415

E13–24

Time variance:

Direct Labor Time Variance = (Actual Direct Labor Hours – Standard Direct

Labor Hours) × Standard Rate per Hour

= (1,100 hrs. – 1,050 hrs.*) × $19.00 per hour

= $950 Unfavorable Variance

*3 hrs. × 350 units

Also computed as:

Actual total direct labor cost (1,100 hrs. × $18.50) ……………. $20,350

Less standard total direct labor cost (1,050 hrs. × $19.00) … (19,950)

Total direct labor unfavorable cost variance …………………. $ 400

416

E13–25

Step 1: Determine the standard direct materials and direct labor per unit.

Standard direct materials quantity per unit:

Step 2: Using the standard quantity and time rates from Step 1, determine the

standard costs for the actual August production.

Step 3: Determine the direct materials quantity and direct labor time variances,

assuming no direct materials price or direct labor rate variances.

Actual direct materials used in production …………………………………. $ 13,320

Standard direct materials (Step 2) ……………………………………………… (12,250)

Direct materials quantity variance—unfavorable ………………………… $ 1,070*

*(33,300 lbs. – 30,625 lbs.) × $0.40 per lb. = $1,070 U

$13,320 ÷ $0.40 per lb. = 33,300 lbs.

$12,250 ÷ $0.40 per lb. = 30,625 lbs. or 24,500 books × 1.25 lbs. per book =

30,625 lbs.

E13–25, Concluded

Step 4: Determine the total variance, assuming no direct materials price or direct

labor rate variances.

E13–26

a. Actual weekly expenditure: 2 people × $21 per hr. × 36 hrs. per week = $1,512

b. Standard time used for the volume of admissions:

Unscheduled Scheduled Total

c. Actual minutes used (2 employees × 36 hrs. × 60 min.) ………. 4,320

Less standard minutes expected at actual volume ……………… (4,800)

Favorable time difference from standard ……………………………. (480)

Standard rate per minute …………………………………………………… × $0.35*

Direct labor time (efficiency) variance—favorable ………………. $ (168)

or

[(2 × 36 hours) – 80 hours] × $21 per hour = $(168)

418

P13–1

1.

A

B C D

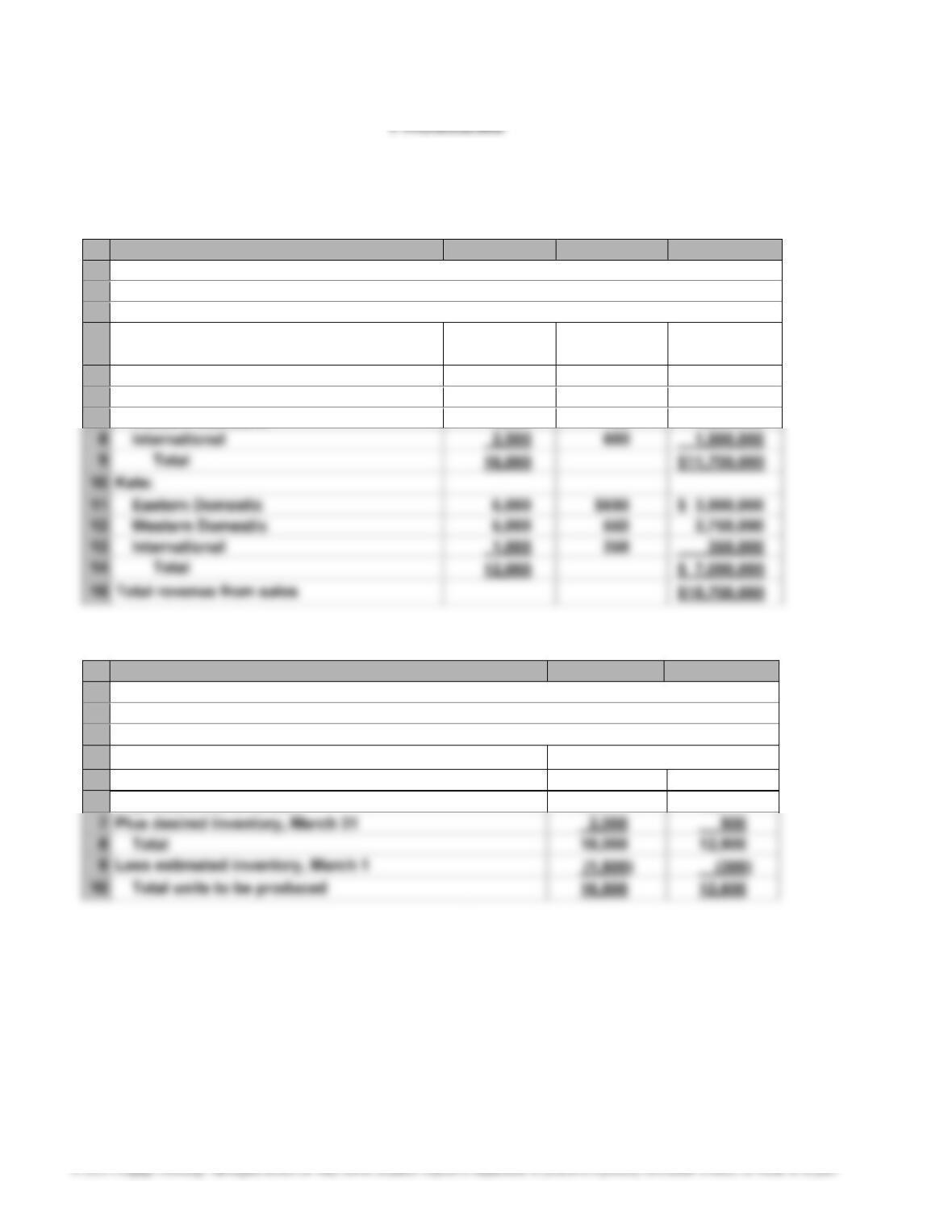

1 ROYAL BRITISH FURNITURE COMPANY

2 Sales Bud

g

et

3 For the Month Endin

g

March 31

Unit Sales Unit Sellin

g

4 Product and Area

V

olume Price Total Sales

5 William:

6 Eastern Domestic 7,500 $800 $ 6,000,000

7 Western Domestic 6,000 700 4,200,000

2.

A

B C

1 ROYAL BRITISH FURNITURE COMPANY

2 Production Bud

g

et

3 For the Month Ending March 31

4 Units

5 William Kate

6 Expected units to be sold 16,000 12,000

(

)

(

)

419

P13–1, Continued

3.

A

B C D E F

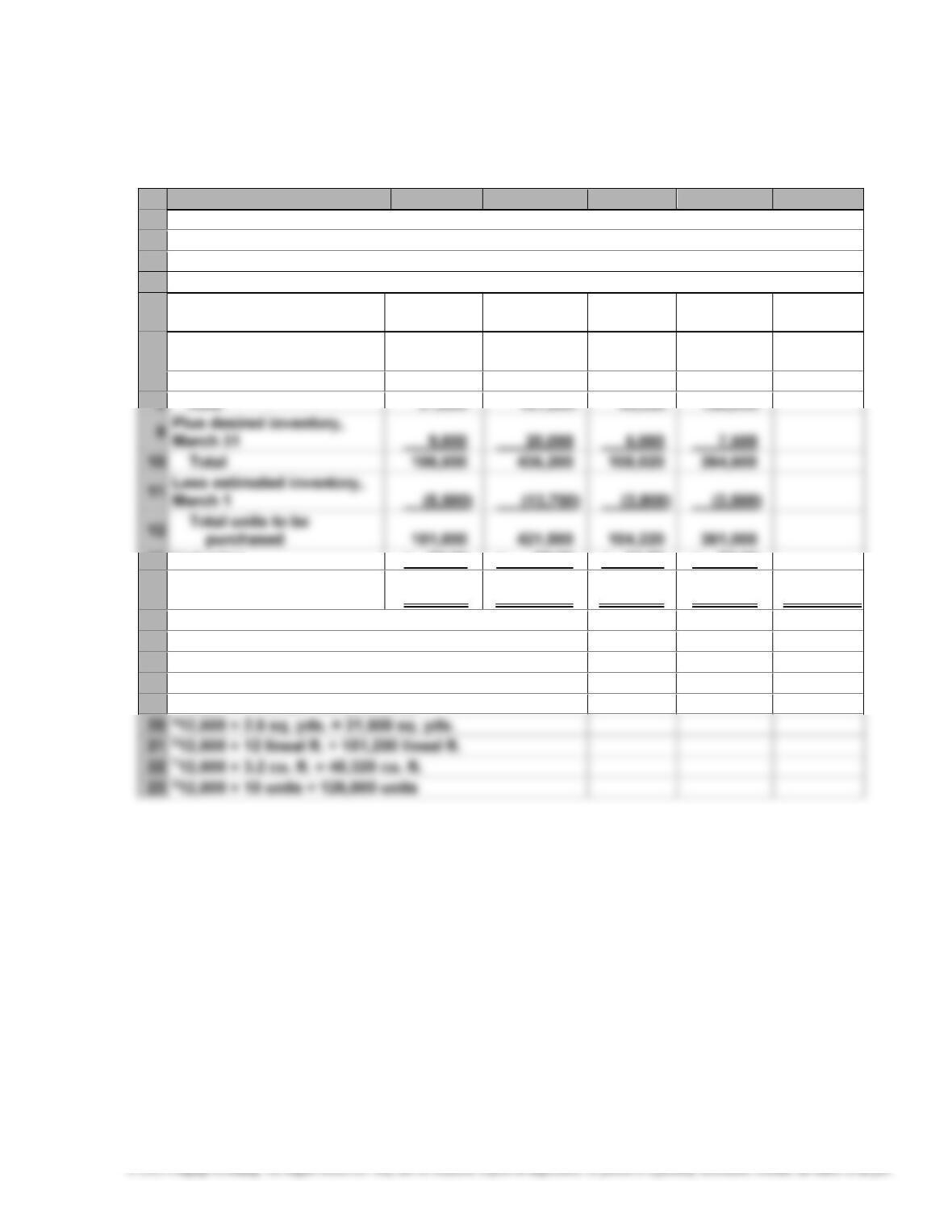

1 ROYAL BRITISH FURNITURE COMPANY

2 Direct Materials Purchases Bud

g

et

3 For the Month Endin

g

March 31

4 Direct Materials

5

Fabric

(

sq.

y

ds.

)

Wood

(

lineal ft.

)

Filler

(

cu. ft.

)

Springs

(

units

)

Total

6 Required units for

production:

7 William 66,0001 264,0002 62,7003 231,0004

(

)

(

)

(

)

(

)

13 Unit price × $9.00 × $5.00 × $1.50 × $2.00

14

Total direct materials to

be purchased

$909,000

$2,107,500

$156,330

$722,000

$3,894,830

15

16 116,500 × 4.0

y

ds. = 66,000 sq.

y

ds.

17 216,500 × 16 lineal ft. = 264,000 lineal ft.

18 316,500 × 3.8 cu. ft. = 62,700 cu. ft.

19 416,500 × 14 units = 231,000 units

420

P13–1, Concluded

4.

A

B C D E

1 ROYAL BRITISH FURNITURE COMPANY

2 Direct Labor Cost Bud

g

et

3 For the Month Endin

g

March 31

4 Framing

Department

Cutting

Department

Upholstery

Department

Total

5 Hours required for production:

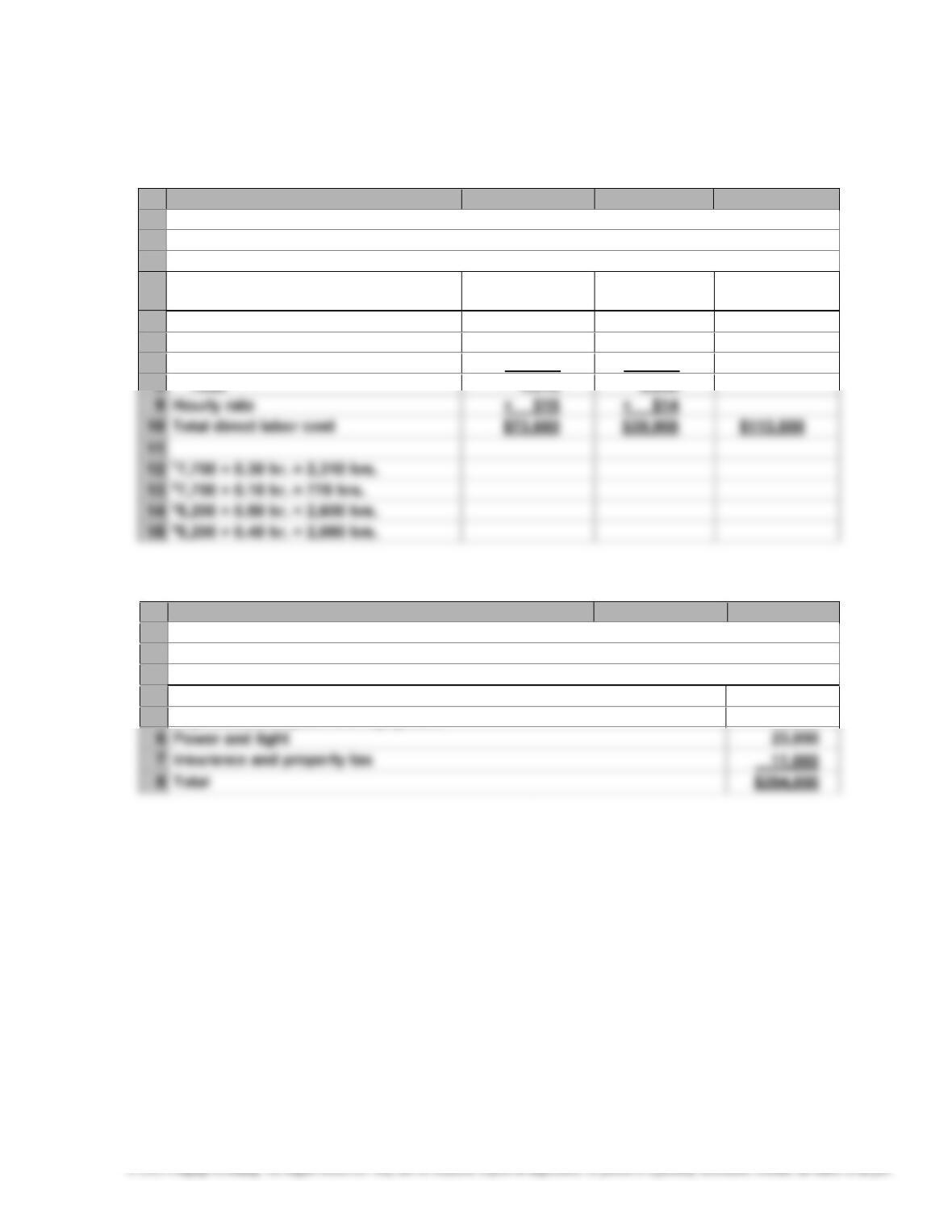

6 William* 41,250 16,500 49,500

421

P13–2

1.

A

B C D

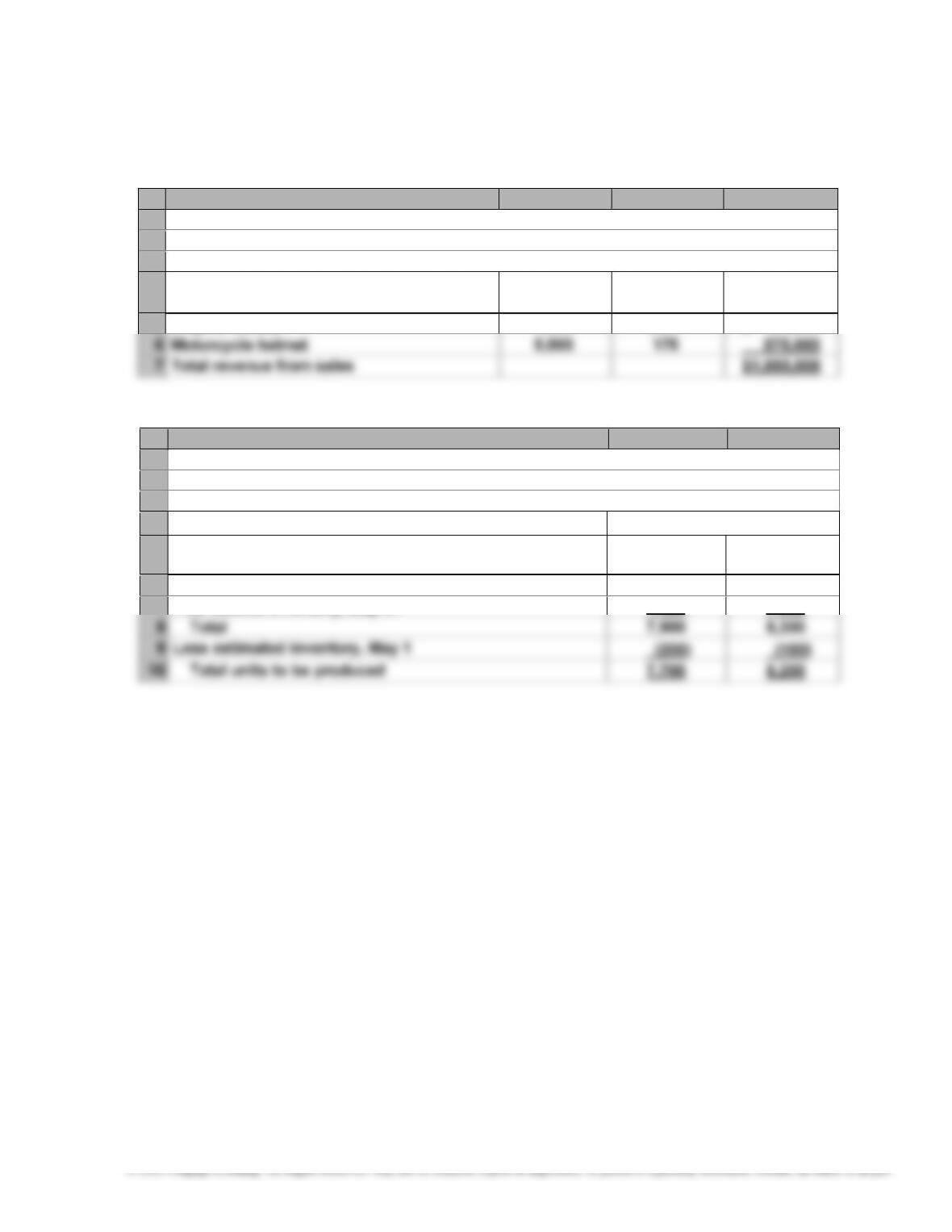

1 JUPITER HELMETS INC.

2 Sales Bud

g

et

3 For the Month Endin

g

Ma

y

31

4 Unit Sales Unit Sellin

g

V

olume Price Total Sales

5 Bic

y

cle helmet 7,500 $ 24 $ 180,000

2.

A

B C

1 JUPITER HELMETS INC.

2 Production Bud

g

et

3 For the Month Endin

g

Ma

y

31

4 Units

5

Bicycle

Helmet

Motorcycle

Helmet

6 Expected units to be sold 7,500 5,000

y

(

)

(

)

422

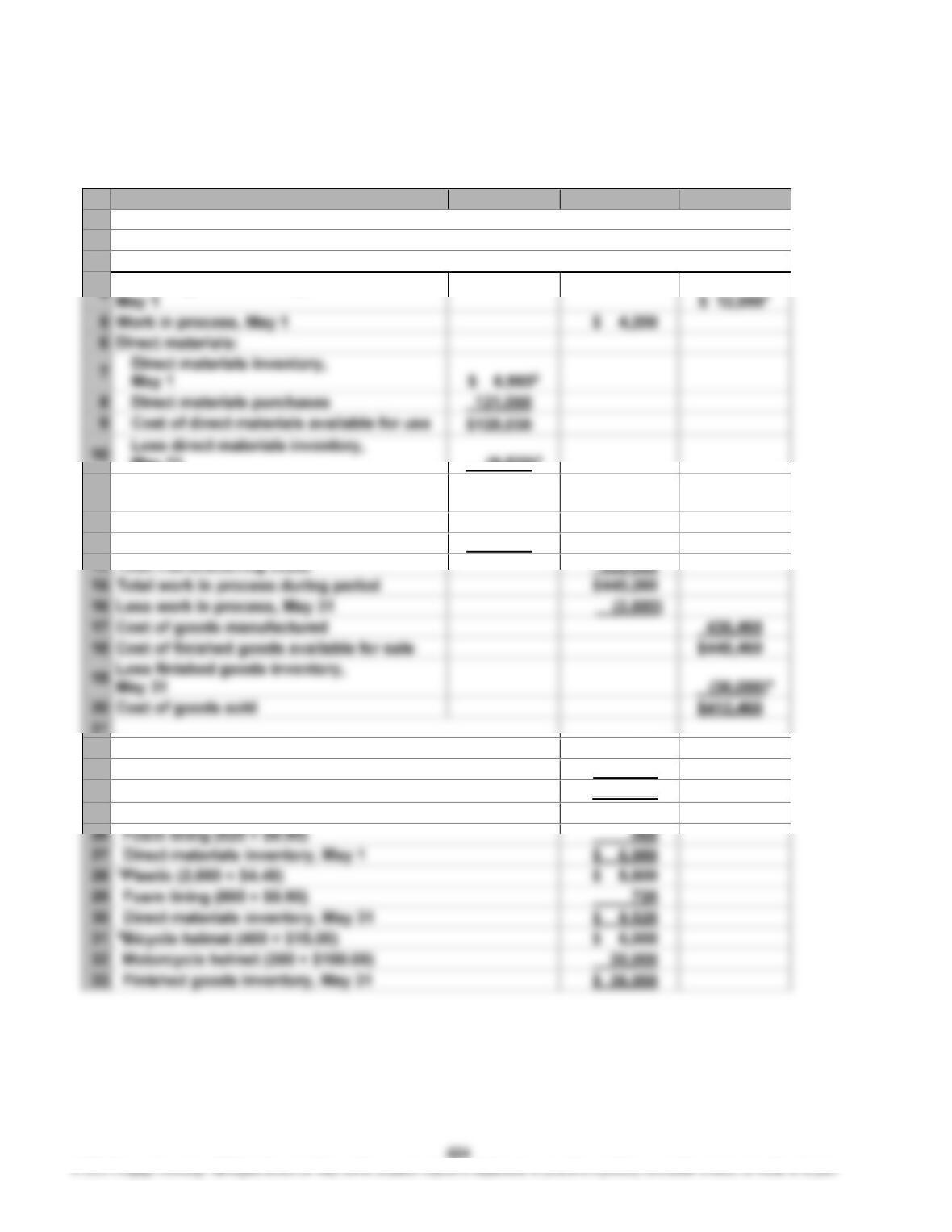

P13–2, Continued

3.

A

B C D

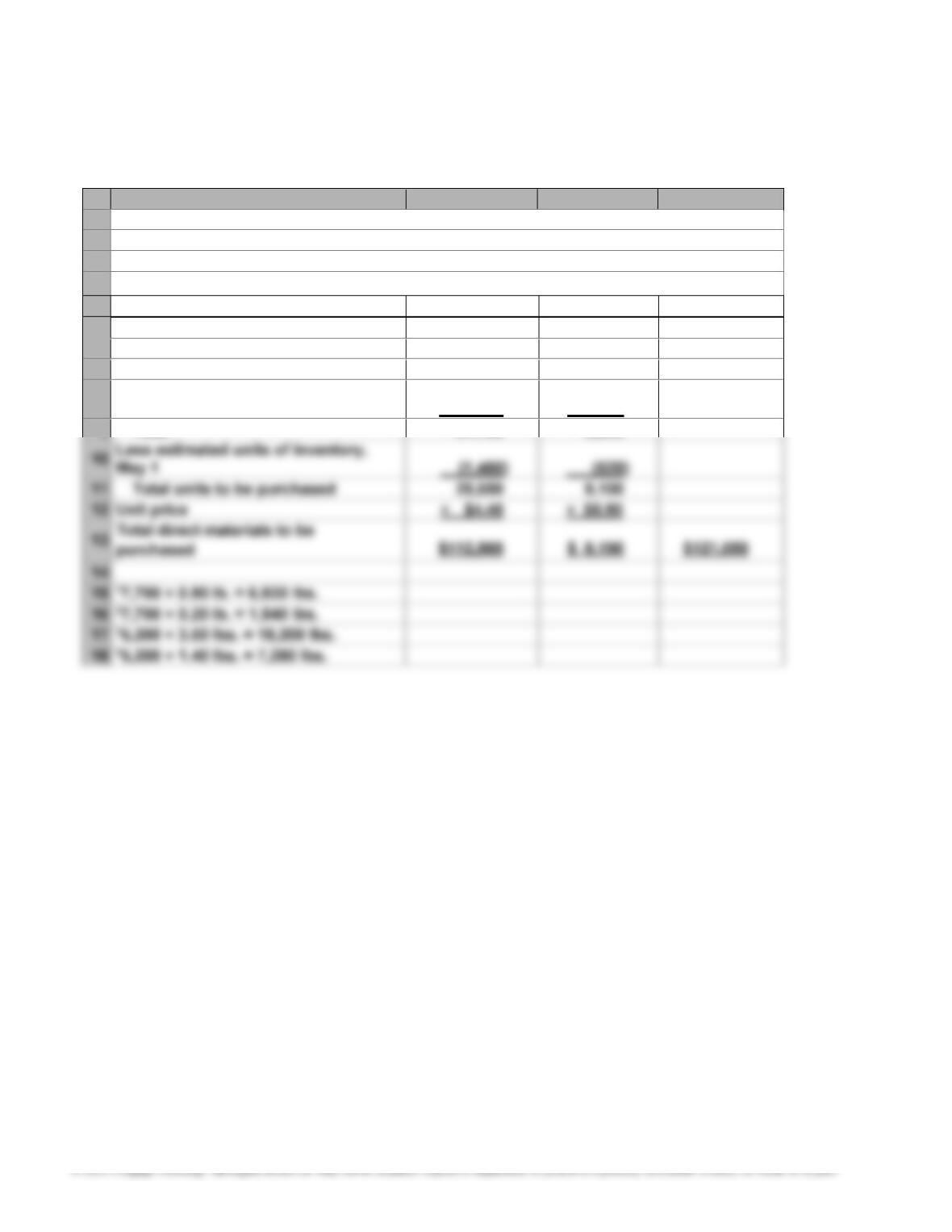

1 JUPITER HELMETS INC.

2 Direct Materials Purchases Bud

g

et

3 For the Month Endin

g

Ma

y

31

Direct Materials

4 Plastic Foam Linin

g

Total

5 Units required for production:

6 Bic

y

cle helmet 6,9301 1,5402

7 Motorc

y

cle helmet 18,2003 7,2804

8 Plus desired units of inventory,

Ma

y

31 2,000 800

y

423

P13–2, Continued

4.

A

B C D

1 JUPITER HELMETS INC.

2 Direct Labor Cost Bud

g

et

3 For the Month Endin

g

Ma

y

31

4 Molding

Department

Assembly

Department

Total

5 Hours required for production:

6 Bic

y

cle helmet 2,3101 7702

7 Motorc

y

cle helmet 2,6003 2,0804

r

r

r

r

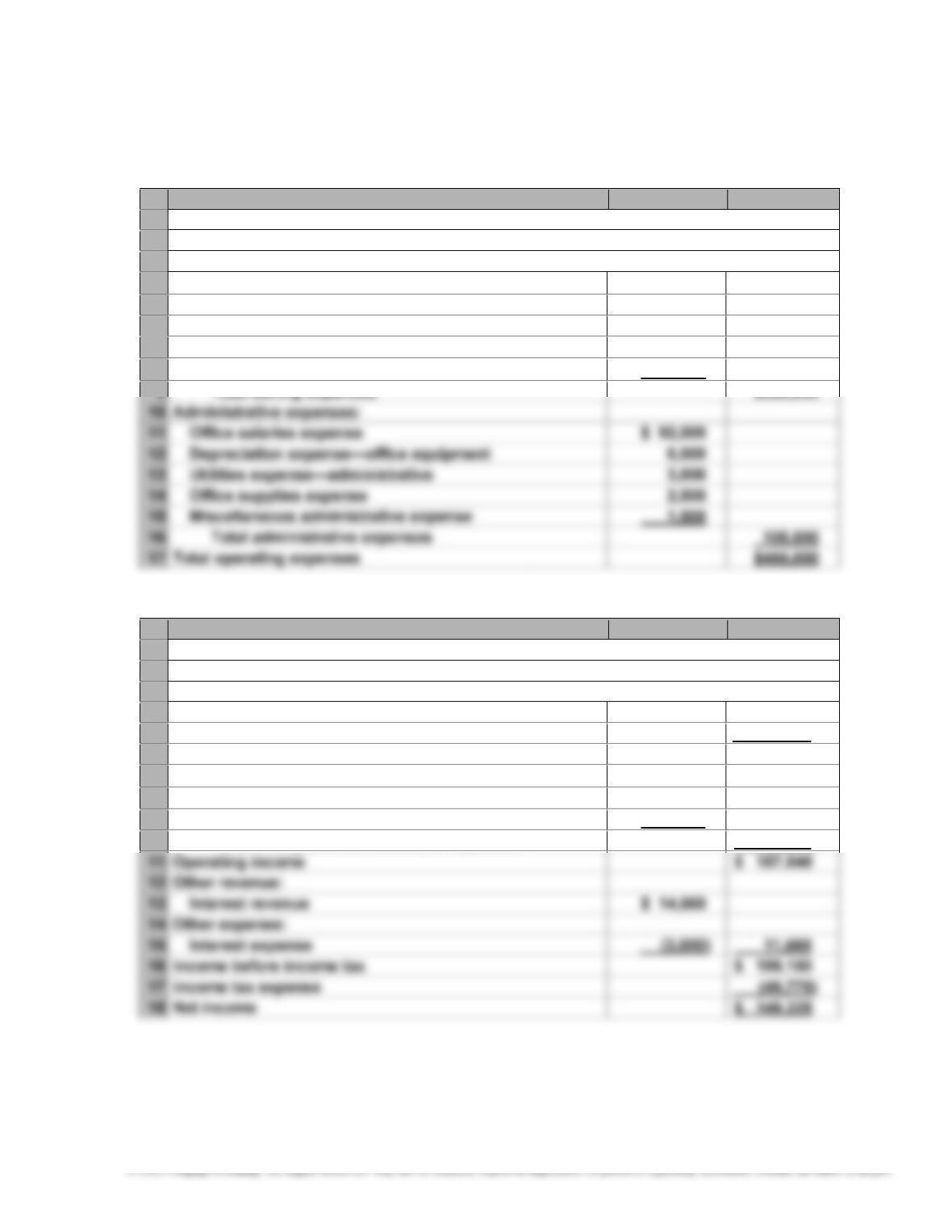

5.

A

B C

1 JUPITER HELMETS INC.

2 Factor

y

Overhead Cost Bud

g

et

3 For the Month Endin

g

Ma

y

31

4 Indirect factor

y

wa

g

es $125,000

5 Depreciation of plant and equipment 45,000

P13–2, Continued

6.

A

B C D

1 JUPITER HELMETS INC.

2 Cost of Goods Sold Bud

g

et

3 For the Month Endin

g

Ma

y

31

y

y

y

Ma

y

31

(

9,520

)

11 Cost of direct materials placed in

production $118,510

12 Direct labo

r

113,550

13 Factor

y

overhead 204,000

y

(

)

y

(

)

22 1Bic

y

cle helmet

(

200 × $15.00

)

$ 3,000

23 Motorc

y

cle helmet

(

100 × $90.00

)

9,000

24 Finished goods inventory, May 1 $ 12,000

25 2Plastic

(

1,480 × $4.40

)

$ 6,512

)

y

(

)

)

y

y

(

)

y

(

)

y

425

P13–2, Concluded

7.

A

B C

1 JUPITER HELMETS INC.

2 Sellin

g

and Administrative Expenses Bud

g

et

3 For the Month Endin

g

Ma

y

31

4 Selling expenses:

5 Sales salaries expense $175,000

6 Advertisin

g

expense 120,000

7 Travel expense—selling 50,000

8 Miscellaneous—selling 5,000

8.

A

B C

1 JUPITER HELMETS INC.

2 Bud

g

eted Income Statement

3 For the Month Endin

g

Ma

y

31

4 Revenue from sales $1,055,000

5 Cost of

g

oods sold

(

412,460

)

6 Gross profit $ 642,540

7 Selling and administrative expenses:

8 Selling expenses $350,000

9 Administrative expenses 105,000

10 Total Sellin

g

and administrative expenses

(

455,000

)

(

)

(

)

426

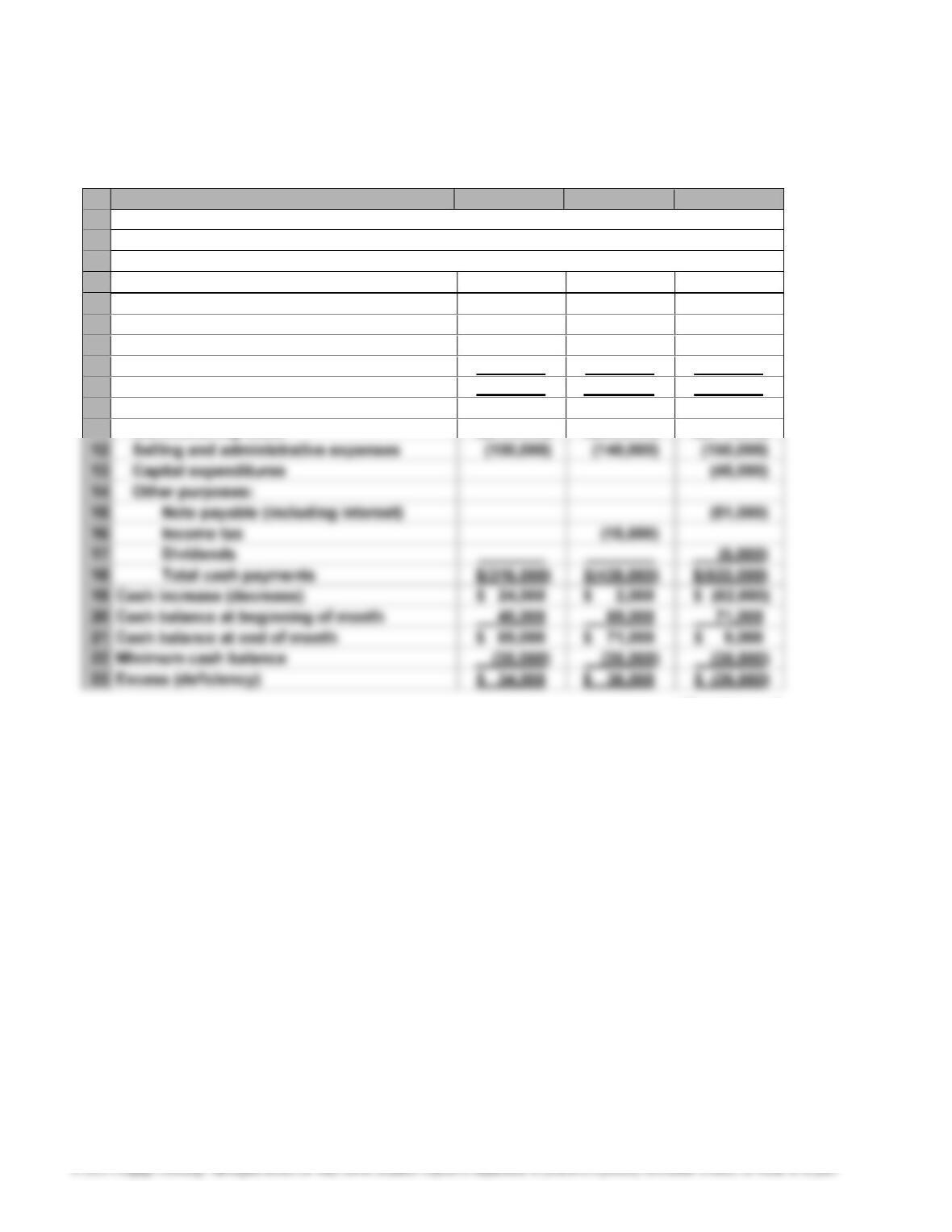

P13–3

1.

A

B C D

1 SHOE MART INC.

2 Cash Bud

g

et

3 For the Three Months Endin

g

March 31

4 Januar

y

Februar

y

March

5 Estimated cash receipts from:

6 Cash sales $ 90,000 $ 110,000 $ 140,000

7 Collections of accounts receivablea 230,000 330,000 420,000

8 Dividends 20,000 _ ______

9 Total cash receipts $ 340,000 $ 440,000 $ 560,000

10 Estimated cash pa

y

ments for:

(

(Continued)

427

P13–3, Concluded

24 Computations:

25 aCollections of accounts receivable: Januar

y

Februar

y

March

26 Novembe

r

sales $ 50,0001

y

32 2$240,000 × 75% = $180,000

33 3$240,000 × 25% = $60,000

34 4$450,000 × 80% × 75% = $270,000

35 5$450,000 × 80% × 25% = $90,000

36 6$550,000 × 80% × 75% = $330,000

37 bPa

y

ments for manufacturin

g

costs: Januar

y

Februar

y

March

38 Payment of accounts payable, beginning

of month balancec $ 18,000 $ 22,000 $ 29,000

39 Pa

y

ment of current month’s costd 198,000 261,000 342,000

40 Total $216,000 $283,000 $371,000

y

(

–

)

(

–

)

(

–

)

(

–

)

46

(

$420,000

–

$40,000

)

× 90% = $342,000

2. The budget indicates that the minimum cash balance will not be maintained in

March. This is due to the capital expenditures and note repayment requiring

significant cash outflows during the month. This situation can be corrected

428

P13–4

a. Standard

$4.60

b. Direct Materials Cost Variance

Price variance:

Direct Materials Price Variance = (Actual Price – Standard Price) × Actual Quantity

= ($1.40 per lb. – $1.25 per lb.) × 10,200 lbs.

= $1,530 Unfavorable Variance

Total direct materials cost variance:

Direct Materials Cost Variance = Direct Materials Price Variance + Direct

Materials Quantity Variance

= $1,530 + $750

= $2,280 Unfavorable Variance

Also computed as: