Chapter 13 – Investment Centers and Transfer Pricing

13-1

CHAPTER 13

INVESTMENT CENTERS AND TRANSFER PRICING

Learning Objectives

1. Explain the role of managerial accounting in achieving goal congruence.

2. Compute an investment center’s return on investment (ROI), residual income

(RI), and economic value added (EVA).

4. Describe some advantages and disadvantages of both ROI and residual income

as divisional performance measures.

6. Use the general economic rule to set an optimal transfer price.

8. Understand the behavioral issues of incentives, goal congruence, and internal

controls.

Chapter 13 – Investment Centers and Transfer Pricing

13-2

Chapter Overview

I. Delegation of Decision Making

A. Obtaining goal congruence

B. Management by objectives (MBO)

C. Adaptation of management control systems

II. Measuring Income and Invested Capital

A. Invested capital

B. Measuring investment-center income

C. Inflation: Historical-cost versus current-value accounting

III. Other Issues in Segment Performance Devaluation

A. Alternatives to ROI, residual income, and economic value added (EVA)

B. Importance of nonfinancial information

C. Measuring performance in nonprofit organizations

IV. Transfer Pricing

A. Goal congruence

B. General transfer-pricing rule

C. Transfers based on the external market price

V. Behavioral Issues: Risk Aversion and Incentives

VI. Goal Congruence and Internal Control Systems

Chapter 13 – Investment Centers and Transfer Pricing

13-3

Key Lecture Concepts

I. Delegation of Decision Making

• Most large organizations are decentralized into divisions and other sizable

subunits. These subunits are usually considered investment centers, as

• Managerial accountants must design a responsibility-accounting

framework whereby evaluation systems encourage goal congruence of

the subunits.

➢ With goal congruence, the behavior of managers throughout an

organization is directed toward attainment of top management’s

goals.

• As a company grows it will often decentralize to better control operations

and make better decisions. Performance evaluation measures thus

become necessary for each of the subunits.

• Return on investment (ROI)

➢ ROI shows the return from a given amount of invested capital:

Chapter 13 – Investment Centers and Transfer Pricing

13-4

▪ Sales margin—the amount of profit generated by each dollar

of sales. Computed as:

➢ ROI captures the interrelationships of both elements, as both are

needed for a successful operation.

➢ Managers strive to increase ROI.

▪ Sales margin can be increased by increasing income. This

can be accomplished by increasing sales prices (and more

➢ ROI measures return in a percentage form rather than in absolute

dollars, which is helpful when comparing segments of different

sizes.

➢ A drawback to using ROI is the potential of decreased goal

congruence.

Chapter 13 – Investment Centers and Transfer Pricing

13-5

• Residual income

➢ Residual income shows the amount of income a given division (or

project) earns in excess of a firm’s minimum goal.

➢ This performance measure integrates a corporate imputed interest

rate and improves goal congruence. The formula is:

➢ As long as the residual income of a project is a positive amount, the

project is deemed attractive because it increases a manager’s

➢ Since residual income is expressed in absolute dollar terms, an

analyst forfeits the ability to compare firms/divisions of differing

sizes on a common basis.

➢ Both ROI and residual income are useful, but both tools have

Teaching Tip: To further emphasize the problems of comparing units of

vastly different size on the basis of dollar measures, you may want to cite

Chapter 13 – Investment Centers and Transfer Pricing

13-6

➢ Economic value added (EVA), which is conceptually similar to

residual income, measures the amount of shareholder wealth being

created. It is computed as follows:

EVA = Investment center after-tax income – [(Investment

➢ The weighted-average cost of capital (WACC) measures the

average cost of a company’s debt and equity capital.

▪ The cost of debt capital is the after-tax cost of interest, after-

tax because interest payments are tax deductible.

II. Measuring Income and Invested Capital

• Income and invested capital, factors in the ROI, residual income, and EVA

performance models, can each be defined in several ways.

• Invested capital can be defined as total assets, productive assets, or total

Chapter 13 – Investment Centers and Transfer Pricing

13-7

➢ The “definition decision” is further complicated when combined

with the additional decision of whether to use net book value or

gross value of long-lived assets. Issues to consider in this decision

include:

▪ The use of net book value produces valuations that are

consistent with those shown on the balance sheet.

• Another decision involves income measurement. Income should be

defined as controllable income if the performance model is to be a

motivator and if responsibility accounting is used by the firm.

III. Other Issues in Segment Performance Devaluation

• Some firms use alternatives to ROI, residual income, and economic value

added. These three measures are short-run performance measures.

IV. Transfer Pricing

• Goal congruence is achieved by following a general transfer-pricing rule:

Transfer price = Additional unit outlay cost incurred because goods are

Chapter 13 – Investment Centers and Transfer Pricing

13-8

transferred + Opportunity cost per unit to the organization because of the

transfer

➢ Using the general rule, the selling division is reimbursed for the

variable costs of the product or service plus any margin forgone by

not selling in the external marketplace.

➢ In situations where the external market is willing to buy all the

➢ If there is no external buyer (excess capacity exists), the product or

service would transfer at an amount equal to variable cost, as there

would be no contribution margin forgone.

➢ The general model is often difficult to implement because of

• Market-based prices

➢ Such prices are consistent with the responsibility-accounting

• Negotiated prices

➢ Some companies allow buying and selling units to negotiate the

transfer price, particularly if no external market exists.

➢ Even in the case of an external price, the external price might serve

Chapter 13 – Investment Centers and Transfer Pricing

13-9

• Cost-based prices

➢ Transfer prices may be based on a cost-plus scheme by marking up

either variable cost or full cost by a percentage. The policy of

• Other transfer pricing issues

➢ Transfer prices are used in a decentralized environment where

managers have authority to make decisions and control operations.

When disputes arise, top management should step aside and let the

V. Behavioral Issues: Risk Aversion and Incentives

• Performance-evaluation systems must include incentives for managers to

achieve goal congruence. Such systems, though, are often affected by

factors beyond a manager’s control, with the manager confronting various

risks while doing his or her job.

VI. Goal Congruence and Internal Control Systems

• An internal control system is designed to provide reasonable assurance of

the achievement of objectives in three areas:

Chapter 13 – Investment Centers and Transfer Pricing

13-10

➢ The effectiveness and efficiency of operations;

Chapter 13 – Investment Centers and Transfer Pricing

13-11

Teaching Overview

The subject matter in this chapter is difficult to teach. I have drawn this conclusion

based on student reaction to my presentations and, perhaps more telling, numerous

conversations with colleagues from around the country. The interest level that

accompanies many other managerial accounting topics is often lacking with this

material.

Exercise 13-29 is a good demonstration problem to use when discussing ROI and

Chapter 13 – Investment Centers and Transfer Pricing

13-12

Links to the Text

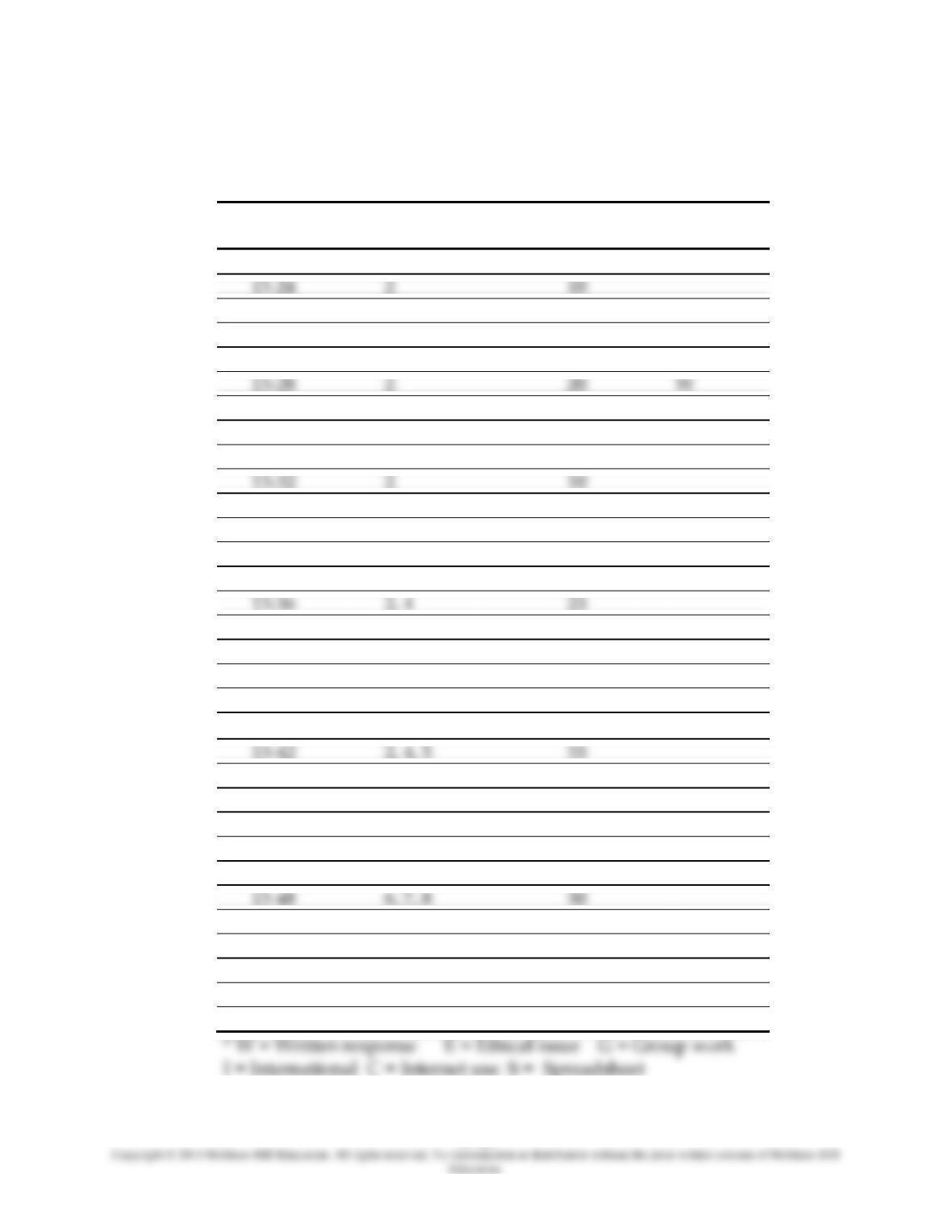

Homework Grid – CHAPTER 13

Item No.

Learning

Objectives

Completion

Time (min.)

Special

Features*

Exercises:

13-24

2

10

13-25

3

15

13-26

2

5

13-27

2

15

I

13-28

2

20

W

13-29

1, 2

30

13-30

2, 4, 5

30

W

13-31

1, 8

15

E

13-32

2

10

13-33

2

15

13-34

6

10

13-35

7

25

Problems:

13-36

2, 4

25

13-37

2, 3

45

13-38

3

20

13-39

2, 4

25

W

13-40

2, 4, 8

40

13-41

2, 4, 5

40

13-42

2, 4, 5

35

13-43

2, 4, 8

30

13-44

2

35

I

13-45

2

35

13-46

7

40

13-47

6, 7, 8

25

E

13-48

6, 7, 8

30

13-49

6, 7

40

I

Cases:

13-50

1, 2, 4, 8

40

W

13-51

6, 7, 8

45

G, E

13-52

6, 7, 8

50

G