Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 13—Statement of Cash Flows

Financial and Managerial Accounting, 18e 13-1

13 STATEMENT OF CASH FLOWS

Chapter Summary

The statement of cash flows was introduced in Chapter 1. This chapter begins by

reviewing the purpose of the statement. Its usefulness to creditors and investors in evaluating

solvency is emphasized from the outset. The classification of cash transactions into operating,

investing, and financing activities is explained in full. This section includes an explanation of the

reasoning behind the classification of interest receipts, interest payments, and dividend receipts

as operating activities. We also take the opportunity at the outset to highlight the importance of

cash flows from operating activities.

The approach to preparing the statement centers on analyzing the income statement and

the associated changes in noncash balance sheet accounts. The approach is introduced using a

simple illustration based on changes in the balance of the marketable securities account. We then

apply this methodology to an example that develops the entire statement.

The direct method is used to compute cash flows from operating activities. Discussion of

the indirect method is also presented.

The analysis of flows from investing and financing activities is somewhat simpler than

that for operating activities and the coverage is as a result relatively brief.

The chapter concludes with a detailed discussion of the use of the SCF in developing

strategies to manage cash flows. Emphasis here is on the use of the accounting information by

internal management rather than investors and creditors external to the firm.

Learning Objectives

1. Explain the purposes and uses of a statement of cash flows.

2. Describe how cash transactions are classified in a statement of cash flows.

3. Compute the major cash flows relating to operating activities.

4. Compute the cash flows relating to investing and financing activities.

5. Distinguish between the direct and indirect methods of reporting operating cash flows.

6. Explain why net income differs from net cash flows from operating activities.

7. Compute net cash flows from operating activities using the indirect method.

8. Discuss the likely effects of various business strategies on cash flows.

9. Explain how a worksheet may be helpful in preparing a statement of cash flows.

Chapter 13—Statement of Cash Flows

13-2 Instructor’s Resource Manual

Brief Topical Outline

A. Statement of cash flows

1. Purposes of the statement

2. Example of a statement of cash flows—see Exhibit 13–1 (page 567)

3. Classification of cash flows

a. Operating activities

b. Investing activities

c. Financing activities

d. Why are receipts and payments of interest classified as operating

activities?—see International Case in Point (page 568)

e. Cash and cash equivalents

f. Cash versus accrual information

B. Preparing a statement of cash flows

1. Additional information

2. Operating activities

3. Investing activities

4. Financing activities

5. Cash and cash equivalents

6. Cash flows from operating activities

a. Cash received from customers

b. Interest and dividends received

7. Cash payments for merchandise and for expenses

a. Cash paid for purchases of merchandise

b. Cash payments for expenses

c. Cash paid to suppliers and employees

d. Cash payments for interest and taxes

e. A quick review

8. Cash flows from investing activities

a. Purchases and sales of securities

b. Loans made and collected—see Your Turn (page 576)

c. Cash paid to acquire plant assets

d. Proceeds from sales of plant assets

e. A quick review

9. Cash flows from financing activities

a. Short-term borrowing transactions

b. Proceeds from issuing bonds payable and capital stock

c. Cash dividends paid to stockholders

d. A quick review

10. Relationship between the statement of cash flows and the statement of

financial position—see Case in Point (page 579)

11. Reporting operating cash flows by the indirect method

12. Reconciling net income with net cash flows

13. The indirect method: a summary

14. Indirect method may be required in a supplementary schedule

Chapter 13—Statement of Cash Flows

Financial and Managerial Accounting, 18e 13-3

15. The statement of cash flows: a second look—see Pathways Connection (page

583) and Your Turn (page 584)

C. Managing cash flows

1. Budgeting: the primary cash management tool

2. What priority should managers give to increasing net cash flows?

a. Short-term results versus long-term growth

b. One-time boosts to cash flows

3. Some strategies for permanent improvements in cash flow

a. Deferring income taxes

b. Peak pricing

c. Develop an effective product mix—see Ethics, Fraud, & Corporate

Governance (page 587)

D. A worksheet for preparing a statement of cash flows

1. Data for an illustration

a. Additional information

2. The worksheet

a. Entries in the two middle columns

3. Entry

E. Concluding remarks

Topical Coverage and Suggested Assignment

Class

Meetings on

Chapter

Topical

Outline

Coverage

Discussion

Questions*

Brief

Exercises*

Exercises*

Problems*

Critical

Thinking

Cases*

1

A

1, 2, 3,

1, 3

1, 5

1, 6

2

B

6, 7, 8

5, 6

2, 4

2, 3

2

3

C – F

11, 13, 15

9

8, 9, 10

7, 8

*Homework assignment (to be completed prior to class)

Comments and Observations

Teaching Objectives for Chapter 13

In presenting the statement of cash flows, our teaching objectives are to:

1. Explain the content and usefulness of this financial statement.

2. Provide a brief history of this financial statement, distinguishing it from the statement of

changes in financial position and emphasizing the need for information regarding cash flows

in this era of corporate “takeovers.”

3. Describe the major classifications within the statement of cash flows. Emphasize the relative

importance of the net cash flow from operating activities.

Chapter 13—Statement of Cash Flows

13-4 Instructor’s Resource Manual

4. Briefly explain why it is that accounting records maintained on the accrual basis of

accounting do not show cash flows as balances of specific ledger accounts.

5. Explain how cash flows may be determined by examining income statement accounts and the

changes in related balance sheet accounts.

6. Illustrate the computation of the basic cash flows (direct method) relating to operating

activities. Emphasize the rationale underlying each computation.

7. Explain the basic reasons why net cash flow from operating activities may differ from the

amount of net income.

8. Illustrate the computation of cash flows relating to investing and financing activities. Again,

emphasize the rationale underlying each computation.

9. Briefly compare and contrast the direct and indirect methods of reporting net cash flows from

operating activities.

10. Discuss the critical importance of managing cash flows and introduce strategic options for

management to improve cash flows from existing operations.

General Comments

The direct and indirect methods Accountants often hear the comment: “Why do we need a

statement of cash flows? We can just look at the comparative balance sheet and see the change in

cash from one accounting period to the next.” While this is true, in order to understand the

changes in cash and cash equivalents and how such change may impact the company’s future

cash flows, users need to have an accurate picture of the specific inflows and outflows causing

the change. In this chapter, we teach students to classify cash flow transactions into the following

categories: operating activities, investing activities, and financing activities.

The next issue is whether to use the direct method or indirect method to prepare the

operating activities section of the statement of cash flows. While FASB has indicated a clear

preference for the direct method, we recognize the most companies in practice use the indirect

method. Therefore, the chapter teaches students to understand and prepare the statement of cash

flows using both the direct and indirect methods. The detailed illustration in the chapter assumes

the direct method as we feel that this method helps to enhance the student’s understanding of

business transactions and how such transactions impact not only the accrual based financial

statement accounts seen on the income statement and balance sheet but also the cash inflows and

outflows of the organization.

Chapter 13—Statement of Cash Flows

Financial and Managerial Accounting, 18e 13-5

Supplemental Exercises

Group Exercise

the most recent annual report and locate the Consolidated Statement of Cash Flows. Does

Macy’s use the direct method or indirect method of preparation? How can you tell? What are the

steps that would need to be taken in order to convert the statement to the direct method?

Internet Exercise

Obtain the latest annual report for ExxonMobil at the ExxonMobil website. Examine the

balance sheet. What amount of current liabilities is the company reporting as of the end of the

current accounting period? Now obtain the statement of cash flows. How much cash did

ExxonMobil generate from operating activities during this accounting period? Was this net cash

flow from operating activities sufficient to pay the company’s current liabilities? If not, how did

the company obtain the necessary cash to remain solvent?

Chapter 13—Statement of Cash Flows

13-6 Instructor’s Resource Manual

CHAPTER 13 NAME #

10-MINUTE QUIZ A SECTION

In order to prepare the statement of cash flows for Rag Dolls Corporation for 2018, the accountant has

compiled the following data regarding cash flows:

Cash paid to acquire marketable securities ........................................................ $ 370,000

Proceeds from sale of marketable securities ...................................................... 17,500

Proceeds from issuance of capital stock ............................................................ 280,000

Proceeds from issuance of bonds payable ......................................................... 55,000

Payments to settle short-term debt ..................................................................... 32,500

Interest and dividends received .......................................................................... 10,000

Cash received from customers ........................................................................... ?

Dividends paid .................................................................................................... 130,000

Cash paid to suppliers and employees ............................................................... 1,030,000

Interest paid ......................................................................................................... 25,000

Income taxes paid ............................................................................................... 70,000

Cash and cash equivalents, January 1, 2018 ...................................................... 43,000

Cash and cash equivalents, December 31, 2018 ................................................ 58,000

Using the above information, indicate the best answer for each question in the space provided.

1. Rag Dolls’ cash flow from investing activities during 2018 is:

a $390,000 net cash used by investing activities.

b $322,500 net cash provided by investing activities.

c $352,500 net cash used by investing activities.

d $360,000 net cash used by investing activities.

2. Rag Dolls’ cash flow from financing activities during 2018 is:

a $322,500 net cash provided by financing activities.

b $172,500 net cash provided by financing activities.

c $127,500 net cash provided by financing activities.

d $375,000 net cash provided by financing activities.

3. Rag Dolls’ cash flow from operating activities during 2018 is:

a $45,000 net cash provided by operating activities.

b $1,155,000 net cash used by operating activities.

c $240,000 net cash provided by operating activities.

d $195,000 net cash provided by operating activities.

4. In the 2018 statement of cash flows for Rag Dolls Corporation, the amount of cash received from

customers is:

a $1,310,000.

b $1,103,000.

c $1,233,000.

d $1,293,000.

Chapter 13—Statement of Cash Flows

Financial and Managerial Accounting, 18e 13-7

CHAPTER 13 NAME #

10-MINUTE QUIZ B SECTION

Use the following information for questions 1 through 4.

Lester Corporation’s statement of cash flows for 2017 shows the following investing activities:

Proceeds from sale of marketable securities ...................................................... $ 160,000

Purchase of land .................................................................................................. (250,000)

Proceeds from sale of land ................................................................................. _125,000

Net cash provided by investing activities ....................................................... $__35,000

Lester’s income statement for 2017 includes the following:

Loss on sale of marketable securities ................................................................. $47,000

Gain on disposal of land ..................................................................................... 65,000

1. Refer to the above data. The cost of the land sold during 2017 was:

a $65,000. b $125,000. c $190,000. d $60,000.

2. Refer to the above data. The cost (book value) of the marketable securities sold during 2017 was:

a $207,000. b $113,000. c $160,000. d Some other amount.

3. Refer to the above data. Lester’s balance sheet at the end of 2016 showed Land of $100,000. On the

basis of the data presented above, compute the amount to be reported for Land in Lester

Corporation’s balance sheet at December 31, 2017.

a $250,000. b $350,000. c $290,000. d Some other amount.

4. Refer to the above data. Lester’s balance sheet at the end of 2016 showed Investment in Marketable

Securities at $250,000. On the basis of the data presented above, compute the amount to be reported

for Investment in Marketable Securities in Lester Corporation’s balance sheet at December 31, 2017.

a $43,000. b $110,000. c $137,000. d $253,000.

5. Which of the following correctly describes a difference between the direct method and the indirect

method of computing operating cash flow?

a The direct method is used when accounting records are kept on a cash basis; the indirect

method is used when accounting records are maintained on an accrual basis.

b The direct method may be used only when a company maintains special journals for cash

receipts and cash disbursements; the indirect method is used in all other situations.

c Both the direct and the indirect methods result in the same net cash flow from operating

activities, but the format of this section of the statement of cash flows is different under the

alternative methods.

d The direct method is used when all accounting records and bank statements are available; the

indirect method is used when some accounting records or documents are missing or have

been destroyed.

Chapter 13—Statement of Cash Flows

13-8 Instructor’s Resource Manual

CHAPTER 13 NAME #

10-MINUTE QUIZ C SECTION

Using the following information, complete the statement of cash flows for Nutritional Foods for the year

ended December 31, 2018. Place parentheses around those figures in the statement representing cash outlays.

Payments for purchase of land ................................................................................................ $ 416,000

Proceeds from sale of land ...................................................................................................... $58,000

Proceeds from issuance of capital stock ................................................................................. $347,000

Proceeds from issuance of bonds payable .............................................................................. $99,000

Payments to settle short-term debt .......................................................................................... $74,000

Interest and dividends received .............................................................................................. $49,500

Cash received from customers ................................................................................................ $1,502,000

Dividends paid ........................................................................................................................ $182,000

Cash paid to suppliers and employees .................................................................................... $1,172,000

Interest paid .......................................................................................................................... $66,000

Income taxes paid .................................................................................................................... $115,500

Cash and cash equivalents, January 1, 2018 .......................................................................... $86,000

Cash and cash equivalents, December 31, 2018 .................................................................... ?

NUTRITIONAL FOODS

Statement of Cash Flows

For the Year Ended December 31, 2018

Cash flows from operating activities (direct method):

Cash received from customers ....................................................... $

_________

Cash provided by operating activities ........................................ $

$

_________

Cash disbursed for operating activities ...................................... (_______)

Net cash flows from operating activities ............................. $

Cash flows from investing activities:

$

_________

Net cash used by investing activities .................................. ( )

Cash flows from financing activities:

$

_________

Net cash provided by financing activities .......................... _______

Net increase (decrease) in cash ............................................................. $

Cash and cash equivalents, beginning of year ...................................... _______

Cash and cash equivalents, end of year ................................................ $______

Chapter 13—Statement of Cash Flows

Financial and Managerial Accounting, 18e 13-9

CHAPTER 13 NAME #

10-MINUTE QUIZ D SECTION____________________________________

The following balance sheets are provided for Socrates Foods:

End of Year Beginning of Year

Cash and cash equivalents ....................................................................... $170,000 $120,000

Accounts receivable ................................................................................. 80,000 65,000

Inventory .................................................................................................. 140,000 130,000

Plant and equipment (net) ........................................................................ _130,000 __80,000

Total assets ............................................................................................ $520,000 $395,000

Accounts payable (for merchandise) ....................................................... $ 65,000 $ 35,000

Wages payable ......................................................................................... 120,000 110,000

Long-term liabilities ................................................................................. 95,000 70,000

Common stock ......................................................................................... 100,000 100,000

Retained earnings ..................................................................................... _140,000 _80,000

Total liabilities and owners’ equity ...................................................... $520,000 $395,000

Selected information from Socrates Foods’ current year income statement:

Sales ................................................................................................................................ $1,650,000

Cost of goods sold ............................................................................................................ 840,000

Wages expense ................................................................................................................. 260,000

a Compute the following:

(1) Cash received from customers during the year ................................................... $__________

(2) Cash payments for merchandise during the year................................................. $__________

(3) Wages paid to employees during the year ......................................................... $__________

(4) In Socrates Foods’ statement of cash flows, what amount would be reported as the net change in cash

and cash equivalents?

$__________ (increase/decrease)

b Socrates Foods recorded the sale of equipment as follows:

Cash ................................................................................................ 25,000

Accumulated Depreciation: Equipment ........................................ 20,000

Loss on Disposal of Equipment ..................................................... 15,000

Equipment .................................................................................. 60,000

How would this transaction be reported in Socrates Foods’ statement of cash flows? (Assume the direct

method is being used.)

Chapter 13—Statement of Cash Flows

13-10 Instructor’s Resource Manual

SOLUTIONS TO CHAPTER 13 10-MINUTE QUIZZES

QUIZ A

1 C

QUIZ B

QUIZ C

NUTRITIONAL FOODS

Statement of Cash Flows

For the Year Ended December 31, 2018

Cash flows from operating activities:

Cash received from customers .......................................................... $ 1,502,000

Cash flows from financing activities:

Proceeds from issuing bonds payable ............................................... $ 99,000

Chapter 13—Statement of Cash Flows

Financial and Managerial Accounting, 18e 13-11

QUIZ D

Chapter 13—Statement of Cash Flows

13-12 Instructor’s Resource Manual

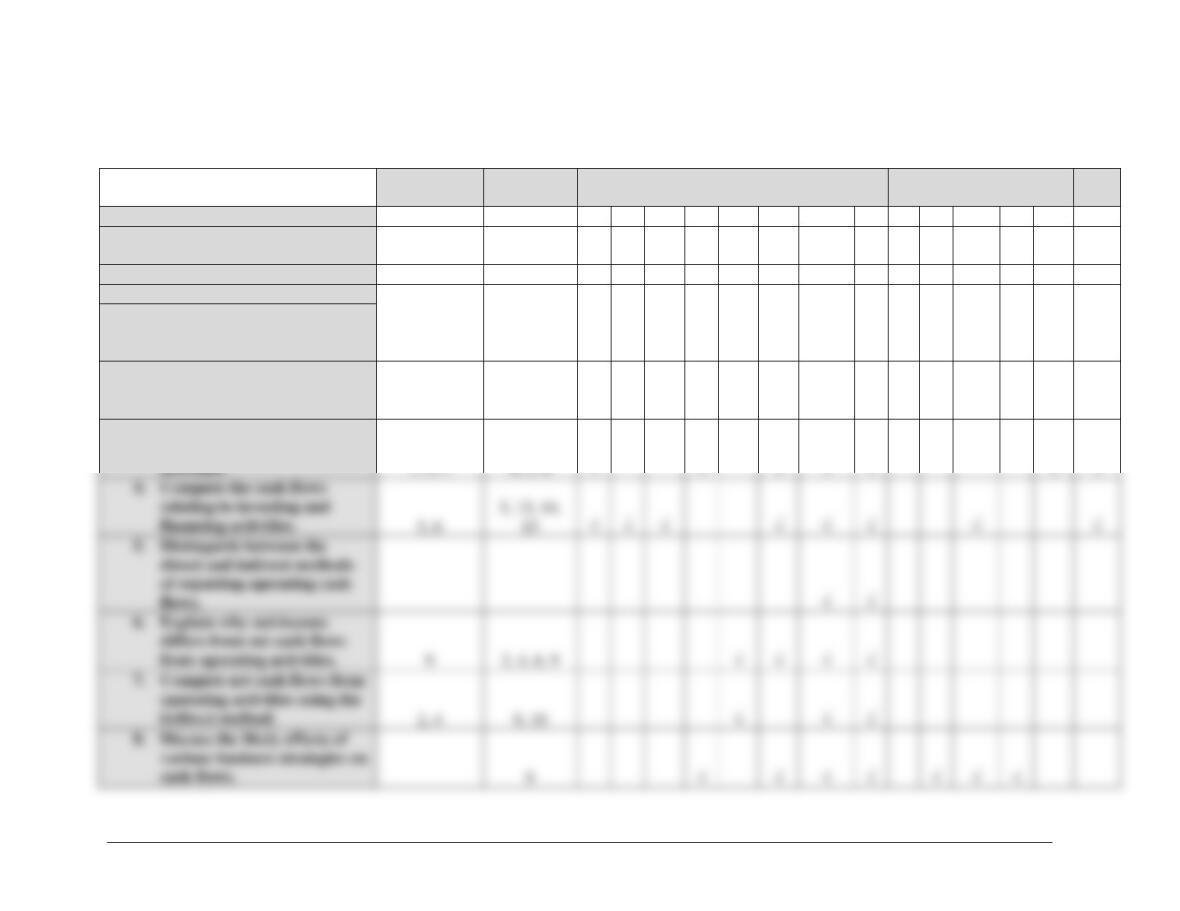

Assignment Guide to Chapter 13

Brief

Exercises

Exercises

Problems

Cases

Net

Item Number

1 – 10

1 – 15

1

2

3

4

5

6

7

8

1

2

3

4

5

6

Time estimate (in minutes)

< 15

< 15

30

25

25

30

25

45

60 A/

40 B

60

2

5

15

45

15

20

30

Difficulty rating

E

E

M

E

E

M

M

S

S

S

S

E

M

E

M

M

Learning Objectives:

1, 2, 15

1. Explain the purposes and

uses of a statement of cash

flows.

2. Describe how cash

transactions are classified in

a statement of cash flows.

8, 10

1, 2, 7, 11,

12, 15

3. Compute the major cash

flows relating to operating

Chapter 13—Statement of Cash Flows

Financial and Managerial Accounting, 18e 13-13

Brief

Exercises

Exercises

Problems

Cases

Net

9. Explain how a worksheet

may be helpful in preparing

a statement of cash flows.