1. A company may temporarily have excess cash that is not needed for use in its current

operations. Instead of letting excess cash remain idle in a checking account, most companies

2. A gain or loss can occur when the selling price of the bond differs from the book value (cost) of

3. The equity method is used for equity investments representing more than 20% and less than 50%

of the outstanding shares of the investee.

4. Under the cost method, a dividend received is treated as dividend revenue. Under the equity

5. An investment greater than 50% of the investee is considered to be an investment that exerts

6. Both portfolios are reported at fair value. However, changes in the fair value of trading securities

7. A credit balance in Valuation Allowance for Available-for-Sale Investments is subtracted from

Available-for-Sale Investments (at cost). The net reported amount is the available-for-sale securities

at fair value.

8. A debit balance in Unrealized Gain (Loss) on Available-for-Sale Investments would be reported as a

reduction in the Stockholders’ Equity section of the balance sheet, after Retained Earnings.

9. Over the past several decades, the financial statements of companies in most industries have

included more fair value measures. This is partially due to the Financial Accounting Standards

10. When an asset or a liability is reported at its fair value, any difference between the asset’s original

cost or prior period’s fair value must be recorded. The account, Valuation Allowance for Trading

CHAPTER 13

INVESTMENTS AND FAIR VALUE ACCOUNTING

DISCUSSION QUESTIONS

13-1

CHAPTER 13 Investments and Fair Value Accounting

PE 13–1A

a. Investments—Oates City Bonds 300,000

Interest Receivable 3,000

Cash 303,000

…

PE 13–1B

a. Investments—Iceline Inc. Bonds 120,000

Interest Receivable 1,000

Cash 121,000

…

PRACTICE EXERCISES

CHAPTER 13 Investments and Fair Value Accounting

PE 13–2A

10 Investments—Sting Company Stock* 375,150

*$0.40 per share × 15,000 shares

29 Cash* 191,880

PE 13–2B

12 Investments—Aspen Company Stock* 100,200

*$0.50 per share × 2,000 shares

10 Cash* 50,250

Feb.

May

Sept.

Nov.

13-3

CHAPTER 13 Investments and Fair Value Accounting

PE 13–3A

2 Investment in Gruden Company Stock 625,000

Cash 625,000

PE 13–3B

2 Investment in Fain Company Stock 500,000

Cash 500,000

PE 13–4A

31 Unrealized Loss on Trading Investments* 27,600

2016

Dec.

Jan.

Jan.

CHAPTER 13 Investments and Fair Value Accounting

PE 13–4B

31 Valuation Allowance for Trading Investments*

PE 13–5A

31 Unrealized Gain (Loss) on Available-for-Sale

Investments*

…

PE 13–5B

31 Valuation Allowance for Available-for-Sale

Investments*

…

Dec.

2,090

2016

5,800

2016

Dec.

2016

Dec. 4,800

13-5

CHAPTER 13 Investments and Fair Value Accounting

PE 13–6A

PE 13–6B

Dividend Yield Dividends per Share of Common Stock

Market Price per Share of Common Stock

=

Dividends per Share of Common Stock

Market Price per Share of Common Stock

Dividend Yield

=

13-6

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–1

a.

*$50,000 × 96%

d.

31 Interest Receivable* 1,000

Interest Revenue 1,000

Accrued interest.

c.

1Cash 7,700

Interest Receivable 3,850

Interest Revenue* 3,850

*$220,000 × 7% × 3/12

Apr.

2017

2016

Dec.

EXERCISES

2016

13-7

CHAPTER 13 Investments and Fair Value Accounting

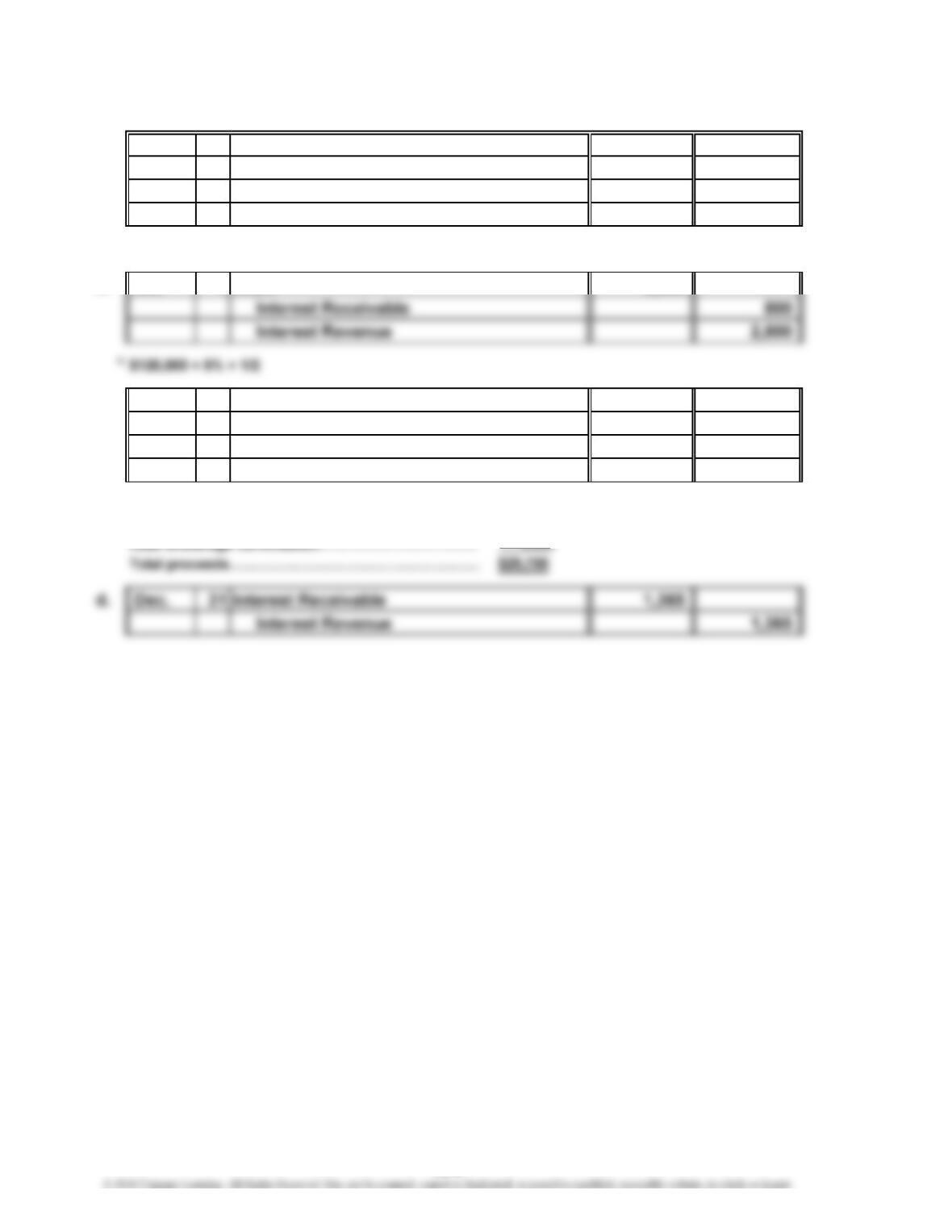

Ex. 13–3

a.

11 Investments—Sanz County Bonds 120,000

Interest Receivable* 800

Cash 120,800

*$120,000 × 6% × 40 ÷ 360

b. 1 Cash* 3,600

c. 31 Cash* 29,750

Loss on Sale of Investments 400

Interest Revenue 150

Investments—Sanz County Bonds 30,000

*Bond sale ($30,000 × 0.99)………………………………

…

$29,700

Accrued interest…………………………………………… 150

(100)

May

2016

Oct

Oct

13-8

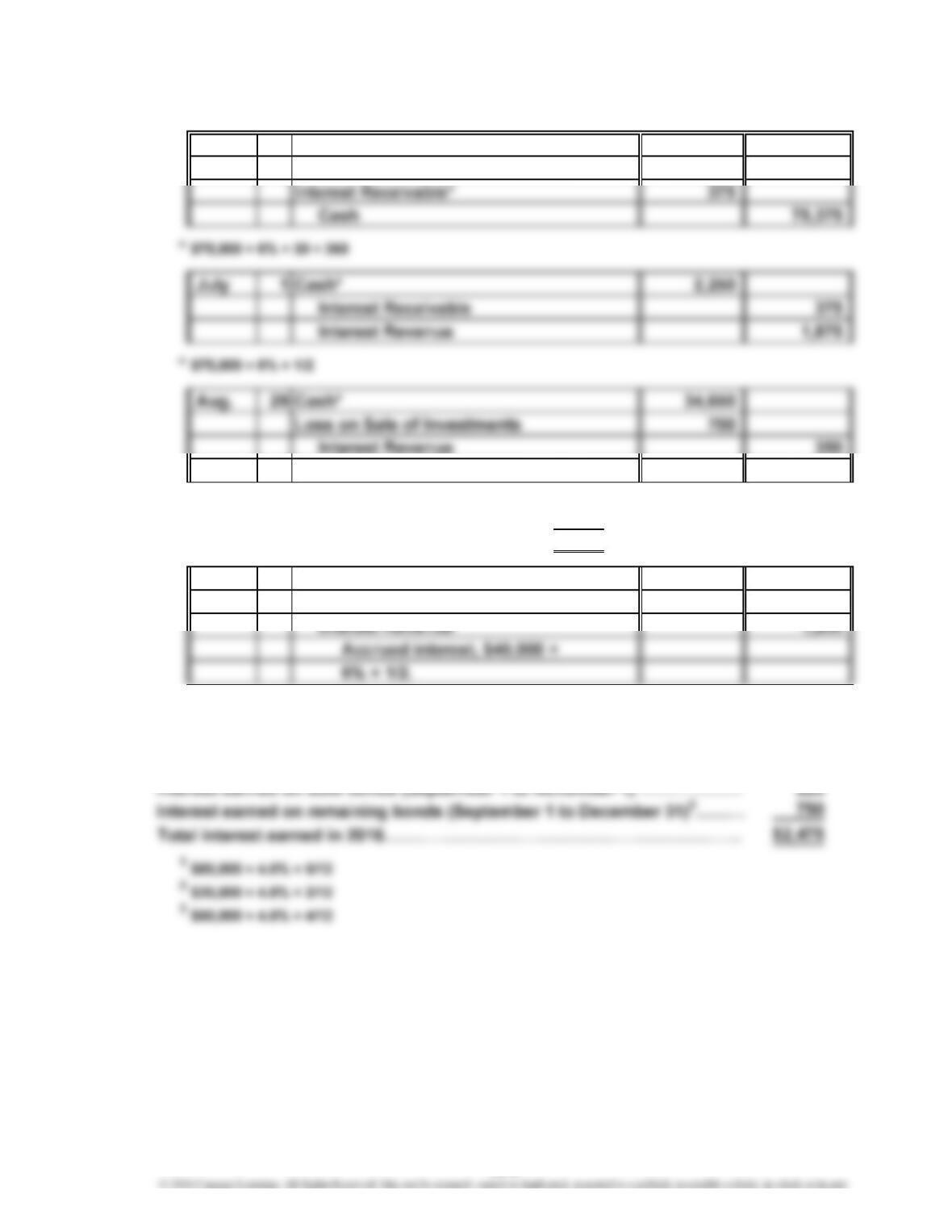

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–4

a.

31 Investments—Government Bonds 75,000

Investments—Government Bonds 35,000

*Bond sale ($35,000 × 98%)………………………………

…

$34,300

Accrued interest…………………………………………… 350

Total proceeds from sale…………………………………

…

$34,650

b.

31 Interest Receivable 1,200

Ex. 13–5

Interest earned (April 1 to September 1)1………………………………………

…

$1,500

Jan.

2016

2016

Dec.

13-9

CHAPTER 13 Investments and Fair Value Accounting

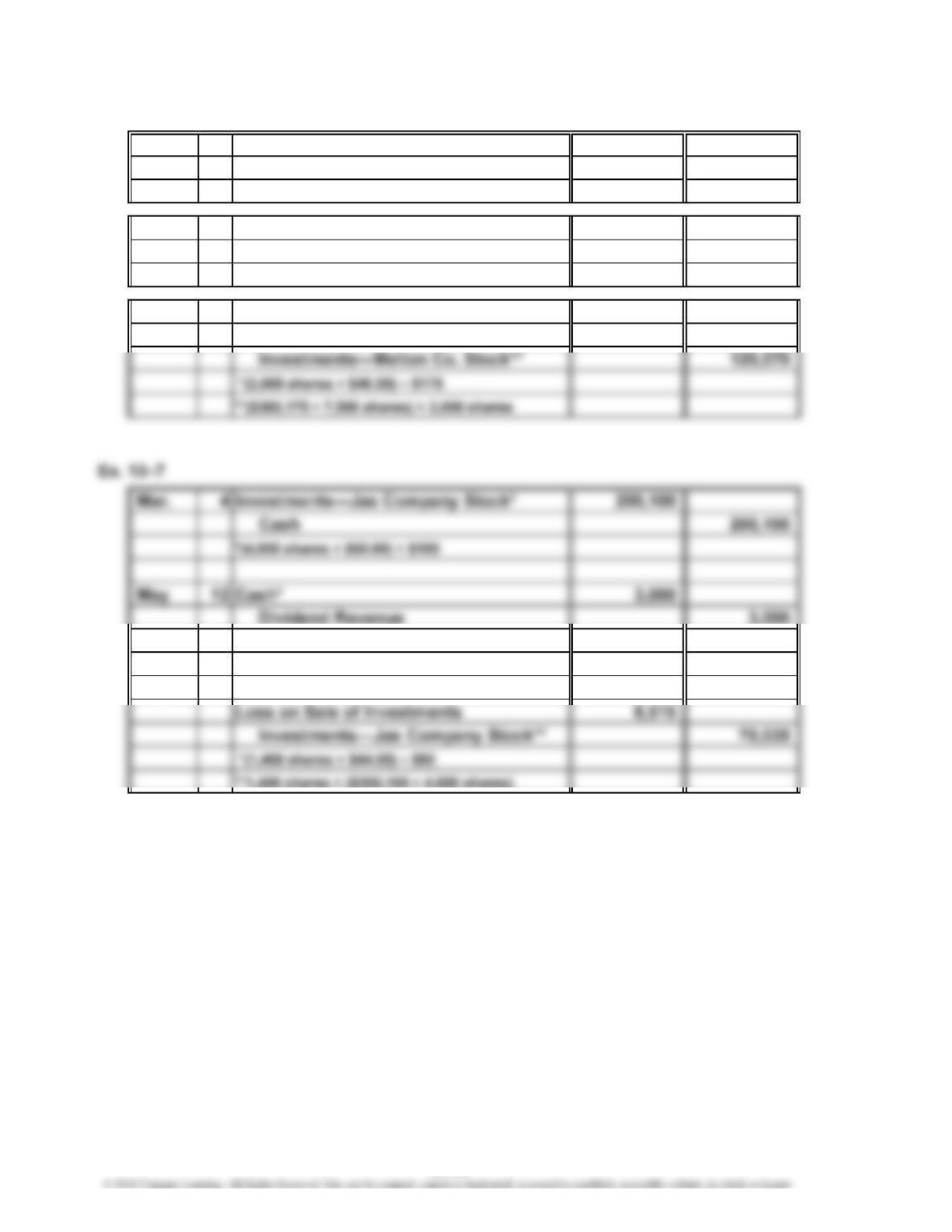

Ex. 13–6

a. 4 Investments—Melton Co. Stock* 300,175

Cash 300,175

*(7,500 shares × $40.00) + $175

b. 15 Cash* 15,750

Dividend Revenue 15,750

*$2.10 × 7,500 shares

c. 12 Cash* 137,825

Gain on Sale of Investments 17,755

*$0.75 per share × 4,000 shares

17 Cash* 61,520

June

Oct.

Mar.

June

13-10

CHAPTER 13 Investments and Fair Value Accounting

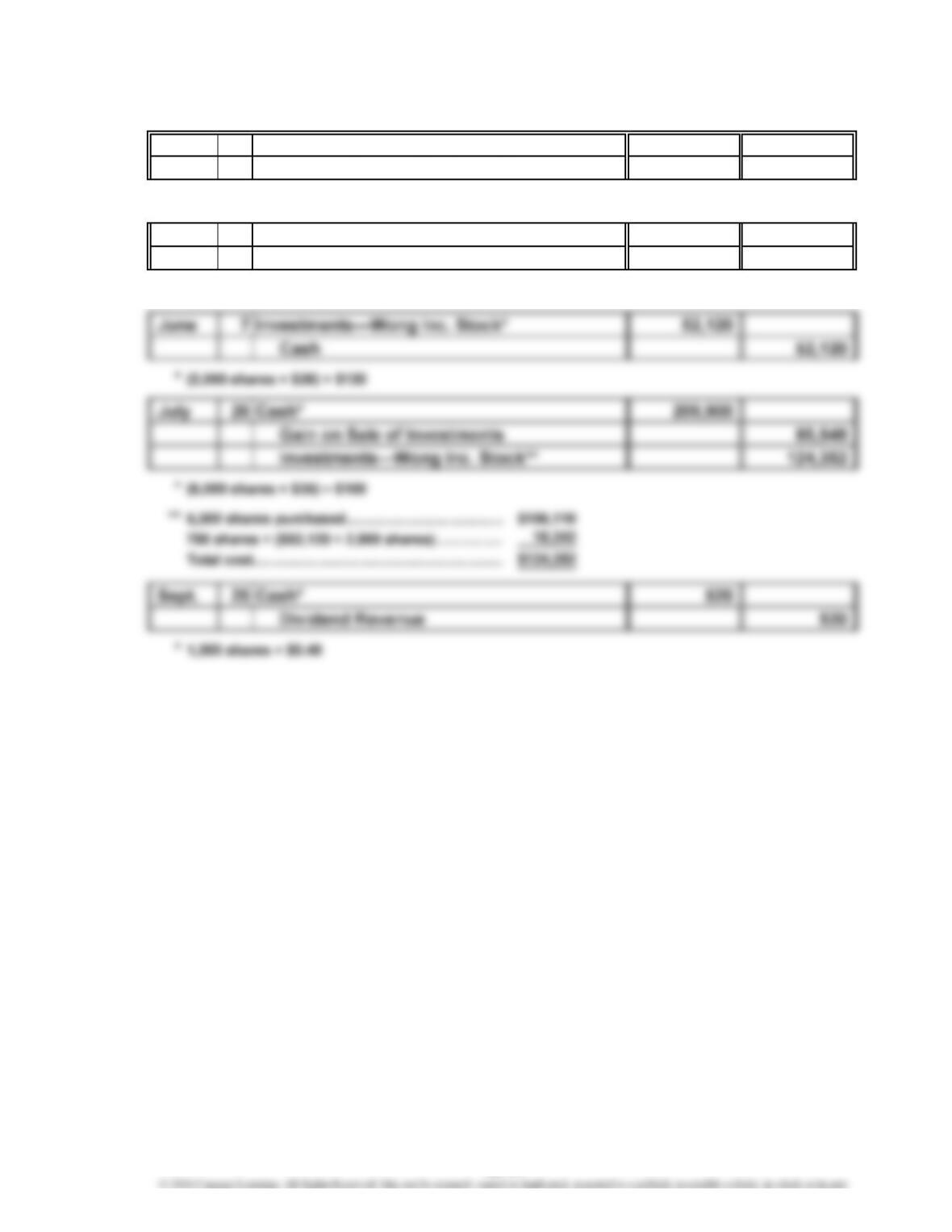

Ex. 13–8

2 Investments—Wong Inc. Stock* 106,110

Cash 106,110

*(5,300 shares × $20) + $110

6 Cash* 1,590

Dividend Revenue 1,590

*5,300 shares × $0.30

Feb.

Mar.

13-11

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–9

Feb. 24 Investments—Tett Co. Stock* 85,150

Cash 85,150

*(1,000 shares × $85) + $150

May 16 Investments—Issacson Co. Stock* 90,100

Cash 90,100

*(2,500 shares × $36) + $100

Oct. 31 Cash* 240

Dividend Revenue 240

*(1,000 shares – 400 shares) × $0.40

Ex. 13–10

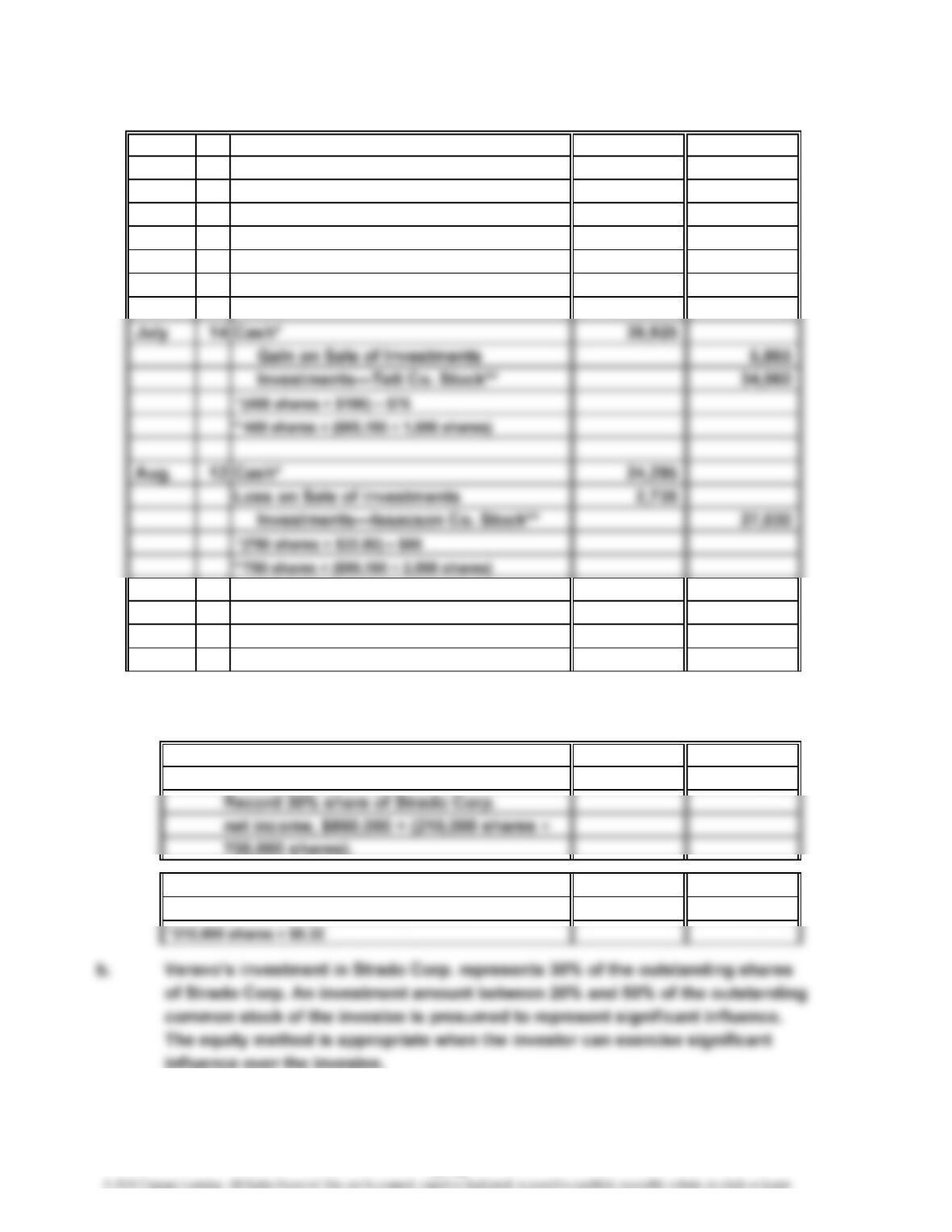

a. 1. Investment in Strado Corp. Stock 258,000

Income of Strado Corp. 258,000

2. Cash* 67,200

Investment in Strado Corp. Stock 67,200

13-12

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–11

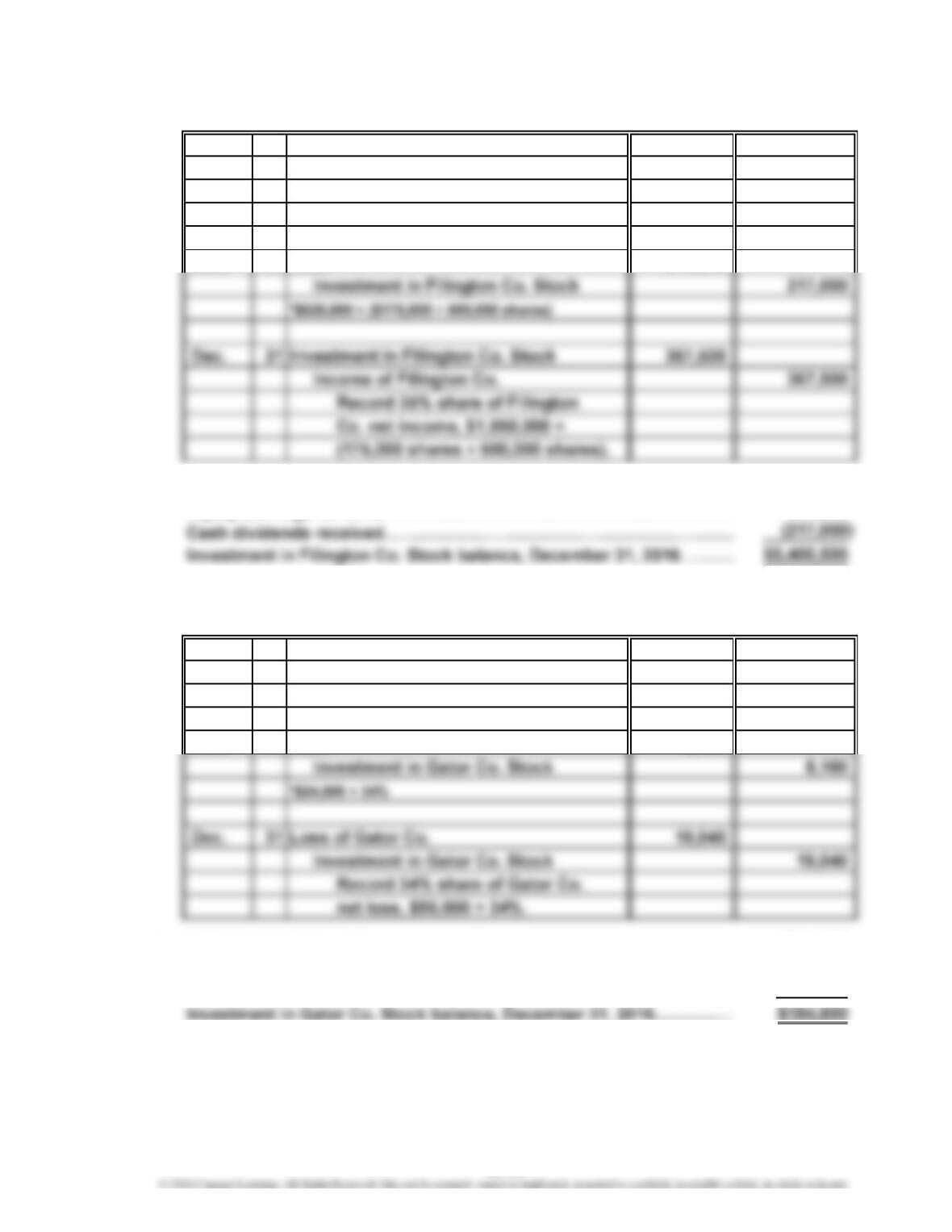

a.

14 Investment in Filington Co. Stock* 5,250,000

Cash 5,250,000

*175,000 shares × $30 per share

24 Cash* 217,000

b. Initial acquisition cost………………………………………………………… $5,250,000

Equity earnings for 2016……………………………………………………… 367,500

…

Ex. 13–12

a.

6 Investment in Gator Co. Stock 212,000

Cash 212,000

30 Cash* 8,160

b. Initial acquisition cost………………………………………………………… $212,000

Equity loss for 2016……………………………………………………………

…

(19,040)

Cash dividends received……………………………………………………

…

(8,160)

June

2016

Jan.

2016

June

Jan.

13-13

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–12 (Concluded)

c. Under the equity method, the investor will record their proportionate share of

the net increase (or decrease) of the book value of the investee resulting from

earnings and dividend distributions. The fair value method uses market price

information to value the investment in the investee. These two methods result

Ex. 13–13

Investment in Raven Company stock, December 31, 2016……………………

…

Plus equity earnings in Raven Company…………………………………………

…

Less dividends received*……………………………………………………………

…

Investment in Raven Company stock, December 31, 2017……………………

…

*The Raven Company investment is accounted for under the equity method. Because

Ex. 13–14

a. $6,000 {$35,000 [from (c)] – $29,000 [from (b)]}

b. $29,000 [$17,000 – $(12,000)]

c. $35,000 ($245,000 – $210,000)

$281

(in millions)

$264

25

(8)

13-14

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–15

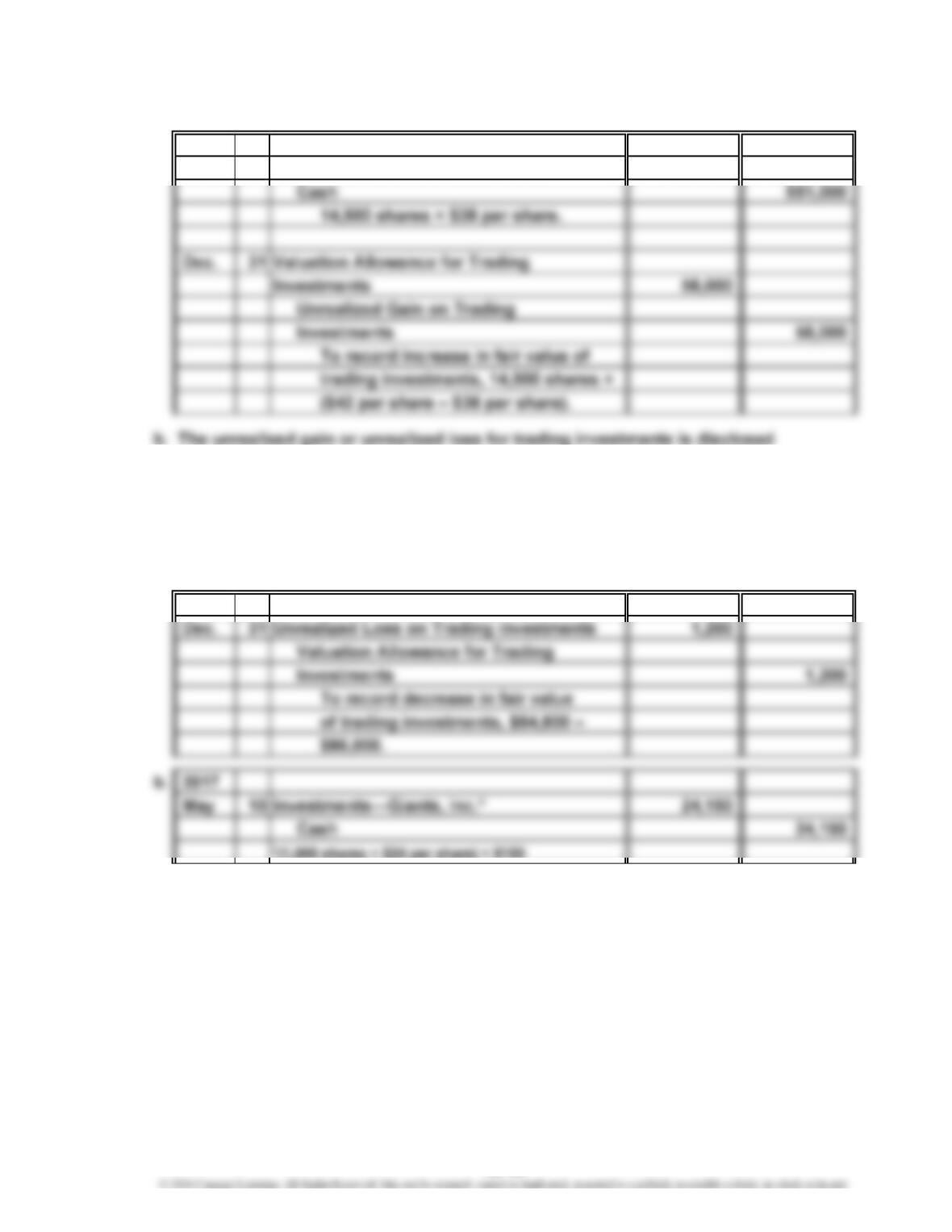

a.

24 Investments—Raiders, Inc. Stock 551,000

in the income statement as “other income” (or a separate item if significant).

Unrealized losses would be deducted in determining net income, while

unrealized gains would be added in determining net income.

Ex. 13–16

a.

Feb.

2016

2016

13-15

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–17

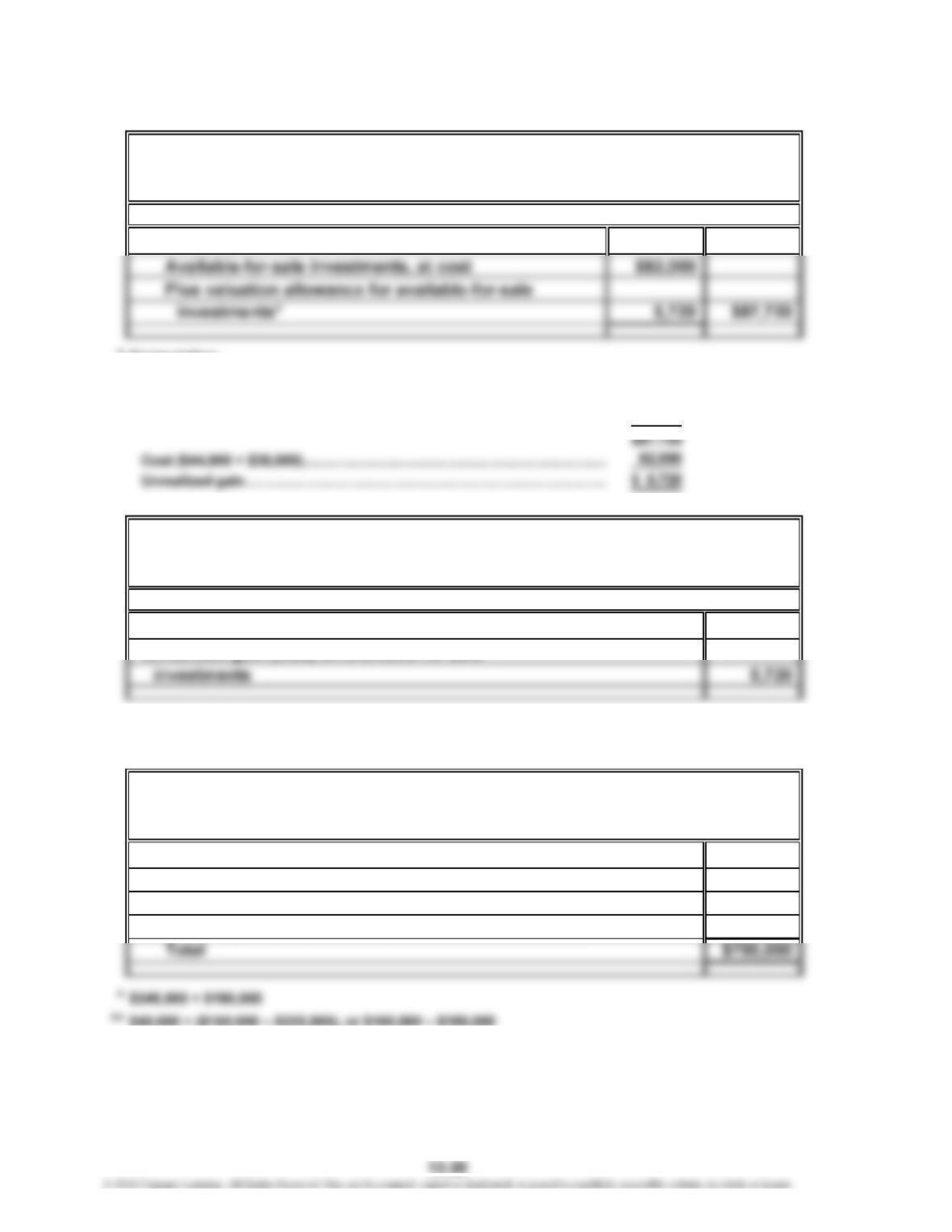

a.

31 Valuation Allowance for Trading

*

$337,500 – $320,000, as determined from the following schedule:

Cost

Arden Enterprises, Inc. ………………………………………………………

…

$150,000 $170,000

French Broad Industries, Inc. ………………………………………………

…

66,000 71,500

b. There would be no adjusting entry for December 31, 2017, if the market prices

remained unchanged from December 31, 2016. This is because the unrealized

Ex. 13–18

a. Retained earnings, December 31, 2015……………………………………

…

Plus net income…………………………………………………………………

…

…

…

$1,070,000

Fair Value

(Dec. 31, 2016)

$ 825,000

245,000

Dec.

2016

1

2

13-16

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–19

a. ($44,600 – $7,500)

b. ($220,000 – $175,400)

12 Investments—Bengals Inc. Stock 430,300

Cash 430,300

33,100 shares × $13 per share.

31 Unrealized Gain (Loss) on Available-for-

Dec.

$37,100

$44,600

2016

Sept.

13-17

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–21

a. 1.

2.

12 Investments—Rogue Wave Inc.* 65,350

2016

2017

June

13-18

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–22

a.

31 Unrealized Gain (Loss) on Available-for-

Sale Investments 4,250

Valuation Allowance for Available-for-

Sale Investments*

*

$259,450 – $263,700, as determined from the following schedule:

Cost

Dust Devil, Inc. …………………………………………………………………

…

$ 81,700 $ 76,000

b. There is no income statement impact from the December 31, 2016, adjusting

entry. Unrealized Gain (Loss) on Available-for-Sale Investments is reported

Fair Value

(Dec. 31, 2016)

4,250

2016

Dec.

1

2

13-19

CHAPTER 13 Investments and Fair Value Accounting

Ex. 13–23

a.

Current assets:

*Computation:

Market:

Hawking Inc.: 900 shares × $50…………………………………………

…

$45,000

Pavlov Co.: 1,780 shares × $24…………………………………………

…

42,720

b.

Retained earnings $300,000

Unrealized gain (loss) on available-for-sale

Ex. 13–24

Common stock $ 50,000

Paid-in capital in excess of par 250,000

Retained earnings* 520,000

Unrealized gain (loss) on available-for-sale investments** (25,000)

GALILEO COMPANY

Assets

GALILEO COMPANY

Balance Sheet (selected items)

December 31, 2016

December 31, 2016

Balance Sheet (selected items)

December 31, 2016

Stockholders’ Equity

COPERNICUS CORPORATION

Balance Sheet (selected Stockholders’ Equity items)