779

Exercise 13-18 (Concluded)

Part 2

ALEXANDER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2017

Retained earnings, December 31, 2016 ………………………

$340,000

Treasury stock reissuances* …………………………….

Part 3

ALEXANDER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2017

Less cost of treasury stock ……………………………………….

Common stock⎯$25 par value, 50,000 shares

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 13

780

PROBLEM SET A

Problem 13-1A (30 minutes)

Part 1

a. To record sale of 10,000 ($250,000/$25 per share) shares of $25 par

value common stock for $30 ($300,000/10,000 shares) per share.

Part 2

Part 3

Part 4

Total paid-in capital from common stockholders

Part 5

Book value per common share

781

Problem 13-2A (60 minutes)

Part 1

Jan. 1

Treasury Stock, Common ………………………………………

80,000

Jan. 5

Retained Earnings …………………………………………………

72,000

Common Dividend Payable ……………………………………

72,000

July 6

Cash* …………………………………………………………………….

36,000

Aug. 22

Cash* …………………………………………………………………….

42,500

Retained Earnings …………………………………………………

Retained Earnings …………………………………………………

80,000

Common Dividend Payable ……………………………………

80,000

Dec. 31

Income Summary …………………………………………………..

782

Problem 13-2A (Concluded)

Part 2

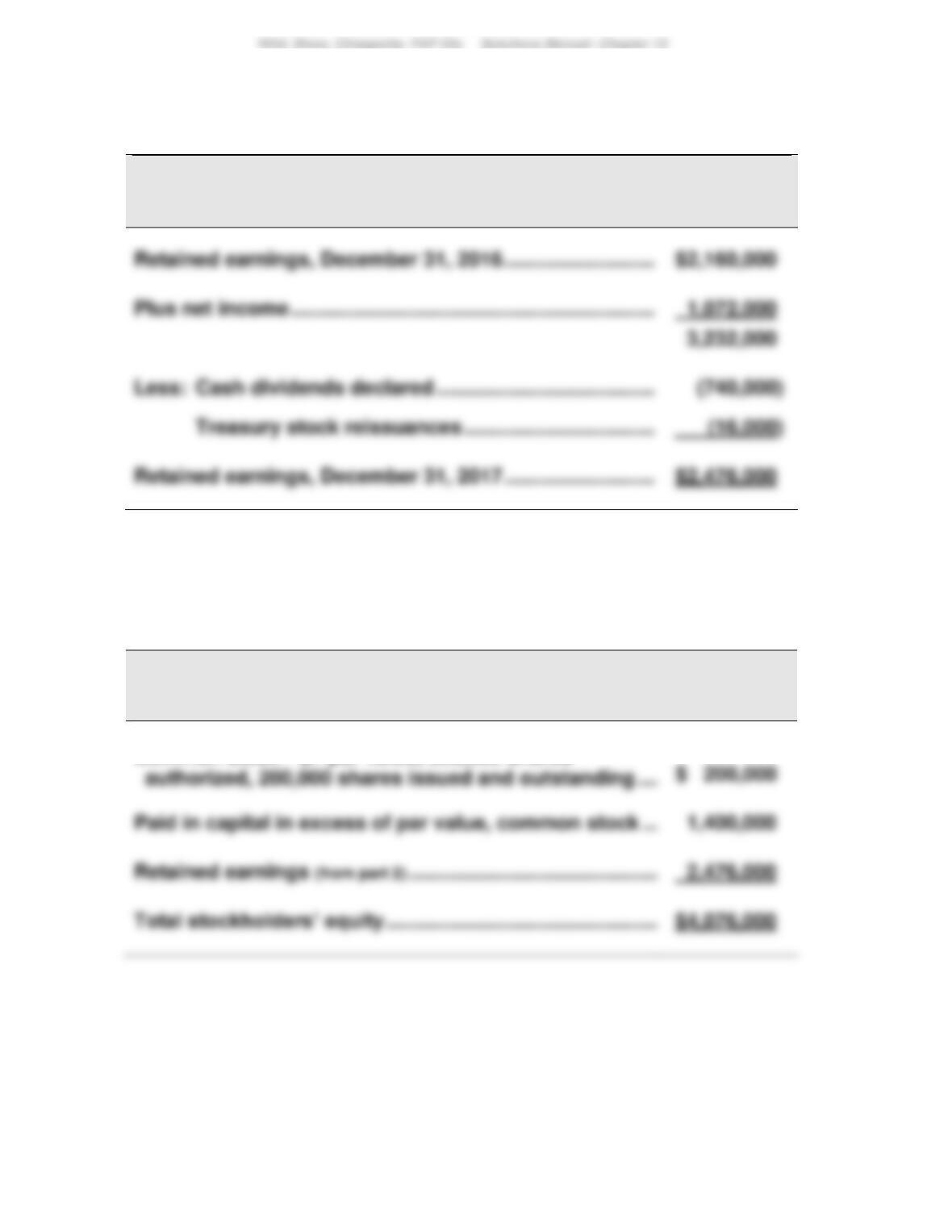

KOHLER CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2017

Retained earnings, December 31, 2016 ………………………

$270,000

Treasury stock reissuances ……………………………..

Part 3

KOHLER CORPORATION

Stockholders’ Equity Section of the Balance Sheet

December 31, 2017

Common stock⎯$10 par value, 100,000 shares

783

Problem 13-3A (45 minutes)

Part 1

Explanations for each of the journal entries

Oct. 2

Declared a cash dividend of $2 per share of common stock.

($60,000 / 30,000 shares)

Oct. 25

Executed a 3-for-1 stock split. ($12 par / $4 par = 3–for-1 ratio)

Part 2

Oct. 2

Oct. 25

Oct. 31

Nov. 5

Dec. 1

Dec. 31

Common stock ………….

$360,000

$360,000

$360,000

$396,000

$396,000

$396,000

Total equity ……………….

$710,000

$710,000

$710,000

$710,000

$710,000

$920,000

784

Problem 13-4A (45 minutes)

Part 1

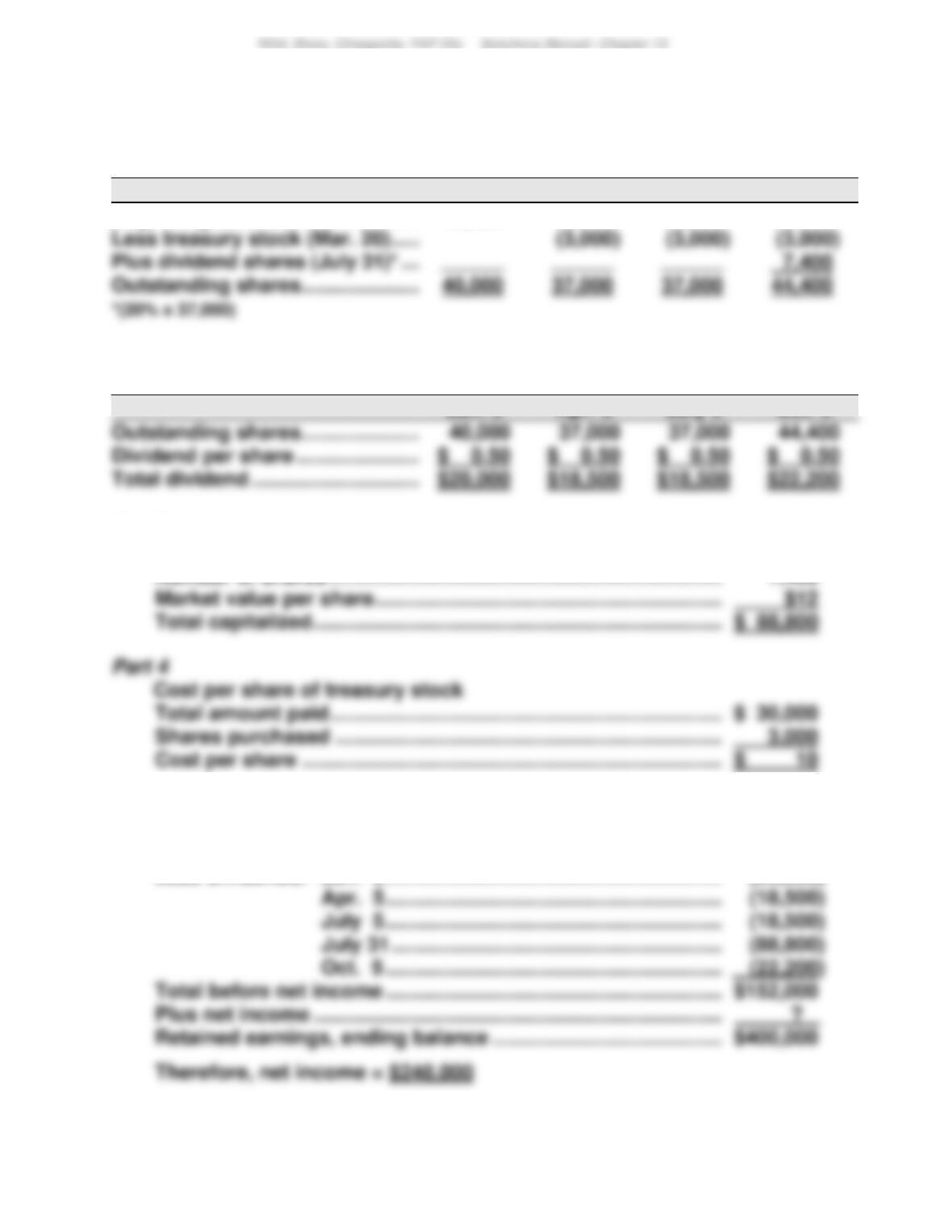

Outstanding common shares

Jan. 5

Apr. 5

July 5

Oct. 5

Beginning balance …………………….

40,000

40,000

40,000

40,000

Less treasury stock (Mar. 20) ……..

Part 2

Cash dividend amounts

Jan. 5

Apr. 5

July 5

Oct. 5

Dividend per share …………………..

Part 3

Capitalization of retained earnings for small stock dividend

Number of shares ………………………………………………………………

7,400

Market value per share ……………………………………………………….

Total amount paid ………………………………………………………………

$ 30,000

Shares purchased ……………………………………………………………..

Part 5

Net income

Retained earnings, beginning balance ………………………………..

$320,000

Less dividends: Jan. 5 ……………………………………………………..

(20,000)

(18,500)

(18,500)

Total before net income ……………………………………………………..

$152,000

?

Retained earnings, ending balance …………………………………….

$400,000

785

Problem 13-5A (40 minutes)

2. Computation of par values of stock

3. Book value with no dividends in arrears

Common stock

Total equity …………………………………………

Less equity for preferred ……………………..

Common stock equity ………………………….

Book value per common share …………….

4. Book value with two years’ dividends in arrears

Common stock

Total equity …………………………………………..

Common stock equity …………………………..

Book value per common share ………………

786

Problem 13-5A (Concluded)

5. Dividend allocation in total

Preferred

Common

Total

Remainder to common …………………

6. Equity represents the residual interest of owners in the assets of the

business after subtracting claims of creditors. With few exceptions,

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 13

PROBLEM SET B

Problem 13-1B (30 minutes)

Part 1

a. To record sale of 3,000 ($3,000/$1 per share) shares of $1 par value

Part 2

Number of outstanding shares

Part 3

Part 4

Total paid-in capital from common stockholders

From transaction (a) ……………………….

$120,000

From transaction (b) ……………………….

From transaction (c) ……………………….

From transaction (d) ……………………….

Part 5

Book value per common share

Mar. 2

Retained Earnings …………………………………………………

240,000

Common Dividend Payable …………………………..

240,000

Cash ………………………………………………………………..

240,000

Paid cash dividend.

312,000

Treasury Stock, Common** …………………………..

288,000

Paid-In Capital, Treasury Stock*** ……………………..

*(24,000 x $13) **(24,000 x $12) ***(24,000 x $1)

152,000

Retained Earnings …………………………………………………

Treasury Stock, Common** …………………………..

192,000

*(16,000 x $9.50) **(16,000 x $12)

Retained Earnings …………………………………………………

500,000

Common Dividend Payable …………………………..

500,000

Income Summary …………………………………………………..

Retained Earnings ……………………………………………

Closed Income Summary account.

Problem 13-2B (60 minutes)

Part 1

Jan. 10

Treasury Stock, Common ………………………………………

480,000

Cash ………………………………………………………………..

480,000

Purchased treasury stock (40,000 x $12).

789

Problem 13-2B (Concluded)

Part 2

BALTHUS CORP.

Statement of Retained Earnings

For Year Ended December 31, 2017

Part 3

BALTHUS CORP.

Stockholders’ Equity Section of the Balance Sheet

December 31, 2017

Common stock⎯$1 par value, 320,000 shares

790

Problem 13-3B (45 minutes)

Part 1

Explanations for each of the journal entries

Jan. 17

Declared a cash dividend of $1 per share of common stock.

($96,000 / 96,000 shares)

Mar. 14

Mar. 25

Mar. 31

Part 2

Jan. 17

Feb. 5

Feb. 28

Mar. 14

Mar. 25

Mar. 31