434

P13–2, Concluded

7.

A

B

C

1

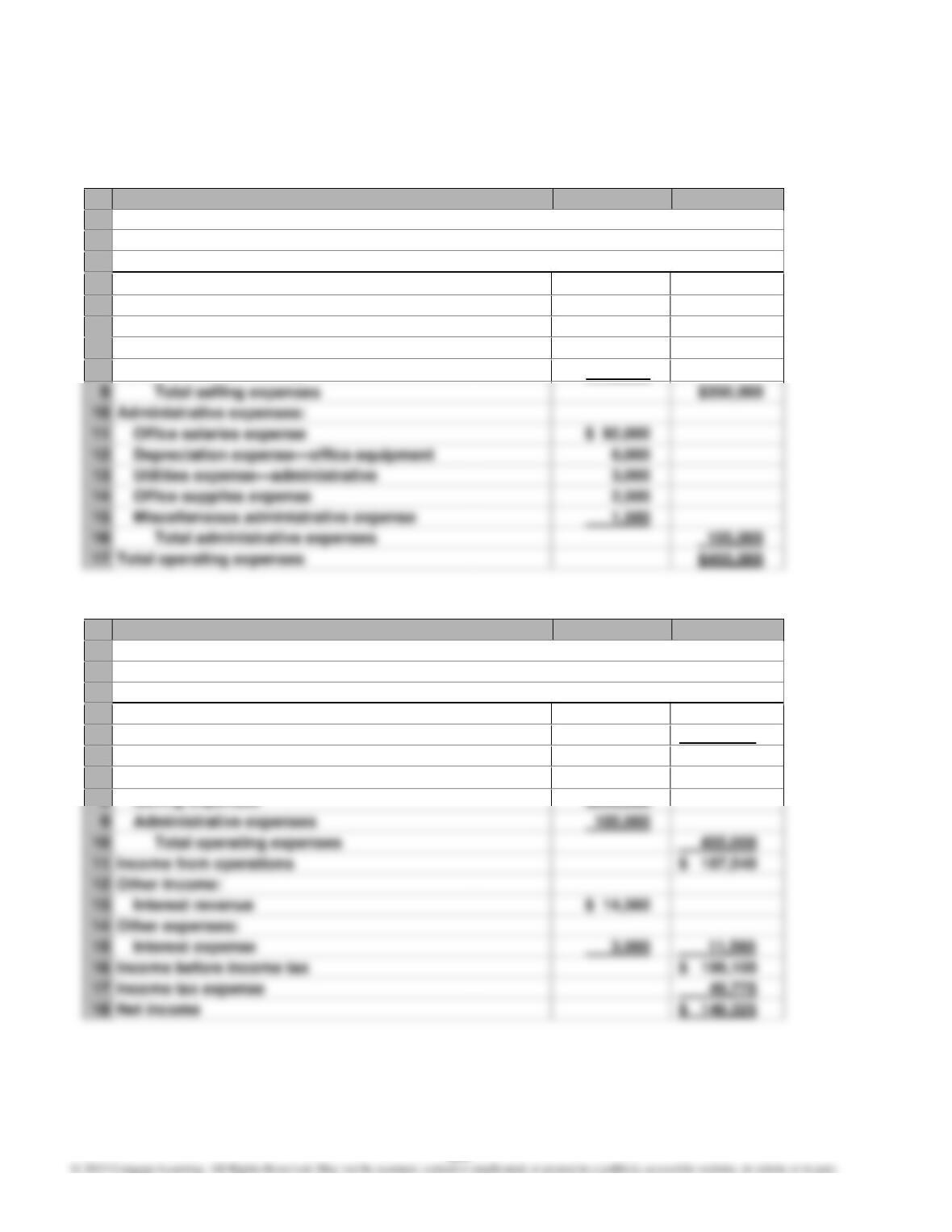

JUPITER HELMETS INC.

2

Selling and Administrative Expenses Budget

3

For the Month Ending May 31

4

Selling expenses:

5

Sales salaries expense

$175,000

6

Advertising expense

120,000

7

Travel expense—selling

50,000

8

Miscellaneous—selling

5,000

9

Total selling expenses

10

Administrative expenses:

11

Office salaries expense

$ 92,000

12

Depreciation expense—office equipment

13

Utilities expense—administrative

14

Office supplies expense

15

Miscellaneous administrative expense

1,500

16

Total administrative expenses

17

Total operating expenses

8.

A

B

C

1

JUPITER HELMETS INC.

2

Budgeted Income Statement

3

For the Month Ending May 31

4

Revenue from sales

$1,055,000

5

Cost of goods sold

412,460

6

Gross profit

$ 642,540

7

Operating expenses:

8

Selling expenses

9

Administrative expenses

105,000

10

Total operating expenses

455,000

11

Income from operations

$ 187,540

12

Other income:

14

Other expenses:

15

Interest expense

3,000

16

Income before income tax

$ 199,100

17

Income tax expense

49,775

18

Net income

$ 149,325

435

P13–3

1.

A

B

C

D

1

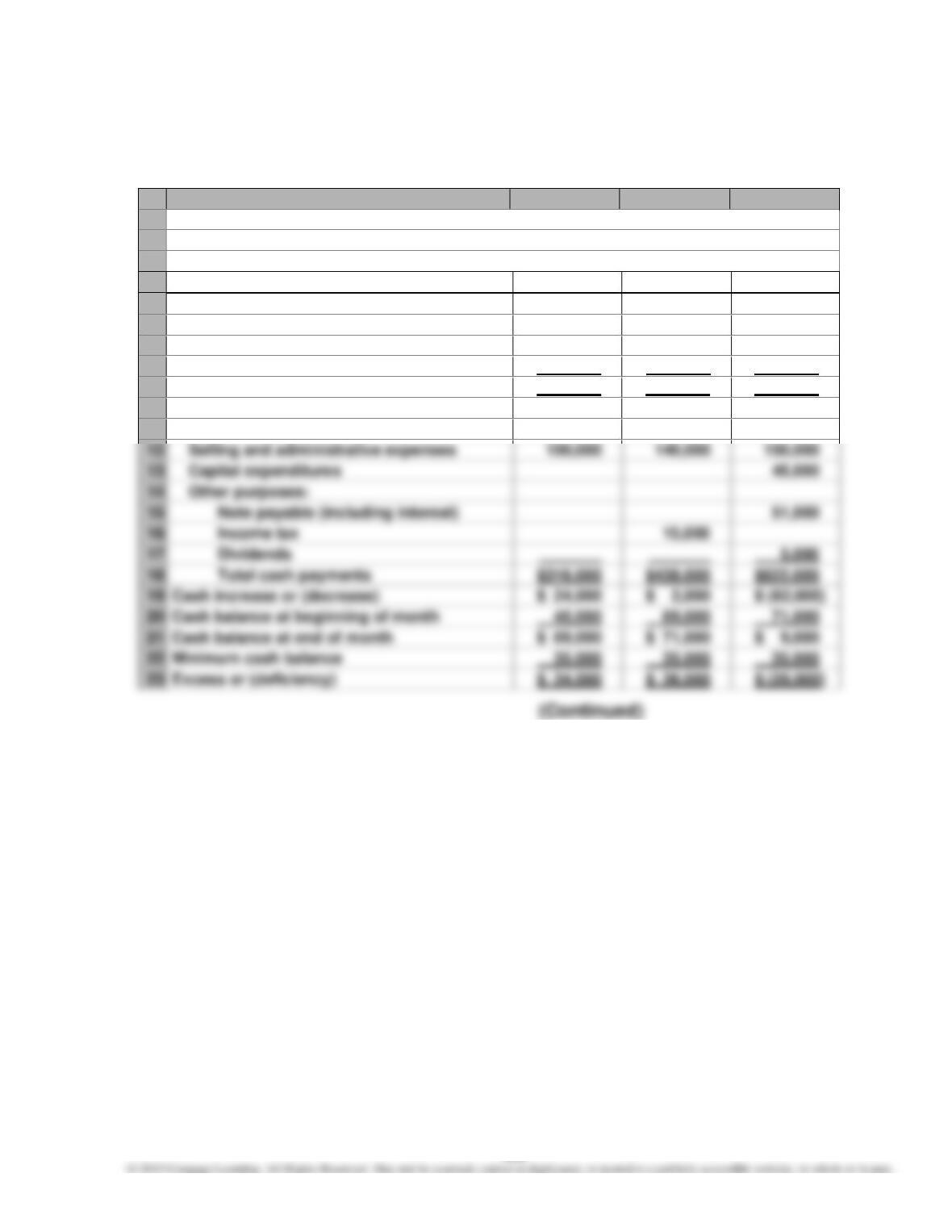

SHOE MART INC.

2

Cash Budget

3

For the Three Months Ending March 31

4

January

February

March

5

Estimated cash receipts from:

6

Cash sales

$ 90,000

$110,000

$140,000

7

Collection of accounts receivablea

230,000

330,000

420,000

8

Dividends

20,000

_______

9

Total cash receipts

$340,000

$440,000

$560,000

10

Estimated cash payments for:

11

Manufacturing costsb

$216,000

$283,000

$371,000

12

Selling and administrative expenses

100,000

150,000

13

Capital expenditures

14

Other purposes:

15

Note payable (including interest)

16

Income tax

17

Dividends

5,000

18

Total cash payments

$316,000

$438,000

$622,000

19

Cash increase or (decrease)

$ 24,000

$ 2,000

20

Cash balance at beginning of month

45,000

69,000

71,000

21

Cash balance at end of month

$ 69,000

$ 71,000

$ 9,000

22

Minimum cash balance

35,000

35,000

35,000

23

Excess or (deficiency)

$ 34,000

$ 36,000

436

P13–3, Concluded

24

Computations:

25

aCollections of accounts receivable:

January

February

March

26

November sales

$ 50,0001

27

December sales

180,0002

$ 60,0003

28

January sales

270,0004

$ 90,0005

29

February sales

330,0006

30

Total

$230,000

$330,000

$420,000

31

32

33

34

35

36

37

bPayments for manufacturing costs:

January

February

March

38

Payment of accounts payable, beginning

of month balancec

$ 18,000

$ 22,000

$ 29,000

39

Payment of current month’s costd

198,000

261,000

342,000

40

Total

$216,000

$283,000

$371,000

41

42

($260,000 – $40,000) × 10% = $22,000

43

($330,000 – $40,000) × 10% = $29,000

44

d($260,000 – $40,000) × 90% = $198,000

46

($420,000 – $40,000) × 90% = $342,000

cAccounts payable, January 1 balance = $18,000

2. The budget indicates that the minimum cash balance will not be maintained in

March. This is due to the capital expenditures and note repayment requiring

significant cash outflows during this month. This situation can be corrected

437

P13–4

a. Standard

Materials and

Labor Cost

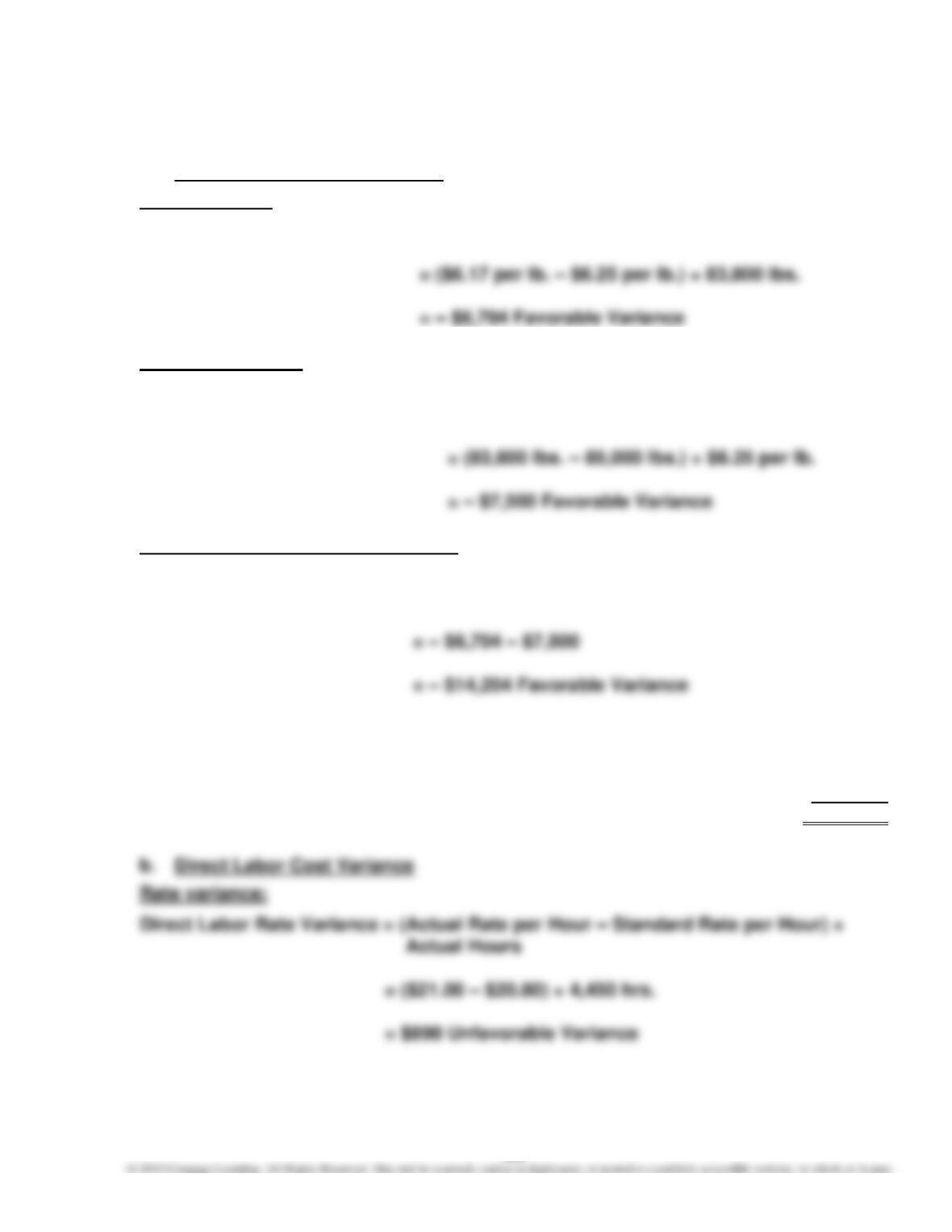

b. Direct Materials Cost Variance

Price variance:

Direct Materials Price Variance = (Actual Price – Standard Price) × Actual Quantity

= ($1.40 per lb. – $1.25 per lb.) × 10,200 lbs.

= $1,530 Unfavorable Variance

*12,000 units × 0.80 lb.

Total direct materials cost variance:

Direct Materials Cost Variance = Direct Materials Price Variance + Direct

Materials Quantity Variance

438

P13–4, Concluded

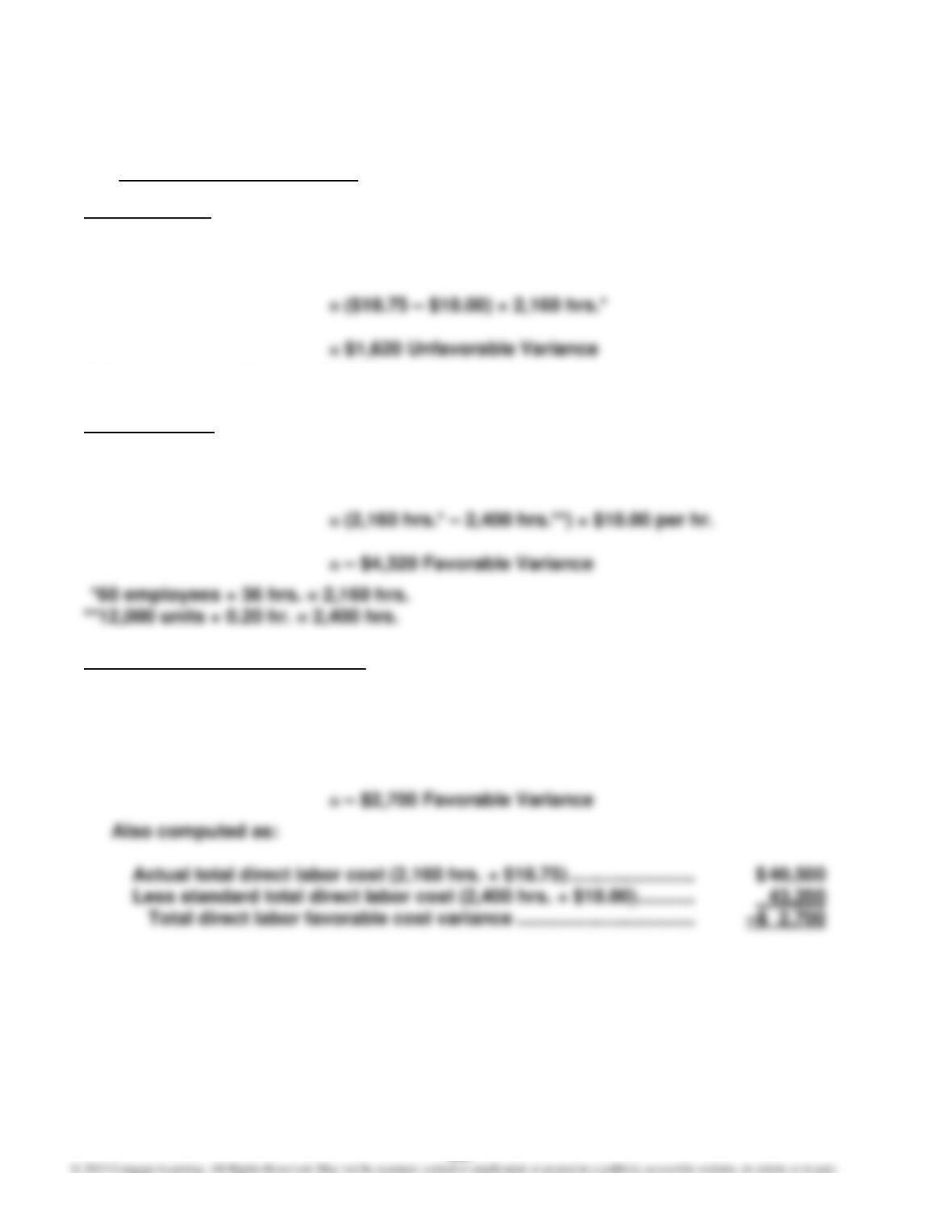

c. Direct Labor Cost Variance

Rate variance:

Direct Labor Rate Variance = (Actual Rate per Hour – Standard Rate per Hour) ×

Actual Hours

*60 employees × 36 hrs. = 2,160 hrs.

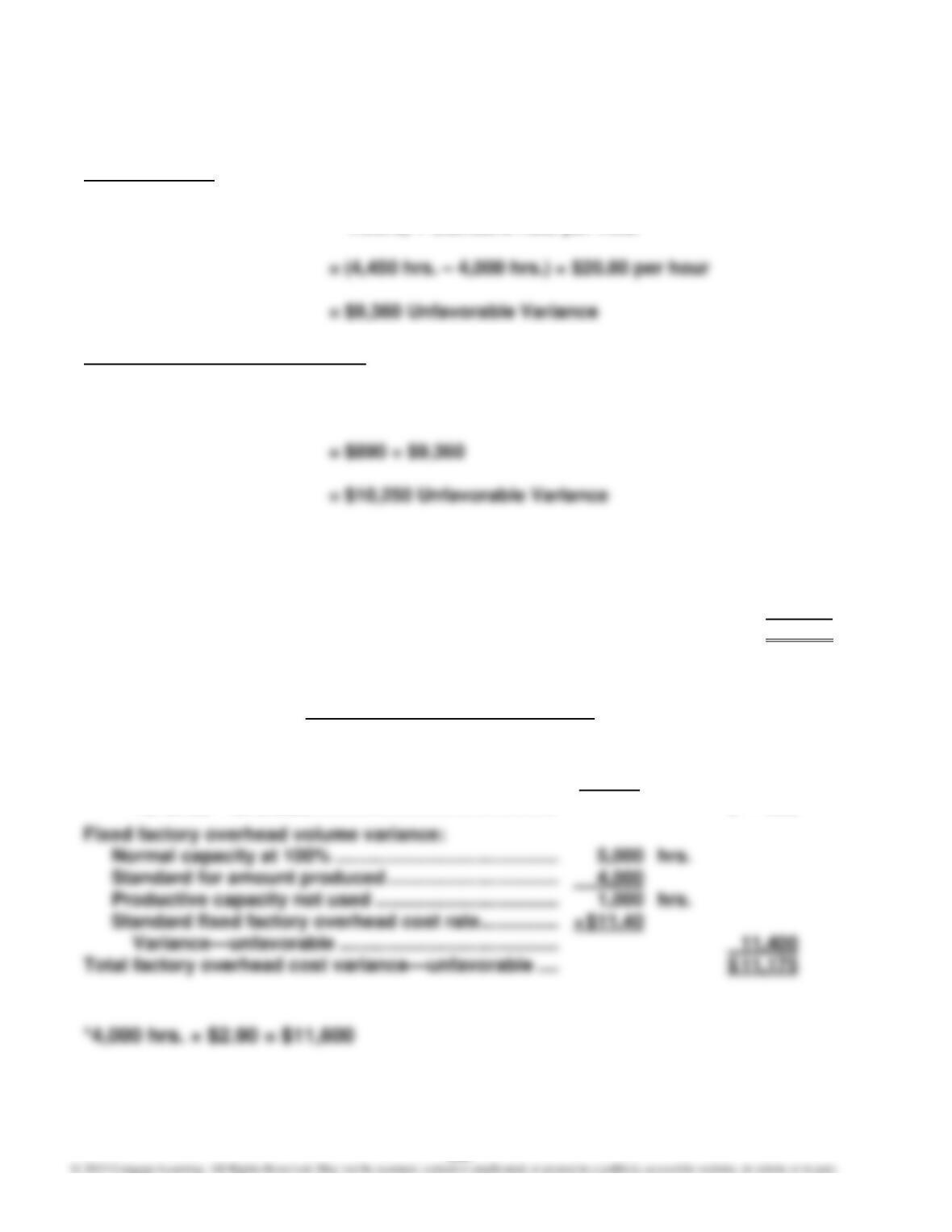

Time variance:

Direct Labor Time Variance = (Actual Direct Labor Hours – Standard Direct Labor

Hours) × Standard Rate per Hour

Total direct labor cost variance:

Direct Labor Cost Variance = Direct Labor Rate Variance + Direct Labor Time

Variance

= $1,620 – $4,320

439

P13–5

a. Direct Materials Cost Variance

Price variance:

Direct Materials Price Variance = (Actual Price – Standard Price) × Actual Quantity

Quantity variance:

Direct Materials Quantity Variance = (Actual Quantity – Standard Quantity) ×

Standard Price

Total direct materials cost variance:

Direct Materials Cost Variance = Direct Materials Price Variance + Direct

Materials Quantity Variance

Also computed as:

Actual total direct materials cost (83,800 lbs. × $6.17) ……………… $517,046

Less standard total direct materials cost (85,000 lbs. × $6.25) …. 531,250

Total direct materials favorable cost variance ………………………. –$ 14,204

440

P13–5, Continued

Time variance:

Direct Labor Time Variance = (Actual Direct Labor Hours – Standard Direct Labor

Hours) × Standard Rate per Hour

Total direct labor cost variance:

Direct Labor Cost Variance = Direct Labor Rate Variance + Direct Labor Time

Variance

Also computed as:

Actual total direct labor cost (4,450 hrs. × $21.00) …………………… $93,450

Less standard total direct labor cost (4,000 hrs. × $20.80) ……….. 83,200

Total direct labor unfavorable cost variance ………………………… $10,250

c. Appendix: Factory Overhead Cost Variance

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred …… $11,375

Budgeted variable factory overhead for 4,000 hrs. 11,600*

Variance—favorable ……………………………………….. $ – 225

441

P13–5, Concluded

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs ($11,375 + $57,000)

$68,375

Applied costs [4,000 × ($2.90 + $11.40)]

–57,200

Balance, underapplied factory overhead

$11,175

442

P13–6

1. Actual hours provided (2 × 40 hrs.) ………………………… 80

Standard hours required for the original plan …………. 80*

2. Actual hours provided (2 × 40 hrs.) ………………………… 80

Standard hours required for the actual results ……….. 88*

3. Actual labor rate ……………………………………………………. $ 20.00

Standard labor rate ……………………………………………….. 18.00

4. Actual hours provided (3 × 40 hrs.) ………………………… 120

Standard hours required for the actual results ……….. 88

Labor time difference ……………………………………………. 32

Standard labor rate ……………………………………………….. × $18.00

Direct labor time variance—unfavorable ………………… $ 576.00

5. The bonus is the better approach by $560. The cost variance for paying the

bonus was $16 unfavorable, which is the sum of the time variance and rate

6. The labor rate and time variances fail to consider the number of errors in the

report from typist fatigue. A report that has many errors will require signifi-

cant time for correction at a later date. In addition, report errors can cause

doctors to draw incorrect conclusions from the test analyses. Thus, manag-

ers should consider not only the efficiency of doing the work but also the

quality of the work.

443

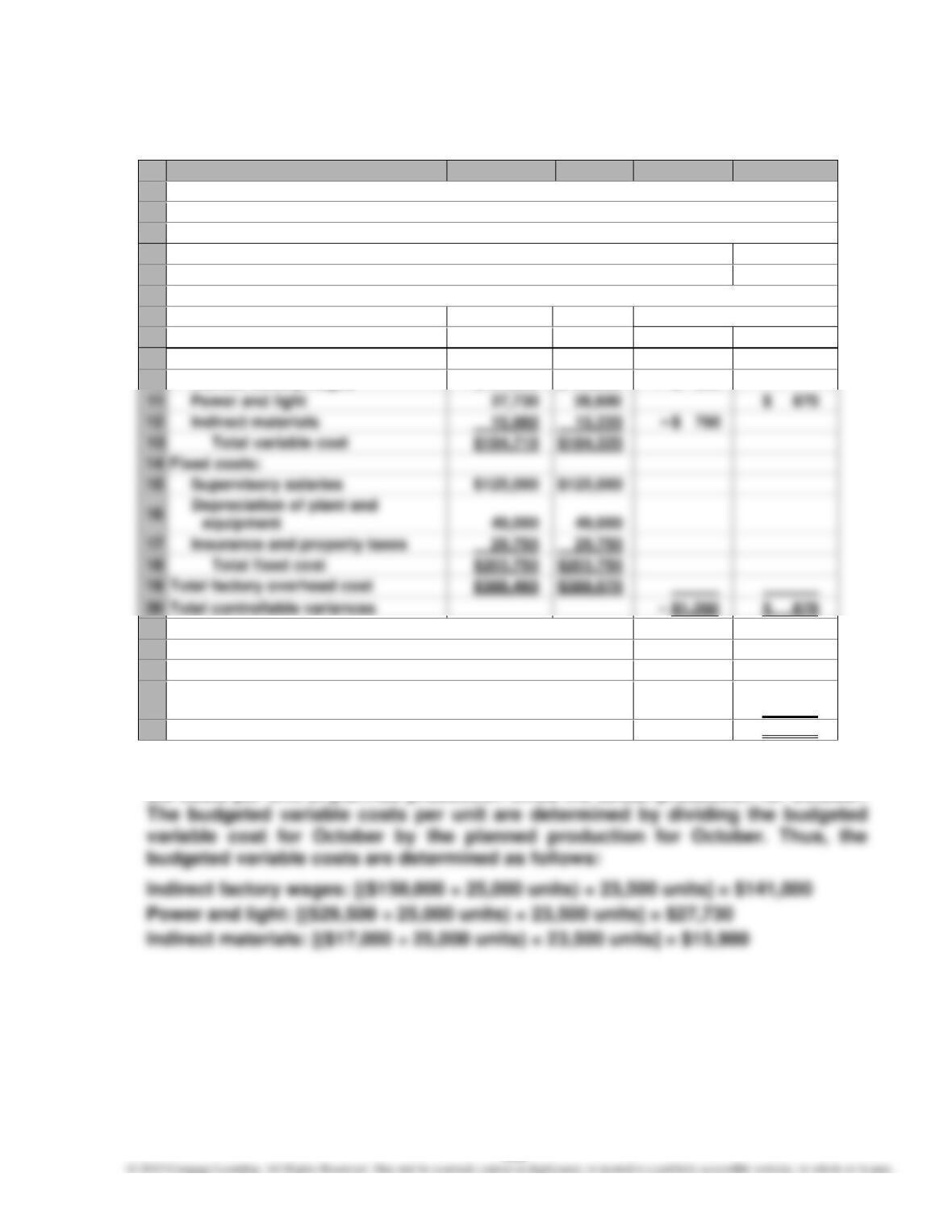

Appendix: P13–7

A

B

C

D

E

1

SEABURY, INC.

2

Factory Overhead Cost Variance Report—Assembly Department

3

For the Month Ended October 31

4

Normal capacity for the month

25,000 hrs.

5

Actual production for the month

23,500 hrs.

6

7

Variances

8

Budget*

Actual

Favorable

Unfavorable

9

Variable costs:

10

Indirect factory wages

$141,000

$140,500

– $ 500

11

Power and light

$ 870

12

Indirect materials

13

Total variable cost

14

Fixed costs:

15

Supervisory salaries

16

17

Insurance and property taxes

18

Total fixed cost

20

Total controllable variances

21

22

Net controllable variance—favorable

– $ 390

23

Volume variance—unfavorable:

24

Idle hours at the standard rate for fixed factory overhead—

(25,000 hrs. – 23,500 hrs.) × $8.15**

12,225

25

Total factory overhead cost variance—unfavorable

$11,835

*The budgeted variable costs are determined by multiplying the budgeted varia-

ble costs per unit at planned production times the actual production for October.

**$203,750 ÷ 25,000 hrs. = $8.15

444

Appendix: P13–7, Concluded

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs

$388,070

Applied costs [23,500 hrs. × ($7.86* + $8.15)]

–376,235

Balance, underapplied factory overhead

$ 11,835

*$196,500 ÷ 25,000 hrs. = $7.86 per hour variable overhead rate

CASES

Case 13–1

Bud should reject Ellen’s request to charge the convention-related costs against

February’s budget. This is just one example of many attempts to slide expenses

into different budget periods than when actually incurred. This is a common issue

that controllers face. Often, operating managers will attempt to accelerate future

expenditures into low-expenditure months or delay present expenditures into fu-

Case 13–2

1. The hospital’s new budget method is clearly an example of a flexible budget.

The budget changes with changes in underlying activity, such as patient–

days. Patient-days are the number of patients multiplied by the number of

days in the hospital. As the number of patient-days changes, it would be rea-

sonable to expect that the hospital’s variable costs should also change. In

addition, the last quote suggests that the new budget approach is a monthly

continuous budget. The budget helps the managers plan month-by-month

expenditures.

2. The advantage of a flexible budget is to accurately plan variable costs of the

hospital with changes in the underlying activity base. Using a static budget

would create actual deviations from budget that would be difficult to interpret.

446

Case 13–3

1. The budget information indicates that the actual expenditures by the Opera-

tions Department exceeded what was planned by $20,000 ($435,000 –

2. The bank manager does not know if the actual resources consumed by the

Operations Department are the right amount of resources for doing the right

things. In other words, this budget doesn’t say anything about the actual

work of the Operations Department and how much cost this work consumes.

The bank manager doesn’t have a good sense if there is waste in the depart-

ment or not. The $20,000 excess expenditure over budget raises several ques-

tions. If the department did twice as much work as planned, then the $20,000

is a bargain. If, on the other hand, the department did much less work than

planned, then the $20,000 understates how poorly the department used re-

sources. Again, how much work the department actually did is unknown, so

these questions cannot be answered. A flexible budget would provide more

information about the work of the department. Examples of the kind of work

447

Case 13–4

Domino’s could use a master budget to plan operations consistent with the sales

forecast. The sales forecast could be used to develop the production budget for

pizzas. The sales and production budgets would be identical since there would be

no finished goods inventory for cooked pizzas. The sales (production) budget

would be used to develop a direct materials purchases budget. For example, the

The budget process could be used to direct and coordinate all the various restau-

rants. In this way, all the managers would be operating under the same set of as-

sumptions. The actual performance of the company and the individual stores could

be compared with the budget in order to provide all levels of the organization ap-

propriate feedback and control. This feedback can be used to adjust operations to

448

Case 13–5

1. The amount of actual expenditures was less than budget for the first 10

months of the budget year. As the end of the budget year-end neared, the

manager spent the remaining excess budget and, as a result, went over the

budget for May and June. The amount spent for the year was equal to the to-

2. The budget system encourages this type of wasteful behavior. The budget

could be redesigned in a number of ways. The budget could be designed to

flex with underlying activity and adjusted monthly. Thus, the manager would

always have budgeted resources for changes in underlying activity. For ex-

ample, if the number of prisoners in the jail increased, then the budget would

increase proportionately. A manager with the flexible budget would be less

likely to “reserve” the budget during the year, since an activity change would

be automatically reflected in the monthly budget. That is, the inherent slack in

the static budget could be reduced, knowing that activity changes are auto-

matically accommodated by the flexible budget. The budget system might al-

so allow a manager to make a request for additional funds after the budget

Case 13–6

The use of ideal standards is a legitimate concern for Everett. It is likely that such

standards are too tight and do not include the necessary fatigue factors that are

likely in this type of operation. It seems as though Everett is arguing for practical

Case 13–7

Although the Trinity Industries’ performance measurement system uses both fi-

nancial and nonfinancial measures, there may still be some serious performance

omissions. The financial measures are good measures of financial performance.

450

Case 13–8

1. The scrap is measured in sales dollars rather than cost in order to communi-

cate the total value of potential lost sales. If an item is scrapped and not sold,

2. The “orders past due” is a common measure of the aggregate sales value of

orders past due. The “buyer’s misery index” measures how many customers

are waiting for orders to be filled. It is a more pure measure of customer satis-

Sales Value of Buyer’s

Scenario Orders Past Due Misery Index

1 $810,000 1

2 810,000 16

In the first scenario, 18% ($810,000 ÷ $4,500,000) of sales are past due to a

single customer. The single customer is probably very upset, but all the other

customers are being satisfied. Apparently, one large order was not delivered

to the customer. This could be an isolated problem.

451

Case 13–9

The plant manager is placing pressure on the controller because the controllable

variance is very unfavorable. The claim is that these costs are not really variable

at all. This is a very difficult claim to accept. This is a small company, so it pur-

chases its power from the outside. The power and light bill is variable to the

The indirect wages may not be completely variable. However, the variance is

$28,800, or 40% ($28,800 ÷ $72,000) higher than the standard. This is much great-

er than the 25% difference between the existing production volume and full ca-

pacity. In other words, even granting the plant manager’s position on the indirect

wages still does not explain the overall size of the variance. The expenditure of

$100,800 on indirect wages is more than the $96,000 ($72,000 ÷ 75%) that would

have been budgeted for 100% of production. Something appears amiss.