Ch. 13—Problems 13–16

PROBLEMS

PROBLEM 13-1

Allocation of $280,000 of Partnership Income

Cumulative

Rockford Skeeba Tapinski Total

Profit and loss percentage ……………. 35% 25% 40%

Salary ………………………………………… $50,000 $40,000 $55,000 $145,000

Bonus based on sales ………………….. 15,000 160,000

Note A: Calculation of Annual Bonus

Bonus When Income Is $280,000

Bonus = 30% (Net Income – Gain on Equipment Sale – Bonus)

Note B: Interest on Weighted-Average Capital, Rockford

Number

Amount of Months Weighted

Invested Invested Dollars

$75,000 5 $375,000

Interest on Weighted-Average Capital, Skeeba

Number

Amount of Months Weighted

Invested Invested Dollars

$125,000 6 $ 750,000

110,000

6

660,000

13–17 Ch. 13—Problems

Problem 13-1, Concluded

Interest on Weighted-Average Capital, Tapinski

Number

Amount of Months Weighted

Invested Invested Dollars

$40,000 3 $120,000

PROBLEM 13-2

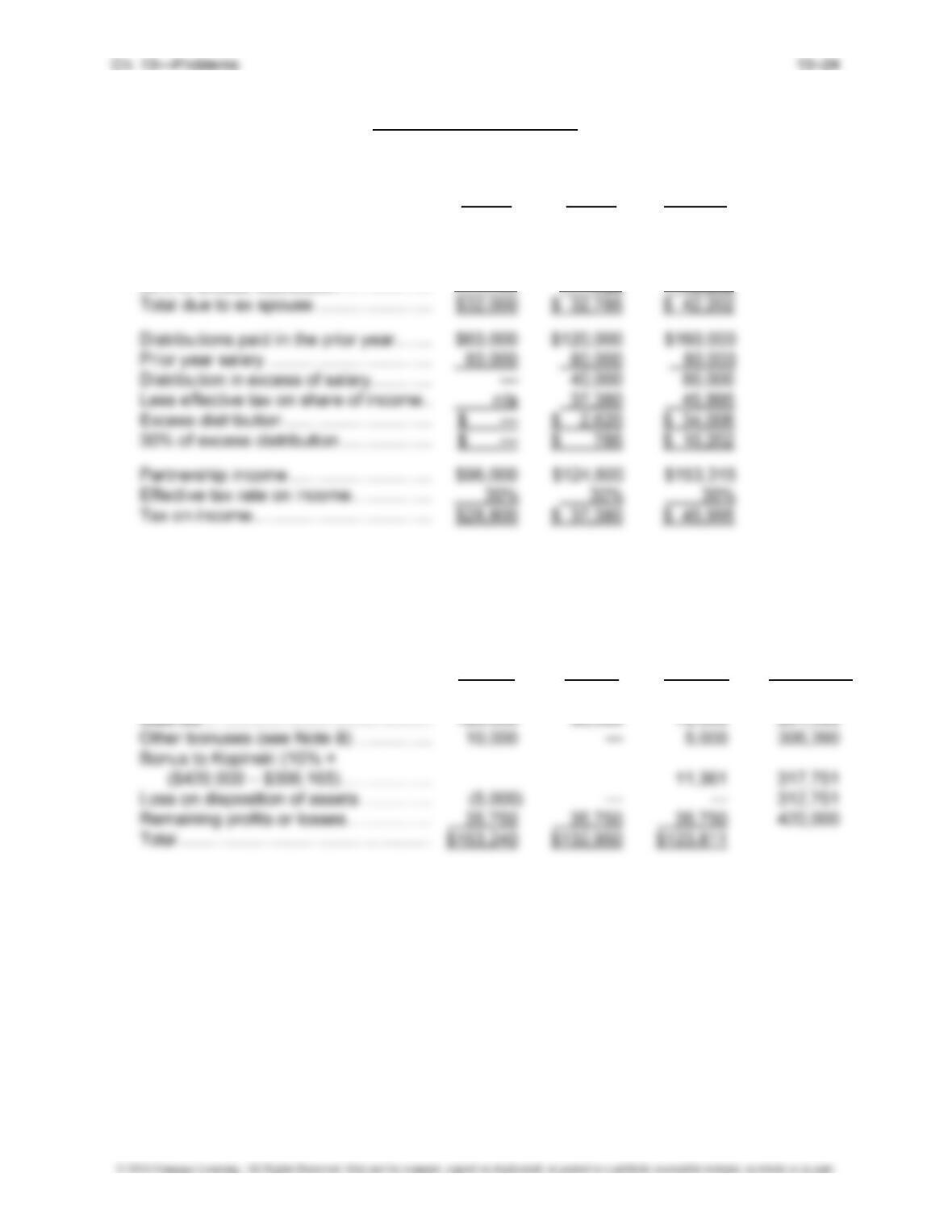

Analysis of Sandburg’s capital account:

January 1, 2015, balance as of date of divorce ………. $ 180,000

Distributions to Sandburg:

June 30 ……………………………………………………….. $ (60,000)

September 30……………………………………………….. (65,000) (125,000)

Distributions to Sandburg’s spouse:

February 28 (see Schedule B) …………………………

August 31 …………………………………………………….. (40,000)

Allocation of partnership net income (see Schedule A) 397,414

December 31, 2015, balance ……………………………….. $ 412,414

Distributions to Sandburg:

Problem 13-2, Continued

Schedule A—Allocation of Partnership Profit

2015 Profits: Sandburg Williams Total

Salaries …………………………………………………….. $100,000 $125,000 $225,000

Bonus (see Note A) …………………………………….. 68,182 68,182

Interest on capital (see Note B) …………………….. 6,021 4,375 10,396

Subtotal …………………………………………………….. $174,203 $129,375 $303,578

Note A: Calculation of 2015 Bonus Calculation of 2016 Bonus

Bonus = 10% ($750,000 – Bonus) Bonus = 10% ($700,000 – Bonus)

110% Bonus = 10% ($750,000) 110% Bonus = 10% ($700,000)

110% Bonus = $75,000 110% Bonus = $70,000

Problem 13-2, Concluded

2016 Weighted-Average Capital, Sandburg 2016 Weighted-Average Capital, Williams

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars Invested Invested Dollars

$412,414 2 $ 824,828 $357,586 6 $2,145,516

326,914 4 1,307,656 57,586 3 172,758

Schedule B—Distributions to Sandburg’s Spouse

In 2015, the first year of divorce, there was no February distribution.

In 2016, there is a February distribution, traceable to the prior year as follows:

Base earnings traceable to 2015:

Net income ……………………………………………………… $ 750,000

Excluded salaries …………………………………………….. (200,000)

Excluded bonus (limited to $50,000) …………………… (50,000)

Total ………………………………………………………………. $ 500,000

In 2017, there is a February distribution, traceable to the prior year as follows:

Base earnings traceable to 2016:

Net income ……………………………………………………… $ 700,000

Excluded salaries …………………………………………….. (200,000)

Excluded bonus (limited to $50,000) …………………… (50,000)

Total ………………………………………………………………. $ 450,000

Percent traceable to spouse ……………………………… × 25%

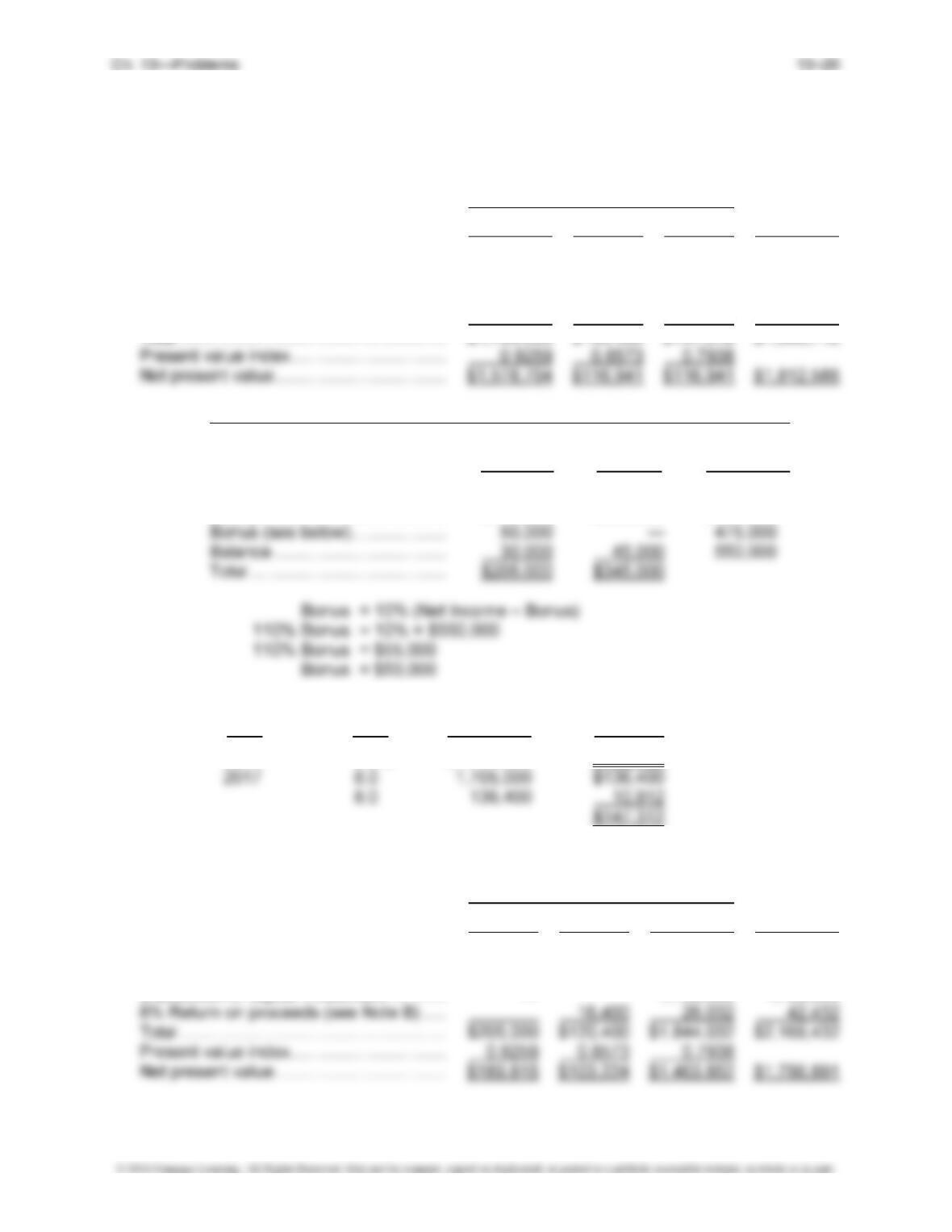

PROBLEM 13-3

Analysis of First Alternative

Cash flow components: March 31

2016

2017 2018 Total

Distribution of prior years’ income

(see Note A)…………………………………. $ 205,000 $ 205,000

Distribution of capital investment ………… 1,500,000 1,500,000

8% Return on proceeds (see Note B) ….. 136,400 147,312 283,712

Total ……………………………………………….. $1,705,000 $136,400 $147,312 $1,988,712

Note A: Year 2015—Allocation of $550,000 of Partnership Income

Other Cumulative

Raymond Partners Total

Profit and loss percentage …….. 40% 60%

Salary ………………………………… $125,000 $300,000 $425,000

Note B: Interest Amount

Year Rate Invested Return

2016 8.0% $1,705,000 $136,400

Analysis of Second Alternative

Cash flow components: March 31

2016

2017 2018 Total

Distribution of prior years’ income

(see Note A)………………………………… $205,000 $104,000 $ 118,000 $ 427,000

Distribution of capital investment ………… — 1,700,000 1,700,000

13–21 Ch. 13—Problems

Problem 13-3, Concluded

Note A: Year 2016—Allocation of $605,000 of Partnership Income

Other Cumulative

Raymond Partners Total

Profit and loss percentage …….. 20% 80%

Salary ………………………………… $ 80,000 $350,000 $430,000

Bonus = 10% (Net Income – Bonus)

110% Bonus = 10% × $605,000

Year 2017—Allocation of $682,000 of Partnership Income

Other Cumulative

Raymond Partners Total

Profit and loss percentage …….. 20% 80%

Salary ………………………………… $ 80,000 $350,000 $430,000

Bonus = 10% (Net Income – Bonus)

110% Bonus = 10% × $682,000

Note B: Interest Amount

Year Rate Invested Return

2017 8.0 205,000 $16,400

PROBLEM 13-4

Allocation of profits for years 2 through 4

Cumulative

Year 2 Jacobs Levine Total

Salaries …………………………………. $80,000 $110,000 $190,000

Bonus based on sales ……………… — — 190,000

Other bonuses (see Note A) …….. 10,000 10,000 210,000

Cumulative

Year 3 Jacobs Levine Total

Salaries …………………………………. $80,000 $110,000 $190,000

Bonus based on sales ……………… 5,000 — 195,000

Other bonuses (see Note A) …….. 12,500 12,500 220,000

Cumulative

Year 4 Jacobs Levine Total

Salaries …………………………………. $80,000 $110,000 $190,000

Bonus based on sales ……………… 10,000 — 200,000

Other bonuses (see Note A) …….. 15,000 15,000 230,000

Note A: Calculation of Bonus

Year 2 Year 3

Bonus = 10% (Net Income – Bonus) Bonus = 10% (Net Income – Bonus)

110% Bonus = 10% (Net Income) 110% Bonus = 10% (Net Income)

Year 4

Bonus = 10% (Net Income – Bonus)

110% Bonus = 10% (Net Income)

Problem 13-4, Continued

Note A: Interest on Weighted-Average Capital

Year 2 Jacobs Levine

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars

Invested Invested Dollars

$100,000 3 $ 300,000 $80,000 3 $240,000

85,000 3 255,000 65,000 3 195,000

Year 3 Jacobs Levine

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars

Invested Invested Dollars

$166,000 3 $ 498,000 $174,000 3 $ 522,000

136,000 3 408,000 144,000 3 432,000

Year 4 Jacobs Levine

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars

Invested Invested Dollars

$170,600 3 $ 511,800 $204,400 3 $ 613,200

130,600 3 391,800 164,400 3 493,200

Problem 13-4, Concluded

Payments to Jacob’s ex spouse for years 3 through 5

Year 3 Year 4 Year 5

Monthly payment of $2,500 ……………… $30,000 $ 30,000 $ 30,000

40% of the prior year salary …………….. 32,000 32,000 32,000

Less monthly payments ………………….. (30,000) (30,000) (30,000)

30% of excess distribution ………………. — 786 10,202

PROBLEM 13-5

Allocation of current year profit

Cumulative

Meyers Lincoln Kopinski Total

Interest on capital (see Note A) ………… $ 2,490 $ 1,200 $ (300) $ 3,390

13–25 Ch. 13—Problems

Problem 13-5, Concluded

Note A: Interest on Weighted-Average Capital

Meyers Lincoln

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars

Invested Invested Dollars

$59,000 3 $177,000 $30,000 6 $180,000

44,000 3 132,000 10,000 6 60,000

Kopinski

Number of

Amount Months Weighted

Invested Invested Dollars

$25,000 6 $150,000

(35,000) 6 (210,000)

—

Note B: Bonus on excess gross billings

Meyers Lincoln Kopinski

Gross billings…………………………………. $500,000 $380,000 $450,000

Threshold billings …………………………… 400,000 400,000 400,000

Determination of year end capital balances

Meyers Lincoln Kopinski

Beginning capital balance ……………….. $ 59,000 $ 30,000 $ 25,000

Withdrawal of salaries …………………….. (120,000) (96,000) (72,000)

Drawings in excess of salaries …………. (25,000) (20,000) (60,000)

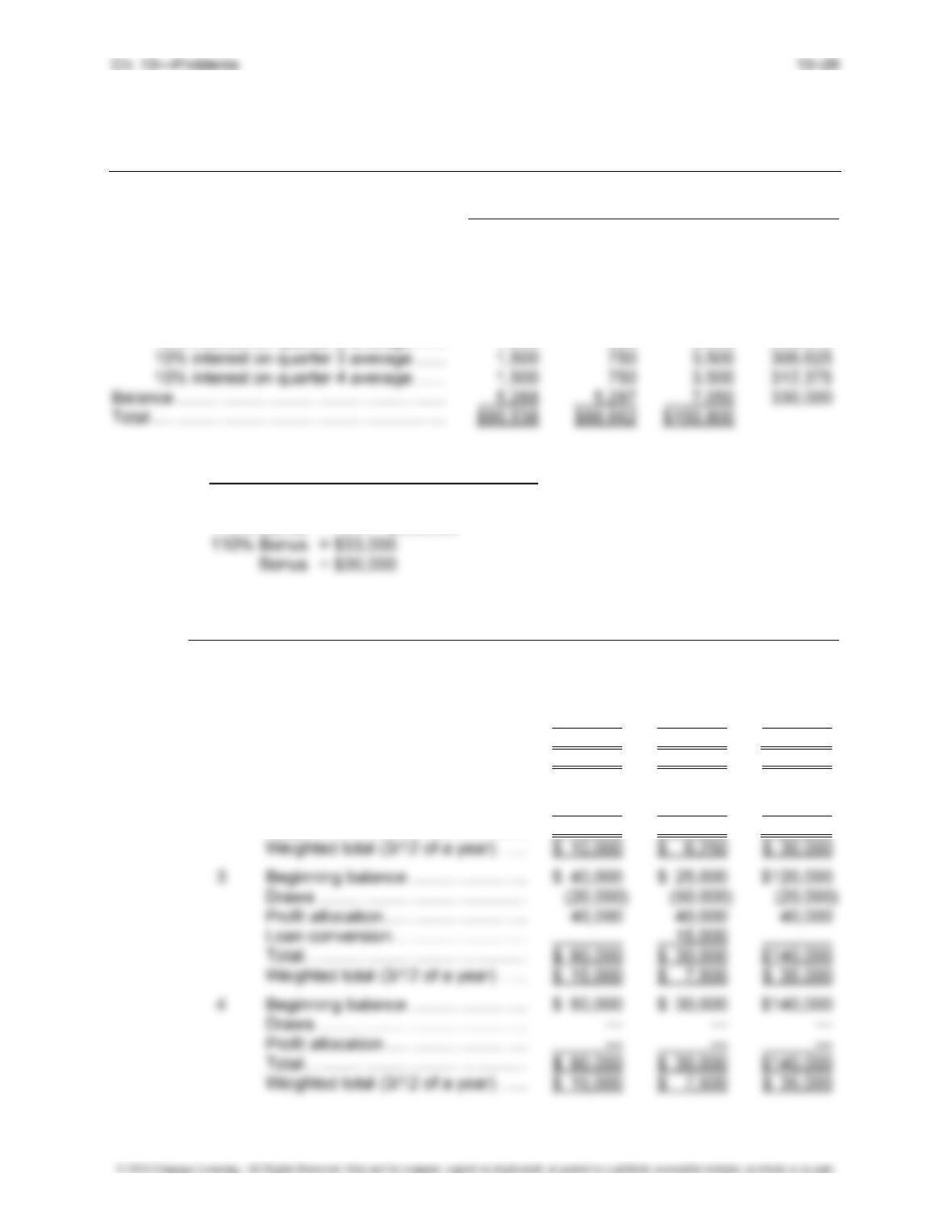

PROBLEM 13-6

Allocation of $330,000 of Partnership Income

Cumulative

Rivera Sampson Elliot Total

Profit and loss percentage ………………………. 30% 30% 40%

Salary …………………………………………………… $80,000 $80,000 $100,000 $260,000

Bonus (see Note A) ………………………………… — — 30,000 290,000

Interest on capital (see Note B):

10% interest on quarter 1 average ……. 1,250 1,250 3,750 296,250

10% interest on quarter 2 average ……. 1,000 625 3,000 300,875

Note A: Calculation of Annual Bonus

Bonus When Income Is $330,000

Bonus = 10% (Net Income – Bonus)

110% Bonus = 10% × $330,000

Note B: Determination of Interest on Capital

Quarter Component Rivera Sampson Elliott

1 Net capital beginning balance ……. $ 40,000 $ 50,000 $ 70,000

Draws …………………………………….. (30,000) (40,000) —

Profit allocation ………………………… 40,000 40,000 40,000

Capital investment …………………….

40,000

Total ……………………………………….. $ 50,000 $ 50,000 $150,000

Weighted total (3/12 of a year) …… $ 12,500 $ 12,500 $ 37,500

2 Beginning balance ……………………. $ 50,000 $ 50,000 $150,000

Draws …………………………………….. (10,000) (25,000) (30,000)

Total ……………………………………….. $ 40,000 $ 25,000 $120,000

PROBLEM 13-7

Amount to Be Paid to the Estate of Franklin

Average of last three years of allocated profit:

2013 allocated profit (as given) …………………………………………………….. $190,000

2014 allocated profit (see Schedule A) ………………………………………….. 134,150

2015 allocated profit (see Schedule A) ………………………………………….. 118,195

Schedule A—Restatement and Allocation of Profits

2014

2015

Profit as reported by Franklin ………………………………….. $500,000 $480,000

Adjustments:

1. Adjust for fictitious sales ……………………………….. (25,000) (75,000)

2. Adjust for inventory pricing errors:

3. Adjust casualty insurance expense ………………… — 60,000

4. Adjust prepaid insurance balance:

5. Remove depreciation on equipment:

6. Remove cash sale ……………………………………….. (42,000)

Adjusted profit ………………………………………………………. $434,000 $376,700

Cumulative

2014 Allocation Wilson Watts Franklin Total

Profit and loss percentage ………………………. 30% 35% 35%

Salaries ………………………………………………… $150,000 $150,000 $150,000 $450,000

Problem 13-7, Continued

Cumulative

2015 Allocation Wilson Watts Franklin Total

Profit and loss percentage ………………………. 30% 35% 35%

Salaries ………………………………………………… $150,000 $150,000 $150,000 $450,000

Interest on capital (see Note A) ……………….. 8,500 3,500 (3,000) 459,000

Note A: Interest on Weighted-Average Capital, Wilson

2014 2015

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars Invested Invested Dollars

$300,000 3 $ 900,000 $100,000 3 $ 300,000

250,000 3 750,000 90,000 3 270,000

200,000 3 600,000 80,000 3 240,000

Interest on Weighted-Average Capital, Watts

2014 2015

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars

Invested Invested Dollars

$250,000 3 $ 750,000 $50,000 3 $150,000

200,000 3 600,000 40,000 3 120,000

13–29 Ch. 13—Problems

Problem 13-7, Concluded

Interest on Weighted-Average Capital, Franklin

2014 2015

Number of Number of

Amount Months Weighted Amount Months Weighted

Invested Invested Dollars

Invested Invested Dollars

$200,000 3 $ 600,000 $ — 3 $ —

150,000 3 450,000 (10,000) 3 (30,000)

Schedule B—Franklin’s Corrected Capital Balance

Balance at year-end 2013 ……………………. $200,000

2014 Profit allocation. ………………………….. 134,150

2014 Drawings ($50,000/quarter) ………….. (200,000)