13–33

PROBLEM 13-49 (CONTINUED)

3. (a) The head of the German division should be a team player; however, when the

circuit board can be obtained locally for $465, it is difficult to get excited

about doing business with the U.S. operation. Courtesy of the shipping fee

(b) Yes. Delta will make $180.00 per circuit board ($72.00 + $108.00) if no transfer

takes place and all circuit boards are sold in the U.S.

U.S. operation:

Sales revenue……………………………………………….

$ 510.00

Less: Variable manufacturing cost……………………..

390.00

Income before tax…………………………………………..

$ 120.00

Less: Income tax expense ($120.00 x 40%)……………

48.00

Income after tax…………………………………………….

$ 72.00

German operation:

Sales revenue…………………………………..

$1,080.00

Less: Purchase price………………………….

$465.00

810.00

Income before tax………………………………

$ 270.00

Less: Income tax expense ($270.00 x 60%)..

162.00

Income after tax…………………………………

$ 108.00

4. When tax rates differ, companies should strive to generate less income in high tax–

Chapter 13 – Investment Centers and Transfer Pricing

13–34

SOLUTIONS TO CASES

CASE 13-50 (40 MINUTES)

1.

If New Age Industries continues to use return on investment as the sole measure of

division performance, Fun Times Entertainment Corporation (FTEC) would be reluctant

to acquire Recreational Leasing, Inc. (RLI), because the post-acquisition combined ROI

would decrease.

2.

Residual income is the profit earned that exceeds an amount charged for funds

committed to a business unit. The amount charged for funds is equal to an imputed

interest rate multiplied by the business unit’s invested capital.

13–35

CASE 13-50 (CONTINUED)

3.

a.

The likely effect on the behavior of division managers whose performance is

measured by return on investment includes incentives to do the following:

b.

The likely effect on the behavior of division managers whose performance is

measured by residual income includes incentives to do the following:

13–36

CASE 13-51 (50 MINUTES)

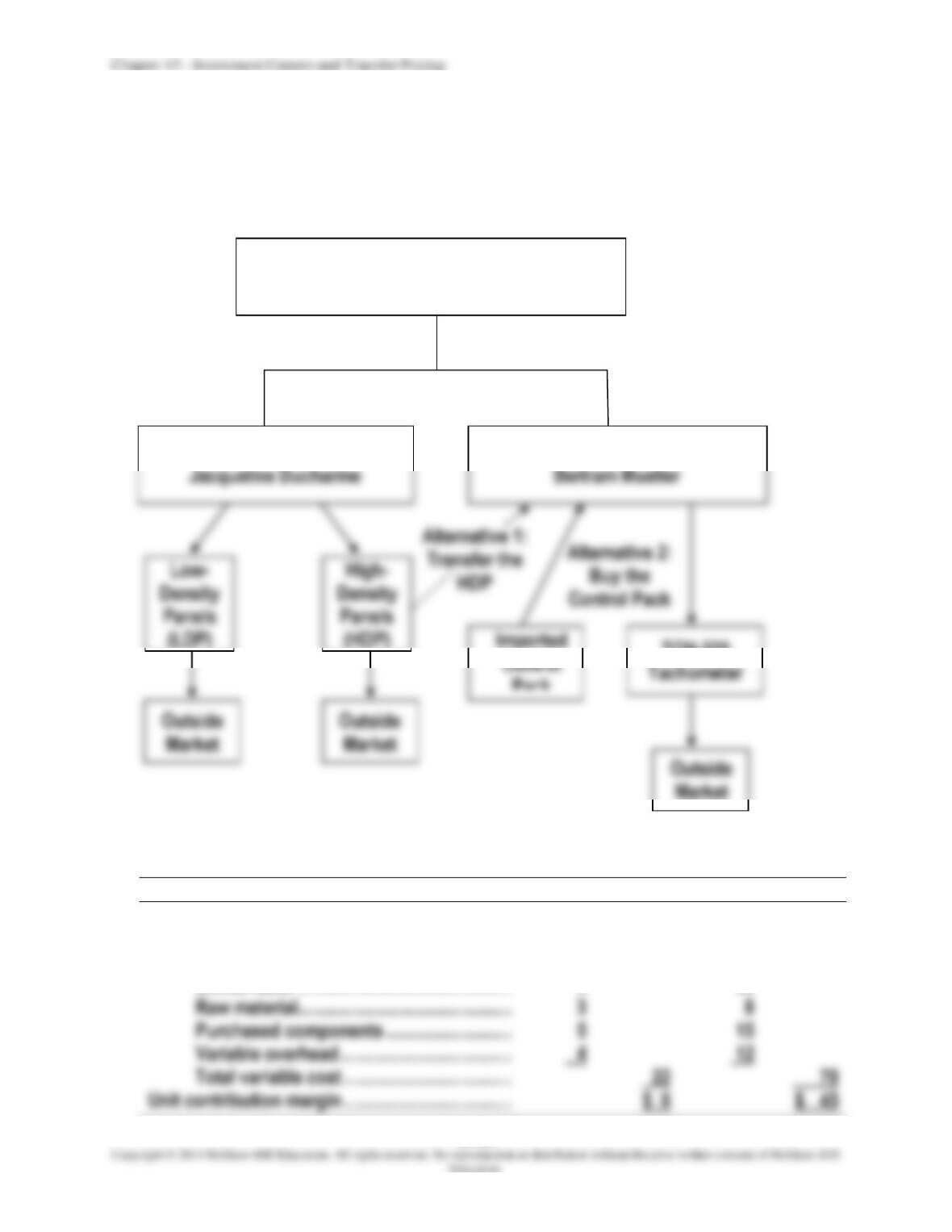

1. Diagram of scenario:

2.

First, compute the unit contribution margin of an LDP and an HDP as follows:

LDP

HDP

Price …………………………………………………………………………..

$28

$ 115

Less: Variable cost:

Unskilled labor …………………………………………………..

$5

$ 5

Skilled labor ………………………………………………………

5

30

Raw material ………………………………………………………

3

8

Purchased components …………………………..

5

15

Variable overhead ………………………………………………

GENERAL INSTRUMENTATION CORPORATION

Top Management

HUDSON BAY DIVISION

VOLKMAR TACHOMETER DIVISION

TCH-320

13–37

CASE 13-51 (CONTINUED)

Second, compute the unit contribution margin of Volkmar’s TCH-320 under each of its

alternatives, as follows:

TCH-320

Using

Imported

Control Pack

TCH-320

Using

an

HDP

Price …………………………………………………….

$275.00

$275.00

Less: Variable cost:

Unskilled labor …………………………….

$ 4.50

$ 4.50

Skilled labor ………………………………..

51.00

85.00

Raw material ……………………………….

10.50

Purchased components ……………….

Variable overhead ……………………….

12.00

12.00

Variable cost of manufacturing HDP

-0-

70.00

Variable cost of transporting HDP ..

Total variable cost ……………………….

Unit contribution margin ……………………….

$ 47.00

Hudson Bay’s “Three” Products

HDP for external sale

HDP for transfer

From the perspective of the entire company, the scarce resource that will limit overall

company profit is the limited skilled labor time available in the Hudson Bay Division. The

question, then, is how can the company as a whole best use the limited skilled labor time

available at Hudson Bay? The division has two products: LDP and HDP. One can view these

LDP

Chapter 13 – Investment Centers and Transfer Pricing

CASE 13-51 (CONTINUED)

What is the unit contribution to covering the overall company’s fixed cost and profit from

each of these three products? The calculations above show that the unit contribution

margin of an LDP is $6, and the unit contribution of an HDP sold externally is $45.

Moreover, the unit contribution to the overall company of an HDP produced for transfer is

$42, which is the increase in the unit contribution margin of the TCH-320 when it is

manufactured with the HDP instead of the imported control pack. To summarize:

Hudson Bay’s Product

Unit Contribution to

Covering the Company’s

Fixed Cost and Profit

HDP sold externally

HDP transferred internally

LDP

The analysis of these three products’ contribution margins (to General Instrumentation as a

whole) has not gone far enough, because the products do not require the same amount of

the scarce resource, skilled labor time. The important question is how much one hour of

limited skilled labor at Hudson Bay spent on each of the three products will contribute

toward the overall firm’s fixed cost and profit.

Hudson Bay’s Product

Unit Contribution

Margin

Skilled Labor per

Unit Required at

Hudson Bay

Contribution

Margin

per Hour

HDP sold externally

HDP transferred internally

LDP

13–39

CASE 13-51 (CONTINUED)

This analysis shows that from the perspective of the entire company, Hudson Bay’s best

use of its limited skilled labor resource is to produce HDPs for external sale, up to the

maximum demand of 6,000 units per year. The second best use of Hudson Bay’s limited

skilled labor is to produce HDPs for internal transfer, up to the maximum number of units

Skilled labor time available at Hudson Bay ………………………………

40,000

hours

(1)

Produce 6,000 HDPs for external sale

Hours remaining …………………………………………………………………….

hours

(2)

Produce 10,000 HDPs for internal transfer

Hours remaining …………………………………………………………………….

hours

Hours remaining …………………………………………………………………….

Division.

3.

Given that 10,000 HDPs are transferred, there is no effect on General Instrumentation

4.

Hudson Bay’s minimum acceptable transfer price is given by the general transfer-

pricing rule, as follows:

Minimum acceptable transfer price

=

=

$70 + $36

=

additional outlay

costs incurred

because goods

+

opportunity

cost to the

organization

Chapter 13 – Investment Centers and Transfer Pricing

13–40

CASE 13-51 (CONTINUED)

Explanatory notes:

(b)

The opportunity cost is equal to the forgone contribution margin on the LDP

units that Hudson Bay will be unable to produce because it is manufacturing an

5.

The maximum transfer price that the Volkmar Tachometer Division would find

acceptable is $112, computed as follows:

Savings if TCH-320 is produced using an HDP:

Imported control pack ………………………………………………………………….

$145.00

Other raw material ……………………………………………………………………….

5.50

Total savings ……………………………………………………………………………….

$150.50

Less: Incremental costs if TCH-320 is produced using an HDP:

Transportation cost ……………………………………………………….…………….

Skilled labor ………………………………………………………………………………..

Net savings if HDP is used ………………………………………………………………..

$112.00

If Volkmar’s management must pay $112 for an HDP, it will be indifferent between using

6.

The transfer is in the overall company’s best interest. Thus, any transfer price in the

13–41

CASE 13-52 (45 MINUTES)

1. Yes, Air Comfort Division should institute the 5% price reduction on its air

conditioner units because net income would increase by $264,000. Supporting

calculations follow:

Before 5%

Price Reduction

After 5%

Price Reduction

Per

Unit

Total

(in thousands)

Per

Unit

Total

(in thousands)

Total

Difference

(in thousands)

Sales revenue

$800

$12,000

$760

$13,224.0

$1,224.0

Variable costs:

Compressor

$140

$ 2,100

$140

$ 2,436.0

$ 336.0

Other direct material

Direct labor

Variable overhead

Variable selling

540

626.4

86.4

Total variable costs

$400

$ 6,000

$400

$ 6,960.0

$ 960.0

Contribution margin

$400

$ 6,000

$360

$ 6,264.0

$ 264.0

Summarized presentation:

Contribution margin of sales increase ($360 2,400) $864,000

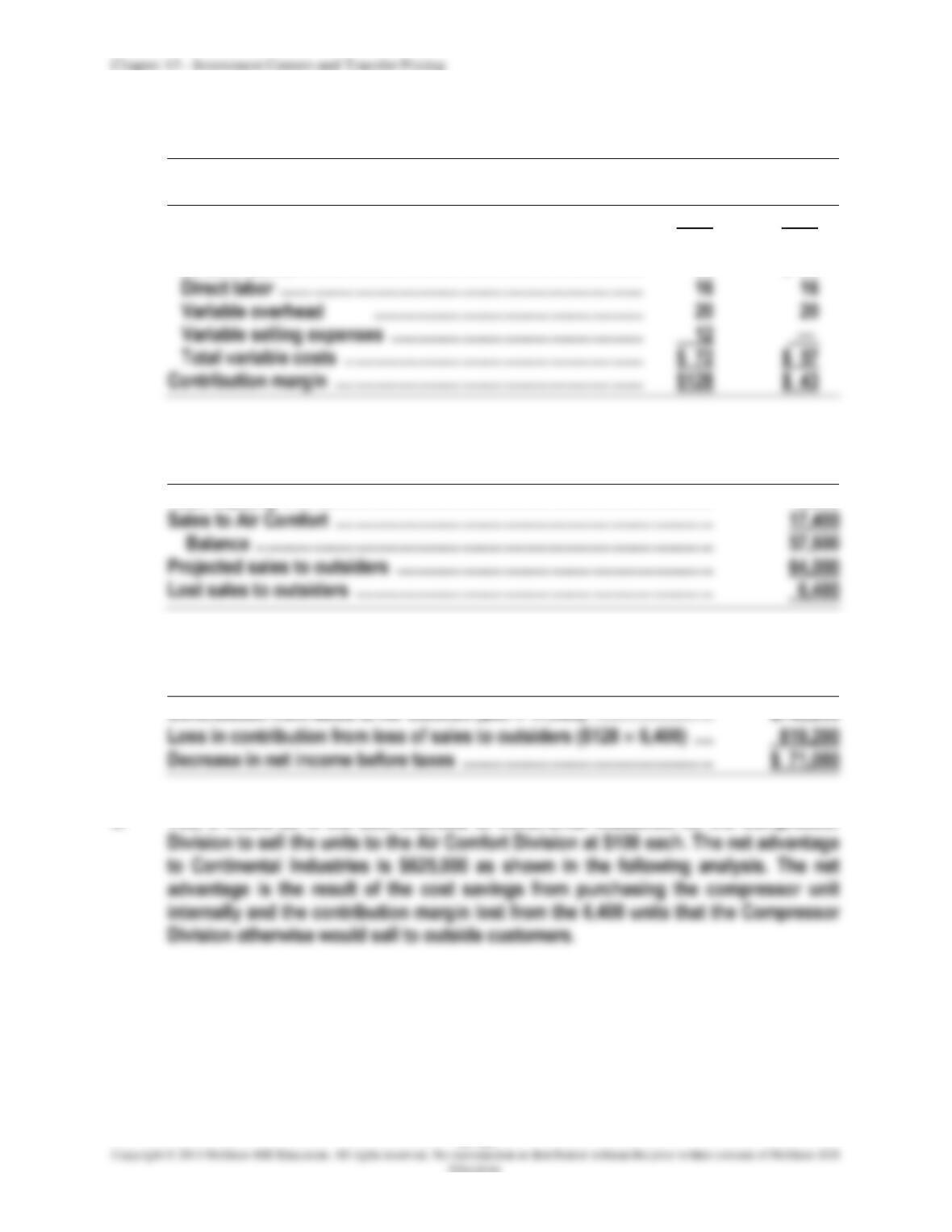

2. No, the Compressor Division should not sell all 17,400 units to the Air Comfort

Division for $100 each. If the Compressor Division does sell all 17,400 units to Air

13–42

CASE 13-52 (CONTINUED)

Outside

Sales

Air Comfort

Sales

Selling price …………………………………………………………………………………..

$200

$100

Variable costs:

Direct material ………………………………………………………………………………

24

$ 21

Direct labor ………………………………………………………………………………….

16

Variable overhead ……………………………………………………….

20

Variable selling expenses ……………………………………………………….

Total variable costs ……………………………………………………….

$ 57

Capacity calculation in units:

Total capacity ………………………………………………………………………………..

75,000

Sales to Air Comfort ………………………………………………………………………

17,400

Balance ……………………………………………………………………………………..

57,600

Projected sales to outsiders …………………………………………………………..

64,000

Solution:

Contribution from sales to Air Comfort ($43 17,400) ……………………..

$748,200

3. Yes, it would be in the best interests of Continental Industries for the Compressor

Chapter 13 – Investment Centers and Transfer Pricing

13–43

CASE 13-52 (CONTINUED)

Cost savings by using compressor unit from Compressor Division:

Air Comfort Division’s outside purchase price ……………………………….

$ 140

Compressor Division’s variable cost to produce (see req. 2). …………

57

Savings per unit ……………………………………………………………………………

$ 83

x Number of units ……………………………………………………………………..

x 17,400

Total cost savings …………………………………………………………………………

$1,444,200

819,200

4. As the answers to requirements (2) and (3) show, $100 is not a goal-congruent