CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-24

$(6,837) – $14

517 shares

= $(13.25)

b. Year 3 Year 2 Year 1

Earnings per share…………………………………

…

$(13.25) $3.21 $2.79

Growth as a percent of Year 1 (base year)……

…

(575)% 15% 100%

Net income (loss)……………………………………

…

$(6,837) $1,660 $1,407

Growth as a percent of Year 1 (base year)……

…

(586)% 18% 100%

Earnings per share and net income varied significantly over the three-year period.

The variability of earnings per share and net income is partially explained by the

unpredictable nature of Pacific Gas and Electric’s regulatory environment. For

example, Pacific Gas and Electric is regulated by the California Public Utilities

Commission (CPUC). The CPUC has jurisdiction over the rates, terms, and

conditions of service for the company’s electricity and natural gas distribution

operations, electricity generation, and natural gas transmission and storage

a. Net Income – Preferred Dividends

=

Avg. Number of Common Shares Outstanding

Year 3 Earnings per Share

=Earnings per Share

*

*

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-25

a. Caterpillar Inc.

Deere & Company

$2,368

323 shares

= $7.33

b. Deere’s earnings per share for Year 1 is higher than Caterpillar’s. However, from

Year 1 to Year 2, the earnings per share for both companies increased. Caterpillar’

s

earnings per share increased by 719% [$10.40 − $1.27) ÷ $1.27], while Deere’s

earnings per share increased by 9% [$7.33 − $6.75) ÷ $6.75]. Overall, Caterpillar

appears to be the more profitable company.

Earnings per Share = Net Income

Avg. Number of Common Shares Outstanding

Avg. Number of Common Shares Outstanding

Net Income

=Earnings per Share

=Year 2: Earnings per Share

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-1A

1.

Total Per Per

Dividends Total Share Total Share

Year 1……… $ 80,000 $ 80,000 $0.32 $ 0 $0.00

Year 2……… 90,000 90,000 0.36 0 0.00

Year 3……… 150,000 130,000 0.52 20,000 0.04

Year 4……… 150,000 100,000 0.40 50,000 0.10

2. Average annual dividend for preferred: $0.40 per share ($2.40 ÷ 6)

Average annual dividend for common: $0.07 per share ($0.42 ÷ 6)

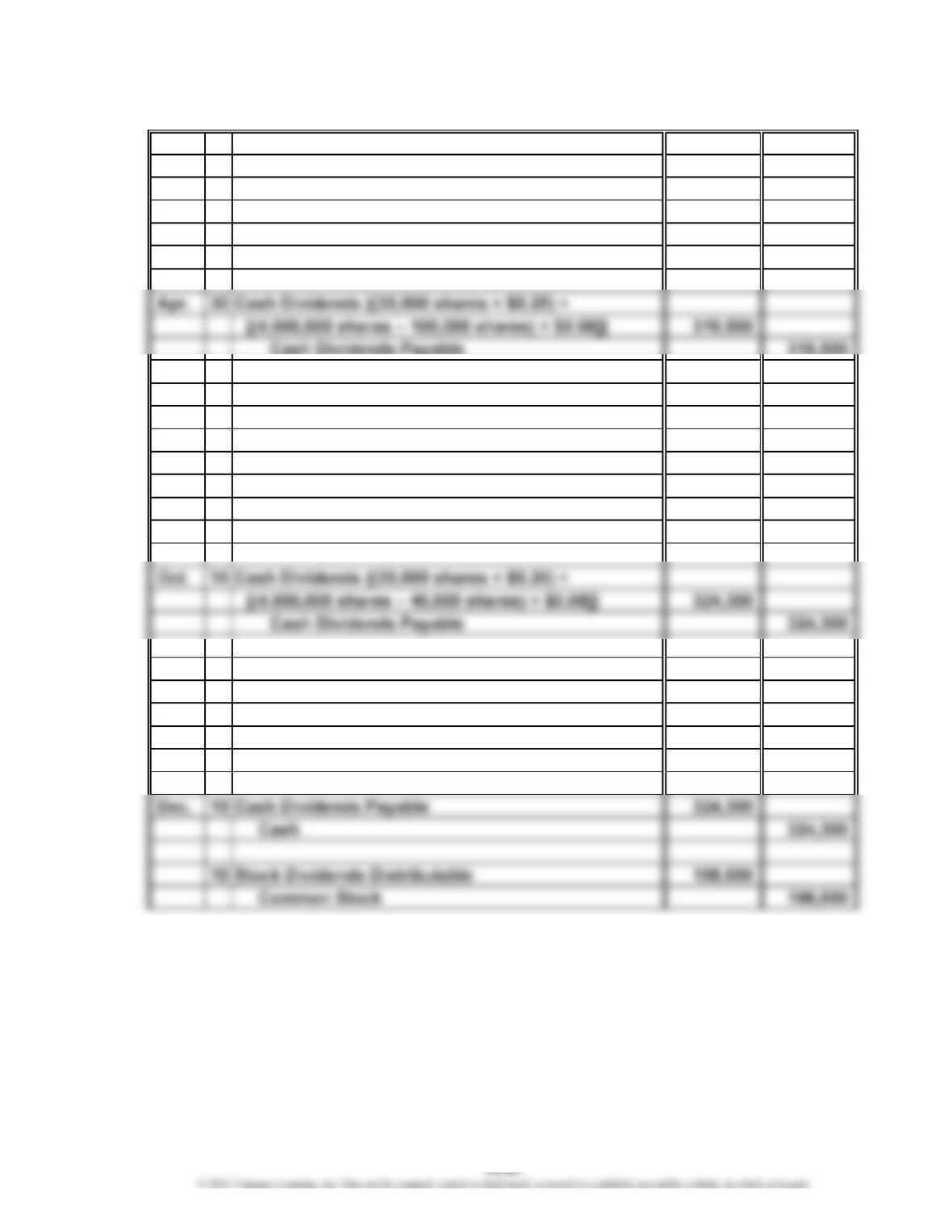

Prob. 13-2A

11 Building 3,375,000

Land 1,500,000

Common Stock (125,000 shares × $35) 4,375,000

Paid-In Capital in Excess of Par—

Common Stock [125,000 shares ×

($39 – $35)] 500,000

31 Cash 4,000,000

Mortgage Note Payable 4,000,000

PROBLEMS

Year

Preferred Dividends Common Dividends

May

*

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-3A

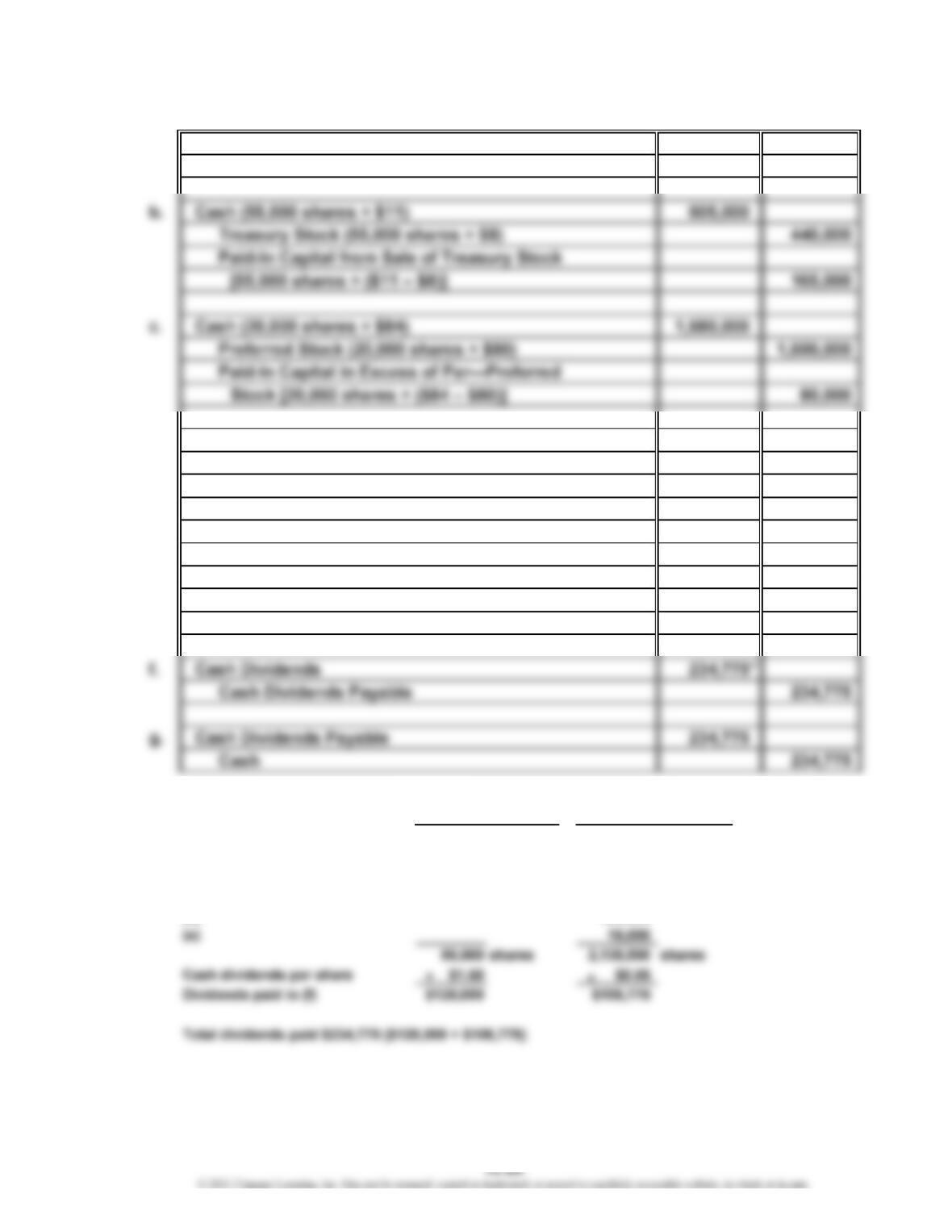

a. Cash (220,000 × $15)

Common Stock (220,000 × $12) 2,640,000

Paid-In Capital in Excess of Par—Common

Stock [220,000 × ($15 – $12)] 660,000

c. Treasury Stock (130,000 × $19)

Cash 2,470,000

e. Cash (40,000 × $17)

Paid-In Capital from Sale of Treasury Stock

[40,000 × ($19 – $17)]

Treasury Stock (40,000 × $19) 760,000

* Calculation of cash dividends:

Beginning of year 65,000 shares 1,400,000 shares

(a) 220,000

(b) 6,000

(c) (130,000)

(d) 70,000

(e) 40,000

71,000 shares 1,600,000 shares

3,300,000

2,470,000

680,000

80,000

Outstanding Shares of Stock

Preferred Stock Common Stock

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-4A

1. and 2.

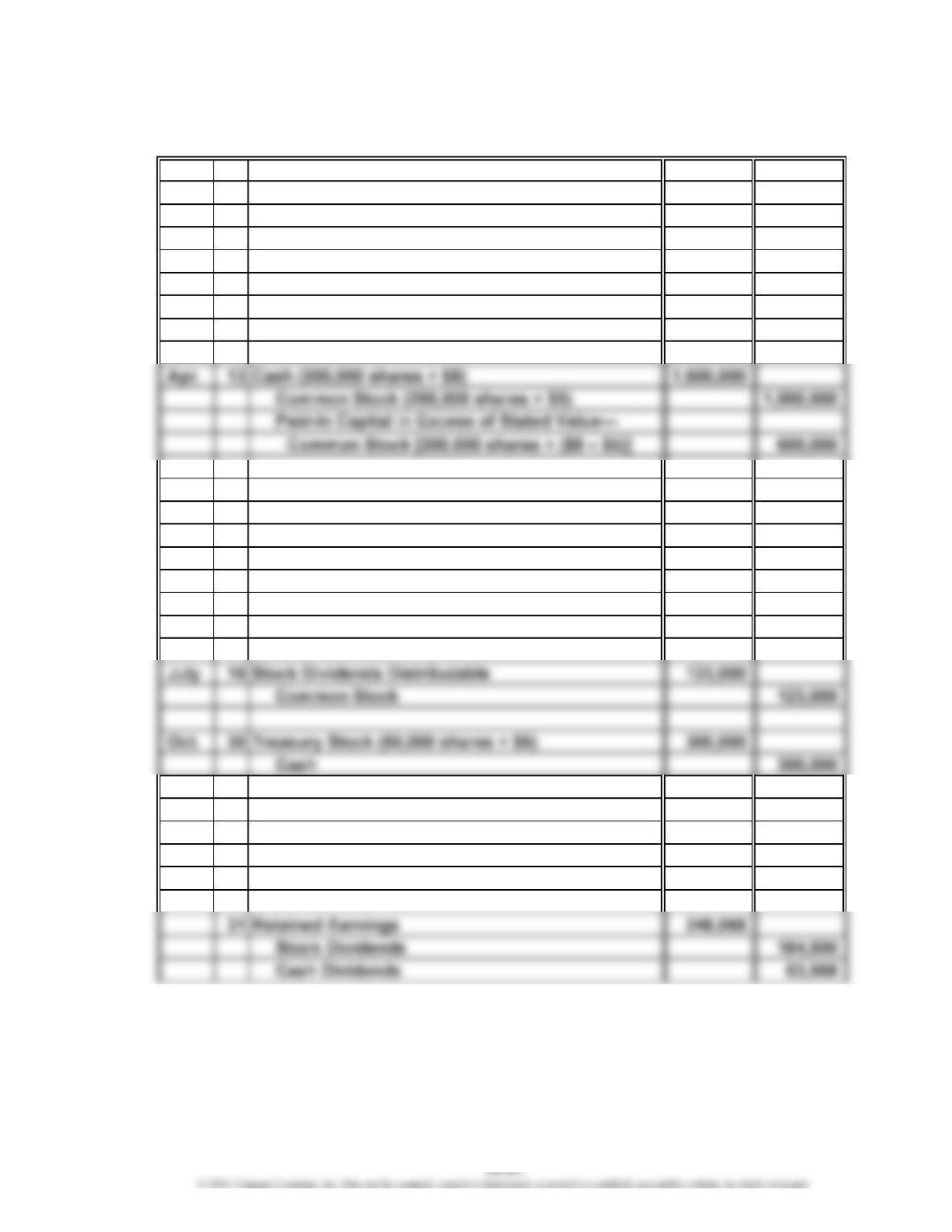

Jan. 1 Bal. 7,500,000

Apr. 10 1,500,000

Aug. 15 360,000

Dec. 31 Bal. 9,360,000

Dec. 31 493,800 Jan. 1 Bal. 33,600,000

Dec. 31 1,125,000

Dec. 31 Bal. 34,231,200

June 6 200,000

Dec. 28 43,800 Dec. 31 43,800

Common Stock

Retained Earnings

Cash Dividends

Paid-In Capital from Sale of Treasury Stock

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-4A (Continued)

2.

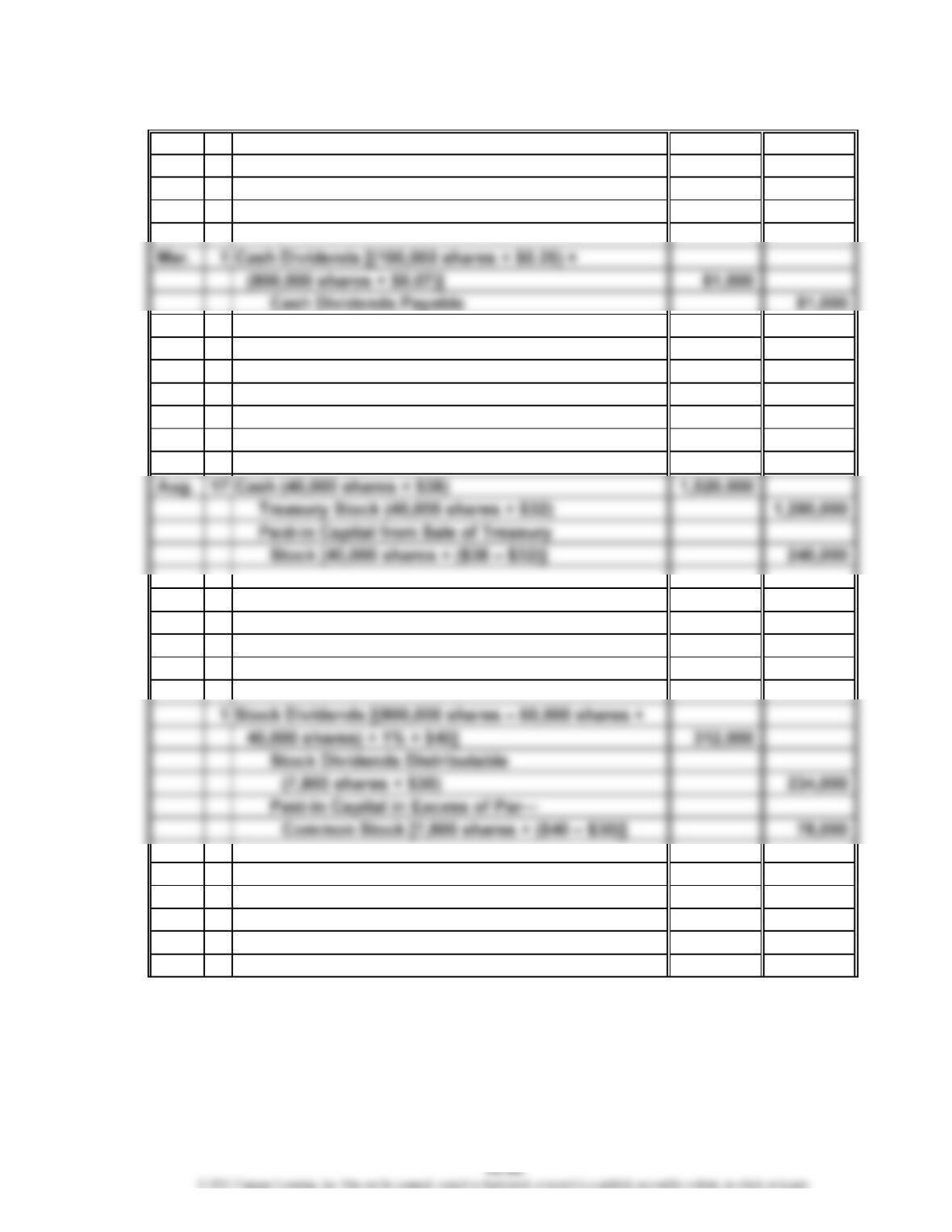

Jan. 22 Cash Dividends Payable [(375,000 shares –

25,000 shares) × $0.08] 28,000

Cash 28,000

June 6 Cash (25,000 shares × $26) 650,000

Treasury Stock (25,000 shares × $18) 450,000

Paid-In Capital from Sale of Treasury Stock

[25,000 shares × ($26 – $18)] 200,000

Aug. 15 Stock Dividends Distributable 360,000

Common Stock 360,000

Nov. 23 Treasury Stock (30,000 shares × $19) 570,000

Cash 570,000

Dec. 28 Cash Dividends [(375,000 shares + 75,000 shares +

18,000 shares – 30,000 shares) × $0.10] 43,800

Cash Dividends Payable 43,800

Cash Dividends 43,800

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-4A (Concluded)

3.

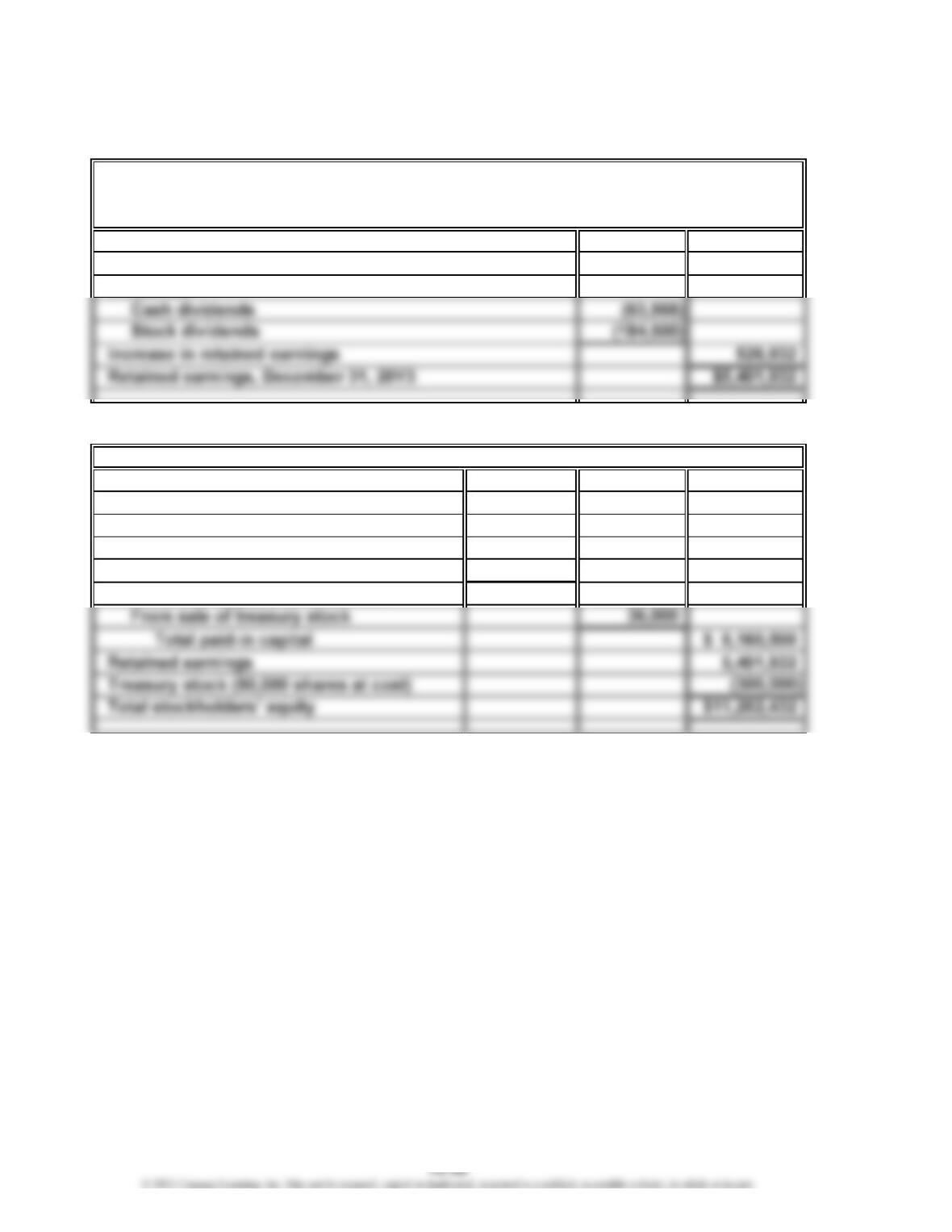

Retained earnings, January 1, 20Y5 $33,600,000

Net income $1,125,000

Dividends:

4.

Paid-in capital:

Common stock, $20 stated value

(500,000 shares authorized,

468,000 shares issued) $9,360,000

Excess over stated value 1,215,000

Paid-in capital, common stock $10,575,000

From sale of treasury stoc

k

200,000

Stockholders’ Equity

Morrow Enterprises Inc.

Retained Earnings Statement

For the Year Ended December 31, 20Y5

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-5A

Jan. 5 No entry required. The stockholders’ ledger would

be revised to record the increased number of shares

held by each stockholder and the new par value.

Mar. 10 Treasury Stock (100,000 shares × $30) 3,000,000

Cash 3,000,000

Cash Dividends Payable 319,500

June 15 Cash Dividends Payable 319,500

Cash 319,500

Aug. 20 Cash (60,000 shares × $40) 2,400,000

Treasury Stock (60,000 shares × $30) 1,800,000

Paid-In Capital from Sale of Treasury

Stock [60,000 shares × ($40 – $30)] 600,000

15 Stock Dividends (39,600 shares × $35) 1,386,000

Stock Dividends Distributable

(39,600 shares × $5) 198,000

Paid-In Capital in Excess of Par—

Common Stock (39,600 shares × $30) 1,188,000

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

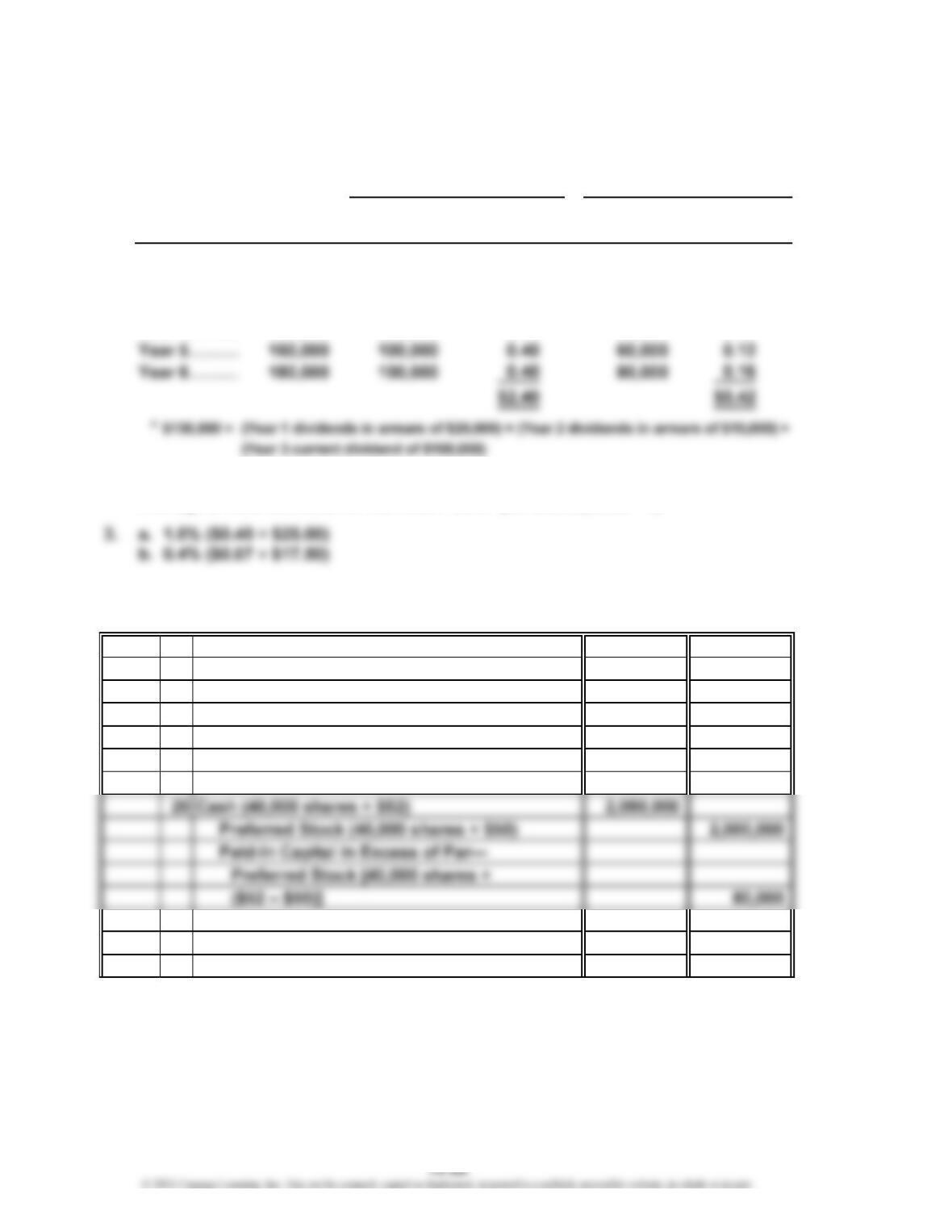

Prob. 13-1B

1.

Total Per Per

Dividends Total Share Total Share

Year 1………

…

$ 42,500 $ 42,500 $0.85 $0 $0.00

Year 2………

…

18,000 18,000 0.36 0 0.00

Year 3………

…

223,500 179,500 3.59 44,000 0.44

$9.60 $4.26

*

$179,500 = Year 1 dividends in arrears of $37,500 + Year 2 dividends in arrears of $62,000 +

Year 3 current dividend of $80,000

2. Average annual dividend for preferred: $1.60 per share ($9.60 ÷ 6)

Average annual dividend for common: $0.71 per share ($4.26 ÷ 6)

Prob. 13-2B

9 Cash 1,500,000

Mortgage Note Payable 1,500,000

17 Cash (20,000 shares × $126) 2,520,000

Preferred Stock (20,000 shares × $120) 2,400,000

Paid-In Capital in Excess of Par—

Preferred Stock [20,000 shares ×

($126 – $120)] 120,000

Year

Preferred Dividends Common Dividends

Oct.

*

…

…

…

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

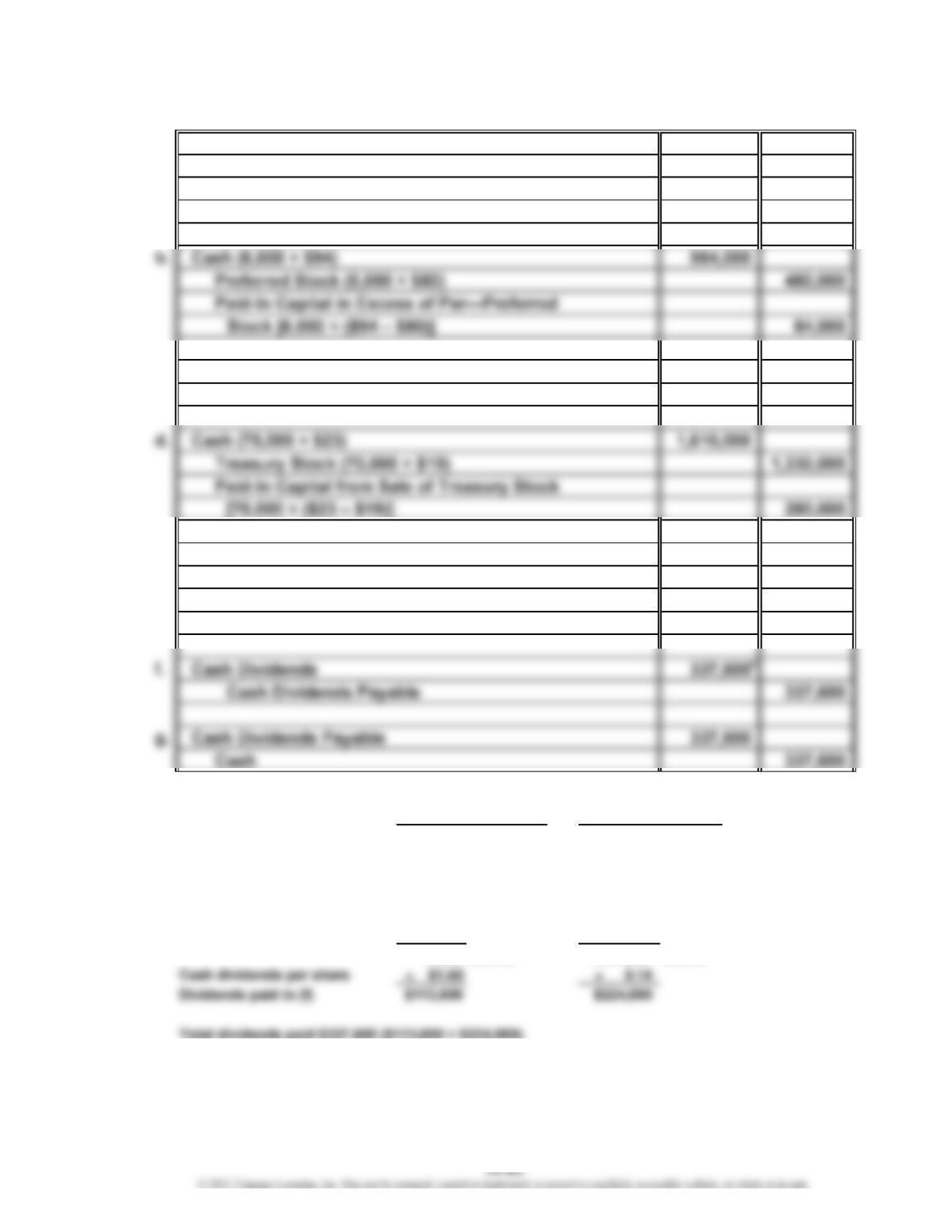

Prob. 13-3B

a. Treasury Stock (87,500 shares × $8)

Cash 700,000

d. Cash (400,000 shares × $13)

Common Stock (400,000 shares × $9) 3,600,000

Paid-In Capital in Excess of Par—Common

Stock [400,000 shares × ($13 – $9)] 1,600,000

e. Cash (18,000 shares × $7.50)

Paid-In Capital from Sale of Treasury Stock

[18,000 shares × ($8.00 – $7.50)]

Treasury Stock (18,000 shares × $8) 144,000

* Calculation of cash dividends:

Beginning of year 60,000 shares 1,750,000 shares

(a) (87,500)

(b) 55,000

(c) 20,000

5,200,000

Preferred Stock Common Stock

Outstanding Shares of Stock

9,000

135,000

700,000

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

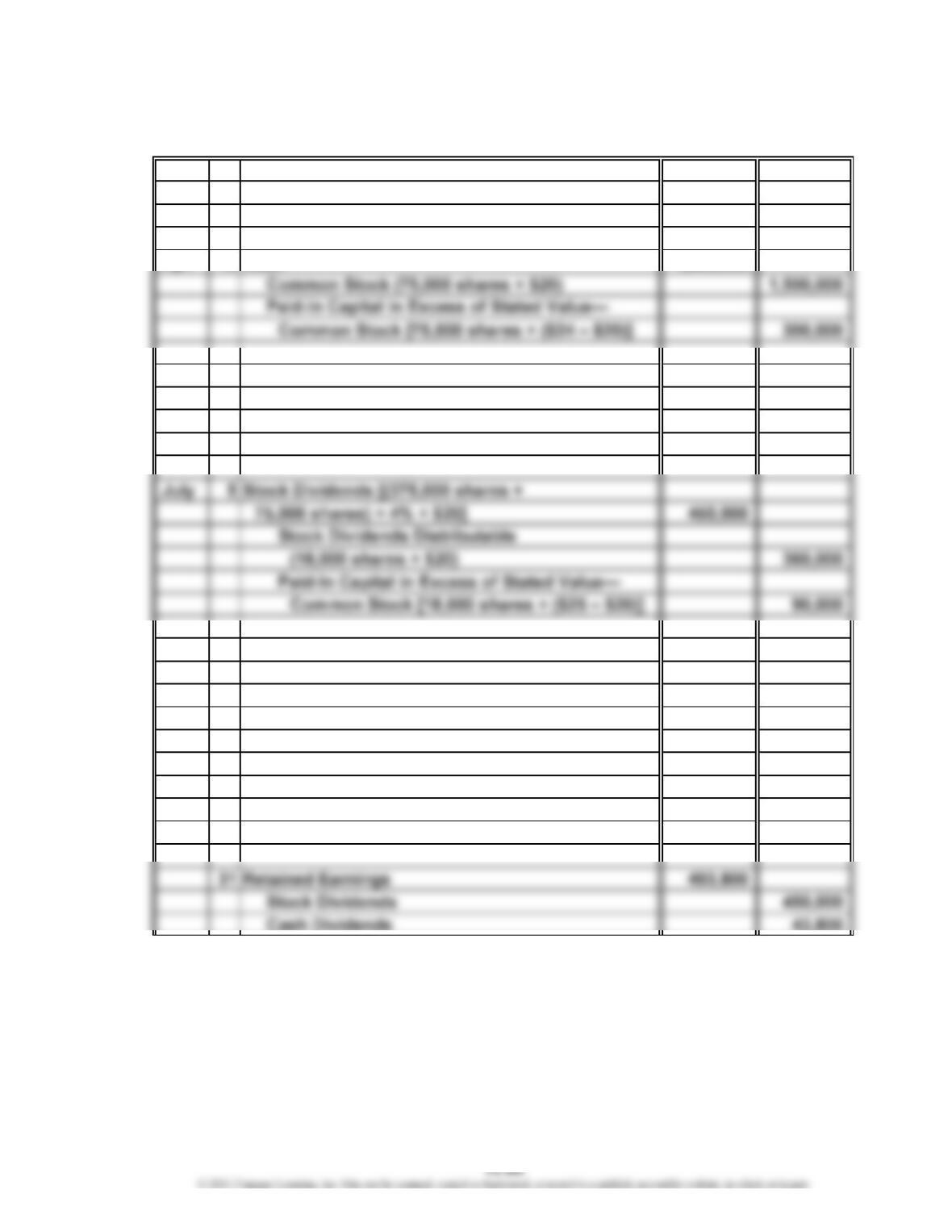

Prob. 13-4B

1. and 2.

Jan. 1 Bal. 3,100,000

Apr. 13 1,000,000

July 16 123,000

Dec. 31 Bal. 4,223,000

Dec. 31 248,068 Jan. 1 Bal. 4,875,000

Dec. 31 775,000

Dec. 31 Bal. 5,401,932

Mar. 15 36,000

July 16 123,000 June 14 123,000

Common Stock

Retained Earnings

Paid-In Capital from Sale of Treasury Stock

Stock Dividends Distributable

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-4B (Continued)

2.

Jan. 15 Cash Dividends Payable

[(620,000 shares – 48,000 shares) × $0.06] 34,320

Cash 34,320

Mar. 15 Cash (48,000 shares × $6.75) 324,000

Treasury Stock (48,000 shares × $6.00) 288,000

Paid-In Capital from Sale of Treasury Stock

[48,000 shares × ($6.75 – $6.00)] 36,000

June 14 Stock Dividends

[(620,000 shares + 200,000 shares) × 3% × $7.50] 184,500

Stock Dividends Distributable

(24,600 shares × $5) 123,000

Paid-In Capital in Excess of Stated Value—

Common Stock [24,600 shares ×

($7.50 – $5.00)] 61,500

Dec. 30 Cash Dividends [(620,000 shares +

200,000 shares + 24,600 shares –

50,000 shares) × $0.08] 63,568

Cash Dividends Payable 63,568

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

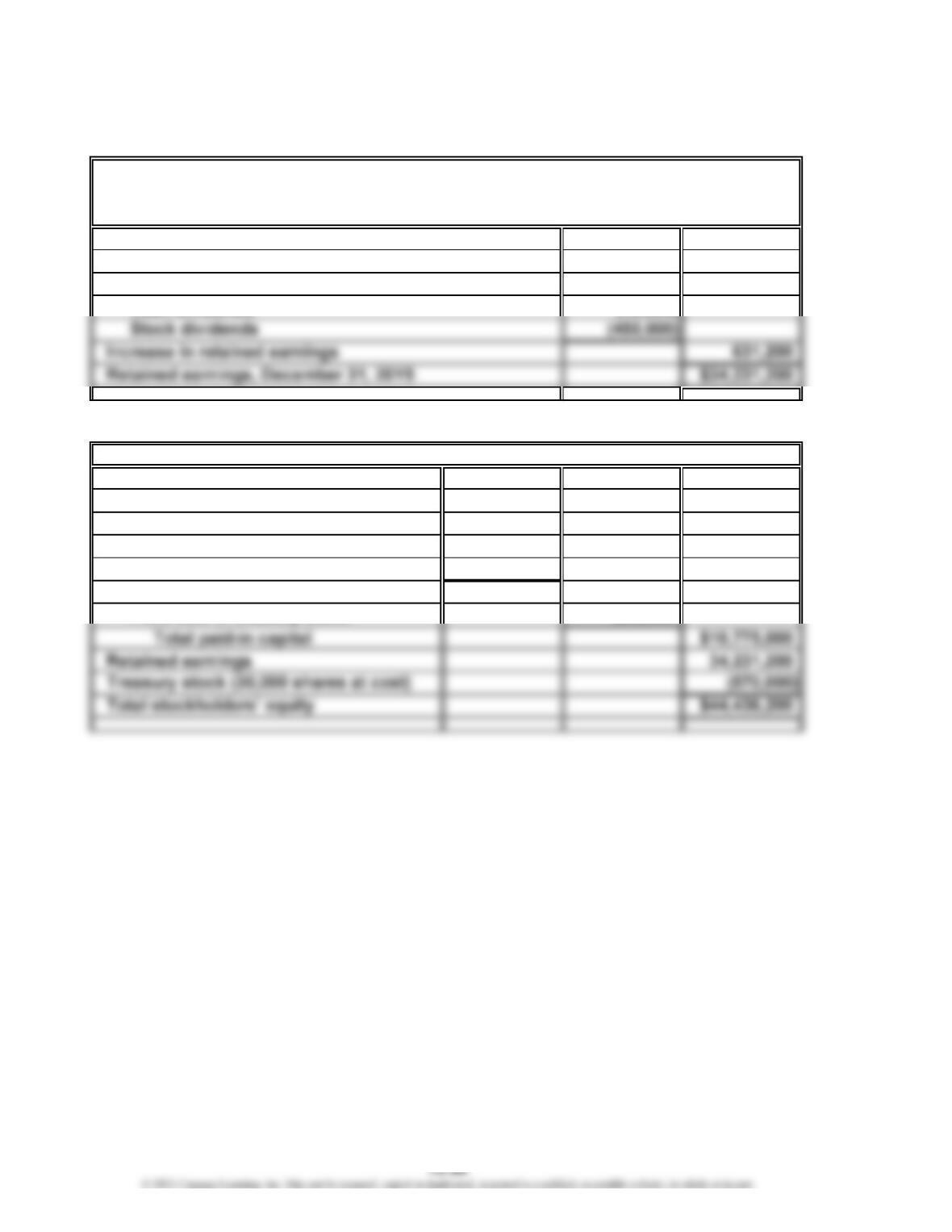

Prob. 13-4B (Concluded)

3.

Retained earnings, January 1, 20Y3 $4,875,000

Net income $ 775,000

Dividends:

4.

Paid-in capital:

Common stock, $5 stated value

(900,000 shares authorized, 844,600

shares issued) $4,223,000

Excess over stated value 1,901,500

Paid-in capital, common stock $6,124,500

Stockholders’ Equity

Nav-Go Enterprises Inc.

Retained Earnings Statement

For the Year Ended December 31, 20Y3

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Prob. 13-5B

Jan. 15 No entry required. The stockholders’ ledger would

be revised to record the increased number of

shares held by each stockholder and the new par

value.

Apr. 30 Cash Dividends Payable 81,000

Cash 81,000

May 31 Treasury Stock (60,000 shares × $32) 1,920,000

Cash 1,920,000

Sept. 1 Cash Dividends {(100,000 shares × $0.25) +

[(800,000 shares – 60,000 shares +

40,000 shares) × $0.09]} 95,200

Cash Dividends Payable 95,200

Oct. 31 Cash Dividends Payable 95,200

Cash 95,200

31 Stock Dividends Distributable 234,000

Common Stock 234,000

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

CP 13-1

Tommy is clearly acting unethically for several reasons. First, he is violating the

company’s policy on stock purchases. This policy was established to ensure the fair

and timely dissemination of information that gives all potential investors the same

chance to participate in the stock price increases. The fact that he is purchasing the

stock in partnership with his father does not get around the company policy. Second,

CP 13-2

Lou and Shirley are behaving in a professional manner as long as full and

complete information is provided to potential investors in accordance with

CP 13-3

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31, 2018

,

follows:

1. Nike, Inc.

2. Oregon

3. Our principal business activity is the design, development, and worldwide

marketing and selling of athletic footwear, apparel, equipment, accessories,

and services.

4. $22,536 million

5. $12,724 million

6. $9,812 million ($22,536 million total assets – $12,724 million total liabilities)

CASES & PROJECTS

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

CP 13-4

Memo

To: Matt Cengage

From: A+ Student

Re: Fourth Quarter 20Y8 Cash Dividend

In order to declare a dividend prudently for the fourth quarter, the company must

have a sufficient Retained Earnings balance from which to declare the dividend.

On December 31, 20Y8, Motion Designs has a $4,630,000 balance in Retained

Earnings. This balance is more than enough to cover the $90,000 declaration of

the normal quarterly cash dividend of $0.50 per share. In addition, the company

must have enough cash on hand to pay the dividend while meeting the remaining

cash needs of the business. The company has a December 31, 20Y8, cash balance

of $250,000, of which $100,000 is committed as the compensating balance under

the loan agreement. This leaves only $150,000 to pay the dividend of $90,000 and

finance normal operations. Unless the cash balance can be expected to increase

significantly in early 20Y9, it is questionable whether the company’s cash balance

is large enough to both pay the cash dividend and provide for the company’s

near-term operating needs.

CP 13-5

At the time of this decision, the WorldCom board had come under intense scrutiny.

This was the largest loan by a company to its CEO in history. The SEC began an

investigation into this loan, and Bernie Ebbers was eventually terminated as the

CEO, with this loan being cited as part of the reason. The board indicated that

the decision to lend Ebbers this money was to keep him from selling his stock

Some press comments:

1. When he borrowed money personally, he used his WorldCom stock as

collateral. As these loans came due, he was unwilling to sell at “depressed

2. It was astonishing to read the other day that the board of directors of the

United States’ second-largest telecommunications company claims to have

had its shareholders’ interests in mind when it agreed to grant more than $430

million in low-interest loans to the company’s CEO, mainly to meet margin

calls on his stock.

Yet that’s the level to which fiduciary responsibility seems to have sunk on

the board of Clinton, Mississippi-based WorldCom, the deeply troubled

telecom giant, as it sought to bail Bernard Ebbers out of the folly of

speculating in shares of WorldCom itself. Sadly, WorldCom is hardly alone.

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

CP 13-5 (Concluded)

best one by far—at least from the point of view of the shareholders—was to

CP 13-6

1. This case involves a transaction in which a security has been issued that has

characteristics of both stock and debt. The primary argument for classifying

the issuance of the common stock as debt is that the investors have a legal

right to an amount equal to the purchase price (face value) of the security.

This is similar to a note payable or a bond payable. The additional $120

payment could be argued to be equivalent to an interest payment, whose

payment has been deferred until a later date.

2. In practice, the $25 million stock issuance would probably be classified as

common stock. However, full disclosure should be made of the 5% of sales

and $120 per share payment obligations in the notes to the financial statements.

In addition, as Epstein Engineering Inc. generates sales, a current liability should

be recorded for the payment to stockholders. Such payments would be classified

as dividend payments rather than interest payments. Dan Fisher should also