Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-1

CHAPTER 13

ACCOUNTING FOR CORPORATIONS

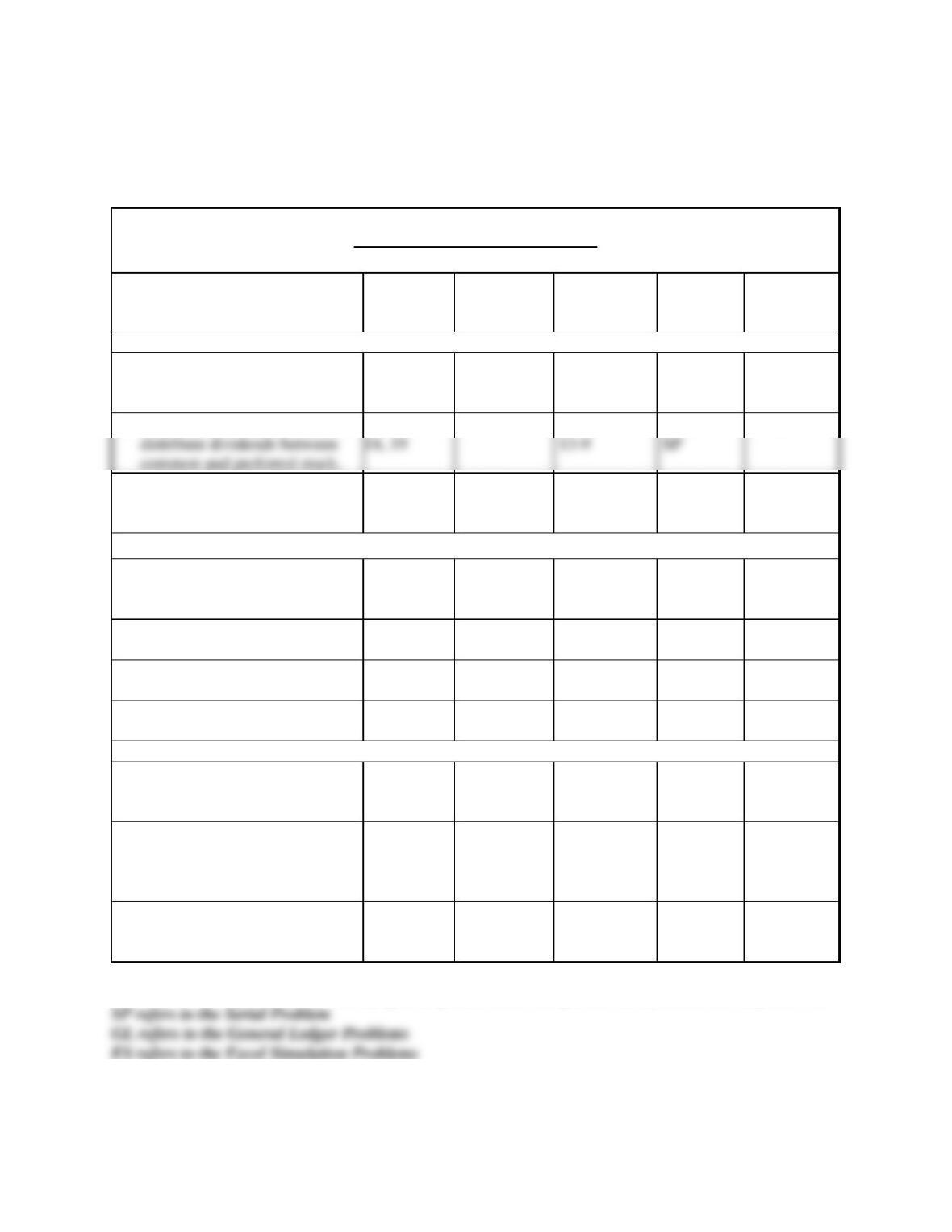

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Identify characteristics of

corporations and their

organization.

1, 2, 3, 4

13-1

13-1

SP

13-5

C2. Explain characteristics of, and

5, 6, 7, 17,

13-9, 13-10

13-7, 13-8,

13-1, 13-5,

13-1, 13-7

C3. Explain the items reported in

retained earnings.

13-13

13-11, 13-17,

13-18

13-2, 13-4,

GL 13-1,

GL 13-2

13-3, 13-5

13-9

Analytical objectives:

A1 Compute earnings per share

and describe its use.

15

13-14, 13-15

13-12, 13-13

13-1, 13-2,

13-4, 13-8,

13-9

A2. Compute price-earnings ratio

and describe its use in analysis.

13-16

13-14

13-2, 13-4,

13-8

A3. Compute dividend yield and

explain its use in analysis.

13-17

13-15

13-2, 13-8

A4. Compute book value and

explain its use in analysis.

16

13-18

13-16

13-5

13-1, 13-2

Procedural objectives:

P1. Record the issuance of

corporate stock.

13-2, 13-3,

13-4, 13-5,

13-19

13-2, 13-3,

13-4, 13-17

13-1, SP

P2. Record transactions

involving cash dividends, stock

dividends and stock splits.

8, 9, 10, 11

12

13-6, 13-7,

13-8, 13-12

13-5, 13-6,

13-18

13-2, 13-3,

13-4, ES

GL13-1,

GL13-2

13-7

P3. Record purchases and sales

of treasury stock.

13, 14

13-11, 13-12

13-10, 13-18

13-2, 13-4,

GL 13-1,

GL 13-2

13-6

*See additional information on next page that pertains to these quick studies, exercises and problems.

distribute dividends between

common and preferred stock.

18, 19

13-9

SP

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-2

Additional Information on Related Assignment Material

Connect

Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all Exercises and

Problems Set A. Connect also provides algorithmic versions for Quick Study, Exercises and Problems. It allows

instructors to monitor, promote, and assess student learning. It can be used in practice, homework, or exam mode.

Connect Insight

The first and only analytics tool of its kind, Connect Insight is a series of visual data displays that are each framed

by an intuitive question and provide at-a-glance information regarding how an instructor’s class is performing.

Connect Insight is available through Connect titles.

The Serial Problem for Success Systems continues in this chapter.

General Ledger

Assignable within Connect, General Ledger (GL) problems offer students the ability to see how transactions post

from the general journal all the way through the financial statements. Critical thinking and analysis components are

added to each GL problem to ensure understanding of the entire process. GL problems are auto-graded and provide

instant feedback to the student.

Excel Simulations

Assignable within Connect, Excel Simulations allow students to practice their Excel skills—such as basic formulas

and formatting—within the context of accounting. These questions feature animated, narrated Help and Show Me

tutorials (when enabled). Excel Simulations are auto-graded and provide instant feedback to the student.

Synopsis of Chapter Revisions

NEW opener—Tesla Motors and entrepreneurial assignment.

Streamlined discussion of corporate characteristics.

Updated the Target stock quote data.

Simplified section on stock dividends.

Continued 5-step process for stock dividends.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-3

Chapter Outline

Notes

I. Corporate Form of Organization—An entity created by law that is

separate from its owners. Owners are called stockholders. A publicly

held corporation offers its stock for public sale (organized stock

market) whereas a privately held (closely held) corporation does not.

A. Characteristics of a Corporation—Advantages

1. Separate legal entity—a corporation, through its agents

(officers and managers), operates with the same rights, duties,

and responsibilities of a person.

2. Limited liability of stockholders—stockholders are not liable

for corporate acts or debt.

3. Transferable ownership rights—transfer of shares generally

has no effect on corporation operation.

4. Continuous life⎯corporation’s life is indefinite because it is

not tied to physical life of owners.

5. Lack of mutual agency for stockholders—stockholders do not

have the power to bind the corporation to contracts.

6. Ease of capital accumulation—Buying stock is attractive to

investors and enables a corporation to accumulate large

amounts of capital.

B. Characteristics of a Corporation—Disadvantages

2. Corporate taxation—corporate income is taxed; and when

income is distributed to shareholders as dividends, it is taxed a

second time as personal income (double taxation).

C. Corporate Organization and Management

fees, promoters’ fees, and amounts paid to obtain a charter.

Expensed as incurred.

1. Incorporation—A corporation is created by obtaining a charter

from a state government. A charter application, signed by

prospective stockholders (incorporators or promoters) must

be filed with the state and fees must be paid.

2. Organization Expenses (organization costs)—include legal

3. Management of a Corporation

a. Stockholders control corporation by electing its board of

directors.

b. Board of directors (BOD) has final managing authority,

but it usually limits its actions to setting broad policy.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-4

Chapter Outline

Notes

c. Executive officers (appointed by the BOD) manage the

day-to-day direction of corporation. President is often the

D. Stockholders of Corporations

1. Rights of Stockholders—Specific rights are granted by the

charter and general rights by state laws. State laws vary but

common stockholders general rights usually include right to:

a. Vote at stockholders’ meeting.

b. Sell or otherwise dispose of their stock.

c. Purchase their proportional shares of any common stock

later issued; called preemptive right.

2. Stock Certificates and Transfer

a. Stock certificate is sometimes received as proof of share

3. Registrar and Transfer Agents—if stock is traded on a major

exchange, the corporation must have both a registrar and

transfer agent (usually large banks or financial institutions).

a. Registrar—keeps stockholder records and prepares

official lists of stockholders for stockholders’ meetings

E. Basics of Capital Stock—shares issued to obtain capital (owner

financing).

1. Authorized stock—the total amount of stock that the charter

authorizes for sale.

2. Issuing stock—can be sold directly/indirectly to stockholders.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-5

Chapter Outline

Notes

3. Market value of stock—the price at which a stock is bought

and sold.

4. Classes of stock

common stockholders in one or more ways.

a. Common—the name of stock when all classes have same

5. Par value stock—a class of stock that is assigned a value per

share by the corporation in its charter.

a. Printed on the stock certificate.

b. In many states, used to establish minimum legal capital.

6. No-par value stock—not assigned a value per share by the

corporate charter.

7. Stated value stock—no–par stock that is assigned a “stated”

8. Stockholders’ (Shareholders’) Equity—has two parts:

a. Paid-in capital (contributed capital)—the total amount of

cash and other assets received by the corporation from its

stockholders in exchange for stock.

II. Common Stock—Issuance of stock affects only paid-in capital

accounts, not retained earnings accounts.

A. Issuing Par Value Stock

1. At par for cash—debit Cash for # shares issued x market price

and credit Common Stock for # shares issued x par value

2. Issuing par value stock at a premium. (Premium on stock is an

amount paid in excess of par by the purchasers of newly

issued stock.)

growth, and other company and economic events.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-6

Chapter Outline

Notes

3. Issuing par value stock at a discount— Discount occurs when

stock is sold for less than its par value (prohibited by most

states).

a. Debit Cash (# shares issued x market price).

b. Credit Common Stock (# shares issued x par value).

B. Issuing No Par Value Stock

When no-par stock is not assigned a stated value, the entire

amount received becomes legal capital and is recorded as

Common Stock.

C. Issuing Stated Value Stock

Stated value becomes legal capital and is credited to a no-par stock

account. If stock is issued at an amount in excess of stated value,

this excess is credited to Paid-In Capital in Excess of Stated Value,

Common Stock.

D. Issuing Stock for Noncash Assets

1. Issuing par value stock for other assets

a. Record the transaction at the market value of the noncash

asset as of the date of the transaction.

2. Issuing par value stock for organizational costs—stock is

issued in exchange for services (from promoters, lawyers,

accountants) in organizing the corporation

a. Record the transaction at the market value of the services

received debiting this amount to Organization Expense.

III. Dividends

A. Cash Dividends—decision to pay these dividends rest with board

of directors and is based on evaluating the amounts of retained

earnings and cash as well as many other factors.

1. Accounting for cash dividends involves three important dates.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-7

Chapter Outline

Notes

b. Date of Record—date specified for identifying

stockholders (owners on this date will receive dividend).

c. Date of Payment—date corporation makes payment.

2. Cash Dividend Entries—reduce in equal amounts both cash

and the retained earnings component of stockholders’ equity.

b. At payment—Debit Dividends Payable and credit Cash.

3. Deficits and Cash Dividends—a debit (abnormal) balance in

retained earnings is called a retained earnings deficit.

of original investment back to investors.

a. Arises when cumulative losses and/or dividends are

B. Stock Dividends—Distribution of additional shares of stock to

stockholders without receipt of any payment in return. They do not

reduce assets or total equity, just the components of equity.

company is doing well.

1. Reasons for a stock dividend

2. Accounting for stock dividends—transfers a portion of equity

from retained earnings to contributed capital (called

capitalizing retained earnings)

a. Small stock dividend is 25% or less of the issuing

corporation’s previously outstanding shares; the market

value of the shares to be distributed is capitalized.

b. Large stock dividend is more than 25% of the shares

outstanding before the dividend; only the legally required

minimum amount (par or stated value of shares) must be

capitalized.

Distributable and credit Common Stock (to transfer par).

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-8

Chapter Outline

Notes

C. Stock Splits

The distribution of additional shares of stock to stockholders

according to their percent of ownership. Involves “calling in” the

outstanding shares of stock and replacing them with a larger

number of shares that have a lower par value.

2. Only a memorandum entry is required.

4. Reverse stock splits reduce number of shares and increase par

value.

IV. Preferred Stock—Has special rights that give it priority over common

stock in one or more areas such as preference for receiving dividends

and for the distribution of assets if the corporation is liquidated.

Usually does not have right to vote.

A. Issuance of Preferred Stock

Usually has a par value; can be sold at a price different from par.

1. Separate contributed capital accounts are used to record

preferred stock.

3. Paid-in in Excess of Par Value, Preferred Stock is used to

record any value received above the par value.

B. Dividend Preference of Preferred Stock

Preferred stockholders are allocated their dividends before any

dividends are allocated to common stockholders. The dividends

allocated per share is usually expressed as a set dollar amount per

share or a percent applied to the par value.

1. Cumulative or Noncumulative Dividend

a. Cumulative preferred stock has a right to be paid both

current and all prior periods’ unpaid dividends before any

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13-9

Chapter Outline

Notes

2. Participating or Nonparticipating Dividend

a. Nonparticipating—dividends are limited each year to a

C. Reasons for Issuing Preferred Stock

1. To raise capital without sacrificing control of the corporation.

2. To boost the return earned by common stockholders on

corporate assets. Called financial leverage or trading on

equity.

V. Treasury Stock—A corporation acquires their own shares for several

reasons such as to acquire another company, or to avoid a hostile

takeover, or to use for employee compensation, or to maintain a strong

market for their stock.

A. Purchasing Treasury Stock—Cost Method

2. Debit Treasury Stock (contra-equity) and credit Cash for full

cost. (Reduces total assets and total equity).

3. The equity reduction is reported by subtracting Treasury Stock

4. Places a restriction on retained earnings.

B. Reissuing Stock

1. Sale at cost—Treasury stock is reduced (credited) for the cost

2. Sale above cost—the amount received in excess of cost is

credited to Paid-in Capital, Treasury Stock.

3. Sale below cost—entry depends on whether the Paid-in

Capital, Treasury Stock account has a balance. If it has no

4. A company ever reports a loss or gain from the sale of

treasury stock.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13–10

Chapter Outline

Notes

VI. Reporting of Equity

A. Statement of Retained Earnings—Retained Earnings is total

cumulative amount of reported net income less any net losses and

dividends declared since the company’s inception. It is part of

stockholders’ equity (claim to the assets) and is not implying that

any certain amount of cash or other assets actually exists.

1. Restrictions and Appropriations

a. Restricted retained earnings refers to both statutory and

2. Prior Period Adjustments

a. Corrections of material errors made in prior periods.

b. Include arithmetic mistakes, unacceptable accounting, and

missed facts.

3. Closing Process

a. Close credit balances in revenue accounts to Income

Summary

B. Statement of Stockholders’ Equity

1. Provided by most companies rather than a separate statement

2. Lists the beginning and ending balances of each equity

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13–11

Chapter Outline

Notes

VII. Decision Analysis

A. Earnings per Share (EPS)

1. Amount of income earned by each share of outstanding

common stock; reported on the income statement.

B. Price-Earnings Ratio (PE ratio)

1. Used to gain understanding of the market’s expected receipts

C. Dividend Yield

1. Used to determine whether a company’s stock is an income

2. Calculated as annual cash dividends per share divided by

market value per share.

D. Book Value per Share—stockholders’ claim to the assets on a per

share basis.

1. Book value per common share

a. If only one class outstanding, equals total stockholders’

equity divided by the number of common shares

2. Equity Applicable to Preferred shares

a. The stockholders’ equity applicable to preferred shares

number of shares outstanding.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13–12

Chapter 13 Alternate Demonstration Problem #1

Uzi Company received a charter granting the right to issue 200,000 shares

of $1 par value common stock and 10,000 shares of 8% cumulative and

nonparticipating, $50 par value preferred stock that is callable at $80 per

share. Selected transactions are presented below.

2017

Feb.

19

Issued 45,000 shares of common stock at par for cash.

22

Gave the corporation’s promoters 30,000 shares of common

stock for their services in getting the corporation organized.

The directors valued the services at $50,000.

Mar

30

Exchanged 100,000 shares of common stock for the

following assets at fair market values: land, $25,000;

building, $100,000; and machinery, $125,000.

Dec.

31

Closed the Income Summary account. A $25,000 loss was

incurred.

2018

Jan.

12

Issued 1,000 shares of preferred stock at $75 per share.

Dec.

15

The board of directors declared an 8% dividend on preferred

shares and $0.10 per share on outstanding common shares,

payable on January 31 to the January 17 stockholders of

record.

31

Closed the Income Summary account. A $69,000 net income

was earned.

2019

Jan.

31

Paid the previously declared dividends.

Required:

1. Prepare general journal entries to record the selected transactions.

2. Prepare a stockholders’ equity section as of the close of business on

December 31, 2018.

3. Determine the book value per preferred share and per common stock

as of December 31, 2018.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13–13

Chapter 13 Solution: Alternate Demonstration Problem #1

Part 1

2017

Feb.

19

Cash …………………………………………………….

45,000

Common Stock ………………………………..

45,000

Mar.

30

Land ……………………………………………………

25,000

Buildings ………………………………………………

Machinery …………………………………………….

Common Stock

Value, Common Stock ………………….

Dec.

31

Retained Earnings …………………………………

25,000

Income Summary …………………………….

25,000

2018

Jan.

12

Cash …………………………………………………….

75,000

Preferred Stock ……………………………….

50,000

Value, Preferred Stock ………………….

25,000

Dec.

15

Retained Earnings …………………………………

21,500

Common Dividend Payable ………………

17,500

Preferred Dividend Payable ……………..

31

Income Summary ………………………………….

69,000

Retained Earnings …………………………...

69,000

2019

Jan.

31

Preferred Dividend Payable …………………..

Common Dividend Payable ……………………

17,500

21,500

22

Organizational Expense ………………………..

50,000

Common Stock ………………………………..

30,000

Value, Common Stock ………………….

20,000

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

Part 2

Stockholders’ Equity

Preferred stock, $50 par value, 8% cumulative and

nonparticipating, 10,000 shares authorized, 1,000

shares issued ………………………………………………………

Common stock, $1 par value, 200,000 shares

authorized, 175,000 issued ……………………………………

Total Paid-in capital …………………………………………………..

Retained earnings ……………………………………………………..

Part 3

Book value per preferred share = call value (or par value if stock does not

have a call value) plus any dividends in arrears if cumulative stock. There

are no arrears.

13–15

Chapter 13 Alternate Demonstration Problem #2

At the beginning of 2017, Austin Corporation’s stockholders’ equity

consisted of the following:

Common stock, $25 par value, 30,000 shares authorized,

24,000 shares issued ……………………………………………………..

$600,000

Paid–In capital in excess of par value common stock ……………

90,000

Retained earnings ……………………………………………………………….

230,000

Total stockholders’ equity ………………………………………………

$920,000

During the year, the company completed these transactions:

June

6

Purchased 1,000 shares of treasury stock at $40 per share.

23

The directors voted a $0.50 per share cash dividend payable

on July 25 to the July 20 stockholders of record.

July

25

Paid the dividend declared on June 23.

Aug.

10

Sold 500 of the treasury shares at $45 per share.

Oct.

20

Sold 500 of the treasury shares at $38 per share.

Dec.

15

The directors voted a $0.50 per share cash dividend payable

on January 20 to the January 15 stockholders of record, and

they voted a 2% stock dividend distributable on January 30 to

the January 20 stockholders of record. The market value of

the stock was $40 per share.

31

Closed the Income Summary account and carried the

company’s $60,000 net income to Retained Earnings.

Required:

1. Prepare general journal entries to record the transactions.

2. Prepare a retained earnings statement for the year and the

stockholders’ equity section of the company’s year-end balance sheet.

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

13–16

Chapter 13 Solution: Alternate Demonstration Problem #2

Part 1

June

6

Treasury Stock, Common ………………………

40,000

Cash ………………………………………………..

40,000

23

Retained Earnings …………………………………

11,500

Common Dividend Payable ………………

11,500

25

Common Dividend Payable ……………………

11,500

Cash ………………………………………………..

11,500

10

22,500

Treasury Stock, Common

20,000

Transactions ………………………………..

20

19,000

Transactions ………………………………..

Treasury Stock, Common …………………

20,000

15

Retained Earnings …………………………………

31,200

Common Dividend Payable ………………

12,000

Common Stock Dividend Distributable.

12,000

Common Stock ………………………………..

31

Income Summary ………………………………….

60,000

Retained Earnings …………………………...

60,000

Wild, Shaw & Chiappetta: Fundamental Accounting Principles, 23rd Edition

Part 2

AUSTIN CORPORATION

Statement of Retained Earnings

For Year Ended December 31, 2017

Retained earnings, January 1, 2017 ……………………

$230,000

Additions:

Deductions:

Cash dividends declared ………………………………

Retained earnings, December 31, 2017 ……………….

$247,300

Stockholders’ Equity

Common stock, $25 par value, 30,000 shares authorized,

24,000 shares issued ………………………………………………….

$600,000

Common stock dividend distributable, 480 shares ……………….

Total common stock issued and to be issued …………………

Total capital paid-in by common stockholders …………

Other Paid-in capital: …………………………………………………………..

Total Paid-in capital ………………………………………………..

Retained earnings ……………………………………………………………….

Total stockholders’ equity ……………………………………….

$958,000