EXERCISE 13-6

(a) EUDALEY CORPORATION

Condensed Income Statement

For the Years Ended December 31

Increase or (Decrease)

During 2014

2014 2013 Amount Percentage

Net sales

$598,000

$500,000

$98,000

19.6%

(b) EUDALEY CORPORATION

Condensed Income Statements

For the Years Ended December 31

2014 2013

$ Percent $ Percent

Net sales

$598,000

100.0%

$500,000

100.0%

EXERCISE 13-7

Current ratio = 2.01:1 ($4,054 ÷ $2,014)

Current cash debt coverage = .69 ($1,251 ÷ $1,807.5a)

EXERCISE 13-8

Current ratio as of February 1, 2014 = 3.00:1 ($120,000 ÷ $40,000).

Feb. 3 3.00 No change in total current assets or liabilities.

EXERCISE 13-9

(a) Current ratio = $145, 000

$50, 000 = 2.90:1

(e) Days in inventory = 365 days ÷ 3.6 = 101.4 days

EXERCISE 13-10

(a) Profit margin $75.9

$5,121.8 = 1.5%

EXERCISE 13-11

(a) Earnings per share $72,000 – $5,000

32,000+ 40,000

2

⎡

⎣

⎢⎤

⎦

⎥

= $67, 000

36, 000 = $1.86

EXERCISE 13-12

(a) Inventory turnover = 3.8 = Cost of goods sold

$200,000 + $180,000

2

⎡

⎣

⎢ ⎤

⎦

⎥

(c) Return on common stockholders’ equity = 22% =

(d) Return on assets = 18% = Net income

Average assets = $111,595 [see (c) above]

Average assets

EXERCISE 13-13

2014 2013

(a) Current ratio:

$1,390 ÷ $820 = 1.70:1

(c) Profit margin:

$252 ÷ $3,800 = 6.6%

(e) Return on common stockholders’ equity:

$252/[($1,040 + $1,040) ÷ 2)] = 24.2%

(g) Times interest earned:

SOLUTIONS TO PROBLEMS

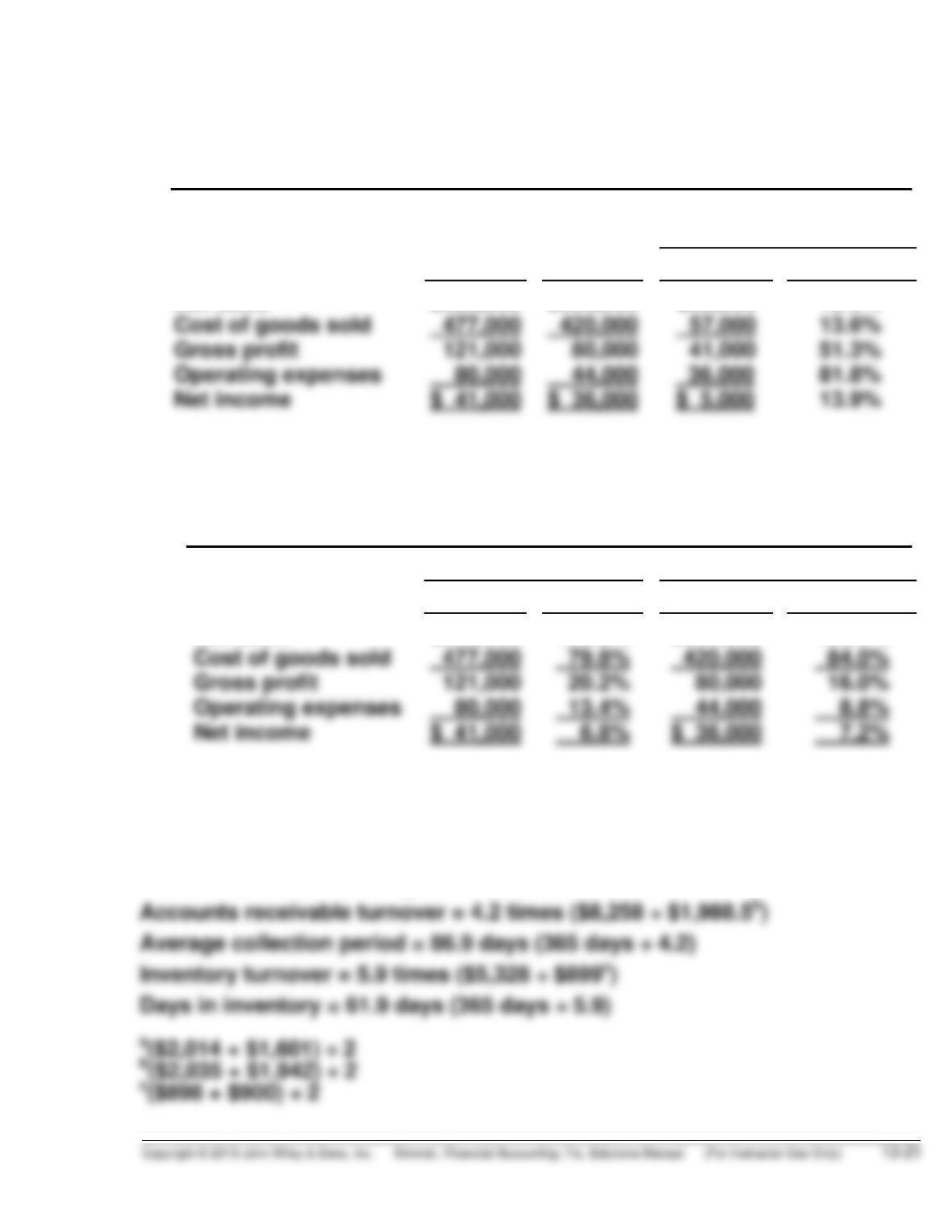

PROBLEM 13-1A

(a) Condensed Income Statement

For the Year Ended December 31, 2014

Prince Company King Company

Dollars Percent Dollars Percent

Net sales

$1,849,000

100.0%

$546,000

100.0%

(b) King Company appears to be more profitable. It has higher relative

gross profit, income from operations, income before taxes, and net in-

PROBLEM 13-1A (Continued)

a$477,000 is Prince’s 2014 net income. $832,593 is Prince’s 2014

average assets:

2014 2013

Current assets

$325,975

$312,410

b$143,400 is King’s 2014 net income. $214,172 is King’s 2014 average

aassets:

2014 2013

Current assets

$ 83,336

$ 79,467

c$477,000 is Prince’s 2014 net income. $659,528 is Prince’s 2014

average stockholders’ equity:

2014 2013

Common stock

$500,000

$500,000

d$143,400 is King’s 2014 net income. $154,047 is King’s 2014 average

dstockholders’ equity:

2014 2013

Common stock

$120,000

$120,000

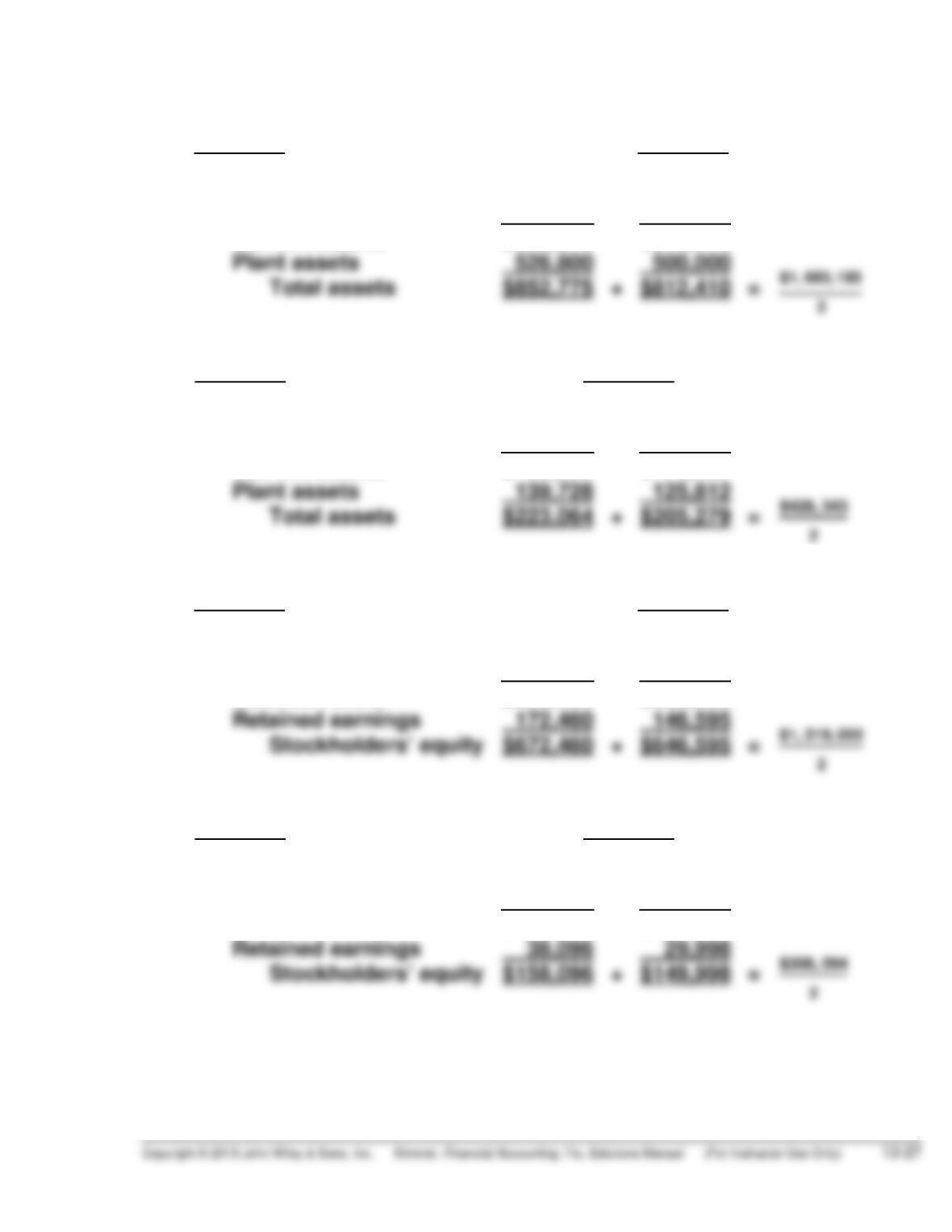

PROBLEM 13-2A

(a) Earnings per share = $218, 000

59, 000 (1) = $3.69

(b) Return on common stockholders’ equity = $218,000

$465,400 + $603,400

⎡

PROBLEM 13-2A (Continued)

(g) Inventory turnover = $1,058,540

$115,500 + $126,000

⎡

= $1, 058, 540

$120,750 = 8.8 times

(l) Current cash debt coverage = $220,000

$187,400 + $203,500

⎡

= 1.13 times

PROBLEM 13-3A

(a) 2014 2013

(1) Profit margin.

(2) Gross profit rate.

(3) Asset turnover.

(4) Earnings per share.

(5) Price-earnings ratio.

(6) Payout ratio.

(7) Debt to assets ratio.

PROBLEM 13-3A (Continued)

(b) The underlying profitability of the corporation appears to have improved.

For example, profit margin and earnings per share have both increased.

PROBLEM 13-4A

(a) LIQUIDITY

2013 2014 % Change

Accounts

$790,000

1%

PROFITABILITY

Profit

margin

$48,000

$790,000 = 6.1% $52,000

$882,000 = 5.9% (3%)

PROBLEM 13-4A (Continued)

(b) 2014 2015 %Change

1. Return on

3. Price-

earnings

ratio

$9.00

$2.60 = 3.5 times $12.00

$2.70 (c) = 4.4 times 26%

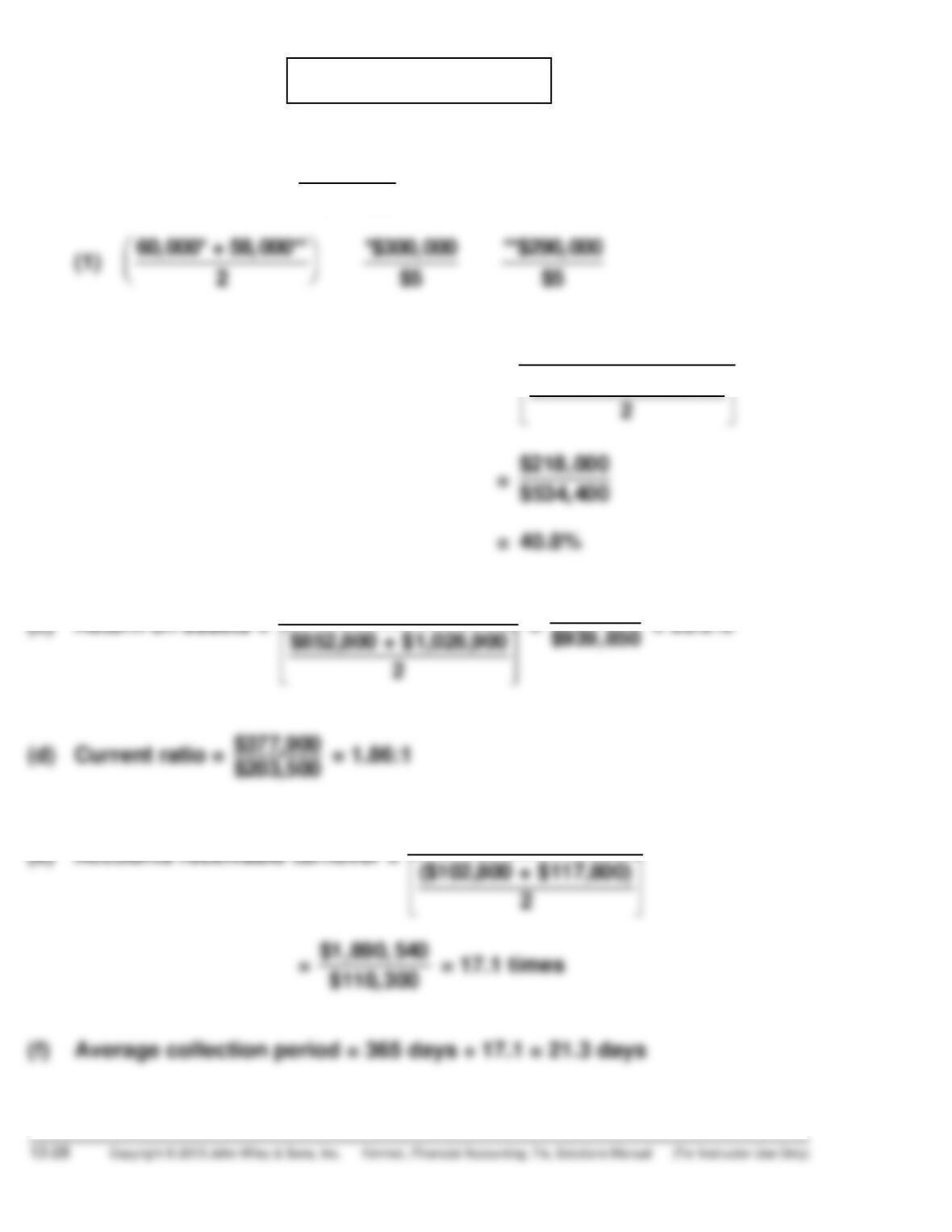

PROBLEM 13-5A

(a) Ratio Target Wal-Mart

(All Dollars Are in Millions)

(1) Current ratio

(2) Accounts receivable

stockholders’ equity

(10) Debt to assets ratio

1.63:1 ($18,424 ÷ $11,327)

17.1 % ($2,488 ÷ $14,529.5b)

66 % ($29,186 ÷ $44,533)

.87:1 ($48,331 ÷ $55,561)

21.0% ($14,335 ÷ $68,369g)

58% ($99,650 ÷ $170,706)

a

($44,533 + $44,106) ÷ 2 f($170,706 + $163,429) ÷ 2

(b) The comparison of the two companies shows the following:

Liquidity—Target’s current ratio of 1.63:1 is better than Wal-Mart’s .87:1.

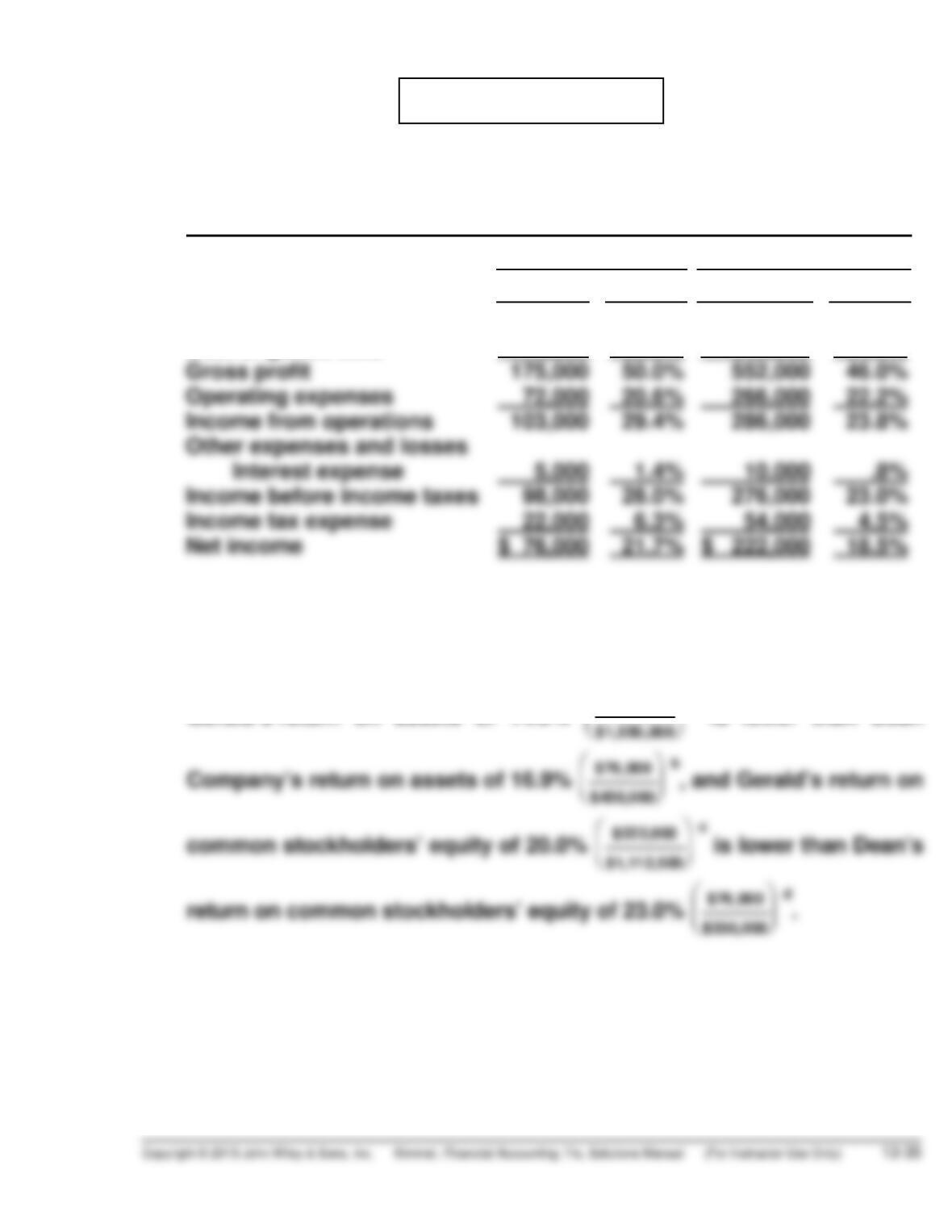

PROBLEM 13-1B

(a) Condensed Income Statement

For the Year Ended December 31, 2014

Dean Company Gerald Company

Dollars Percent Dollars Percent

Net sales

Cost of goods sold

$350,000

175,000

100.0%

50.0%

$1,200,000

648,000

100.0%

54.0%

(b) Dean Company appears to be more profitable. It has higher relative

income from operations, income before taxes, and net income.

Gerald’s return on assets of 14.3% $222,000

⎛

a is lower than Dean

PROBLEM 13-1B (Continued)

a$222,000 is Gerald’s 2014 net income. $1,550,000 is Dean’s 2014

average assets: Return on assets = ($222,000 ÷ $1,550,000) = 14.3%

2014 2013

Current assets

$ 700,000

$ 650,000

b$76,000 is Dean’s 2014 net income. $450,000 is Dean’s 2014 average

assets: Return on assets = ($76,000 ÷ $450,000) = 16.9%

2014 2013

c$222,000 is Gerald’s 2014 net income. $1,112,500 is Gerald’s 2014

average stockholders’ equity: Return = $222,000 ÷ $1,112,500 = 20.0%

2014 2013

d$76,000 is Dean’s 2014 net income. $330,000 is Dean’s 2014 average

stockholders’ equity: Return = $76,000 ÷ $330,000 = 23%

2014 2013

PROBLEM 13-2B

(b) Return on common stockholders’ equity = $119,200

$376,000 + $480,300

⎡

⎤

PROBLEM 13-2B (Continued)

(g) Inventory turnover = $440,000

$74,000 + $116,400

2

⎡

⎣

⎢⎤

⎦

⎥

= $440,000

$95,200 = 4.6 times

(l) Current cash debt coverage = $108,000

$163,500 + $156,000

⎡

= $108,000

$159,750 = .68 times

PROBLEM 13-3B

(a) 2014 2013

(1) Profit margin.

$110,000

$760,000 = 14.5% $85,000

$700,000 = 12.1%

(4) Earnings per share.

$110,000

= $2.97 $85,000

= $2.66

(6) Payout ratio.

(7) Debt to assets ratio.

PROBLEM 13-3B (Continued)

(b) The underlying profitability of the corporation has improved. For example,

the profit margin and gross profit rate have both improved. In addition,