CHAPTER 13

STATEMENT OF CASH FLOWS

Brief Learning

Exercises Objectives Skills

B. Ex. 13.1 Cash flows from operations (direct) 13-3 Analysis

B. Ex. 13.2 Cash flows from operations (indirect) 13-7 Analysis

B. Ex. 13.3 Cash flows from operations (direct) 13-3 Analysis

B. Ex. 13.4 Cash flows from operations (indirect) 13-7 Analysis

B. Ex. 13.5 Cash flows from investing activities 13-4 Analysis

B. Ex. 13.6 Cash flows from financing activities 13-4 Analysis

B. Ex. 13.7 Cash payment for merchandise 13-3 Analysis

B. Ex. 13.8 Determining beginning cash balance 13-2 Analysis

B. Ex. 13.9

Analysis

13-6

B. Ex. 13.10 Prepare statement of cash flows 13-2

Analysis

Skills

13.1 Using a cash flow statement 13-1, 13-2 Analysis, communication

13.2 Using a cash flow statement

13-1, 13-2,

13-6

Analysis, communication

13.3 13-4 Analysis

13.4 13-3, 13-6 Analysis, communication

13.5 Accrual versus cash flows 13-3 Analysis

13.6 13-3, 13-6 Communication

13.7 Format of a cash flow statement 13-2 Analysis

13.8 13-8

13.9 Indirect method 13-6, 13-7 Analysis, communication

13.10 Indirect method 13-7 Analysis

13.11 Classification of cash flows 13-2 Analysis

13.12 Classification of cash flows 13-2 Analysis

13.13 Cash flows from operating activities 13-4

13.14 Cash flows from financing activities 13-4

13.15 Real World: Home Depot, Inc.

OVERVIEW OF BRIEF EXERCISES, EXERCISES, PROBLEMS, AND CRITICAL

THINKING CASES

Investing activities and interest revenue

Relationship between accrual and cash

flows

Learning

Objectives

Using noncash accounts to compute cash

flows

Topic

Cash effects of business strategies

13-1, 13-2,

13-4

Topic

Reconciling net income to cash from

operations

Analysis, communication,

judgment

Analysis, communication,

judgment

Analysis, communication,

judgment, research

Analysis, communication,

judgment

Problems Learning

Sets A, B

Objectives Skills

13.1 A,B 13-2–13-4 Analysis

13.2 A,B 13-4 Analysis

13.3 A,B 13-4

Analysis, communication,

judgment

13.4 A,B 13-3, 13-8

Analysis, communication,

judgment

13.5 A,B 13-6, 13-7

13.6 A,B

13-2–13-4,

13-6, 13-8

Analysis, communication,

judgment

13.7 A,B 13-1–13-9

13.8 A,B 13-1–13-9

13.1 Using a statement of cash flows 13-1

13.2 Budgeting at a personal level 13-1, 13-8

13.3

13.4 Peak pricing 13-8

13.5 13-3

governance)

13.6 13-2–13-4

(Internet)

Analysis, communication,

judgment

Analysis, communication,

judgment

Analysis, communication,

judgment

Cash flow from operating

activities—direct method

Analytical, communication,

judgment

Analytical, communication,

judgment

Analytical, communication,

judgment, research

Analytical, communication,

judgment

Window dressing; effects on net

income and net cash flow

13-1, 13-4,

13-8

Improving the Statement of Cash

Flows (Ethics, fraud & corporate

Real World: Coca-Cola,

Amazon.com Cash Flow Analysis

Analytical, communication,

judgment

Analytical, communication,

judgment

Critical Thinking Cases

Preparing a statement of cash

flows—direct method (short)

Investing activities

Investing activities

Preparing a worksheet and statement

of cash flows; evaluate the company’s

financial position—indirect method.

Preparing a worksheet and statement

of cash flows; evaluate the

company’s liquidity-indirect method.

Cash flow from operating

activities—indirect method

Preparing a statement of cash

flows—direct method; comprehensive

DESCRIPTIONS OF PROBLEMS AND CRITICAL THINKING CASES

Problems (Sets A and B)

45 Strong

13.6 A,B

21st Century Technologies/Foxboro Technologies

Prepare the operating activities section of a statement of cash

flows from accounting records maintained using the accrual basis

of accounting. Students also are to explain how more efficient

asset management could increase cash flow provided by operating

activities. Uses the direct method. (Problem 13–5 uses the same

data but requires use of the indirect method. )

A comprehensive problem covering conversion from the accrual

basis to the cash basis and preparation of a statement of cash

flows. Uses the direct method.

Using the data provided in Problem 13.4 A,B, prepare the

operating activities section of a statement of cash flows using the

indirect method.

13.5 A,B

Below are brief descriptions of each problem and case. These descriptions are accompanied by the

estimated time (in minutes) required for completion and by a difficulty rating. The time estimates assume

use of the partially filled-in working papers.

Treece, Inc./Royce Interiors, Inc.

13.2 A,B

25 Easy

Prepare a statement of cash flows. Emphasis is on format of the

statement, with computations held to a minimum. However,

sufficient computations are required to assure that students are

able to distinguish between cash flows and accrual basis

measurements. Uses the direct method.

25 Easy

Holmes Export Co./RPZ Imports

30 Medium

Lambert Company/Welch Company

13.1 A,B

13.4 A,B

Prepare the investing activities section of a statement of cash flows

by analyzing changes in balance sheet accounts and gains and

losses reported in the income statement.

30 Medium

Treece, Inc. (Indirect)/Royce Interiors, Inc. (Indirect)

25 Medium

13.3 A,B

Prepare the investing activities section of a statement of cash

flows. Problem demonstrates how this section of the financial

statement can be prepared by analyzing income statement amounts

and changes in balance sheet accounts.

Hampton Inc./Mary’s Fashions

Problems (cont’d)

60 Strong (P13.7A)

40 Strong (P13.7B)

13.7 A,B

Satellite World/LGIN

A comprehensive problem covering all learning objectives.

Includes a worksheet, the indirect method, and analysis of the

company’s financial position. We assign this to groups and let

them deal with the worksheet mechanics on their own.

60 Strong

A comprehensive problem covering all learning objectives. P13.7A

includes a worksheet, the indirect method, and analysis of the

company’s financial position. P13.7B does not include a

worksheet and uses the indirect method. We assign this to groups

and let them deal with the worksheet mechanics on their own.

Miracle Tool, Inc./Purcells, Inc.

13.8 A,B

Critical Thinking Cases

Another Look at Allison Corporation

Cash Budgeting for You as a Student

Lookin’ Good?

Peak Pricing

Improving the Statement of Cash Flows

Ethics, Fraud & Corporate Governance

Comparing Cash Flow Information from Two Companies

Internet

25 Strong

Students are to discuss various aspects of peak pricing and discuss

how it might be applied in specific situations. Also, they are to

describe situations in which peak pricing might be considered

unethical.

15 Easy

13.2

A simple case that illustrates the usefulness of cash budgeting in the

environment of a college student.

An automobile manufacturer is in serious financial difficulty, and

management is considering several proposals to increase reported net

income and net cash flow. Students are asked to evaluate the probable

effects of each proposal. This case can lead into an open-ended

discussion of “window dressing” in annual statements.

13.1

45 Medium

Students are asked to review the cash flow statement of Allison

Corporation (the company used as an example throughout the

chapter) and to evaluate the company’s ability to maintain its present

level of dividends.

13.4

13.3

20 Medium

Students explore the website of the Securities & Exchange

Commission and locate a speech by an S.E.C. official in which

suggestions for improving the statement of cash flows are discussed.

13.5

13.6

Visit a website that actually provides assistance in preparing cash

budgets and statements of cash flows.

30 Medium

15 Easy

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

1.

3.

a.

b. c.

(1) Sales of investments. (1)

(2) Collecting loans. (2)

(3) Sales of plant assets. (3)

(1) Purchases of investments. (1)

(2) Lending cash.

(3) Purchases of plant assets.

Payments:

Payments:

Repayment of debt.

Purchase of treasury stock or retirement of

outstanding shares.

Payment of dividends.

Issuance of capital stock.

Sales of treasury stock.

4.

5.

The primary purpose of a statement of cash flows is to provide information about the cash

The income statement provides the better measurement of profitability, especially when the

business is financially sound and short-run survival is not the critical issue. The statement of cash

Receipts:

Receipts:

Investing activities:

Financing activities:

In the long run, it is most important for a business to have positive cash flows from operating

activities. To a large extent, the ability of a business to generate positive cash flows from

financing activities is dependent upon its ability to generate cash from operations. Investors are

Net cash flow from operating activities generally reflects the cash effects of transactions entering

2.

Receipts:

Examples of cash receipts and of cash payments in the three major classifications of a cash flow

statement are shown below (two receipts and two payments required):

Operating activities:

Short-term or long-term borrowing.

Payments:

Cash paid to suppliers and employees.

Income taxes paid.

Dividends and interest received.

Cash received from customers.

Interest paid.

6.

7.

8.

9.

10.

Among the classifications shown in the cash flow statement, a successful and growing company is

The credit to the Land account indicates a sale of land and, therefore, a cash receipt. However, the

Net income may differ from the net cash flows from operating activities as a result of such factors

as:

The direct method identifies the major operating sources and uses of cash, using such captions as

One purpose of a statement of cash flows is to provide information about all the investing and

financing activities of a business. Although the acquisition of land by issuing capital stock does

Nonoperating gains and losses that, although included in the measurement of net income,

Depreciation and other noncash expenses that enter into the determination of net

11.

12.

Add: Decrease during the year in the liability for dividends payable

13.

14.

15.

From a short-term creditor’s point of view, free cash flow is a “buffer,” indicating that the business

Credits to paid-in capital accounts usually indicate the issuance of additional shares of capital stock.

Free cash flow is that portion of the net cash flow from operating activities that is available for

discretionary purposes after the basic obligations of the business have been met.

The amount of cash dividends paid during the current year may be determined as follows:

Speeding up the collection of accounts receivable does not increase the total amount collected.

Peak pricing means charging higher prices in periods in which customer demand exceeds the

company’s capacity, and lower prices in “off-peak” periods. This serves the dual purposes of

B.Ex. 13.1

$470,000

$558,000

Net cash provided by operating activities

Adjustments to reconcile net income to net cash from operations:

B.Ex. 13.3

Cash received from customers

$750,000

$722,000

$654,000

$(50,000)

(55,000)

Net cash provided by operating activities

B.Ex. 13.5

Cash paid for investments

$(55,000)

SOLUTIONS TO BRIEF EXERCISES

Cash flows from operating activities:

Net income

B.Ex. 13.4

B.Ex. 13.2

Cash flows from operating activities:

Net income

Adjustments to reconcile net income to net cash from operations:

Cash used for investing activities:

$270,000

B.Ex. 13.6

Cash received from sale of common stock

$560,000

Cost of goods sold

$100,800

B.Ex. 13.8

$155,000

$67,000

B.Ex. 13.9

$68,000

$15,000

$86,000

Net cash provided by operating activities

Cash flows provided by operating activities

$136,000

$46,000

72,000

Cash flows used in financing activities

Cash, beginning of year

B.Ex. 13.10

Maines, Inc.

Statement of Cash Flows

For year ended _____________

Net income

B.Ex. 13.7

Adjustments to reconcile net income to net cash from

Cash balance at the beginning of the year:

Cash payments for purchases:

Ex. 13.1 a.

b.

Ex. 13.2

a. 280,000$

b.

SOLUTIONS TO EXERCISES

Cash from operations …………………………………………………………………

The gain on the sale of marketable securities represents a reclassification of this

The major sources and uses of cash from financing activities during 2018

were:

The operating activities section generally includes the cash provided by and used for

those transactions that are normal, ongoing operations and that included in the

Wallace Company’s cash increased significantly during the year, going from $75,000 to

$255,000. Operations were strong, providing $275,000 of positive cash flow. Based on the

d.

(1)

Expenditures for property and equipment …………………………………………..

Dividends paid …………………………………………………………………………

(2)

Ex. 13.4 a. (1)

$289,000

$472,000

$504,000

$761,000

$793,000

Cash received from customers ……………………………………….

Credit sales ………………………………………………………………

Credit sales ……………………………………………………………

Cash received from collecting accounts receivable:

Add: Decrease in accounts receivable ……………………………….

Collections of accounts receivable ……………………………………

Net sales (includes cash sales and credit sales) …………

Add: Decrease in accounts receivable …………………………………

Cash received from customers:

Ex. 13.5

Increase in inventory ($820,000 − $780,000) ……………..

Ex. 13.6

Cash payments to suppliers of merchandise ………………….

$ 2,992,000

Cash sales ………………………………………………………………

Cash payments to suppliers of merchandise:

The increase in accounts receivable represents credit sales which were not collected

Net sales:

$ 2,882,000

Cost of goods sold …………………………………………………………..

Ex. 13.3 a. $125,000

$115,000

value less $25,000 loss) ………………………………………………………………

Purchases of marketable securities ……………………………………………..

Proceeds from sales of marketable securities ($140,000 book

795,000$

(2)

a.

(1)

Cash received from customers ……………………………………

Ex. 13.7

WYOMING OUTFITTERS, INC.

Statement of Cash Flows

For the Year Ended December 31, Current Year

Cash flows from operating activities:

d.

b.

Selling to customers using bank credit cards taps a new market of potential

(1)

c.

(1)

(2)

Reducing inventory will lessen expenditures for inventory purchases

(2)

Deferring taxes can postpone taxes each year. For a growing business, this

Interest and dividends received ………………………………….

Cash provided by operating activities ………………………..

Cash and cash equivalents, December 31, 20__ ………………………………

Cash paid to suppliers and employees …………………………..

Interest paid ……………………………………………………….

Income taxes paid …………………………………………………..

Cash paid to acquire plant assets ………………………………..

Proceeds from sales of plant assets ………………………………

Collections on loans ……………………………………………….

Cash disbursed for operating activities ……………………….

Net cash flow from operating activities

Cash flows from investing activities:

Loans made to borrowers …………………………………………

Net cash used for investing activities …………………………………

Net cash used for financing activities ………………………………………………..

Net increase in cash and cash equivalents …………………………….

Cash and cash equivalents, January 1, 20__ …………………….

Cash flows from financing activities:

Proceeds from short-term borrowing …………………………….

Dividends paid ……………………………………………………..

e.

Ex. 13.9 a.

b.

c.

d.

e.

f.

h.

Dividends are a financing activity, not an operating activity. Therefore,

Added to net income. Depreciation is a noncash expense. Although it reduces the

Added to net income . In a statement of cash flows, the uninsured loss from fire is

Added to net income. An increase in accounts payable means that purchases of

merchandise, measured on the accrual basis, exceed the payments during the

Added to net income. A reduction in prepaid expenses indicates that the amounts

Omitted from the computation. The transfer of cash from a bank account to a

Deducted from net income. An increase over the year in the amount of accounts

Omitted from the computation. Cash received from customers is a cash inflow

$ 385,000

Ex. 13.11

a.

g.

o.

Operating activity

Operating activity

Operating activity

Investing activity

Operating activity

Investing activity

Not included in a statement of cash flows prepared by the direct method.

Operating activity

Financing activity

Financing activity

Operating activity

Financing activity

Operating activity

Ex. 13.10

FREEMAN MACHINERY, INC.

Net income ……………………………………………………………………………….

Partial Statement of Cash Flows

For the Year Ended December 31, 2018

Cash flows from operating activities:

$ 737,000

$ 607,000

Net cash flow from operating activities …………………………………………….

Subtotal ……………………………………………………………………………..

Ex. 13.12

1.

2.

Financing activity

Operating activity

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

13.

14.

15.

Operating activity

Financing activity

Operating activity

Operating activity

Investing activity

Investing activity

Operating activity

Financing activity

Operating activity

Operating activity

Ex. 13.13 a.

b.

Cost, less accumulated depreciation

Gain on sale

Cash received from sale

Loss on sale

Cash received from sale

c.

Cash provided by investing activities:

The amount of gain or loss is reflected in the cash receipts figure. For example,

The following items were excluded because they are financing activities, not

investing activities:

Sale of land

Ex. 13.14 a.

$420,000

b.

●Cash received from customers

Cash received from interest and dividends

●Cash paid to purchase inventory

Classified as investing activities:

c.

While an argument could be made that interest expense should be

Cash

Sale of bonds

Classified as operating activities:

The following items were excluded from the above calculations because

they are classified as indicated below in the statement of cash flows:

$392,000

Sale of treasury stock

Dividends on common stock

Purchase of treasury stock

(60,000)

(20,000)

Ex. 13.15

a.

b.

c.

d.

2015 2014 2013

9,373$ 8,242$ 7,628$

Net earnings for 2015 (year ending January 31, 2016) were $7,009 million, compared

Free cash flow for the three years is determined as follows (in millions):

Net cash from operations

The major uses of cash, other than operations, are as follows:

Negative cash flows from investing and financing activities do not necessarily lead to a

plant, and equipment

Cash paid for dividends

Cash invested in property,

30 Minutes, Medium

a.

Cash flows from operating activities:

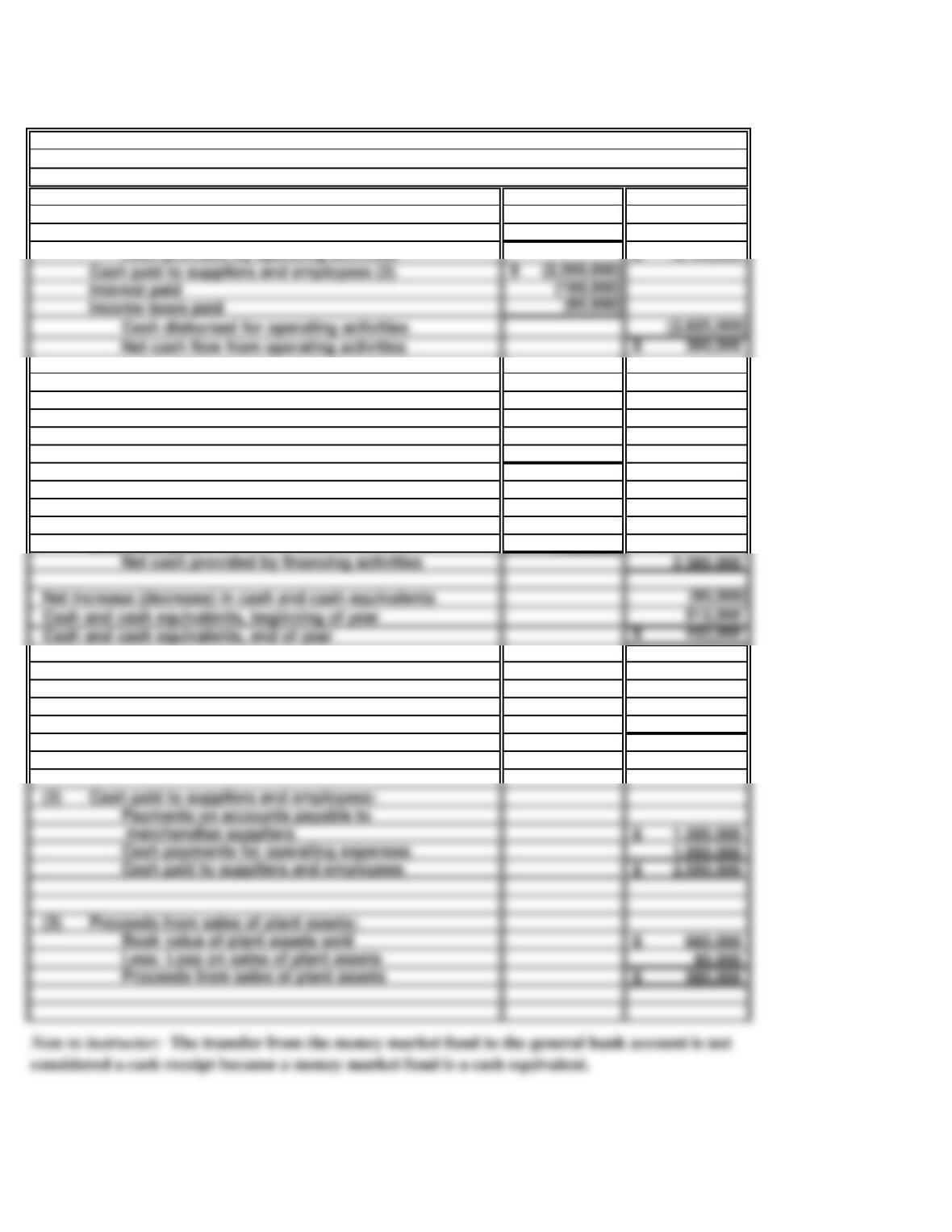

Cash received from customers (1) 3,025,000$

Interest and dividends received 100,000

Cash provided by operating activities 3,125,000$

Cash flows from investing activities:

Loans made to borrowers (500,000)

Collections on loans 260,000

Cash paid to acquire plant assets (3,100,000)

Proceeds from sales of plant assets (3) 580,000

Net cash used in investing activities: (2,760,000)

Cash flows from financing activities:

Proceeds from issuing bonds payable 2,500,000$

Dividends paid (120,000)

Net cash provided by financing activities 2,380,000

Net increase (decrease) in cash and cash equivalents (80,000)

Supporting computations:

(1)

Cash sales 825,000$

Collections on accounts receivable 2,200,000

Cash received from customers 3,025,000$

(2) Cash paid to suppliers and employees:

Cash payments for operating expenses 1,050,000

Cash paid to suppliers and employees 2,550,000$

(3) Proceeds from sales of plant assets:

Book value of plant assets sold 660,000$

Less: Loss on sales of plant assets 80,000

Proceeds from sales of plant assets 580,000$

SOLUTIONS TO PROBLEM SET A

Cash received from customers:

PROBLEM 13.1A

LAMBERT COMPANY

For the Year Ended December 31, Current Year

Statement of Cash Flows

LAMBERT COMPANY

Cash paid to suppliers and employees (2) (2,550,000)$

Interest paid (180,000)

Income taxes paid (95,000)