CHAPTER 13

Financial Analysis: The Big Picture

Learning Objectives

1. Understand the concept of sustainable income.

2. Indicate how irregular items are presented.

3. Explain the concept of comprehensive income.

4. Describe and apply horizontal analysis.

5. Describe and apply vertical analysis.

6. Identify and compute ratios used in analyzing a company’s liquidity, solvency, and profitability.

7. Understand the concept of quality of earnings.

Summary of Questions by Learning Objectives and Bloom’s Taxonomy

Item LO BT Item LO BT Item LO BT Item LO BT Item LO BT

Questions

1. 1 C 6. 6 C 11. 6 C 16. 6 C 20. 6 C

Brief Exercises

1. 2 AP 4. 4 AP 7. 4 AP 10. 6 AP 13. 6 AN

Do It! Review Exercises

Exercises

1. 2 AP 3. 4 AP 6. 4, 5 AP 9. 6 AP 12. 6 AP

Problems: Set A

Problems: Set B

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A Prepare vertical analysis and comment on profitability. Simple 20–30

2A Compute ratios from balance sheet and income

statements.

Simple 20–30

5A Compute selected ratios, and compare liquidity,

profitability, and solvency for two companies.

Moderate 50–60

1B Prepare vertical analysis and comment on profitability. Simple 20–30

2B Compute ratios from balance sheet and income

statements.

Simple 20–30

3B Perform ratio analysis, and discuss change in

financial position and operating results.

Simple 20–30

ANSWERS TO QUESTIONS

1. Sustainable income is defined as the most likely level of income to be obtained in the future. It is

the amount of regular income that a company can expect to earn from its normal operations.

In order to distinguish a company’s net income from its sustainable income, irregular items, such

as an extraordinary gain or discontinued operations, are reported separately on the income

statement.

4. Companies report a change from FIFO to average cost pricing for inventory retroactively. That is,

they report both the current period and any previous periods reported on the face of the state-

ment using the new principle. As a result, the same principle applies in all periods. This treatment

improves the ability to compare results across years.

7. (a) Comparison of financial information can be made on an intracompany basis, an inter-

company basis, and an industry average basis.

1. An intracompany basis compares the same item with prior periods, or with other

(b) The intracompany basis of comparison is useful in detecting changes in financial relation-

ships and significant trends within a company.

8. Horizontal analysis (also called trend analysis) measures the dollar and percentage increase or

decrease of an item over a period of time. In this approach, the amount of the item on one state–

Questions Chapter 13 (Continued)

9. (a) $300,000 X 1.245 = $373,500, 2014 net income.

10. (a) Liquidity ratios: Working capital, current ratio, current cash debt coverage, inventory turnover,

11. Andrea is correct. A single ratio by itself may not be very meaningful and is best interpreted by

12. (a) Liquidity ratios measure the short-term ability of the company to pay its maturing obligations

and to meet unexpected needs for cash.

13. Working capital and the current ratio both relate current assets to current liabilities. Working

capital produces a dollar amount that indicates the difference between current assets and current

14. Quick Mart does not necessarily have a problem. The accounts receivable turnover can be

15. (a) Asset turnover.

16. The price earnings (P-E) ratio is a reflection of investors’ assessments of a company’s future

earnings. The P-E ratio takes into account such factors as relative risk, stability of earnings,

17. The payout ratio is cash dividends declared on common stock divided by net income. In a growth

company, the payout ratio is often low because the company is reinvesting earnings in the business.

Questions Chapter 13 (Continued)

19.

Return on assets

(7.6%)

= Net Income

Average Total Assets

20. (a) Times interest earned, which is an indication of the company’s ability to meet interest charges,

and the debt to total assets ratio, which indicates the company’s ability to withstand losses

without impairing the interests of creditors.

21. Net income – Preferred dividends

Average common shares outstanding = Earnings per share.

Questions Chapter 13 (Continued)

22. (1) Use of alternative accounting methods. Variations among companies in the application of

generally accepted accounting principles may hamper comparability.

23. (a) During a period of inflation, net income will be less under the LIFO inventory costing method

than it will be using the FIFO method because LIFO results in the larger cost of goods sold

amount.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 13-1

REYES CORPORATION

Partial Income Statement

Discontinued operations: Loss on disposal of

BRIEF EXERCISE 13-2

FIELDER CORPORATION

Partial Income Statement

Income before income taxes ………………………………………………. $300,000

Income tax expense ($300,000 X 30%) ………………………………… 90,000

BRIEF EXERCISE 13-3

The change in inventory pricing for Jenner should be reported retroactively.

That is, it should report both the current period and previous periods

BRIEF EXERCISE 13-4

Horizontal analysis:

Increase

or (Decrease)

Dec. 31, 2014 Dec. 31, 2013

A

mount Percentage*

Accounts receivable

$ 460,000

$ 400,000

$ 60,000

15%

BRIEF EXERCISE 13-5

Vertical analysis:

Dec. 31, 2014 Dec. 31, 2013

Amount Percentage*

A

mount Percentage**

Accounts receivable

$ 460,000

14.5%

$ 400,000

14.3%

BRIEF EXERCISE 13-6

2014 2013 2012

Net income $518,400 $485,000 $500,000

Increase or (Decrease)

Amount Percentage*

(a)

2012

–

2013

($15,000)

(3%)

BRIEF EXERCISE 13-7

2014 2013 Increase

Net income $382,800

X

16%

BRIEF EXERCISE 13-8

2014 2013 2012

Sales revenue

100.0

100.0

100.0

BRIEF EXERCISE 13-9

Comparing the percentages presented results in the following conclusions:

The net income for Roswell increased in 2013 because of the combination

BRIEF EXERCISE 13-10

Current ratio:

2014 2013

BRIEF EXERCISE 13-11

Accounts receivable turnover = Net credit sales

Average net accounts receivable

2014 2013

BRIEF EXERCISE 13-12

(a) Inventory turnover = Cost of goods sold

Average inventory

2014 2013

2

⎝

⎜⎞

⎠

⎟

2014 2013

Beginning inventory

$ 960,000

$ 840,000

(b) Days in inventory

BRIEF EXERCISE 13-13

(a) Asset turnover = Net sales

Average total assets

BRIEF EXERCISE 13-13 (Continued)

(b) Profit margin =

Net income

Net sales

BRIEF EXERCISE 13-14

Payout ratio =

Cash dividends declared on common stock

Net income

Return on assets = Net income

Average total assets

.20 =

$72, 000

X

BRIEF EXERCISE 13-15

(a) Current cash debt

coverage =Net cash provided by operating activities

Average current liabilities

(b) Cash debt

coverage =Net cash provided by operating activities

Average total liabilities

(c) Free Cash Flow = Cash provided by operating activities –

Capital expenditures – Cash dividends

SOLUTIONS TO DO IT! REVIEW EXERCISES

DO IT! 13-1

SUNFLOWER CORPORATION

Income Statement (partial)

Income before income taxes ……………………………………. $500,000

Income tax expense ………………………………………………… 200,000

Income before irregular items …………………………………. 300,000

DO IT! 13-2

Increase in 2014

Amount Percent

Current assets $ (20,000) (9.1)% [($ 200,000 – $ 220,000) ÷ $ 220,000]

DO IT! 13-3

(a) Profitability ratio

DO IT! 13-4

1. Current ratio: A measure used to evaluate a company’s liquidity.

SOLUTIONS TO EXERCISES

EXERCISE 13-1

UTECH COMPANY

Partial Income Statement

For the Year Ended December 31, 2014

Income before irregular items …………………………………………….. $310,000

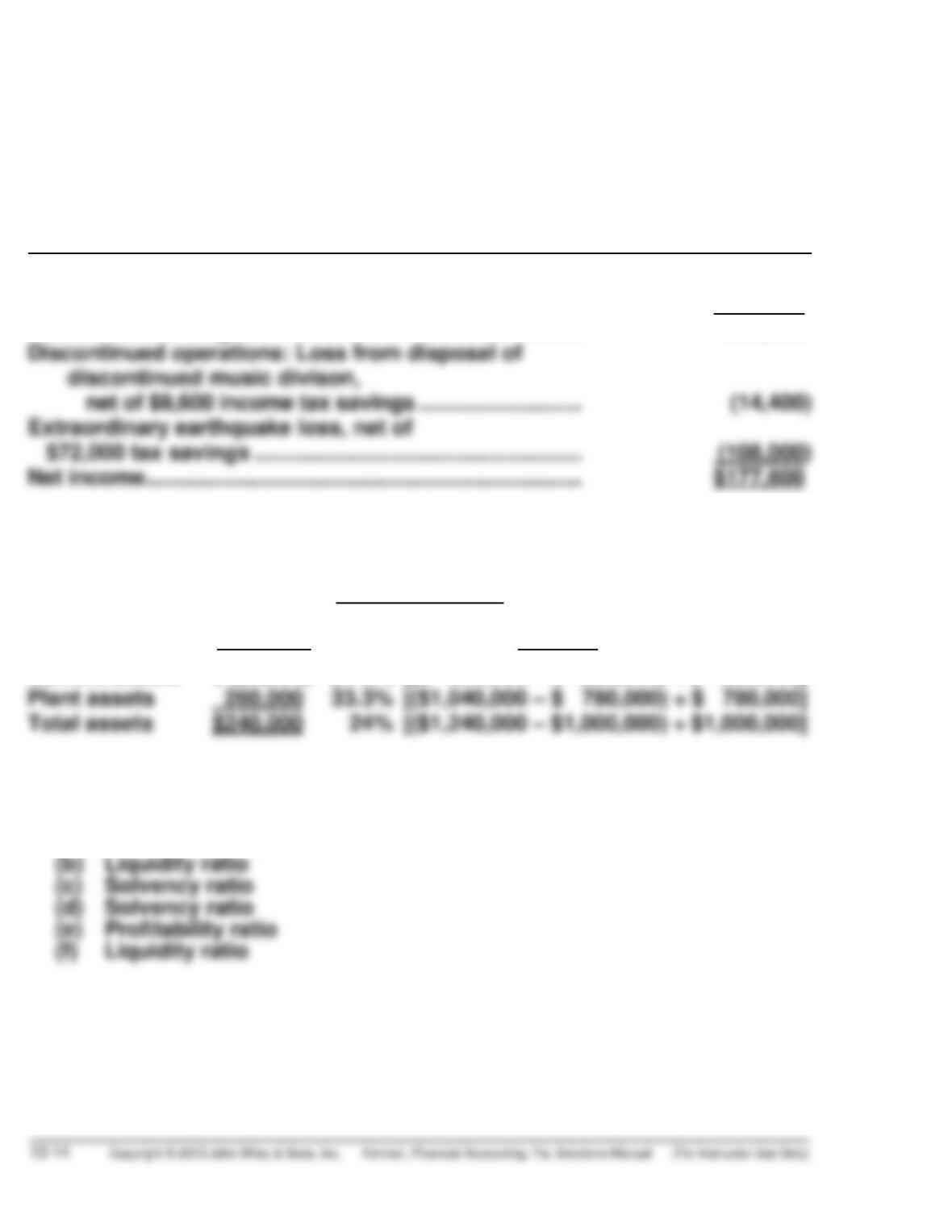

Discontinued operations: Gain from disposal

EXERCISE 13-2

(a) The loss on the sale of electrical equipment was reported as a part of

continuing operations. The loss was reported in the fourth quarter of

(b) The extraordinary items are listed separately so that the reader can

evaluate the company’s results on the basis of normal operations and

(c) The extraordinary gain is the expropriation (takeover) of company

property in the Middle East. It was not included in income for the fourth

EXERCISE 13-2 (Continued)

(d) The company had net income of over $68 million during the fourth

quarter of 2013 but the year-to-date total shows net income of only $33.25

million. Therefore, Energy Enterprises had an operating loss at the end

(e) Energy Enterprises had 75,514,706 shares of stock outstanding (Net

(f) The profit margin should be based on the company’s net income from

its normal and continuing operations. The net income figure should be

a more conservative amount and should not include any irregular items.

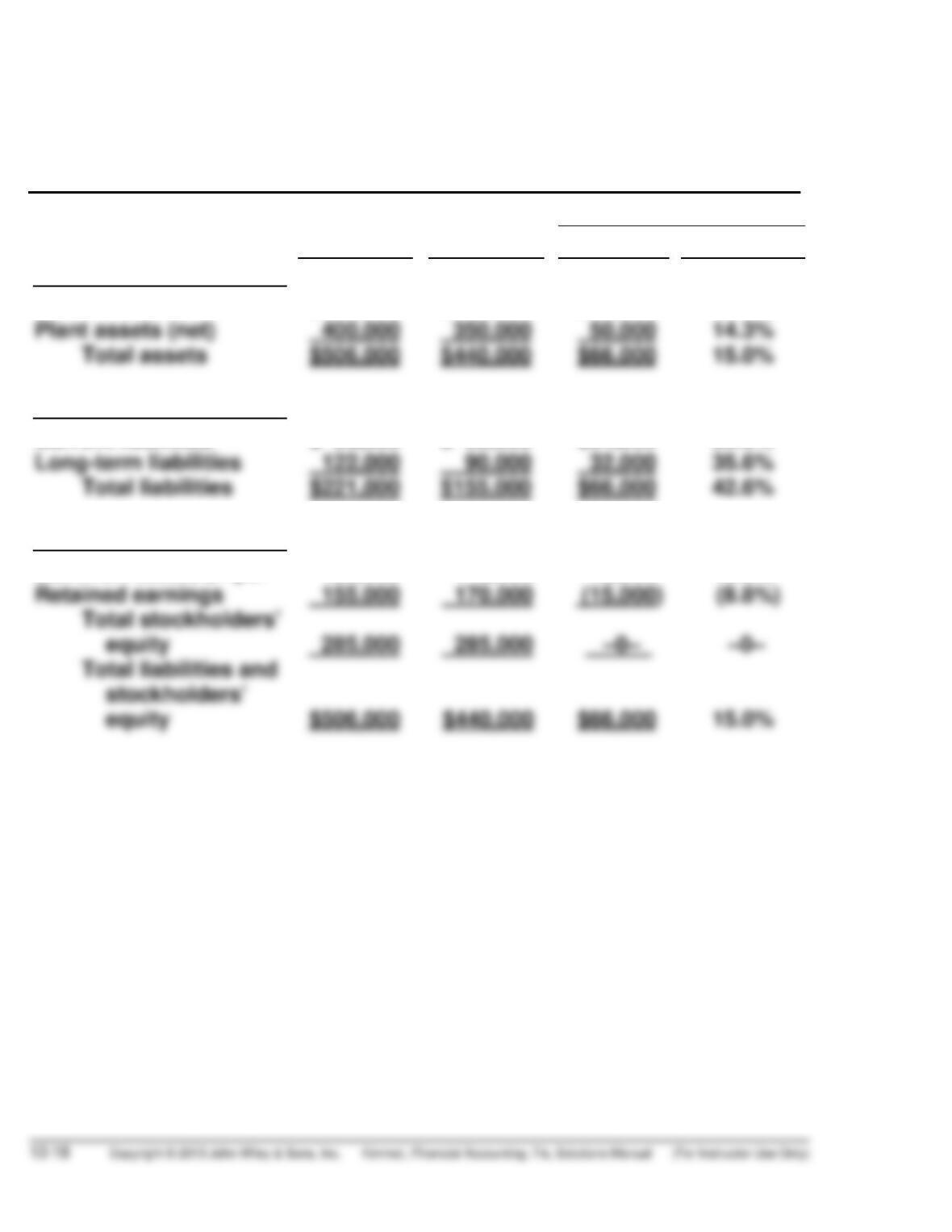

EXERCISE 13-3

SPANGLES INC.

Condensed Balance Sheet

December 31

Increase or (Decrease)

2014 2013

A

mount Percentage

Assets

Current assets

$106,000

$ 90,000

($16,000

(17.8%)

Liabilities

Current liabilities

$ 99,000

$ 65,000

($34,000

(52.3%)

Stockholders’ Equity

Common stock, $1 par

130,000

115,000

15,000

(13.0%)

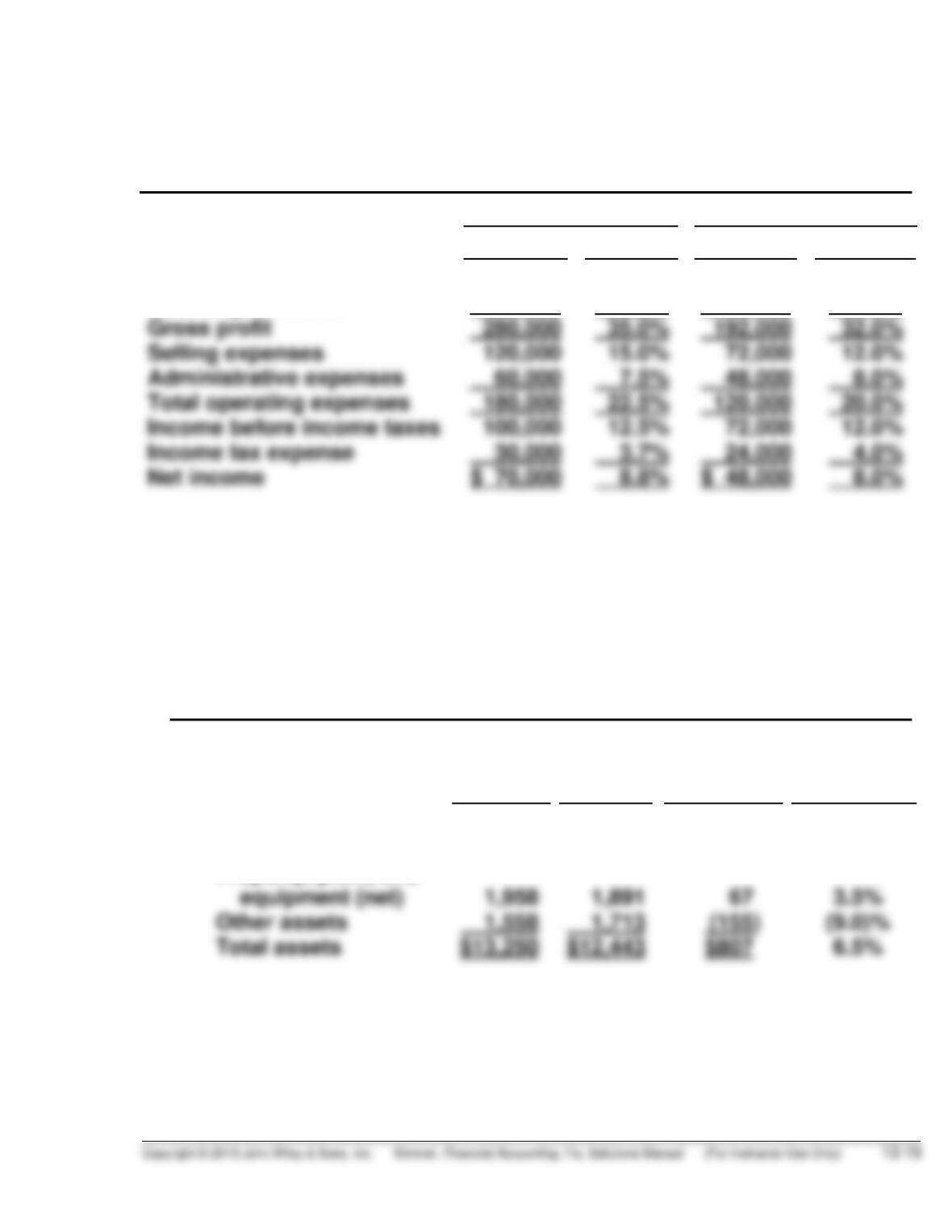

EXERCISE 13-4

JACOBS CORPORATION

Condensed Income Statement

For the Years Ended December 31

2014 2013

A

mount Percent Amount Percent

Sales revenue

Cost of goods sold

$800,000

520,000

100.0%

65.0%

$600,000

408,000

100.0%

68.0%

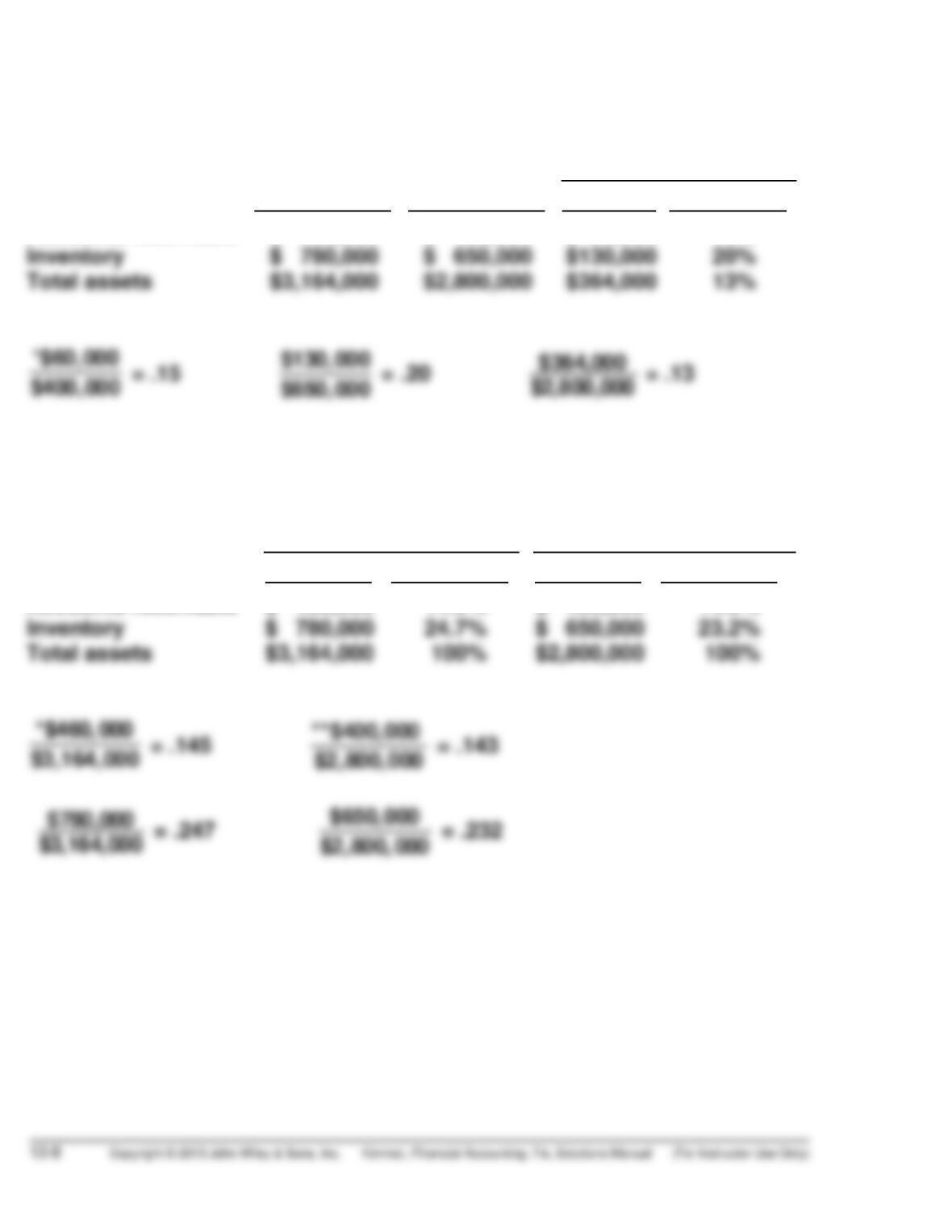

EXERCISE 13-5

(a) NIKE, INC.

Condensed Balance Sheet

May 31

($ in millions)

2014

2013

Increase

(Decrease)

Percentage

Change

from 2013

Assets

Current assets

Property, plant, and

$ 9,734

$ 8,839

$895

10.1%

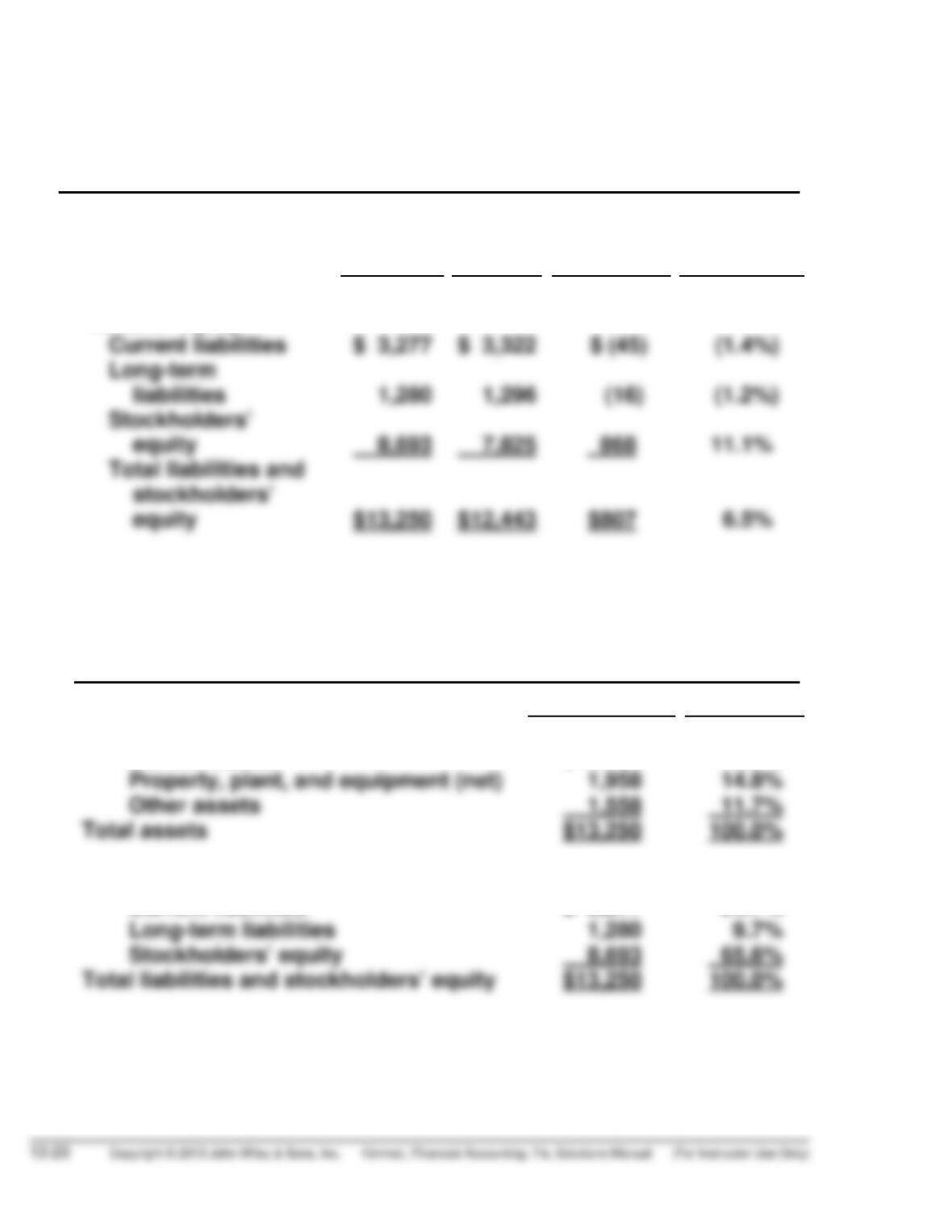

EXERCISE 13-5 (Continued)

NIKE, INC.

Condensed Balance Sheet (Continued)

December 31

2014

2013

Increase

(Decrease)

Percentage

Change

from 2013

Liabilities and stock-

holders’ equity

(b) NIKE, INC.

Condensed Balance Sheet

May 31, 2014

$ (in millions) Percent

Assets

Current assets

Liabilities and stockholders’ equity

Current liabilities

$ 9,734

$ 3,277

73.5%

24.7%