CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Prob. 27–2B (FIN MAN); Prob. 13–2B (MAN)

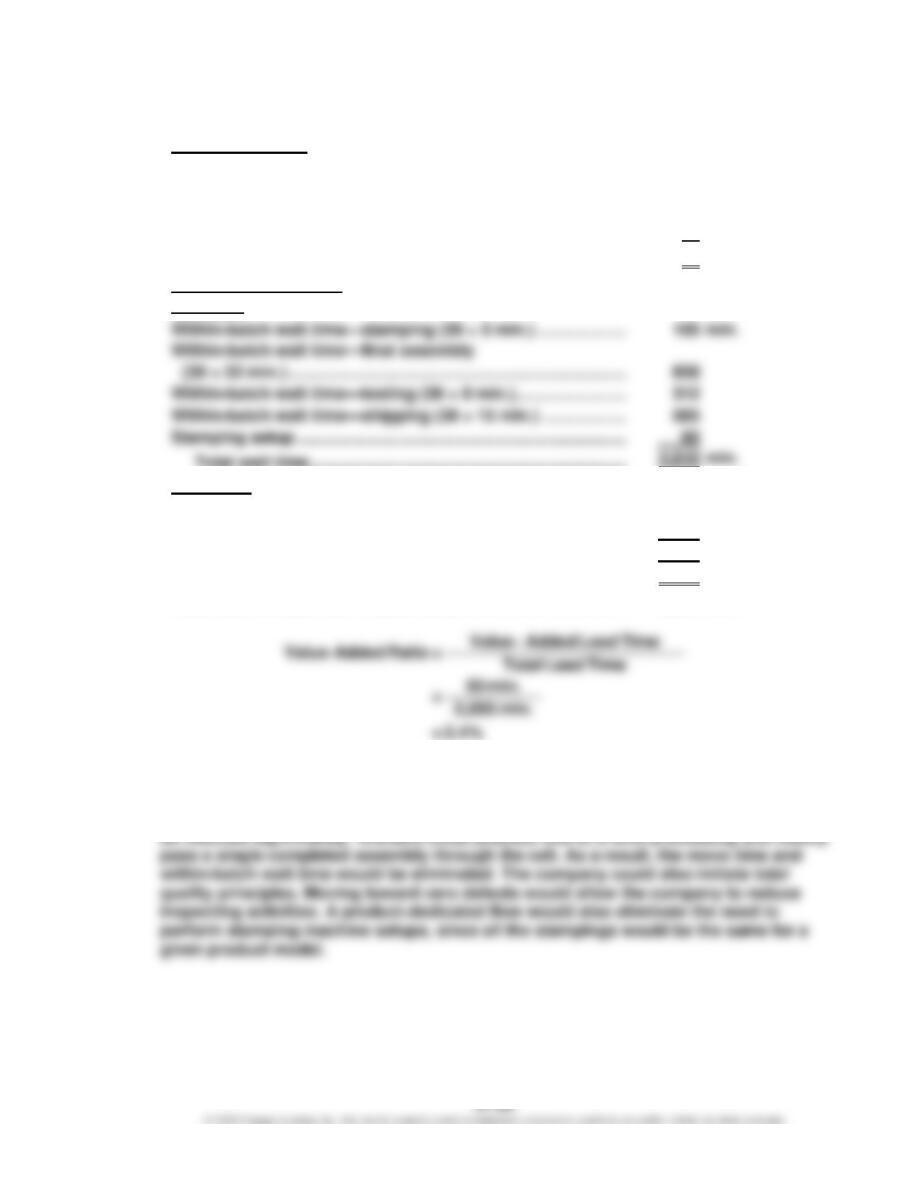

1.

Value-added time:

Stamping ………………………………………………………………………

5

min.

Appliance assembly ……………………………………………………….

22

Time to test one unit ………………………………………………………

8

Pack and shipment labeling ……………………………………………

15

Total …………………………………………………………………………

50

min.

Non-value-added time:

Wait time:

Within-batch wait time—stamping (39 × 5 min.) ……………….

min.

Within-batch wait time—final assembly

Within-batch wait time—testing (39 × 8 min.)……………………

Within-batch wait time—shipping (39 × 15 min.) ………………

Stamping setup ……………………………………………………………..

Total wait time …………………………………………………………..

Move time:

Move from stamping to final assembly …………………………...

10

min.

Move from final assembly to testing ………………………………..

25

Total move time …………………………………………………………

35

min.

Total non-value-added time …………………………………………….

2,045

min.

Total lead time (50 min. + 2,045 min.) ………………………………

2,095

min.

2. The existing process is very wasteful. The company could improve the process by

changing the layout from a process orientation to a product orientation. Each appliance

model could be formed into a production cell. Each cell would have stamping, final

assembly, testing, and shipping next to each other. In this way, the batch sizes could

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Prob. 27–3B (FIN MAN); Prob. 13–3B (MAN)

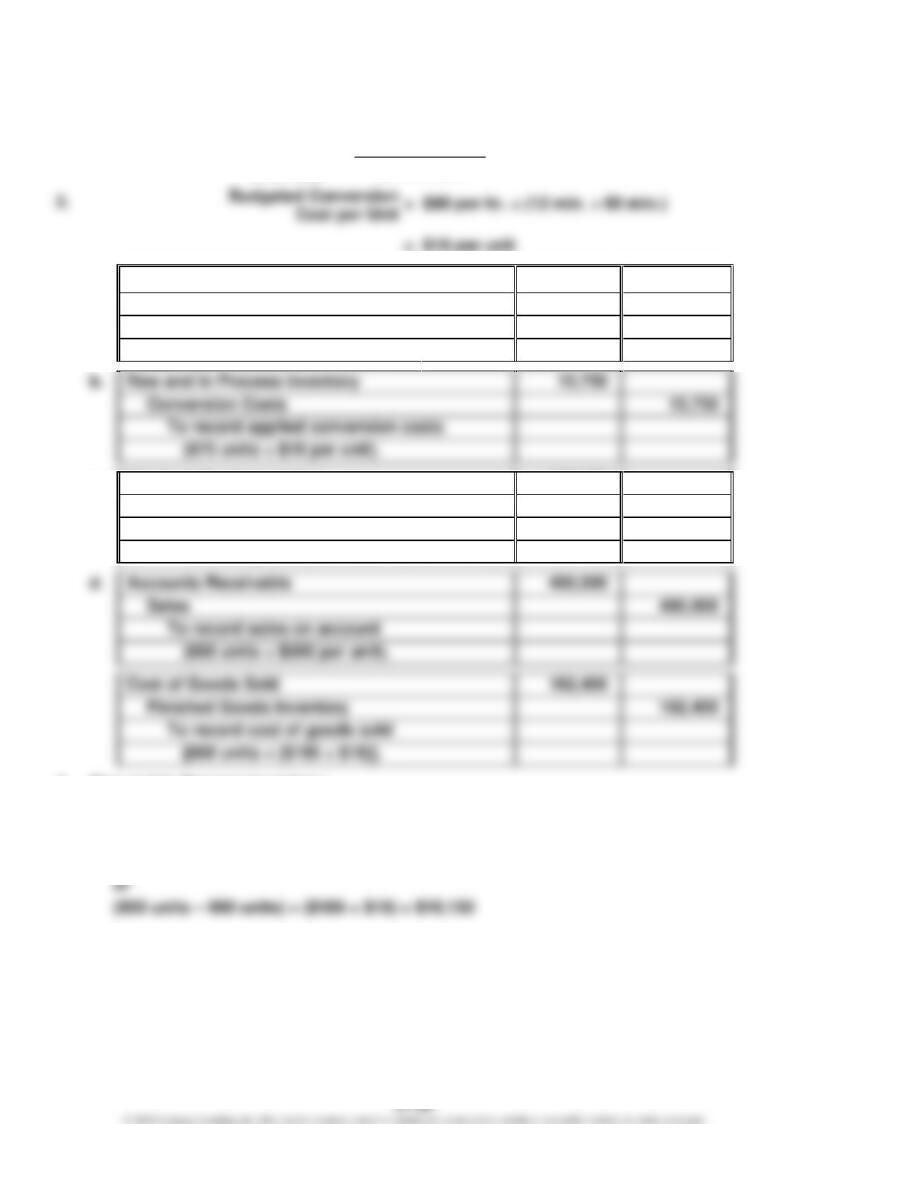

1.

Budgeted Cell Conversion $189,000

= = $90 per hour

2,100 hours

Cost Rate

=

$18 per unit

3.

a.

Raw and In Process Inventory

166,500

Accounts Payable

166,500

To record materials purchases

(900 units × $185 per unit).

To record applied conversion costs

c.

Finished Goods Inventory

172,550

Raw and In Process Inventory

172,550

To transfer the cost of completed units to

finished goods [850 units × ($185 + $18)].

To record sales on account

Finished Goods Inventory

162,400

To record cost of goods sold

4.

Raw and In Process Inventory:

$166,500 + $15,750 – $172,550 = $9,700

Finished Goods Inventory:

$172,550 – $162,400 = $10,150

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Prob. 27–3B (FIN MAN); Prob. 13–3B (MAN) (Concluded)

5. Lean accounting is different from traditional accounting in a number of respects.

Most importantly, lean accounting is simplified and uses minimal control. As a

result, the number of transactions is reduced, and the control intervals between

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Prob. 27–4B (FIN MAN); Prob. 13–4B (MAN)

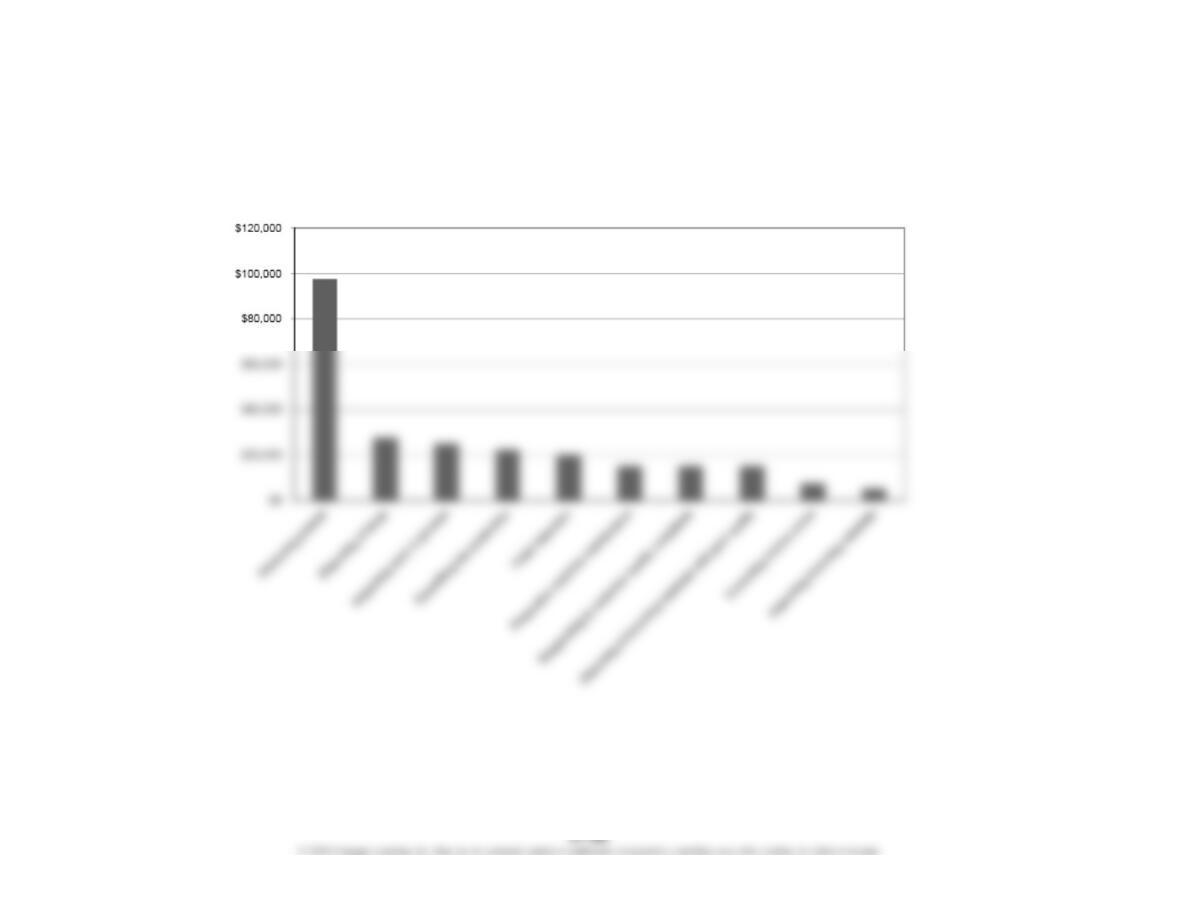

1.

Pareto Chart of Quality Activities

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Prob. 27–4B (FIN MAN); Prob. 13–4B (MAN) (Continued)

2. Activity classifications:

Activity

Cost

Cost of Quality

Classification

Value-Added/

Non-Value-Added

Classification

Activity

Correcting invoice errors ……

$ 7,500

External failure

Non-value-added

Disposing of incoming

materials with poor quality …

15,000

Internal failure

Non-value-added

Disposing of scrap …………….

27,500

Internal failure

Non-value-added

Expediting late production …

22,500

Internal failure

Non-value-added

Final inspection …………………

Inspecting incoming

materials ……………………….

Appraisal

Value-added

Inspecting work in process ..

25,000

Appraisal

Value-added

Preventive machine

maintenance ………………….

15,000

Prevention

Value-added

Producing product …………….

97,500

Not a quality cost

Value-added

Responding to customer

quality complaints …………

External failure

Non-value-added

3. Percent of total activity cost for each quality cost (and nonquality cost) classification:

Quality Cost Classification

Activity

Cost

Percent of Total

Department Cost

Prevention ……………………………………………..

$ 15,000

6%

Appraisal ……………………………………………….

Internal failure ………………………………………..

External failure ………………………………………

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

Prob. 27–4B (FIN MAN); Prob. 13–4B (MAN) (Concluded)

4. Percentages of total activity cost that are value- and non-value-added:

Activity

Cost

Percent of Total

Department Cost

5. The company has 65% of its total costs as value-added. However, there is still room

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

MAKE A DECISION

MAD 27–1 (FIN MAN); MAD 13–1 (MAN)

a.

Average

Lead Time

Total non-value-added lead time to arrive at clinical area …………..

60

min.

–Value – Added Lead Time

Value Added Ratio = Total Lead Time

c. The non-value-added lead time is related to waiting between each process element.

Adding resources to the process during the busier times of the day can reduce the

waiting. The check-in window could be expanded to multiple service lines, and the

admissions desk could be expanded to multiple desks. This would reduce the waiting

time between these activities. Adding more escorts could reduce the amount of time

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

MAD 27–2 (FIN MAN); MAD 13–2 (MAN)

Shield Insurance Company should adopt lean principles in its claims payment

operations. Management should first consider changing the layout for this process.

Instead of processing the claims payments through three different departments that are

organized by process, the company could design claims payment “cells” that are

organized around different types of insurance products or customers and consolidated

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

MAD 27–3 (FIN MAN); MAD 13–3 (MAN)

a.

Sterilization ……………………………………………………………..

15

minutes

Equipment and supply setup …………………………………….

2

Patient preparation …………………………………………………..

3

Total TAT …………………………………………………………….

20

minutes

c. Number of minutes in an eight-hour day: 480 minutes (8 hours × 60 minutes)

Sum of TAT and surgical time per procedure under the old process: 40 minutes

TAT + 40 minutes surgical time = 80 minutes

Number of surgeries 480 minutes per day = 6 surgeries

80 minutes total time per surgery

under the old process:

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

MAD 27–4 (FIN MAN); MAD 13–4 (MAN)

a. and b.

Elapsed

Time (a)

Activity

Value-Added

Time

Non-

Value-Added

Time (b)

1:00

p.m.

Arrives at doctor office

1:25

Waits in waiting room (5 × 5 min.)

25

min.

1:30

Waits in examining room

5

1:40

Nurse takes readings

10

min.

2:10

Waits in examining room

2:15

Doctor performs diagnosis

2:25

Waits to pay for services

2:30

Walks to pharmacy

2:50

Waits to fill prescription (4 × 5 min.)

20

2:55

Prescription is filled

3:10

Drives home

Simmons arrives home at 3:10 p.m.

Of the total elapsed time of 130 minutes, 90 minutes is non-value-added time.

c.

–

–Value Added Lead Time 40 min.

Value Added Ratio = = = 30.8%

Total Lead Time (40 min. + 90 min.)

d. The doctor requires patients to wait in order to increase the productivity of the office.

The patients represent the “work in process inventory” of the office, while the

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

TAKE IT FURTHER

TIF 27–1 (FIN MAN); TIF 13–1 (MAN)

The controller should confront the plant manager. The plant manager is attempting to

skew the sampling results by giving the sampled items special treatment. The original

intent of the sampling plan is to represent the average performance of the manufacturing

process. Thus, the tagged items should receive no better treatment than the average

not met.

The controller should first insist that the plant manager issue a new memo to all

employees, reversing the first memo. The controller should help the plant manager see

that skewing the results will provide only a short-term benefit. Eventually, this action will

come back to haunt them as the real performance of the plant becomes evident to

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

TIF 27–2 (FIN MAN); TIF 13–2 (MAN)

This would be a good assignment for the teams to report back to the class. Each of the

groups will likely go to different restaurants at different times of the day and will have

different results. The results could be shared with the class, and “averages” could be

determined for the various non-value-added categories.

Note to Instructors: The following types of activities will likely be noted in students’ reports:

Waiting to be seated ……………………………………………..

Non-value-added

Being seated ………………………………………………………..

Value-added

Waiting to give drink order…………………………………….

Non-value-added

Waiting to receive drink ………………………………………..

Non-value-added

Giving meal order …………………………………………………

Value-added

Waiting for meal order …………………………………………..

Non-value-added

Waiting for check (after meal is finished) ……………….

Non-value-added

Reviewing check (appraisal) ………………………………….

Value-added

Waiting to pay with credit card ………………………………

Non-value-added

TIF 27–3 (FIN MAN); TIF 13–3 (MAN)

Memo

To: Ethan Fromme

From: Ima Student

Re: Analysis of quality, cost, availability, and response time

A review of Maximal’s three performance charts indicates a steadily deteriorating

situation. Chart A shows that inventory steadily increased during the year, while Chart B

shows that the company’s ability to meet sales orders on time has steadily decreased.

CHAPTER 27 (FIN MAN); CHAPTER 13 (MAN) Lean Manufacturing and Activity Analysis

CERTIFIED MANAGEMENT ACCOUNTANT (CMA®)

EXAMINATION QUESTIONS (ADAPTED)

1. c. Prevention costs include design engineering ($300,000), supplier evaluation

2. b. Appraisal costs are incurred to detect individual units that do not conform to

specifications, e.g., inspecting raw materials.

3. b. Appraisal costs are incurred to detect individual units that do not conform to