This lecture consists of:

an overview

a ratio analysis

an interpretation of the ratio analysis.

Formal calculations are only the start. Ratios must be interpreted.

Overview

Identification of important trends over time

……YEAR PERIOD

Sales (revenue)

Net assets

O…………..……………………………………………….

P………….……………….………………………..……..

E……………..……………………………………………

For example, Craigielaw plc

Year 7 Year 6 Year 5

Financial Accounting

Purpose of ratio analysis

The aim is to build up a picture of the performance of the company.

Absolute figures are of little value. They only provide insights if they can be

……………………...….

……………………..…………..………………………………..…………………..

For example, (a) Sales compared to gross profits

(b) ………..…………………..…………….

Uses

1. Allows predictions to be made of likely increases in profit given an anticipated increased

level of sales

2. Provides data that allows a judgement to be made about achievements and levels of

performance

To determine whether these levels of achievement are satisfactory, we need standards for

comparison.

(i) Compare with earlier years.

……………………………………….…………………………………….?

……………………………………….…………………………………….?

(ii) Compare it with the companys plan.

………………………..………………..…………………………….……………………

………………………..………………..…………………………….……………………

………………………..………………..…………………………….……………………

………………………..………………..…………………………….………….…....

(iii) Compare with those of other companies in the same industry.

………………………..………………..…………………………….……………………

………………………..………………..…………………………….……………………

………………………..………………..…………………………….…….………..…

………………………..………………..…………………………….……………………

………………………..………………..…………………………….……………………

Financial Accounting

(iv) Compare with industrial average.

………………………..………………..…………………………….…………………..

………………………..………………..…………………………….……………….

………………………..………………..………………………..………….

………………………..………………..………………………..……..….

………………………..………………..……………………….…………..……

….………………..…………………………..………………….……..

….………………..…………………………..………………….……………..

….………………..…………………………..………………….………………

Additional comments

3. Ensure that the company has used consistent accounting policies over time.

4. No explicit attempt to take into account the effect of inflation……………..………………..……….

5. Many sources of information about competing companies performance:

6. Ratio analysis is a starting point in the interpretation of companies performance.

………………………………….………………………………..…………….………

………………………………….……………………………….……………….…….

………………………………….………………………………..……………..………

………………………………….………………………………..…………….………….

Financial Accounting

Systematic approach to ratio analysis

Lecture examples will calculate the ratios for Year 2.

After the lecture, calculate the ratios for Year 1 and attempt to comment on the picture

presented by these ratios.

Compare your calculations and comments with the textbook, Section 13.7

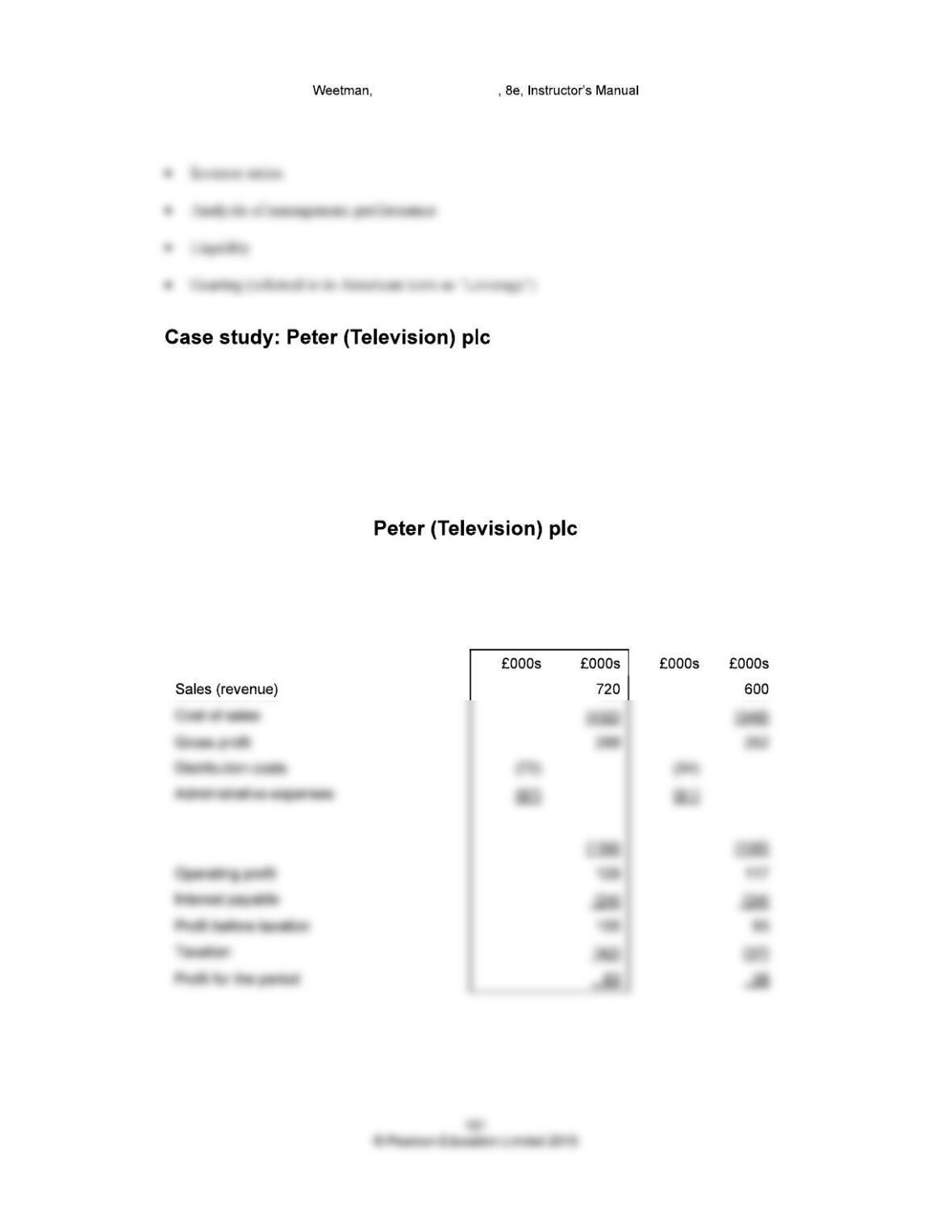

Income statement (profit and loss account)

for the year ended 31 December Year 2

Year 2 Year 1

Financial Accounting

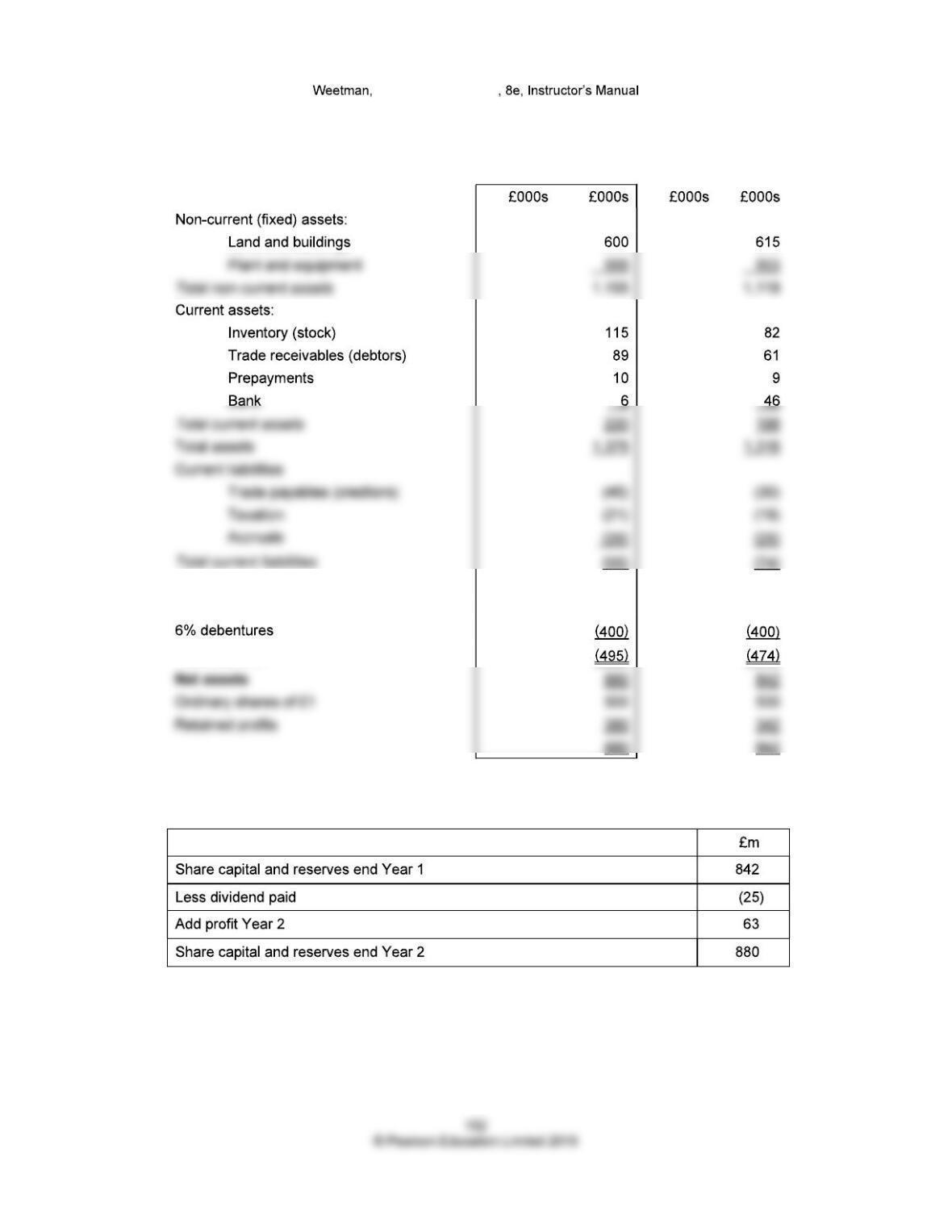

Statement of financial position (balance sheet) as on 31 December Year 2

Year 2 Year 1

Total liabilities

Statement of changes in equity

Market price on 1 March Year 2 202 pence

Market price on 1 March Year 3 277 pence

Financial Accounting

Directors propose a dividend of 6.0 pence per share.

Earnings per share Profit after tax for ordinary shareholders

Number of ordinary shares

Dividend per share Dividend payable to ordinary shareholders

Number of issued shares

Dividend yield Dividend per share ×100%

Share price

Financial Accounting

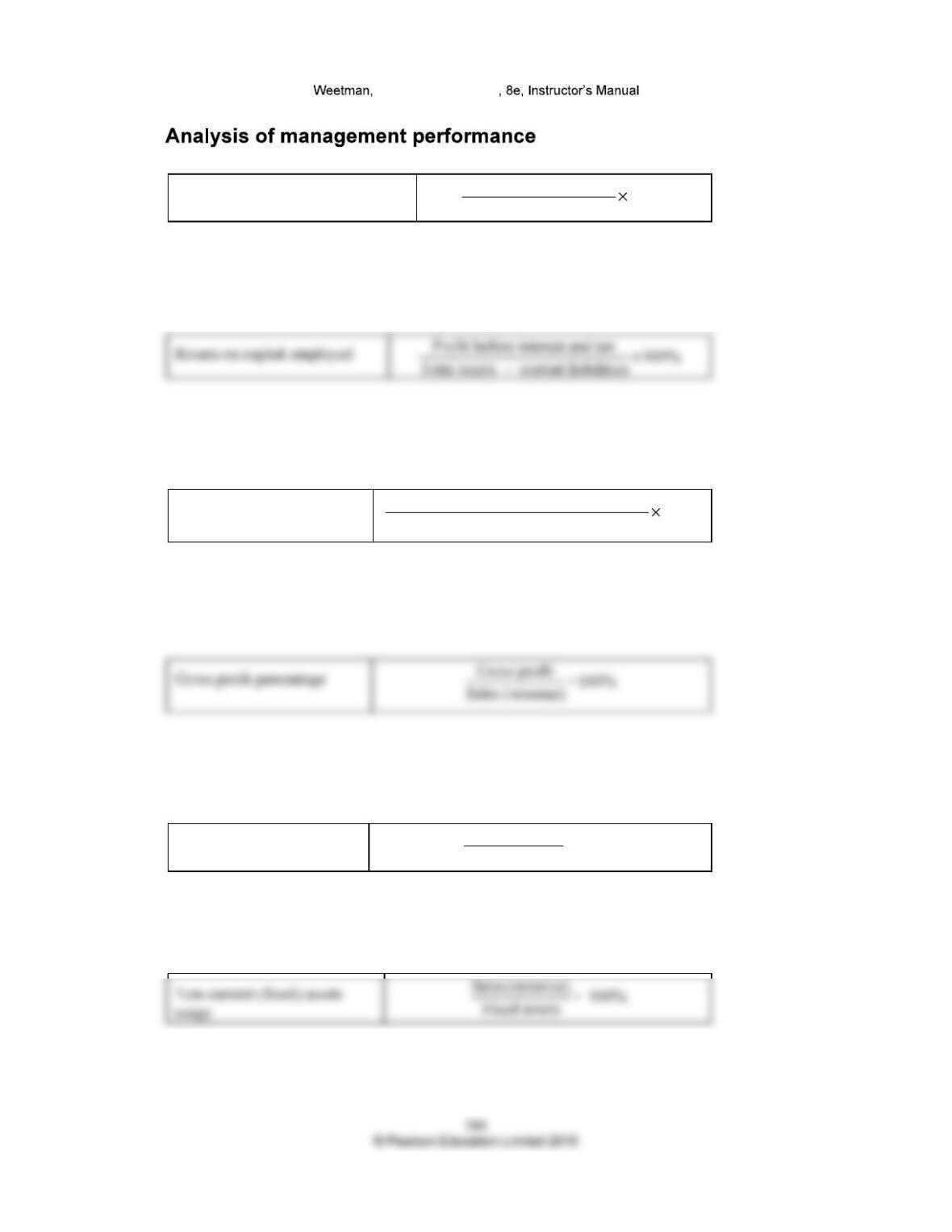

Return on shareholders equity Profit after tax 100%

Share capital + reserves

Operating profit on sales Operating profit (before interest and tax) 100%

Sales (revenue)

Total assets usage Sales (revenue) ×

Total assets 100%

Financial Accounting

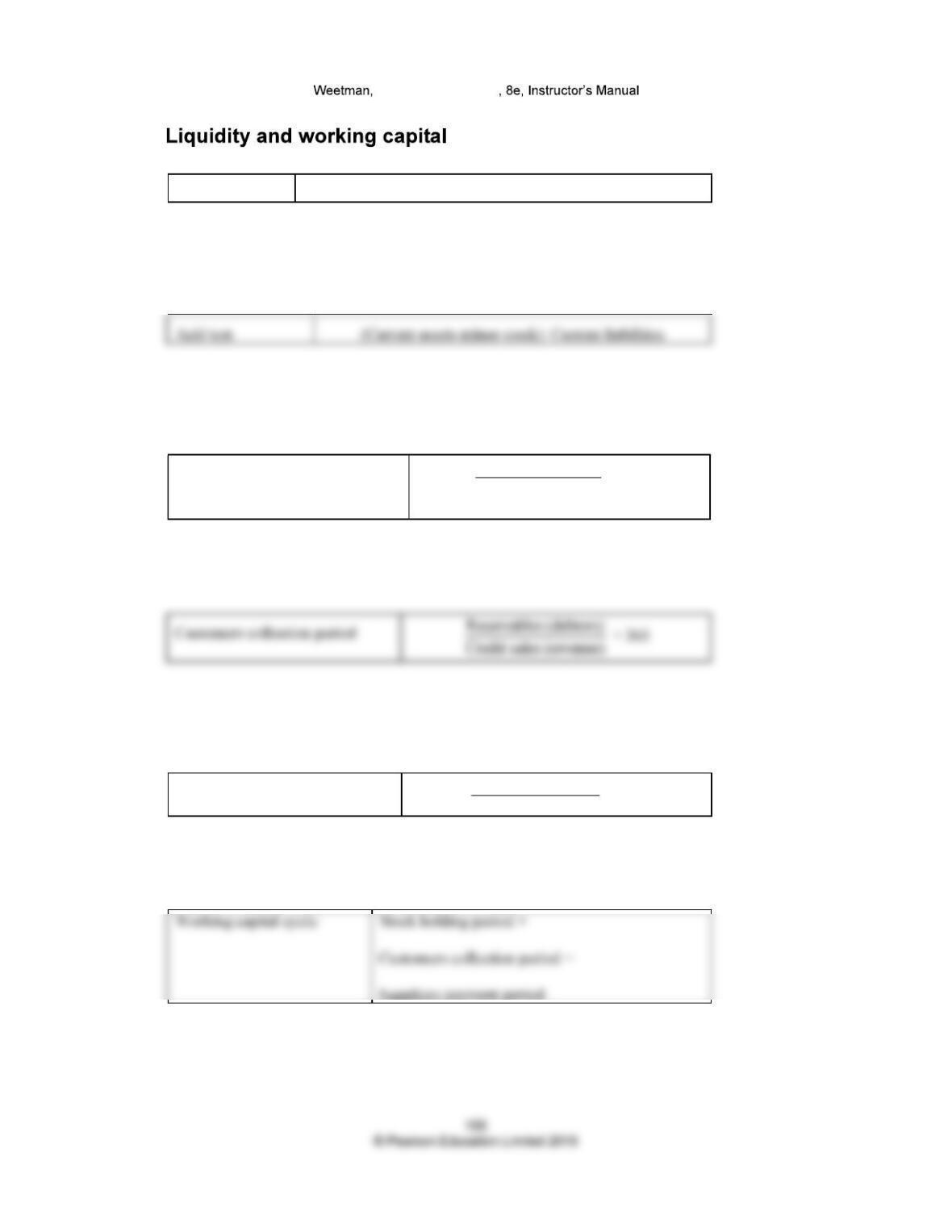

Current ratio Current assets: Current liabilities

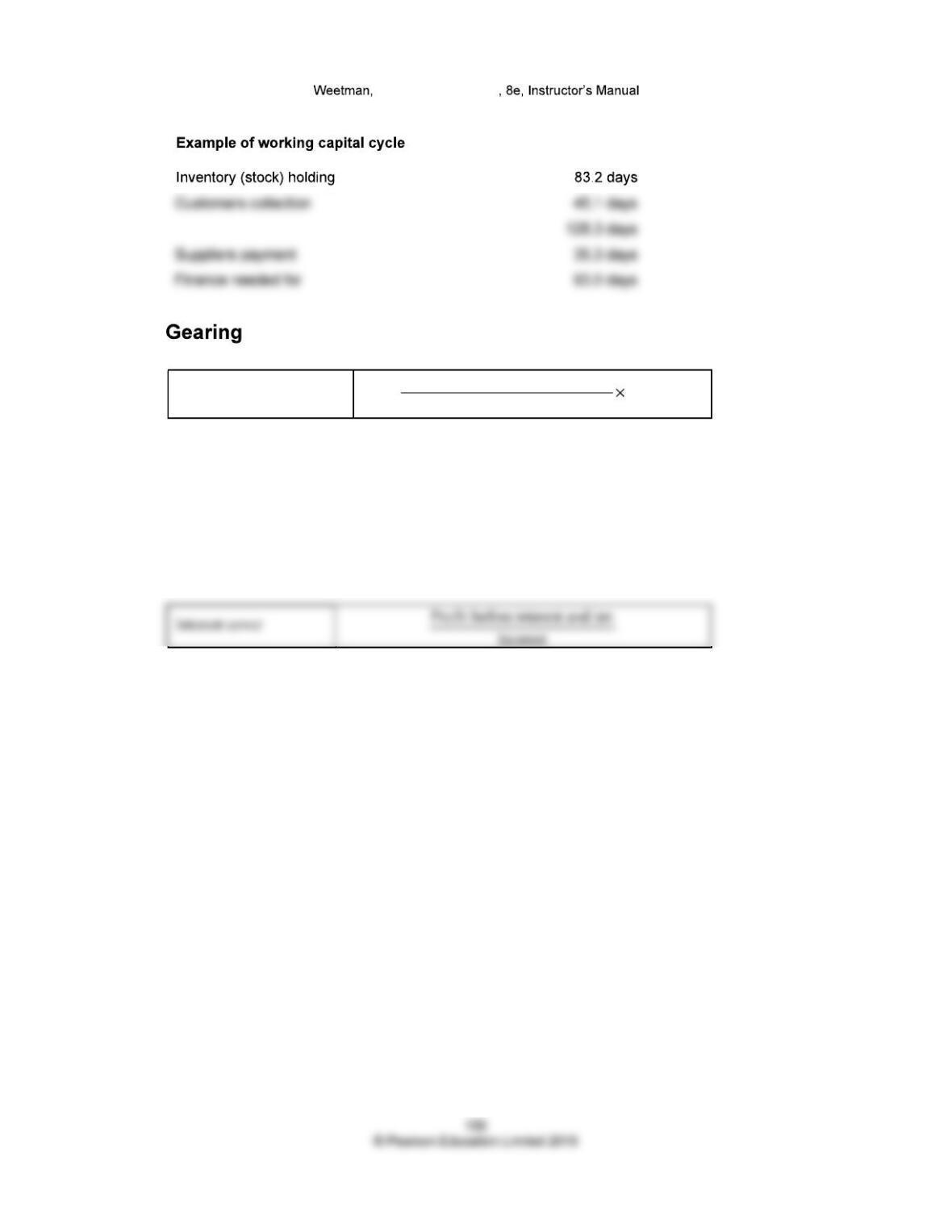

Inventory (stock) holding period

Average stock held

Cost of sales × 365

Suppliers payment period Payables (creditors)

Purchases × 365

Financial Accounting

Debt/equity ratio Long-term loans 100%

Ordinary share capital + reserves

Financial Accounting

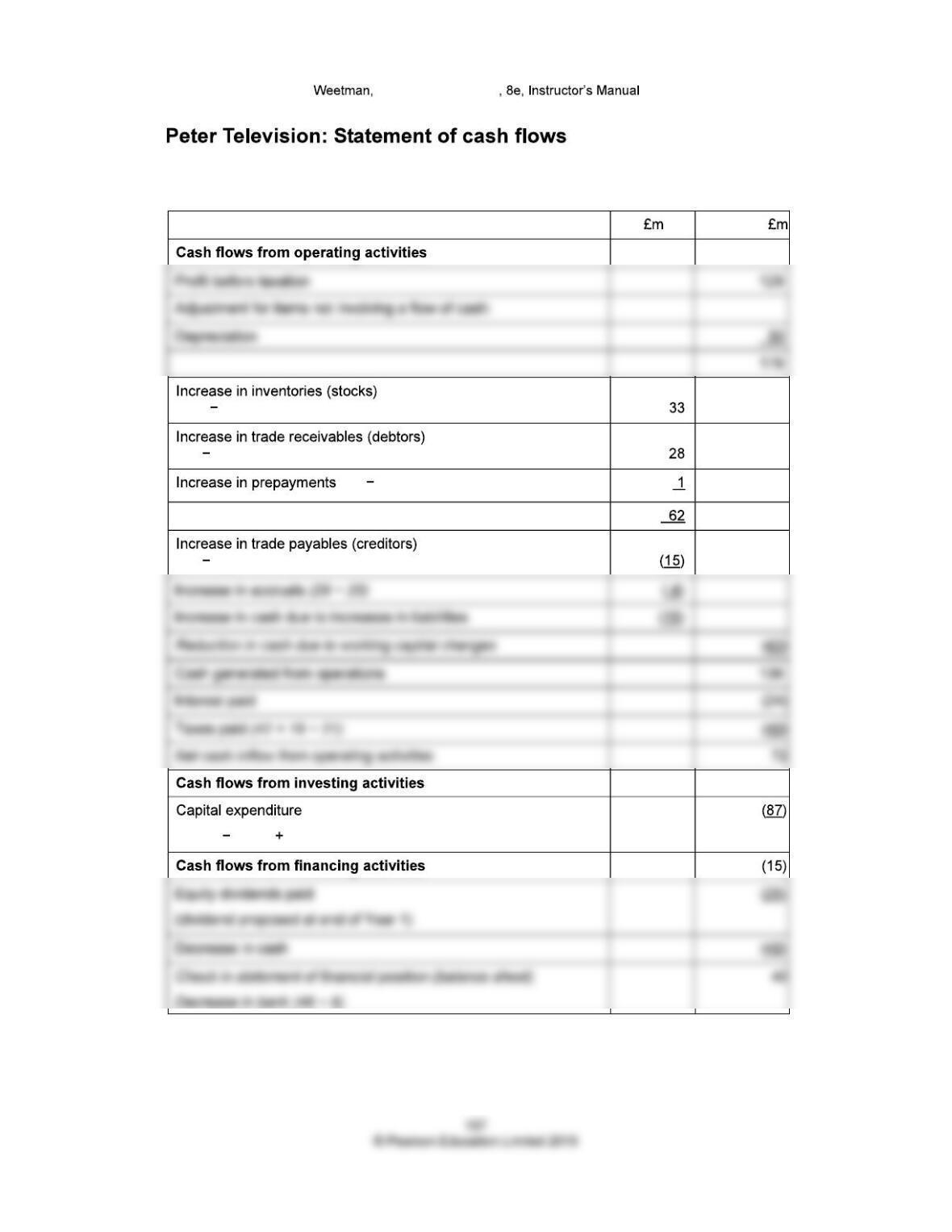

(Assume depreciation £50 million)

(115 82)

(89 61)

(10 9)

Reduction in cash due to increases in current assets

(45 30)

(1,155 1,118 50)

Financial Accounting

Earnings before deducting:

interest

taxation

Free cash flow