PROBLEM 13-41 (40 MINUTES)

Year

Income

Before

Depreciation

Annual

Depreciation

Income

Net of

Depreciation

Average

Net Book

Value*

ROI

Based

on

Net Book

Value†

Average

Gross

Book

Value

ROI

Based

on

Gross

Book

Value

1

$150,000

$200,000

$(50,000)

$400,000

—

$500,000

—

2

150,000

120,000

30,000

240,000

12.5%

500,000

6.0%

3

150,000

78,000

144,000

54.2%

500,000

4

150,000

96,000

118.5%

500,000

5

150,000

96,000

355.6%

500,000

†ROI rounded to the nearest tenth of 1 percent.

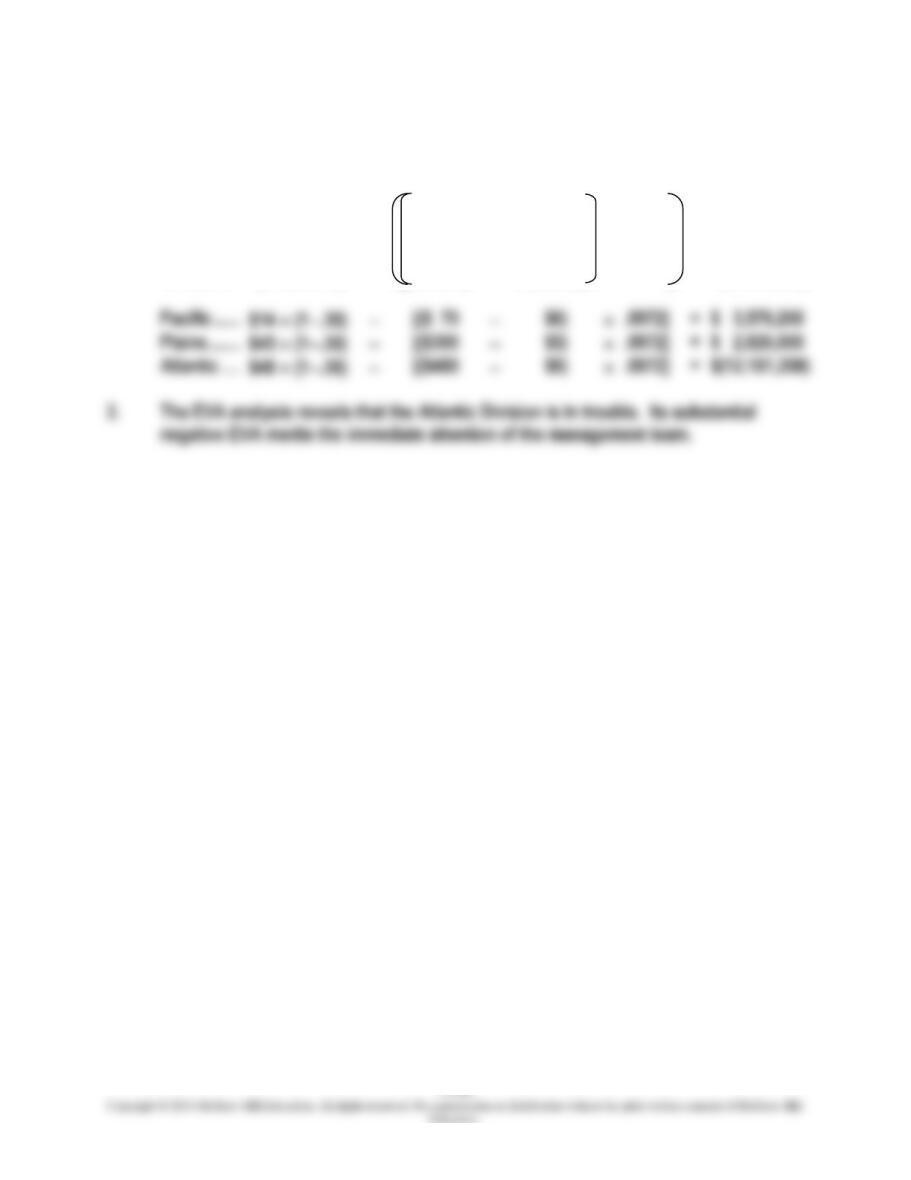

1.

This table differs from Exhibit 13-3 in that ROI rises even more steeply across time than

2.

One potential implication of such an ROI pattern is a disincentive for new investment. If

a proposed capital project shows a loss or very low ROI in its early years, a manager

Chapter 13 – Investment Centers and Transfer Pricing

PROBLEM 13-42 (40 MINUTES)

Based on Net Book Value

Based on Gross Book Value

Year

Income

Before

Depreciation

Annual

Depreciation

Income

Net of

Depreciation

Average

Net Book

Value*

Imputed

Interest

Charge†

Residual

Income

Average

Gross

Book

Value

Imputed

Interest

Charge†

Residual

Income

1

$150,000

$100,000

$50,000

$450,000

$45,000

$ 5,000

$500,000

$50,000

0

2

150,000

100,000

50,000

350,000

35,000

15,000

500,000

50,000

0

3

150,000

100,000

50,000

250,000

25,000

25,000

500,000

50,000

0

4

150,000

100,000

50,000

150,000

15,000

35,000

500,000

50,000

0

5

150,000

100,000

50,000

50,000

45,000

50,000

0

*Average net book value is the average of the beginning and ending balances for the year in net book value.

†Imputed interest charge is 10 percent of the average book value, either net or gross.

PROBLEM 13-43 (30 MINUTES)

1. Sales margin: income divided by sales revenue.

Capital turnover: sales revenue divided by invested capital

Return on investment: income divided by invested capital (or sales margin x capital

turnover).

2. Strategy (a): Income will be reduced to $450,000 because of the loss, and invested

capital will fall to $8,910,000 from the disposal. ROI = $450,000 ÷ $8,910,000, or

PROBLEM 13-43 (CONTINUED)

4. Anderson Manufacturing ROI: ($4,500,000 – $3,600,000) ÷ $7,500,000 = 12%

Palm Beach Enterprises ROI: ($6,750,000 – $6,180,000) ÷ $7,125,000 = 8%

From the preceding calculations, both investments appear attractive given the

current state of affairs (i.e., the Hardware Division’s current ROI of 6%). However, if

PROBLEM 13-44 (35 MINUTES)

1. The weighted-average cost of capital (WACC) is defined as follows:

equity

of value

Market

capital

equity

ofCost

debt of

value

Market

capital

debt

ofcost

tax–After

average

–Weighted

+

Chapter 13 – Investment Centers and Transfer Pricing

PROBLEM 13-44 (CONTINUED)

2. The three divisions’ economic–value-added measures are calculated as follows:

Division

After-Tax

Operating

Income

(in millions)

−

Total

Assets

(in

millions)

−

Current

Liabilities

(in

millions)

WACC

=

Economic

Value

Added

(in millions)

PROBLEM 13-45 (35 MINUTES)

1. The weighted-average cost of capital (WACC) is defined as follows:

equity of

value

Market

capital

equity

ofCost

debt of

value

Market

capital

debt of

cost tax–After

average–Weighted

+

2. The economic value added (EVA) is defined as follows:

−−=

average–Weighted

Investment

Investment

scenter’ Investment

Economic

For Cape Cod Lobster Shacks, Inc., we have the following calculations of EVA for each of

the company’s divisions.

PROBLEM 13-46 (25 MINUTES)

1. The Birmingham divisional manager will likely be opposed to the transfer. Currently,

2. Although Tampa is receiving a $50 “price break” on each unit purchased from

Birmingham, the $1,500 transfer price would probably be deemed too high. The

3. Although top management desires to introduce the positioning system, it should not

lower the price to make the transfer attractive to Tampa. MTI uses a responsibility

4. MTI would benefit more if it sells the diode reducer externally. Observe that the

Produce Diode;

Sell Externally

Produce Diode;

Transfer; Sell

Positioning System

Sales revenue ………………..

$1,550

$2,800

Less: Variable cost::

Contribution margin ……….

$ 550

$ 460

PROBLEM 13-47 (40 MINUTES)

1.

a.

Transfer price

=

outlay cost + opportunity cost

=

$130 + $30 = $160

b.

Transfer price

=

standard variable cost + (10%)(standard variable cost)

=

$130 + (10%) ($130) = $143

Note that the Frame Division manager would refuse to transfer at this price.

2.

a.

Transfer price

=

outlay cost + opportunity cost

=

$130 + 0 = $130

b.

When there is no excess capacity, the opportunity cost is the forgone

c.

Fixed overhead per frame (125%)($40) = $50

+ (10%)(variable cost + fixed overhead per frame)

=

$130 + $50 + [(10%)($130 + $50)]

=

$198

d.

Incremental revenue per window …………………………….

$310

Incremental cost per window, for Weathermaster

Window Company:

Direct material (Frame Division) ………………………….

$30

Direct labor (Frame Division) ………………………………

40

Variable overhead (Frame Division) ……………………..

60

Direct material (Glass Division) …………………………..

60

Direct labor (Glass Division) ……………………………….

30

Variable overhead (Glass Division) ………………………

Total variable (incremental) cost………………………….

Incremental contribution per window in special order

for Weathermaster Window Company …………………..

Chapter 13 – Investment Centers and Transfer Pricing

PROBLEM 13-47 (CONTINUED)

e.

Incremental revenue per window …………………………….

$ 310

Incremental cost per window, for the Glass Division:

Transfer price for frame [from requirement 2(c)] …..

$198

Direct material (Glass Division) …………………………..

Direct labor (Glass Division) ……………………………….

Variable overhead (Glass Division) ………………………

Total incremental cost ………………………………………..

f.

One can raise an ethical issue here to the effect that a division manager should

always strive to act in the best interests of the whole company, even if that action

3.

The use of a transfer price based on the Frame Division’s full cost has caused a cost

PROBLEM 13-48 (40 MINUTES)

1. Among the reasons transfer prices based on total actual costs are not appropriate as a

divisional performance measure are the following:

2. Using the market price as the transfer price, the contribution margin for both the

Mining Division and the Metals Division is calculated as follows:

Mining

Division

Metals

Division

Selling price …………………………………………………………………..

Less: Variable costs:

$ 270

$ 450

PROBLEM 13-48 (CONTINUED)

3. If RIRC instituted the use of a negotiated transfer price that also permitted the

divisions to buy and sell on the open market, the price range for toldine that would

be acceptable to both divisions would be determined as follows.

4. General transfer-pricing rule:

Transfer price = outlay cost + opportunity cost

= ($36 + $48 + $72)* + ($114 – $15) **

5. A negotiated transfer price is probably the most likely to elicit desirable management

behavior, because it will do the following:

PROBLEM 13-49 (30 MINUTES)

1. If the transfer price is set equal to the U.S. variable manufacturing cost, Delta

Telecom will make $98.40 per circuit board:

U.S. operation:

Sales revenue (transfer price)………………………………

$ 390.00

Less: Variable manufacturing cost………………………..

390.00

Contribution margin………………………………………….

$ —

Sales revenue……………………………………

$1,080.00

Less: Transfer price…………………………….

$390.00

60.00

39.00

834.00

Income before tax……………………………….

$ 246.00

Less: Income tax expense ($246.00 x 60%)..

147.60

Income after tax…………………………………

$ 98.40

2. If the transfer price is set equal to the U.S. market price, Delta will make $117.60 per

circuit board: $72.00 + $45.60 = $117.60. The U.S. market price is therefore more

attractive as a transfer price than the U.S. variable manufacturing cost.

U.S. operation:

Sales revenue………………………………………………….

$ 510.00

Less: Variable manufacturing cost………………………..

390.00

Income before tax…………………………………………….

$ 120.00

Less: Income tax expense ($120.00 x 40%)………………

48.00

Income after tax……………………………………………….

$ 72.00

German operation:

Sales revenue……………………………………

$1,080.00

Less: Transfer price…………………………….

$510.00

60.00

51.00

966.00

Income before tax……………………………….

$ 114.00

Less: Income tax expense ($114.00 x 60%)..

68.40

Income after tax…………………………………

$ 45.60