415

E13–23

a. Rate variance:

Direct Labor Rate Variance = (Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

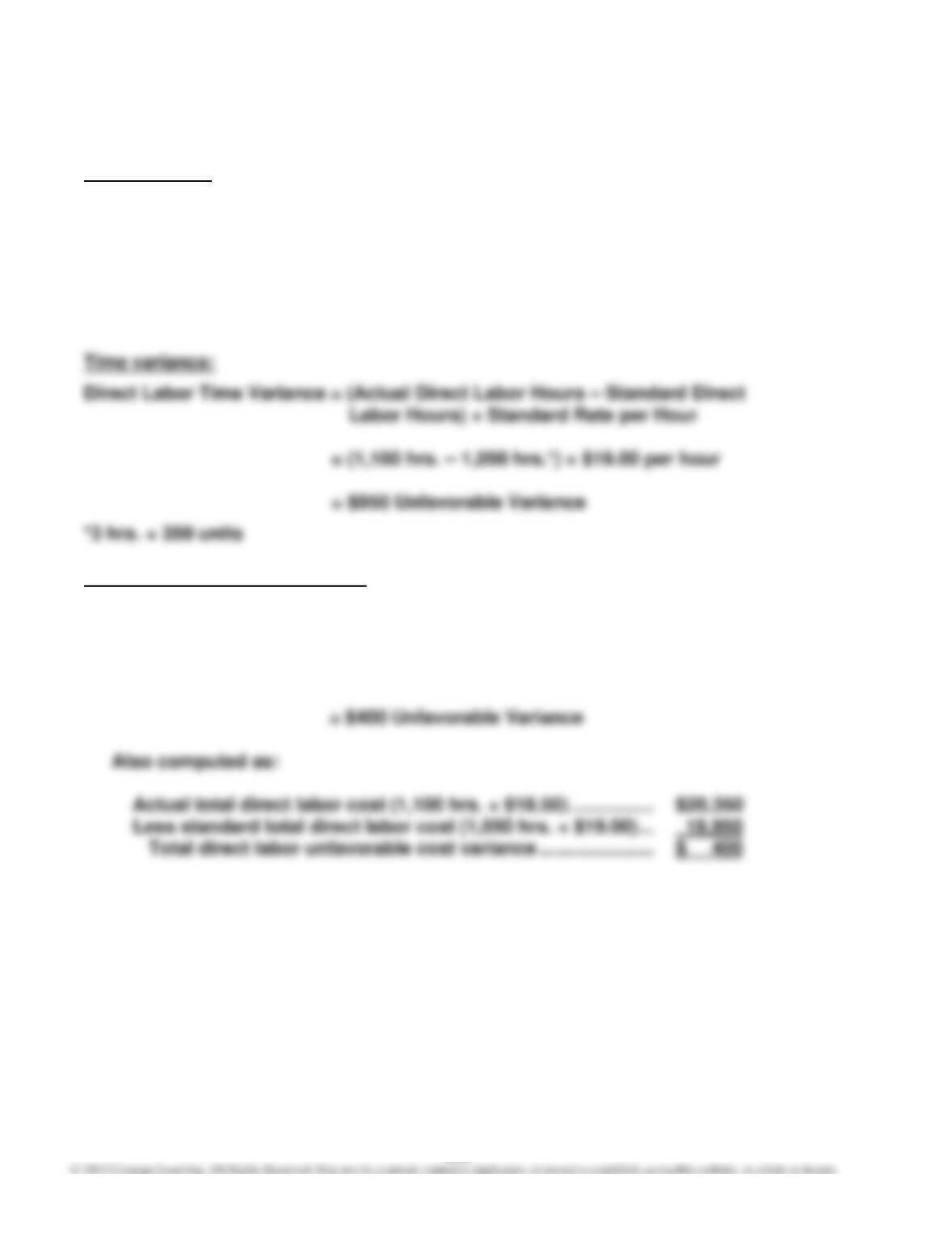

Time variance:

Direct Labor Time Variance = (Actual Direct Labor Hours – Standard Direct

Labor Hours) × Standard Rate per Hour

= (4,200 hrs. – 4,260 hrs.) × $16.75 per hour

= – $1,005 Favorable Variance

Also computed as:

Actual total direct labor cost ………………. $72,240

Less standard total direct labor cost …… 71,355

Total direct labor cost variance ………… $ 885 Unfavorable Variance

b. The employees may have been more experienced or better trained, thereby

416

E13–24

Rate variance:

Direct Labor Rate Variance = (Actual Rate per Hour – Standard Rate per Hour)

× Actual Hours

= ($18.50 – $19.00) × 1,100 hrs.

= – $550 Favorable Variance

Total direct labor cost variance:

Direct Labor Cost Variance = Direct Labor Rate Variance + Direct Labor Time

Variance

= – $550 + $950

417

E13–25

Step 1: Determine the standard direct materials and direct labor per unit.

Standard direct materials quantity per unit:

Direct materials lbs. budgeted for August:

lb. per $0.40

$15,000

= 37,500 lbs.

units 30,000

Step 2: Using the standard quantity and time rates in Step 1, determine the

standard costs for the actual August production.

Step 3: Determine the direct materials quantity and direct labor time variances,

assuming no direct materials price or direct labor rate variances.

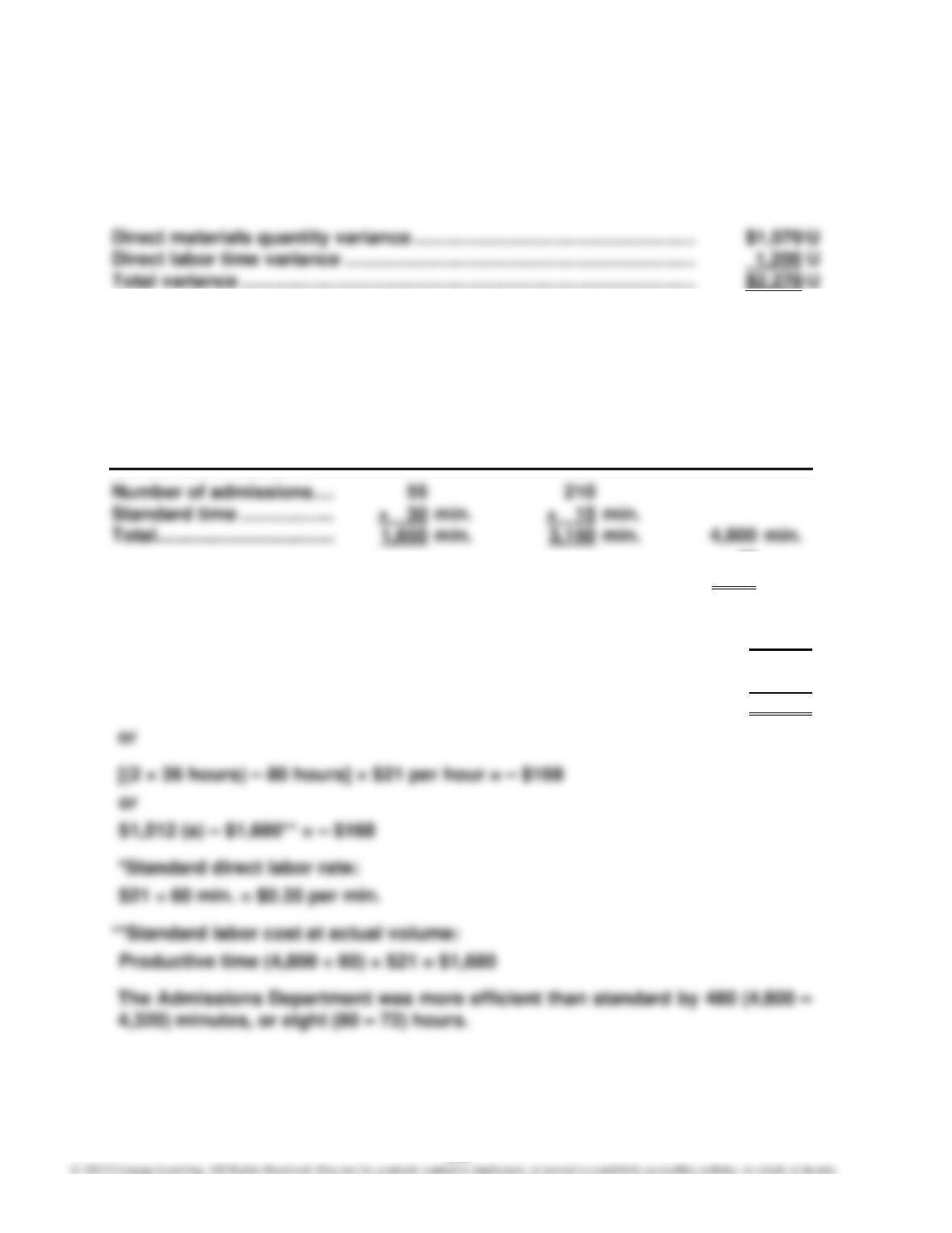

Actual direct materials used in production …………………………………. $13,320

Standard direct materials (Step 2) ……………………………………………… 12,250

Direct materials quantity variance—unfavorable ………………………… $ 1,070*

*(33,300 lbs. – 30,625 lbs.) × $0.40 = $1,070 U

$13,320 ÷ $0.40 = 33,300 lbs.

$12,250 ÷ $0.40 = 30,625 lbs. or 24,500 books × 1.25 lbs. = 30,625 lbs.

418

E13–25, Concluded

Step 4: Determine the total variance, assuming no direct materials price or direct

labor rate variances.

E13–26

a. Actual weekly expenditure: 2 people × $21 per hr. × 36 hrs. per week = $1,512

b. Standard time used for the volume of admissions:

Unscheduled Scheduled Total

or

80 hrs.

c. Actual minutes available (2 employees × 36 hrs. × 60 min.) … 4,320

Less standard minutes used at actual volume ……………………. 4,800

Favorable time difference from standard……………………………. – 480

Standard rate per minute…………………………………………………… × $0.35*

Direct labor time (efficiency) variance—favorable ………………. $ – 168

E13–27

a. Possible Input Measures

Registration staffing per student

Technology investment per period for registration process

Training hours per registration personnel

student

Number of times a replacement course was used by a student

Number of registration errors

Student satisfaction score with the registration process

Number of student complaints about registration process

420

E13–28

a. and b.

Input

Measure

Output

Measure

Explanation

lose customers.

Dollar amount of returned

X

An important measure of customer satis-

faction with the final product that was or-

dered.

Elapsed time between

customer order and prod–

uct delivery

An important overall measure of process

responsiveness. If the company is too slow

in providing product, we may lose custom-

ers.

Average computer

response time to custom-

X

A measure of the speed of the ordering

process. If the speed is too slow, we may

Maintenance dollars

divided by hardware

investment

X

across time.

Number of customer

complaints divided by the

number of orders

X

An extreme measure of customer dissatis-

faction with the ordering process.

Number of orders per

warehouse employee

This measure is related to the capacity of

the warehouse relative to the demands

placed upon it. This relationship will impact

the delivery cycle time.

A driver of the ordering system’s reliability

and downtime. The maintenance dollars

should be scaled to the amount of hard-

ware in order to facilitate comparison

Number of page faults or

errors due to software

programming errors

X

The page errors will negatively impact the

customer’s ordering experience. It’s a

measure of process output quality.

Number of software fixes

per week

X

Software bugs reduce the effectiveness of

the order fulfillment system; thus, fixes are

an input that will improve the performance

of the order fulfillment system.

Server (computer) down–

time

A measure of computer system reliability.

Training dollars per pro-

grammer

Trained programmers should enhance the

421

Appendix: E13–29

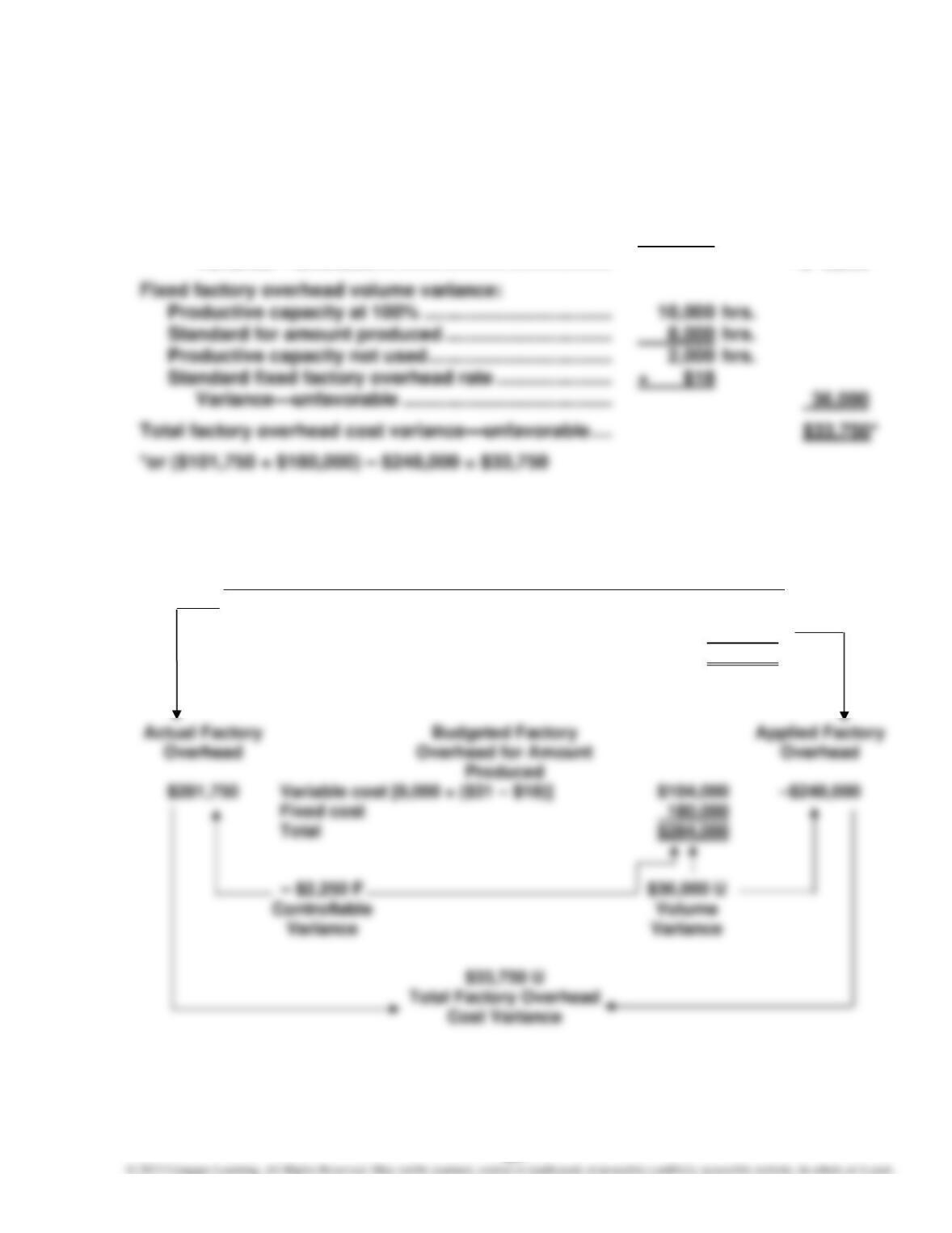

Variable factory overhead controllable variance:

Actual variable factory overhead cost incurred …… $101,750

Budgeted variable factory overhead for 8,000 hrs.

[8,000 × ($31 – $18)] ……………………………………… 104,000

Variance—favorable ……………………………………… –$ 2,250

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs ($101,750 + $180,000)

$281,750

Applied costs (8,000 hrs. × $31)

–248,000

Balance, underapplied factory overhead

$ 33,750

422

Appendix: E13–30

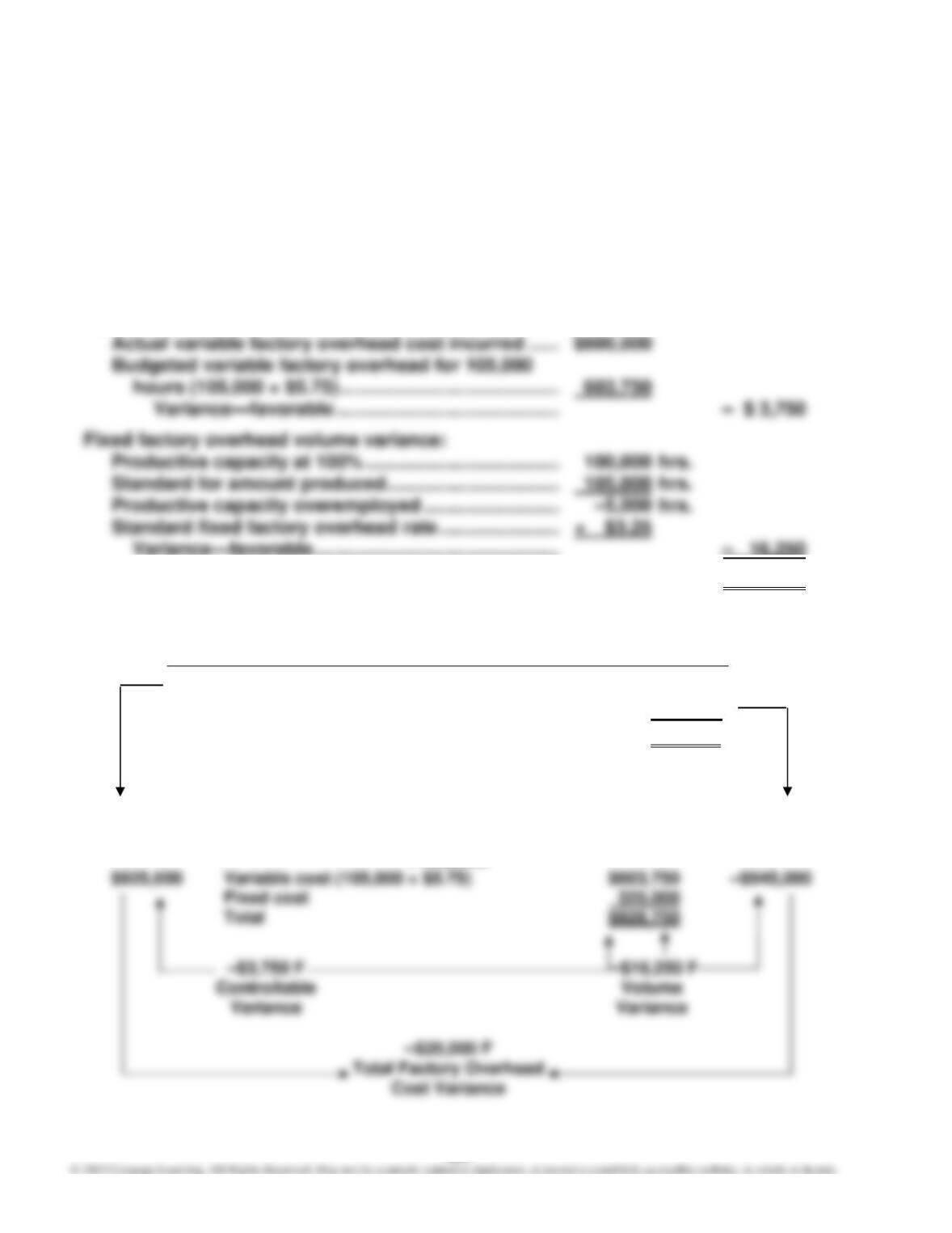

a. Controllable variance:

Actual variable factory overhead

($1,428,000 – $300,000) …………………….. $1,128,000

Standard variable factory overhead at

b. Volume variance:

Volume at 100% of normal capacity ……………. 60,000

Less standard hours ………………………………….. 52,000

Idle capacity ……………………………………………… 8,000

Fixed overhead rate2 ………………………………….. × $5

423

Appendix: E13–30, Concluded

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs

$1,428,000

Applied costs ($27 × 52,000 hrs.)

1,404,000

Balance, underapplied factory overhead

$ 24,000

424

Appendix: E13–31

In determining the volume variance, the productive capacity overemployed (5,000

hours) should be multiplied by the standard fixed factory overhead rate of $3.25

($9.00 – $5.75) to yield a favorable variance of $16,250. The variance analysis pro-

vided by the chief cost accountant incorrectly multiplied the 5,000 hours by the

total factory overhead rate of $9.00 per hour and reported it as unfavorable.

A correct determination of the factory overhead cost variances is as follows:

Variable factory overhead controllable variance:

Total factory overhead cost variance—favorable ……… – $20,000

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs ($600,000 + $325,000)

$925,000

Applied costs (105,000 hrs. × $9.00)

–945,000

Balance, overapplied factory overhead

–$ 20,000

Actual Factory Budgeted Factory Applied Factory

Overhead Overhead for Amount Overhead

Produced

Appendix: E13–32

A

B

C

D

E

1

TOPEKA PLASTICS INC.

2

Factory Overhead Cost Variance Report—Trim Department

3

For the Month Ended July 31

4

Productive capacity for the month

30,000 hrs.

5

Actual productive capacity used for the month

28,000 hrs.

6

Budget

7

at actual

8

production of

Actual

Variances

9

28,000 hrs.

Cost

Favorable

Unfavorable

10

Variable factory overhead cost:*

$ 22,400

$ 850

20,160

13

Indirect materials

10,080

11,100

Total variable factory overhead

$ 52,640

$ 54,350

15

Fixed factory overhead cost:

16

Supervisory salaries

$ 50,000

$ 50,000

17

Depreciation of plant and

equipment

33,100

33,100

18

Insurance and property taxes

11,400

11,400

19

Total fixed factory overhead

cost

$ 94,500

$ 94,500

20

Total factory overhead cost

$147,140

$148,850

22

23

Net controllable variance—unfavorable

$1,710

24

Volume variance—unfavorable:

25

Idle hours at the standard rate for fixed factory overhead—

6,300

*The budgeted variable factory overhead costs are determined by multiplying

28,000 hours by the variable factory overhead cost rate for each variable cost

category. These rates are determined by dividing each budgeted amount (esti-

mated at the beginning of the month) by the planned (budgeted) volume of

25,000 hours as shown below.

426

Appendix: E13–32, Concluded

Alternative Computation of Overhead Variances

Factory Overhead

Actual costs

$148,850

Applied costs [28,000 × ($1.88* + $3.15)]

140,840

Balance, underapplied factory overhead

$ 8,010

*$47,000 ÷ 25,000 hours budgeted at the beginning of the month

427

PROBLEMS

P13–1

1.

A

B

C

D

1

ROYAL BRITISH FURNITURE COMPANY

2

Sales Budget

3

For the Month Ending March 31

Unit Sales

Unit Selling

4

Product and Area

Volume

Price

Total Sales

5

William:

6

Eastern Domestic

7,500

$800

$ 6,000,000

7

Western Domestic

6,000

700

4,200,000

8

International

600

Eastern Domestic

$650

$ 3,900,000

Western Domestic

5,000

550

International

350

$ 7,000,000

2.

A

B

C

1

ROYAL BRITISH FURNITURE COMPANY

2

Production Budget

3

For the Month Ending March 31

4

Units

5

William

Kate

6

Expected units to be sold

16,000

12,000

7

Plus desired inventory, March 31

8

Total

18,000

P13–1, Continued

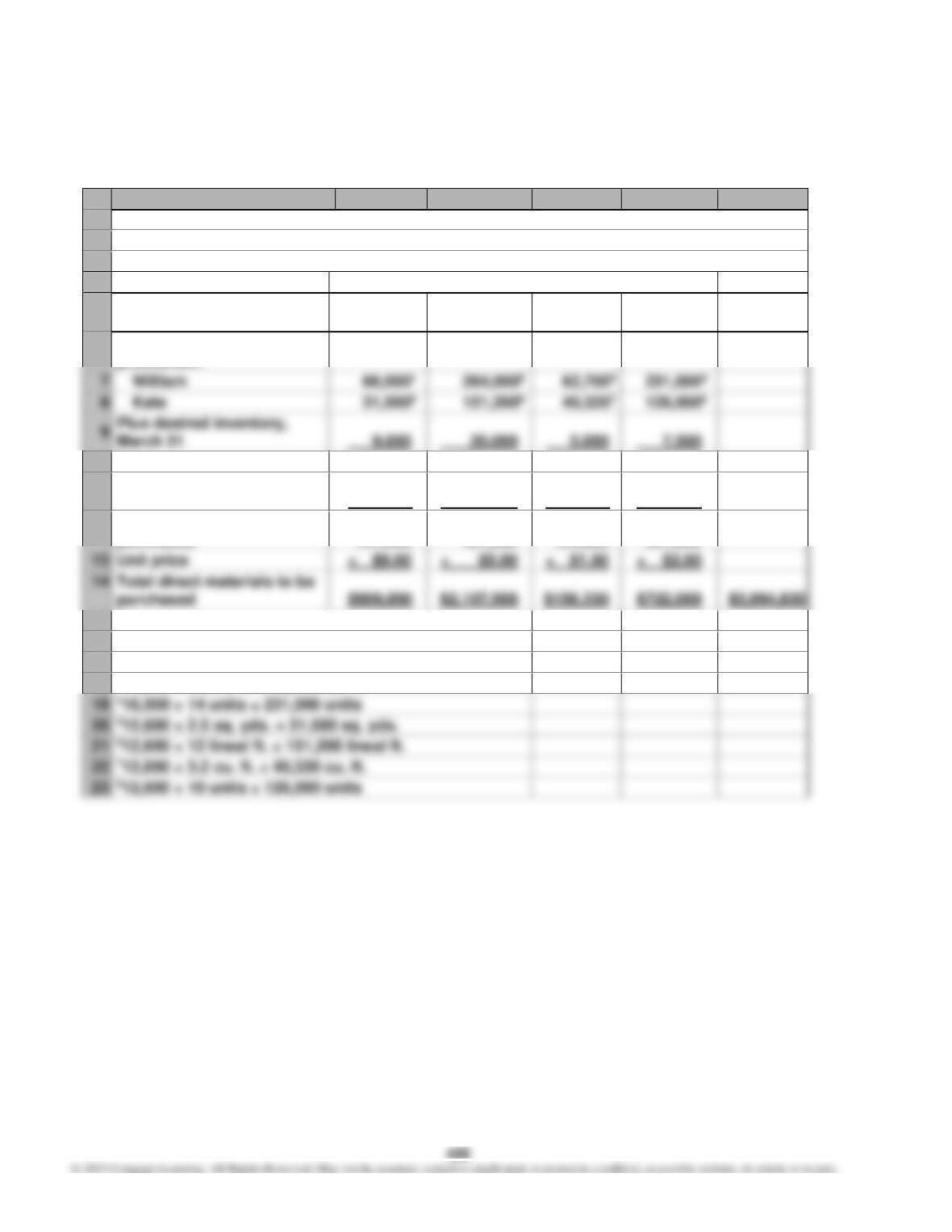

3.

A

B

C

D

E

F

1

ROYAL BRITISH FURNITURE COMPANY

2

Direct Materials Purchases Budget

3

For the Month Ending March 31

4

Direct Materials

5

Fabric

(sq. yds.)

Wood

(lineal ft.)

Filler

(cu. ft.)

Springs

(units)

Total

6

Required units for

production:

William

66,0001

264,0002

62,7003

231,0004

Kate

31,5005

151,2006

40,3207

126,0008

Plus desired inventory,

March 31

9,000

20,000

5,000

10

Total

106,500

435,200

108,020

364,500

11

Less estimated inventory,

March 1

5,500

13,700

3,800

3,500

12

Total units to be

purchased

101,000

421,500

104,220

361,000

13

Unit price

× $9.00

× $5.00

× $1.50

× $2.00

15

16

116,500 × 4.0 yds. = 66,000 sq. yds.

17

216,500 × 16 lineal ft. = 264,000 lineal ft.

18

316,500 × 3.8 cu. ft. = 62,700 cu. ft.

19

416,500 × 14 units = 231,000 units

20

512,600 × 2.5 sq. yds. = 31,500 sq. yds.

21

612,600 × 12 lineal ft. = 151,200 lineal ft.

22

712,600 × 3.2 cu. ft. = 40,320 cu. ft.

23

812,600 × 10 units = 126,000 units

429

P13–1, Concluded

4.

A

B

C

D

E

1

ROYAL BRITISH FURNITURE COMPANY

2

Direct Labor Cost Budget

3

For the Month Ending March 31

4

Framing

Department

Cutting

Department

Upholstery

Department

Total

5

Hours required for production:

6

William*

41,250

16,500

49,500

7

Kate**

18,900

6,300

25,200

8

Total

60,150

22,800

74,700

9

Hourly rate

× $15.00

× $12.00

× $16.00

10

Total direct labor cost

$902,250

$273,600

$1,195,200

$2,371,050

41,250 = 16,500 × 2.5; 16,500 = 16,500 × 1.0; 49,500 = 16,500 × 3.0

the hours per unit in each department estimated for the Kate chairs.

18,900 = 12,600 × 1.5; 6,300 = 12,600 × 0.5; 25,200 = 12,600 × 2.0

430

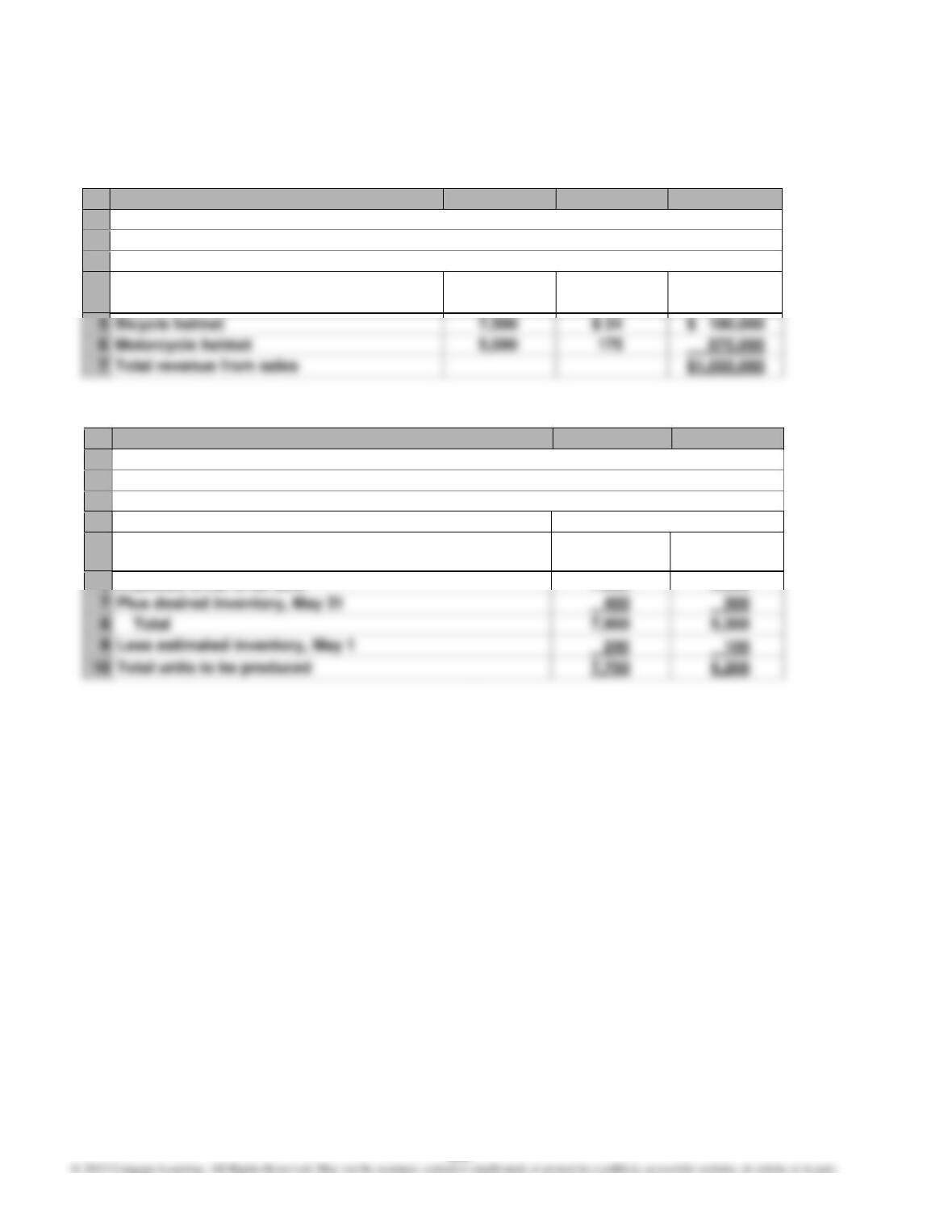

P13–2

1.

A

B

C

D

1

JUPITER HELMETS INC.

2

Sales Budget

3

For the Month Ending May 31

4

Unit Sales

Unit Selling

Volume

Price

Total Sales

5

Bicycle helmet

6

Motorcycle helmet

2.

A

B

C

1

JUPITER HELMETS INC.

2

Production Budget

3

For the Month Ending May 31

4

Units

5

Bicycle

Helmet

Motorcycle

Helmet

6

Expected units to be sold

7,500

5,000

7

Plus desired inventory, May 31

8

Total

431

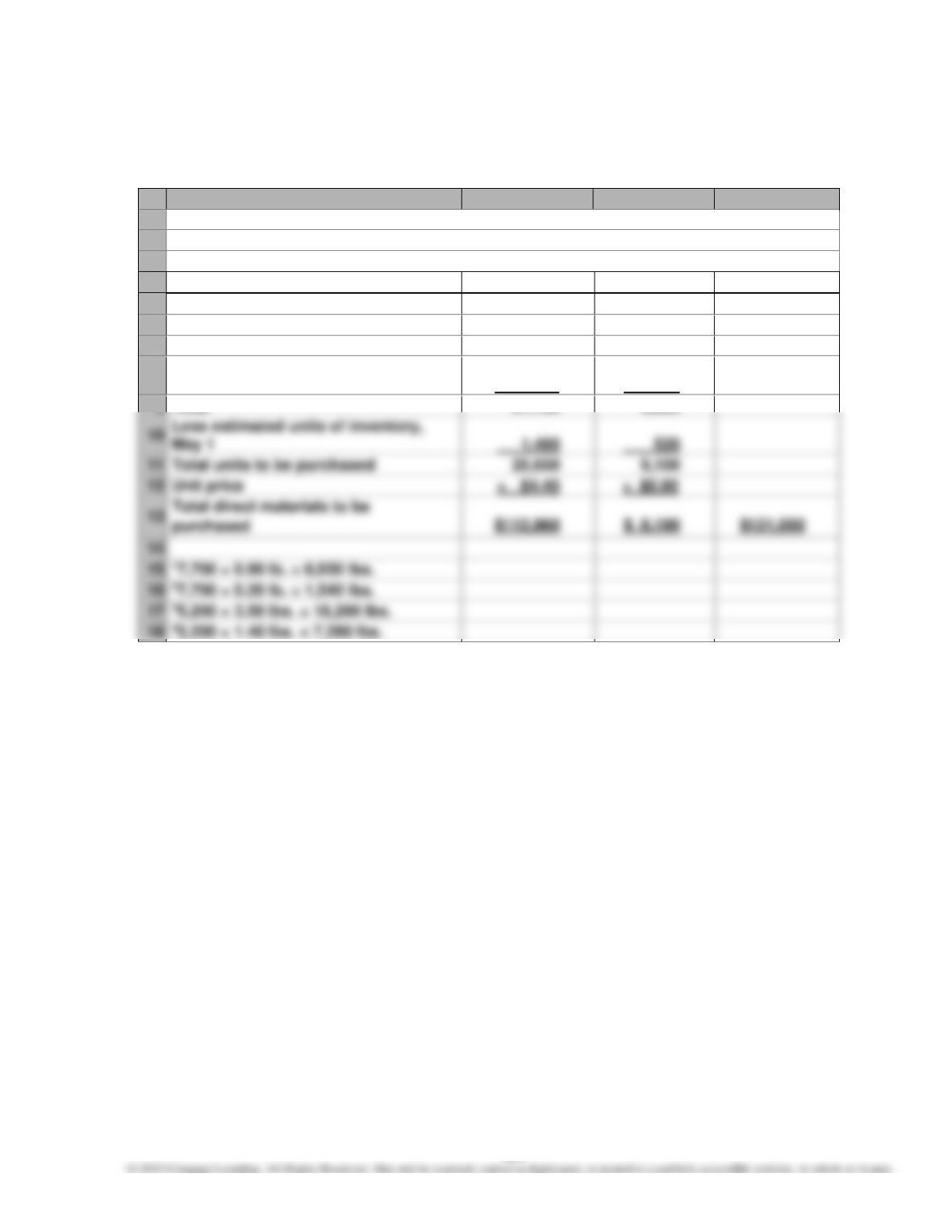

P13–2, Continued

3.

A

B

C

D

1

JUPITER HELMETS INC.

2

Direct Materials Purchases Budget

3

For the Month Ending May 31

4

Plastic

Foam Lining

Total

5

Units required for production:

6

Bicycle helmet

6,9301

1,5402

7

Motorcycle helmet

18,2003

7,2804

8

Plus desired units of inventory,

May 31

2,000

800

9

Total

27,130

9,620

Total units to be purchased

9,100

Unit price

× $4.40

× $0.90

17,700 × 0.90 lb. = 6,930 lbs.

27,700 × 0.20 lb. = 1,540 lbs.

35,200 × 3.50 lbs. = 18,200 lbs.

45,200 × 1.40 lbs. = 7,280 lbs.

432

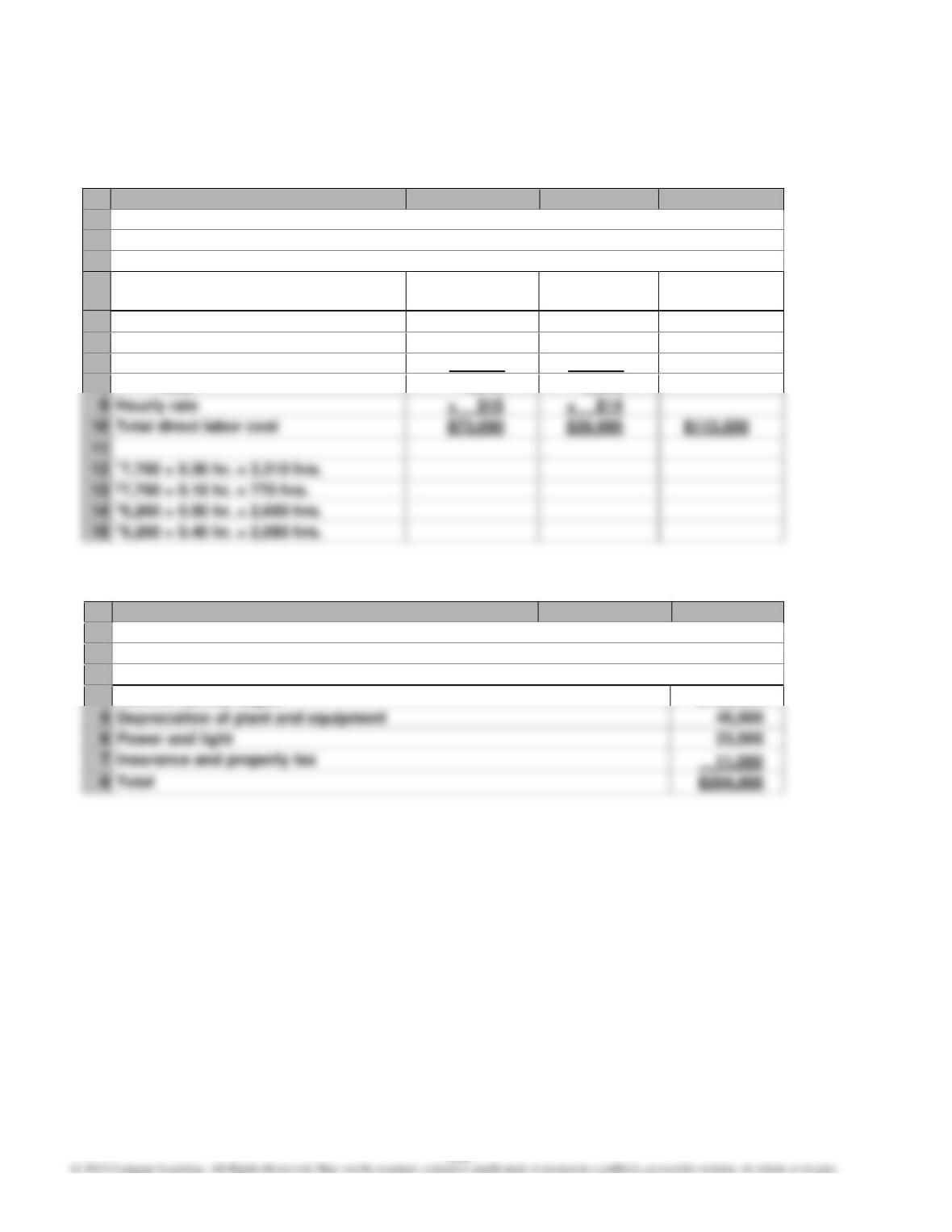

P13–2, Continued

4.

A

B

C

D

1

JUPITER HELMETS INC.

2

Direct Labor Cost Budget

3

For the Month Ending May 31

4

Molding

Department

Assembly

Department

Total

5

Hours required for production:

6

Bicycle helmet

2,3101

7702

7

Motorcycle helmet

2,6003

2,0804

8

Total

4,910

2,850

9

Hourly rate

× $15

× $14

17,700 × 0.30 hr. = 2,310 hrs.

27,700 × 0.10 hr. = 770 hrs.

35,200 × 0.50 hr. = 2,600 hrs.

45,200 × 0.40 hr. = 2,080 hrs.

5.

A

B

C

1

JUPITER HELMETS INC.

2

Factory Overhead Cost Budget

3

For the Month Ending May 31

4

Indirect factory wages

$125,000

5

Depreciation of plant and equipment

6

Power and light

433

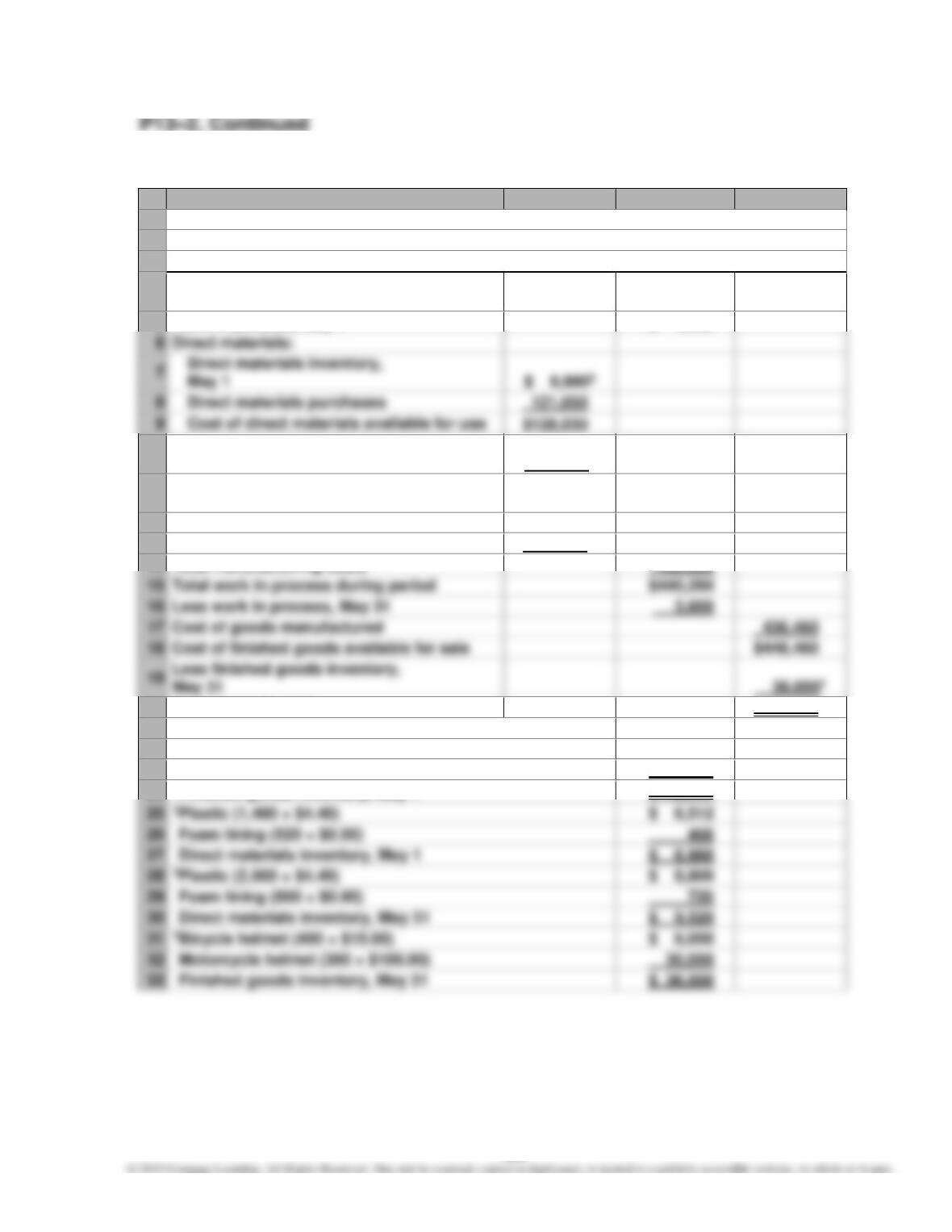

6.

A

B

C

D

1

JUPITER HELMETS INC.

2

Cost of Goods Sold Budget

3

For the Month Ending May 31

4

Finished goods inventory,

May 1

$ 12,0001

5

Work in process, May 1

$ 4,200

6

7

Direct materials inventory,

May 1

$ 6,9802

8

Direct materials purchases

121,050

Cost of direct materials available for use

$128,030

10

Less direct materials inventory,

May 31

9,5203

11

Cost of direct materials placed in

production

$118,510

12

Direct labor

113,550

13

Factory overhead

204,000

14

Total manufacturing costs

436,060

15

Total work in process during period

$440,260

16

Less work in process, May 31

17

Cost of goods manufactured

436,460

18

Cost of finished goods available for sale

$448,460

19

Less finished goods inventory,

20

Cost of goods sold

$412,460

21

22

1Bicycle helmet (200 × $15.00)

$ 3,000

23

Motorcycle helmet (100 × $90.00)

9,000

24

Finished goods inventory, May 1

$ 12,000

25

2Plastic (1,480 × $4.40)

$ 6,512

26

Foam lining (520 × $0.90)

468

27

Direct materials inventory, May 1

$ 6,980

28

3Plastic (2,000 × $4.40)

$ 8,800

29

Foam lining (800 × $0.90)

720

30

Direct materials inventory, May 31

$ 9,520

31

4Bicycle helmet (400 × $15.00)

$ 6,000

32

Motorcycle helmet (300 × $100.00)

30,000

33

Finished goods inventory, May 31

$ 36,000