available

Cost per

Unit

Units

Cost

Units

Cost

12-Apr-07

545

$27.00

87

$ 2,349.00

458

$12,366.00

Totals

1905

1447

$45,509.00

458

$12,366.00

Tax Savings from LIFO

LIFO Cost $ 45,509.00

P13-22

1

2

3

4

5

6

7

8

9

10

11

12

13

d

a

b

b

a

c

b

a

b

CASES

C13-1 A. About 72% ($765 million out of $1,063 million total) of General Mills’

negligible impact on fiscal 2003 and 2002 earnings.

B. The allowance for doubtful accounts declined from $28 million in 2003

C. From the statement of cash flows, we learn that General Mills record-

360

360

1000

1000

Operating Activities 421

C13-2 (NOTE: There are many different solution approaches that students might

take. The discussion and numerical information provided below are illus-

trative. The most important lesson of this case is that different accounting

be very useful.

To better understand and compare the results of the two companies, it is

necessary to apply the same accounting methods and procedures to each

firm. That step is particularly appropriate here because the two firms op-

erate in the same industry, sell the same products, and have many of the

same customers. While either firm’s income statement might be held con-

stant and the other modified to conform using the same accounting meth-

ods, it probably makes the most sense here to hold Sunlight’s income

On two other choices, Moonbeam simply made different estimates. Re-

garding uncollectible accounts, Moonbeam thought they would be low;

Sunlight thought they would be higher. Regarding warranty costs, Moon-

beam thought they would be immaterial, Sunlight thought differently. With

the companies being in the same line of business, selling the same prod-

422 Chapter 13

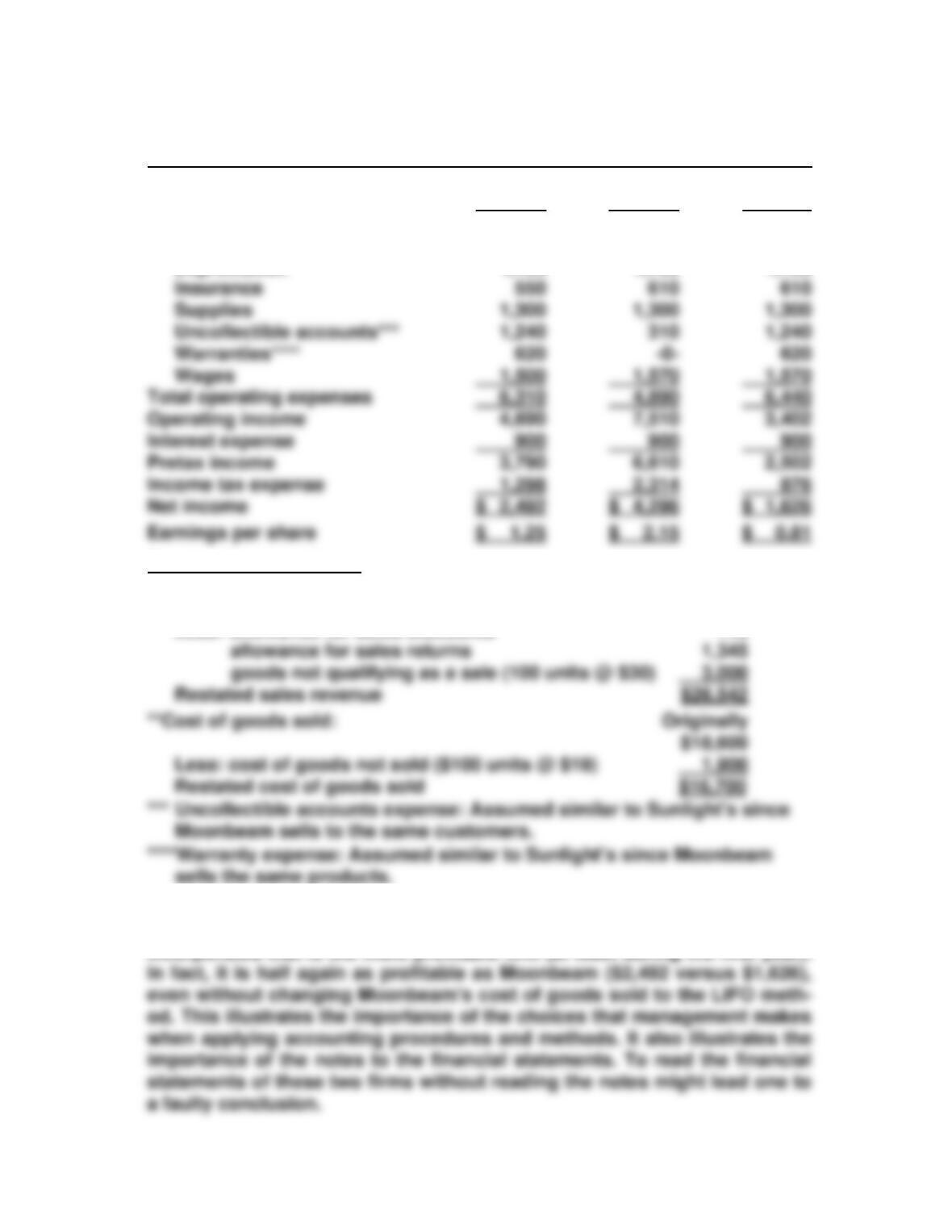

(a) (b) (c)

Sunlight Moonbeam Moonbeam

Income Statements for Year 2007 Inc. (as reported) (restated)

Sales revenue* $ 31,000 $ 31,000 $ 26,542

Cost of goods sold** 20,000 18,600 16,700

Gross profit $ 11,000 $ 12,400 $ 9,842

Operating expenses:

Depreciation 1,100 1,100 1,100

Proofs of restated items

*Sales revenue: Originally

$31,000

Less: allowance for sales discounts 113

When the financial results of the two companies are prepared using the

same set of assumptions, a very different picture appears. It is Sunlight

Incorporated that is the more profitable firm (at least during the first year).