CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN)

LEAN MANUFACTURING AND ACTIVITY ANALYSIS

DISCUSSION QUESTIONS

1. The lean philosophy focuses on reducing time, cost, and poor quality within manufacturing

and nonmanufacturing processes.

2. Move time and wait time in inventory are examples of non-value-added lead time.

5. Pull or “make to order” manufacturing requires the manufacturer to build product only as it is

needed for actual customer orders. As a result, finished goods, work in process, and materials

inventories are minimized. Make to order manufacturing requires a high degree of flexibility and

insignificant setup costs.

6. Product defects can cause additional costs and unpredictability in the process in the form of

scrap, rework, record keeping, and inspection. In addition, product defects can cause a

process to shut down, because there is very little work in process inventory to keep the next

(downstream) operations running. Thus, a lean manufacturer would wish to eliminate the

negative consequences of product defects.

8. A lean environment will result in fewer (or no) work in process control points. As a result,

there are no in-process transactions into and out of work in process inventory locations

throughout the process. The lean accounting system backflushes cost to finished product

rather than pushing cost through intermediate work in process departments.

9. The raw and in process inventory account combines the materials and work in process

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

DISCUSSION QUESTIONS (Concluded)

11. A Pareto chart shows the totals of a particular attribute for a number of categories. The

categories are ranked and displayed left to right, so that the largest total is on the left and the

smallest total is on the right. In this way, management can quickly identify important

problems.

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

BASIC EXERCISES

BE 27–1 (FIN MAN); BE 13–1 (MAN)

a.

Value-added lead time ………………………………

25

min. (5 min. + 20 min.)

Total within-batch wait time …………………

Move time …………………………………………..

Total lead time …………………………………………

1,002

Non-value-added lead time:

BE 27–2 (FIN MAN); BE 13–2 (MAN)

BE 27–3 (FIN MAN); BE 13–3 (MAN)

a.

Raw and In Process Inventory

15,000

Accounts Payable

15,000

To record materials purchases

Raw and In Process Inventory

36,000

Conversion Costs

36,000

To record applied conversion costs

× 600 units}.

c.

Finished Goods Inventory

40,500

Raw and In Process Inventory

40,500

To transfer the cost of completed units to

finished goods [($30 + $60) × 450 units].

($30 per unit × 500 units).

BE 27–4 (FIN MAN); BE 13–4 (MAN)

Cost of Quality Report

Quality Cost Classification

Quality

Cost

Percent of

Total Quality

Cost

Percent of

Total

Sales

Prevention (employee training) ……………..

$265,000

53%

6.6%

Appraisal (inspecting rooms) ………………..

175,000

35%

4.4%

Internal failure (reworking room

service meals) …………………………………

20,000

4%

0.5%

External failure (processing lost

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

BE 27–5 (FIN MAN); BE 13–5 (MAN)

Inspection activity before improvement ……….

$105,600 ÷ 40,000 units = $2.64 per unit

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

EXERCISES

Ex. 27–1 (FIN MAN); Ex. 13–1 (MAN)

The CEO must not have been reading the article very carefully. Lean manufacturing is

not primarily an inventory reduction method. Lean manufacturing is a process

improvement philosophy that focuses on reducing time, cost, poor quality, and

uncertainty from a process. Large inventories are merely a symptom of poorly designed

In addition, the CEO has not provided the training or action plan for moving to lean

manufacturing. The CEO has only commanded that it be done. This will create anxiety in

the workforce, and it is not consistent with employee involvement.

Ex. 27–2 (FIN MAN); Ex. 13–2 (MAN)

This is an actual situation facing the U.S. apparel industry. Warren Featherbone and

other U.S.-based apparel manufacturers are discovering the strategic power of lean

manufacturing. Rather than competing with the offshore manufacturers on price,

these companies are providing smaller quantities with much faster delivery. The

retailer is able to order and receive goods in smaller, more frequent batch sizes. As a

result, the retailer is able to move with fashion trends much more quickly. For

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–3 (FIN MAN); Ex. 13–3 (MAN)

Piecework compensation is a characteristic of a traditional manufacturing philosophy

that is inconsistent with lean manufacturing. Under lean manufacturing, workers are

viewed not just as laborers but as valuable assets of the company. The company wants

workers to also bring their minds to the job. Thus, workers should be compensated for

contributing to process improvements, for training themselves to work other jobs in the

Ex. 27–4 (FIN MAN); Ex. 13–4 (MAN)

Management is incorrect in stating that the direct labor time is equal to the lead time. The

lead time also includes the wait time and other non-value-added time required to make the

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–5 (FIN MAN); Ex. 13–5 (MAN)

a. Long setup times have two negative consequences. First, a long setup time

consumes valuable machine capacity that could be used for productive purposes.

b. One obvious improvement would be to limit the trips to the tool room to one round

trip, rather than two. However, even this could be improved upon by changing the

location of the fixtures. Changing the location of the fixtures could significantly

reduce the lathe setup time. Instead of using a tool room to control the fixtures, the

appropriate fixtures for the lathe could be located at the lathe operation. In this case,

c.

Turn off machine and remove fixture from lathe ……….

15

minutes

Clean lathe …………………………………………………………….

20

Install new fixture and turn on machine ……………………

5

Total setup time ………………………………………………..

40

minutes*

*

Plus time for replacing and retrieving a tool at a point of use.

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

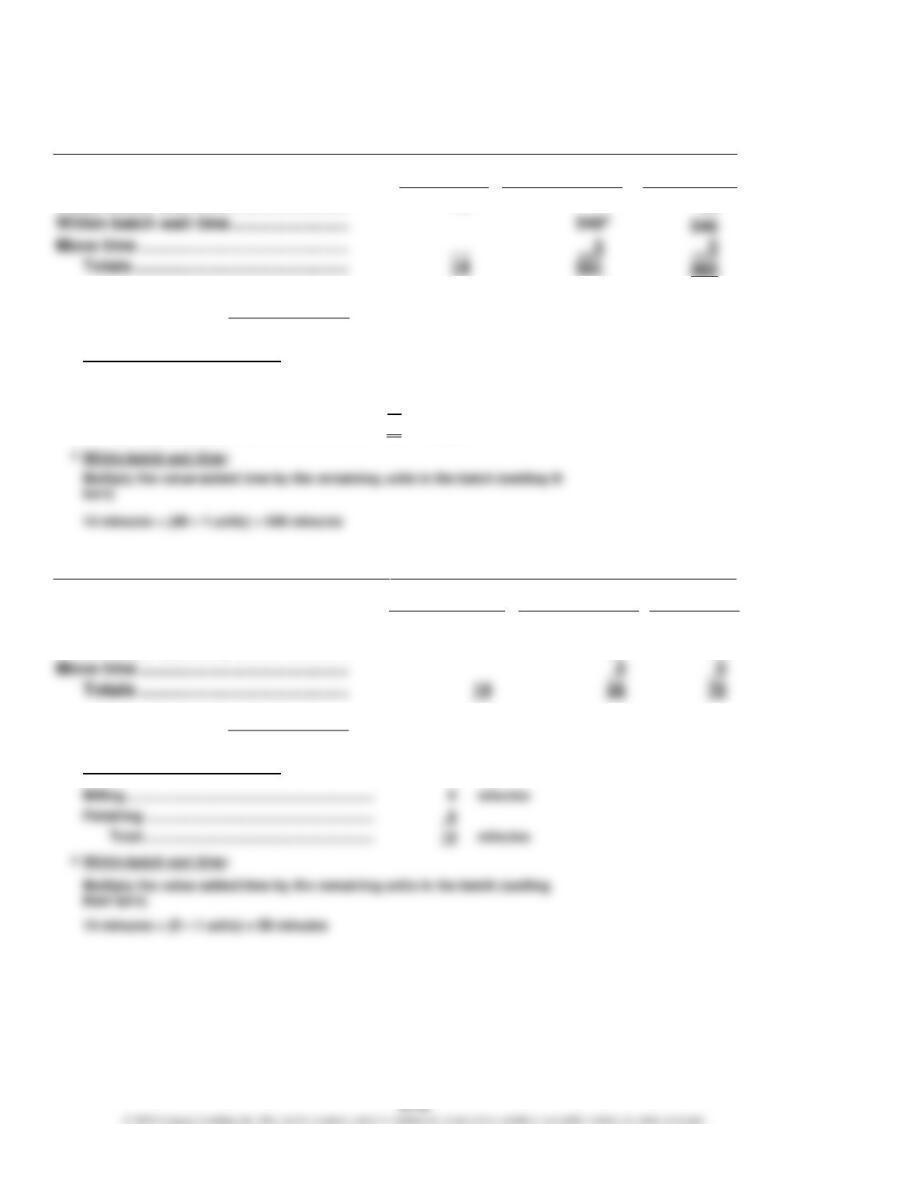

Ex. 27–6 (FIN MAN); Ex. 13–6 (MAN)

Traditional Philosophy

Value-Added

Time

Non-Value-

Added Time

Total

Time

– 14 minutes

Value added ratio: = 2.5%, rounded

565 minutes

1

Total value-added time per unit:

Milling …………………………………………………………

6

minutes

Finishing …………………………………………………….

8

Total ……………………………………………………..

14

minutes

Lean Manufacturing Philosophy

Value-Added

Time

Non-Value-

Added Time

Total

Time

Value-added time …………………………...

141

14

Within-batch wait time …………………….

562

56

Move time ………………………………………

70

– 14 minutes

Value added ratio : = 20.0%

70 minutes

1

Total value-added time per unit:

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

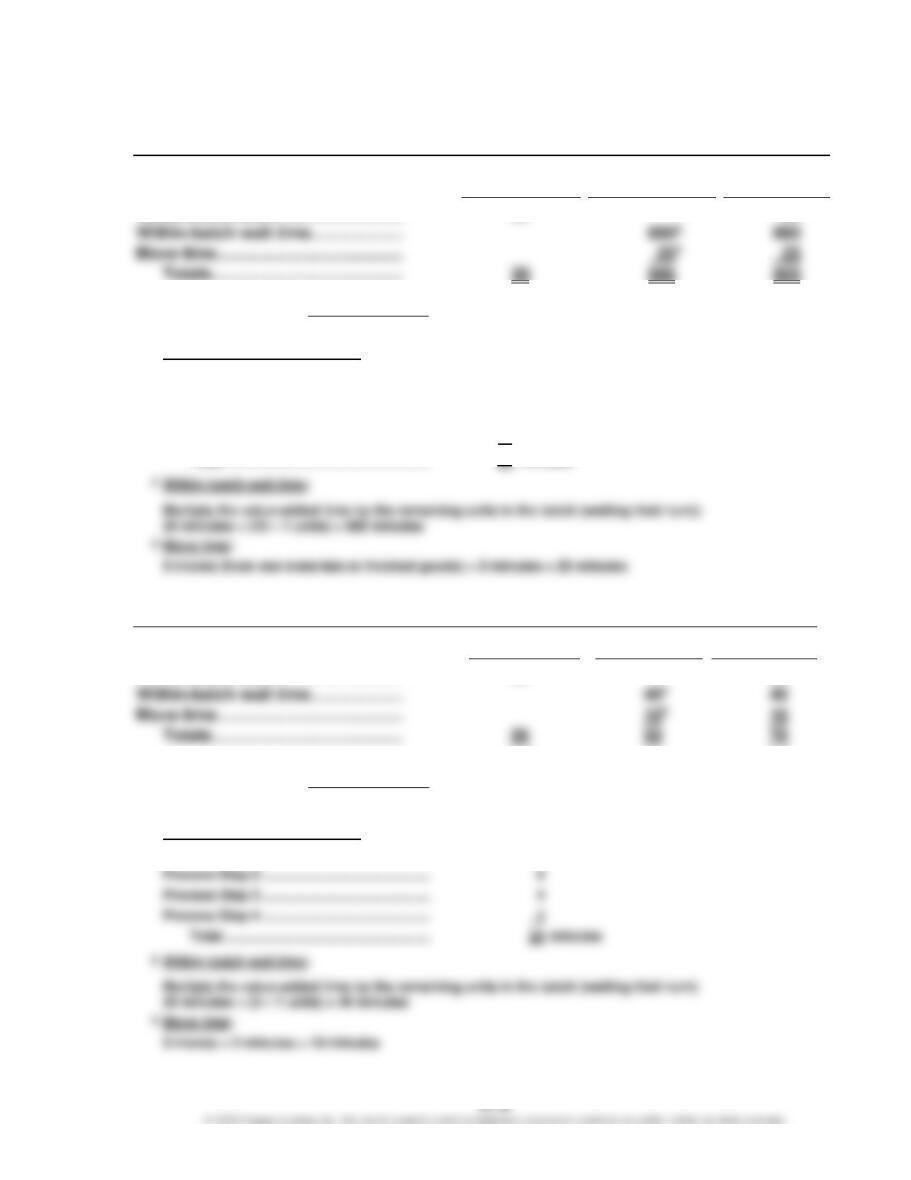

Ex. 27–7 (FIN MAN); Ex. 13–7 (MAN)

a.

Present Approach

Value-Added

Time

Non-Value-

Added Time

Total

Time

Value-added time ……………………….

20

Within-batch wait time ………………..

880

Move time ………………………………….

Totals …………………………………..

20

905

925

– 20 minutes

Value added ratio : = 2.2%, rounded

925 minutes

1

Total value-added time per unit:

Process Step 1 ………………………………………

5

minutes

Process Step 2 ………………………………………

8

Process Step 3 ………………………………………

4

Process Step 4 ………………………………………

3

Within-batch wait time:

3

Move time:

b.

Proposed Lean Approach

Value-Added

Time

Non-Value-

Added Time

Total

Time

Value-added time ……………………….

Within-batch wait time ………………..

40

Move time ………………………………….

10

201

20

– 20 minutes

Value added ratio : = 28.6%, rounded

70 minutes

1

Total value-added time per unit:

Process Step 1 ………………………………………

5

minutes

Process Step 2 ………………………………………

Process Step 3 ………………………………………

Process Step 4 ………………………………………

2

Within-batch wait time:

5 moves × 2 minutes = 10 minutes

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–8 (FIN MAN); Ex. 13–8 (MAN)

a. The Japanese supply chain model is one based on long-term arrangements and

partnership. The Japanese automobile manufacturers want their suppliers to be

b. These suppliers support the Japanese system because it provides for win–win

opportunities, whereby the customer and the supplier can both be successful. The

suppliers are concerned about their margins being squeezed down to the point that

business over time.

c. Supply chain management is often beneficial to the customer. However, the

customer may have to trade off between short-term and longer-term benefits. For

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–9 (FIN MAN); Ex. 13–9 (MAN)

Quickie’s team approaches are very different from using a manager to hire and evaluate

employees. First, the input of many individuals goes into the hiring decision. In this way,

the viewpoints of a variety of people are brought into the decision. Moreover, the new hire

needs to “fit” with the culture of the team. Team-based hiring can produce a higher

probability of having an effective team member by having a good fit. A possible concern is

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–10 (FIN MAN); Ex. 13–10 (MAN)

a. The present Daddy-O’s service delivery system is an example of a push system.

Special orders are “pushed” through the system. The order is placed at the

have to wait for the complete cook and dress cycle to be completed.

b. A new system could be designed so that a custom order is introduced after cooking

the burger, rather than prior to cooking. In this way, hamburgers are made to order

without the use of finished goods inventory. Under this process, assume a customer

ordered a hamburger with ketchup and pickles only. The order would be received at

the dressing station. Here, a food preparer would take a hamburger off the grill and

place ketchup and pickles on the burger using materials at the dressing station

(termed point-of-use materials). The hamburger that is pulled from the grill would

Note to Instructors: You may recognize that the first system described in this exercise is

similar to the method invented by McDonald’s, while Wendy’s uses the second method.

McDonald’s indicated that it was switching its method to work more like Wendy’s

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–11 (FIN MAN); Ex. 13–11 (MAN)

The production manager probably has some good points. If the accounting system does

not change when an organization embraces a lean strategy, then there will likely be

complaints. A conventional accounting system needs to have a strong accounting control

orientation. Under lean manufacturing, the accounting system can be designed with much

wider transaction control intervals. The company could have a very wide transaction

The direct labor reporting can be eliminated. Using lean accounting practices, the direct

labor employees are assigned to production cells. Their wages are treated as part of the

cell’s conversion costs and are not separately traced or reported. The traditional financial

measures should be supplemented with nonfinancial measures, such as schedule

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–12 (FIN MAN); Ex. 13–12 (MAN)

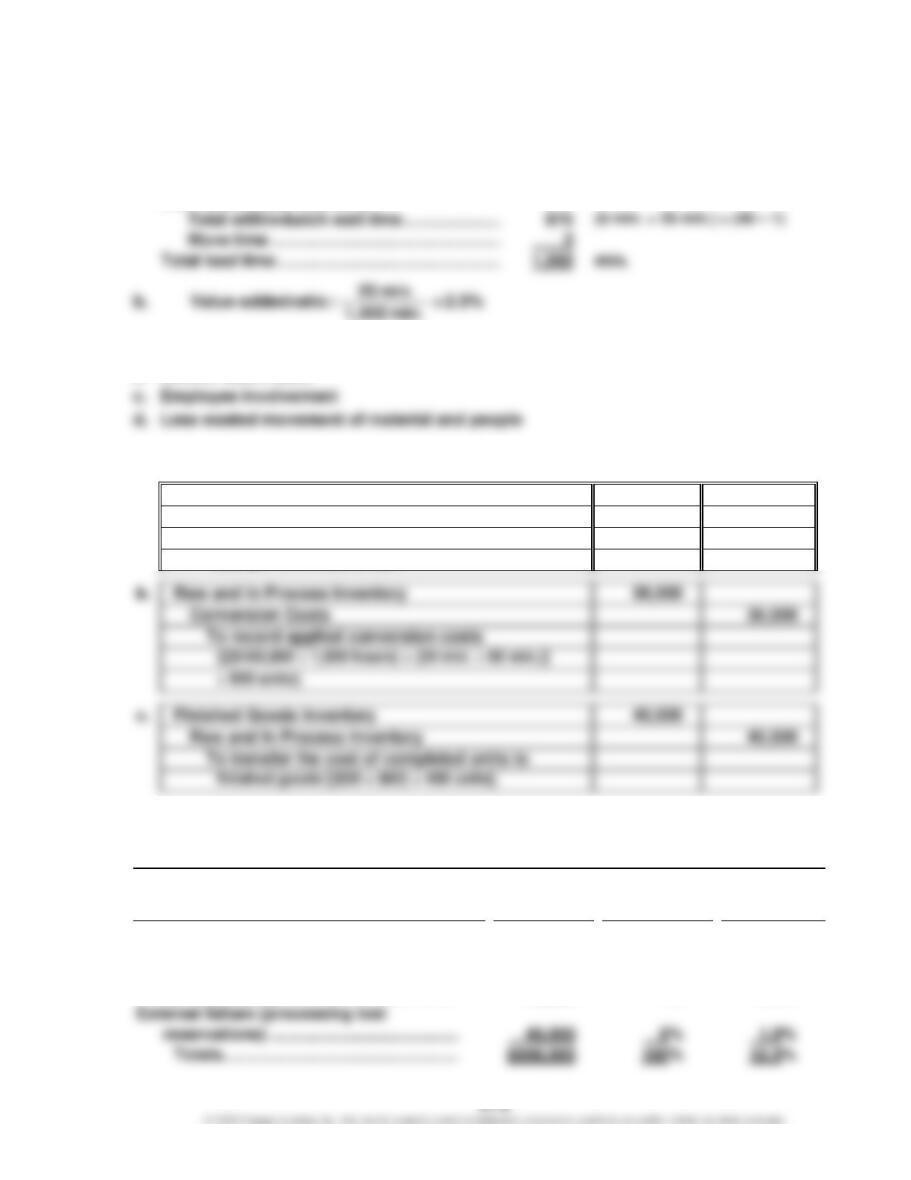

a.

Budgeted Cell Conversion $600,000

== $300 per hour

2,000 hours

Cost Rate

c.

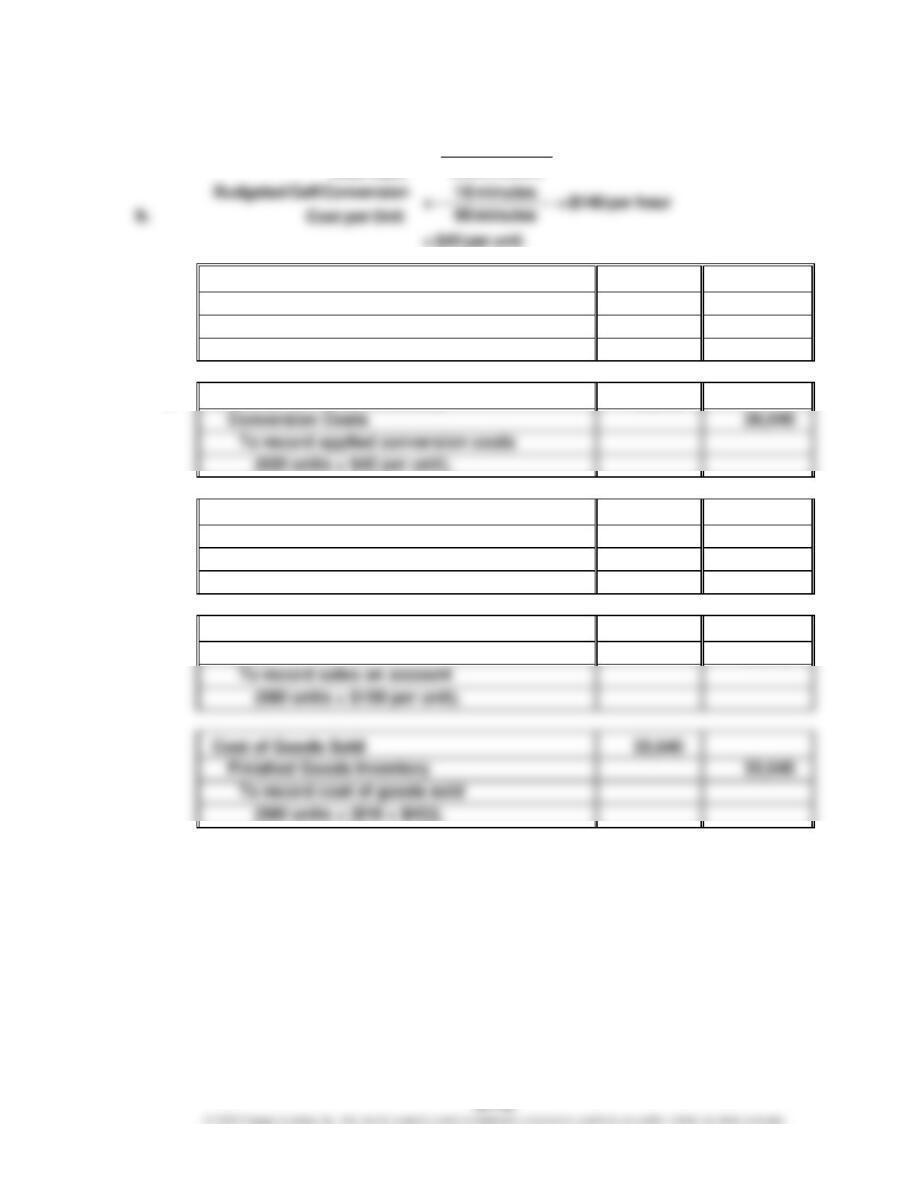

1.

Raw and In Process Inventory

30,000

Accounts Payable

30,000

To record materials purchases

(500 units × $60 per unit).

2.

Raw and In Process Inventory

52,500

3.

Finished Goods Inventory

82,500

Raw and In Process Inventory

82,500

To transfer the cost of completed units to

finished goods [500 units × ($60 + $105)].

4.

Accounts Receivable

115,200

Sales

115,200

To record sales on account

Cost of Goods Sold

79,200

Finished Goods Inventory

79,200

To record cost of goods sold

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–13 (FIN MAN); Ex. 13–13 (MAN)

a.

Budgeted Cell Conversion $308,000

= = $140 per hour

= $42 per unit

c.

1.

Raw and In Process Inventory

9,920

Accounts Payable

9,920

To record materials purchases

(620 units × $16 per unit).

2.

Raw and In Process Inventory

26,040

26,040

To record applied conversion costs

(620 units × $42 per unit).

3.

Finished Goods Inventory

34,800

Raw and In Process Inventory

34,800

To transfer the cost of completed units to

finished goods [600 units × ($16 + $42)].

4.

Accounts Receivable

58,000

Sales

58,000

To record sales on account

(580 units × $100 per unit).

Cost of Goods Sold

33,640

Finished Goods Inventory

33,640

To record cost of goods sold

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

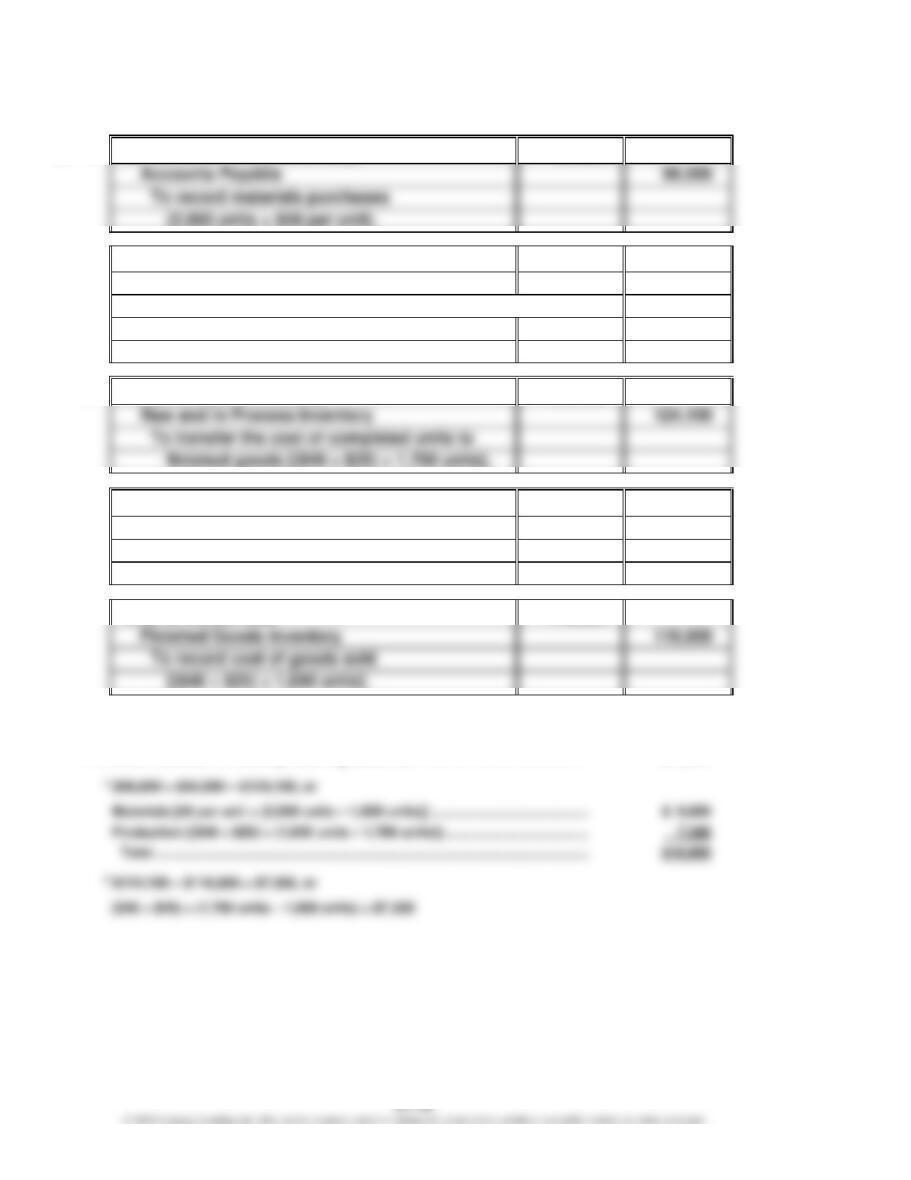

Ex. 27–14 (FIN MAN); Ex. 13–14 (MAN)

a.

1.

Raw and In Process Inventory

96,000

To record materials purchases

(2,000 units × $48 per unit).

2.

Raw and In Process Inventory

45,000

Conversion Costs

45,000

To record applied conversion costs

{[($50,000 ÷ 800 hours) × (24 min. ÷ 60 min.)]

× 1,800 units}.

3.

Finished Goods Inventory

124,100

4.

Accounts Receivable

144,000

Sales

144,000

To record sales on account

($90 per unit × 1,600 units).

Cost of Goods Sold

116,800

116,800

To record cost of goods sold

b.

Raw and In Process Inventory, ending balance1 ………………………..

$16,900

Finished Goods Inventory, ending balance2 ……………………………..

$7,300

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–15 (FIN MAN); Ex. 13–15 (MAN)

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–16 (FIN MAN); Ex. 13–16 (MAN)

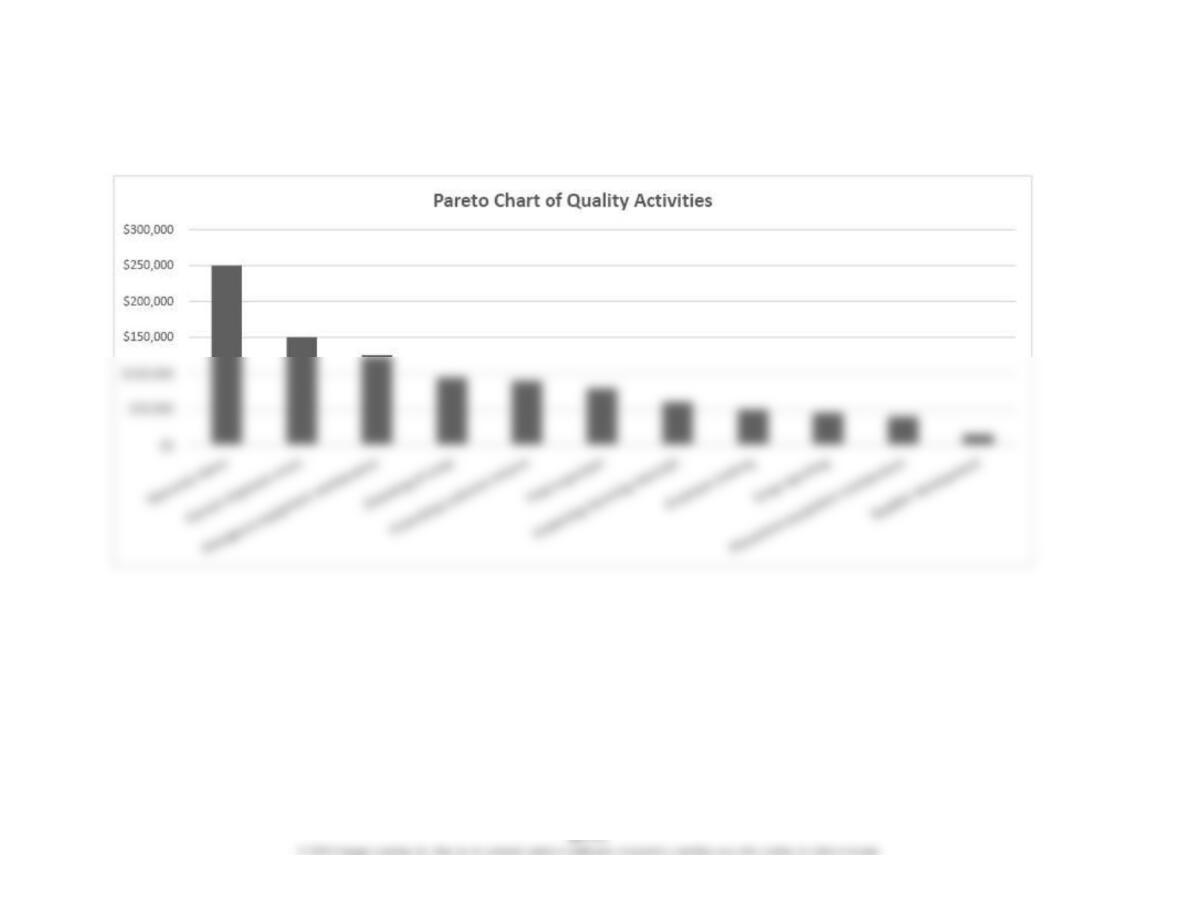

a. Activities classified by cost of quality:

Activity Cost

Quality Cost

Classification

Quality Activities

Correct shipment errors ………………………….

$ 150,000

External failure

Disposing of scrap …………………………..……..

95,000

Internal failure

Emergency equipment maintenance ………..

125,000

Internal failure

Employee training …………………………………..

50,000

Prevention

Final inspection ………………………………………

80,000

Appraisal

Inspecting incoming materials …………………

60,000

Appraisal

Scrap reporting ………………………………………

45,000

Internal failure

Supplier development ……………………………..

15,000

Prevention

b.

Meagher Solutions Inc.

Cost of Quality Report

Quality Cost Classification

Cost Summary

Quality

Cost

Percent of

Total

Quality Cost

Percent

of Total

Sales

Prevention

$ 105,000

10.5%1

2.6%2

1

$105,000 ÷ $1,000,000

2

$105,000 ÷ $4,000,000

c. The majority of the company’s quality efforts are in correcting quality problems. This

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–17 (FIN MAN); Ex. 13–17 (MAN)

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Ex. 27–18 (FIN MAN); Ex. 13–18 (MAN)

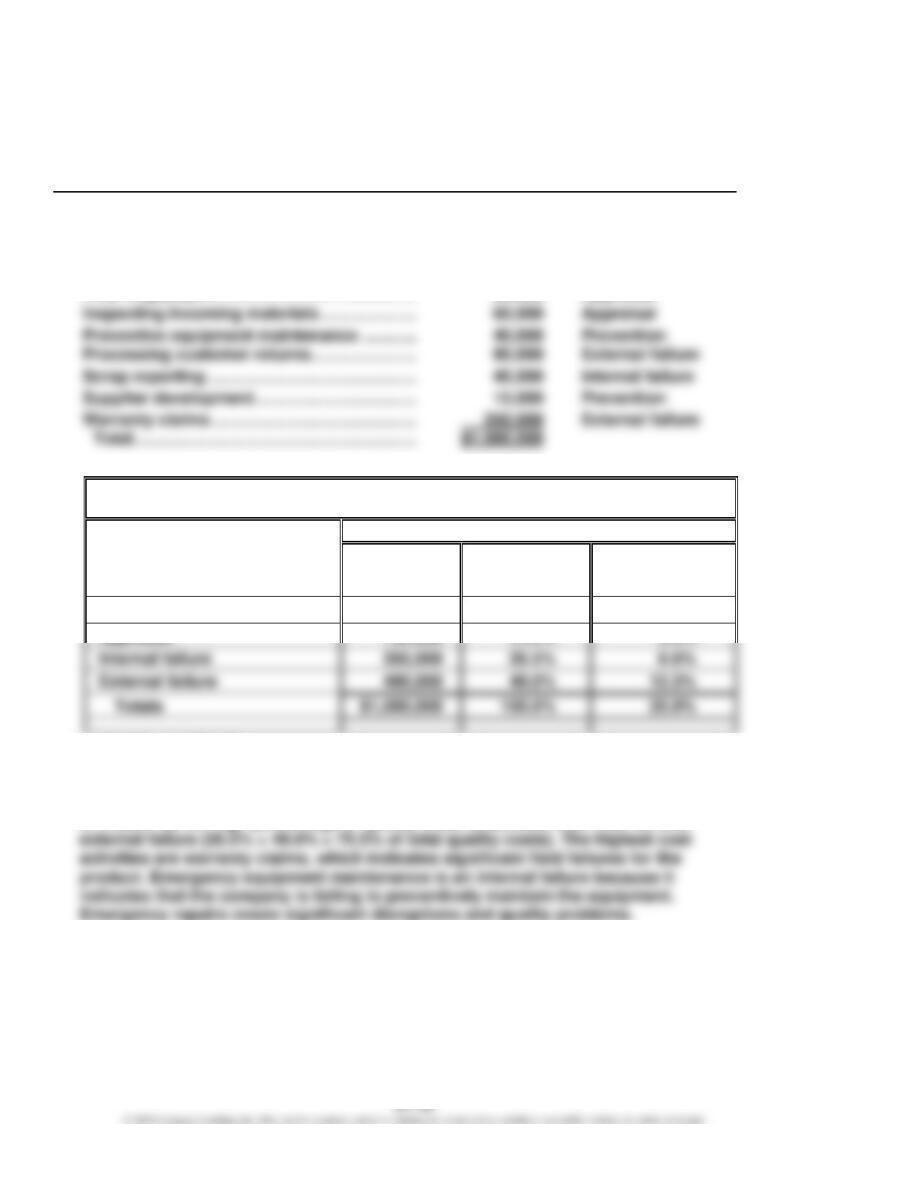

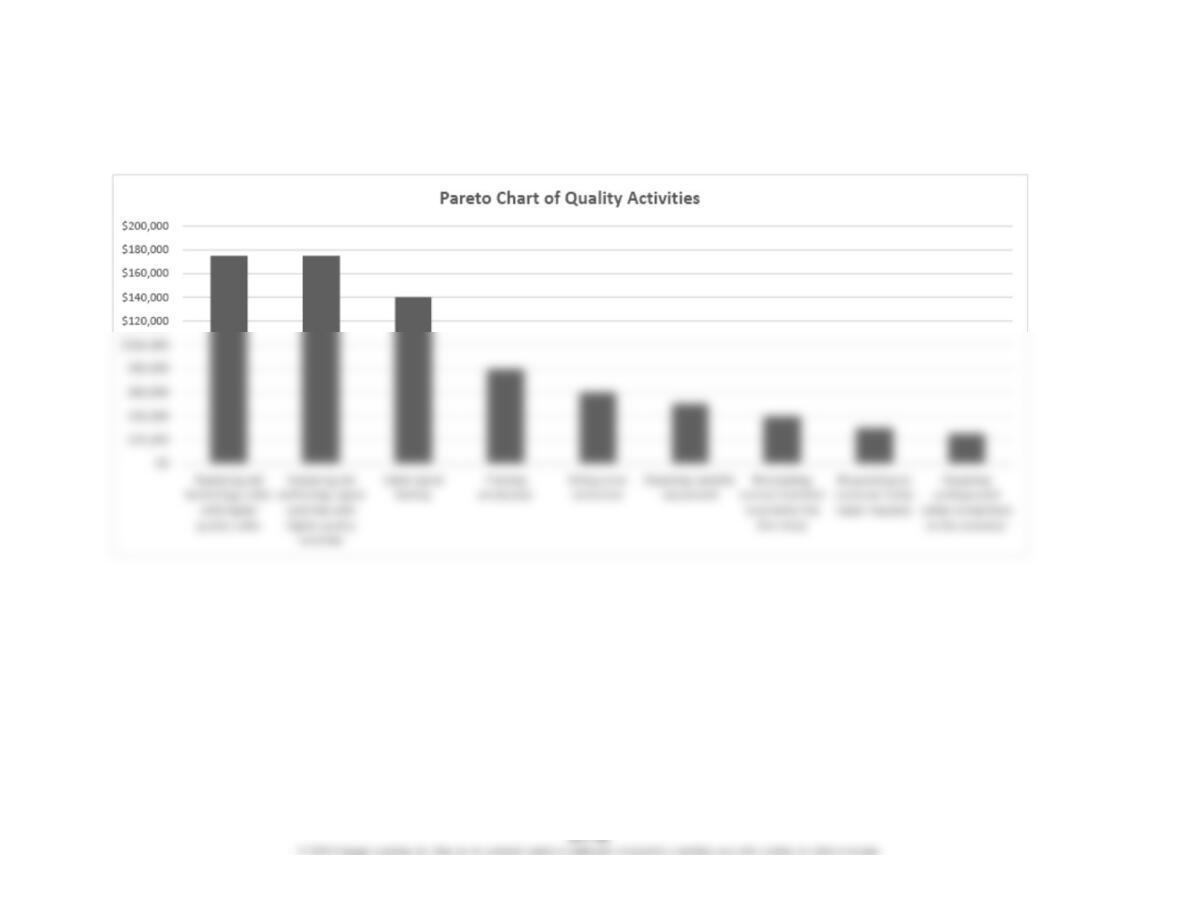

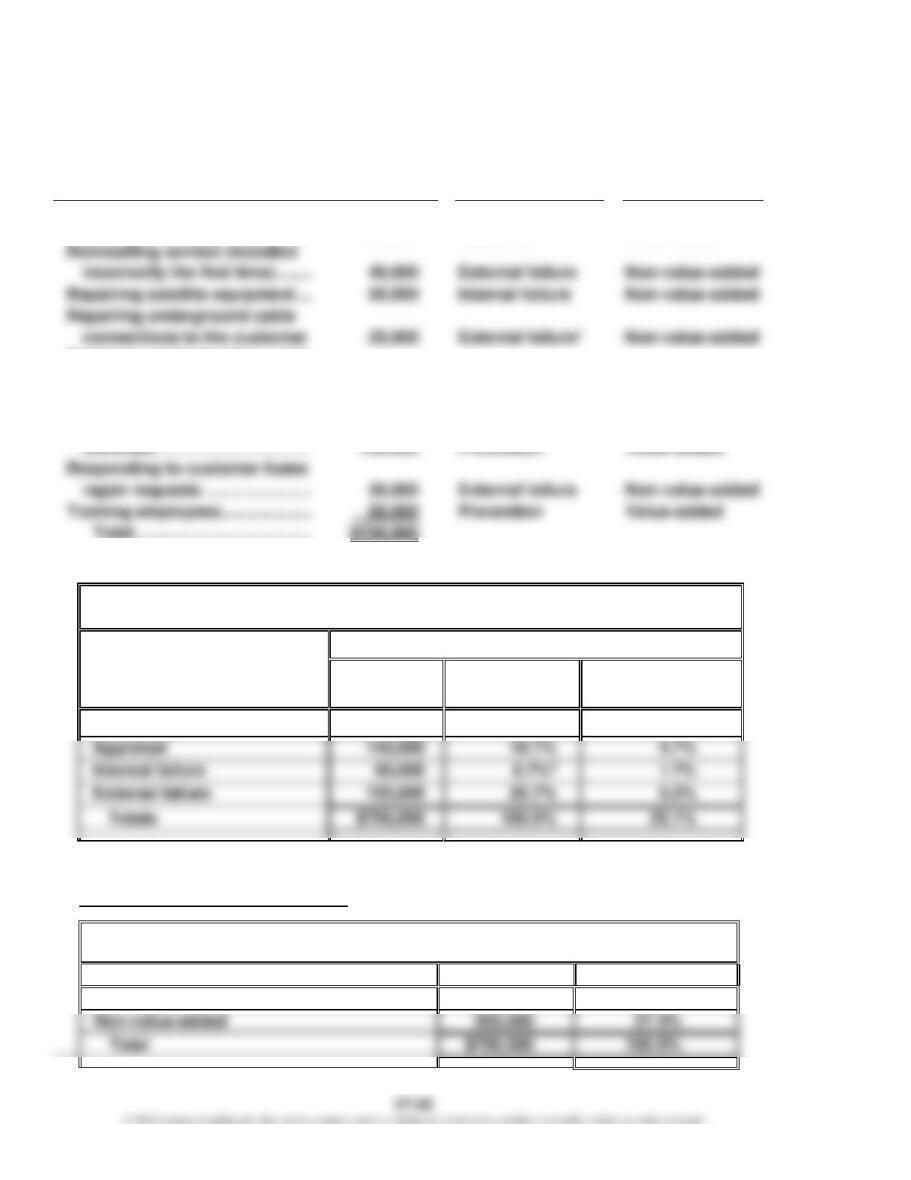

a. Quality cost and value-added/non-value-added classifications:

Quality Activities

Activity

Cost

Quality Cost

Classification

Value-Added/

Non-Value-Added

Classification

Billing error correction …………..

$ 60,000

External failure

Non-value-added

Cable signal testing ……………….

140,000

Appraisal

Value-added

Reinstalling service (installed

incorrectly the first time) …….

Non-value-added

Repairing underground cable

connections to the customer

Non-value-added

Replacing old technology cable

with higher quality cable …….

175,000

Prevention

Value-added

Replacing old technology signal

switches with higher quality

Training employees ……………….

Total …………………………..……

$750,000

* This is an external failure because the underground cable connection needs to be repaired after

receiving notification of disrupted service from a customer.

b.

Three Rivers Inc.

Cost of Quality Report

Quality Cost Classification

Cost Summary

Quality

Cost

Percent of

Total

Quality Cost

Percent

of Total

Sales

Prevention

$405,000

54.0%1

13.5%2

$750,000

1

$405,000 ÷ $750,000

2

$405,000 ÷ $3,000,000

3

Unrounded percentages total to 100.0%.

c.

Three Rivers Inc.

Value-Added/Non-Value-Added Activity Analysis

Category

Amount

Percent

Value-added

$545,000

72.7%