25 Minutes, Easy

a.

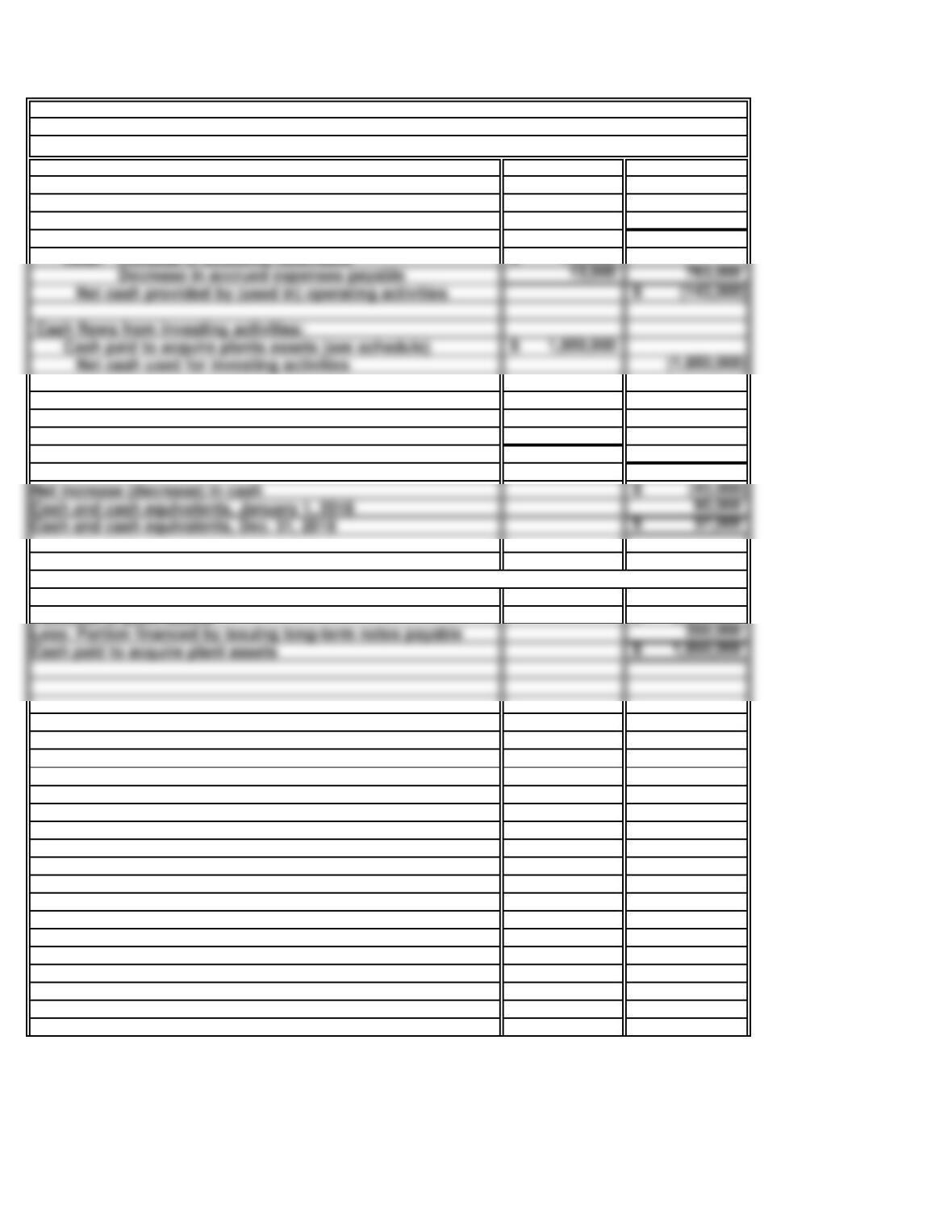

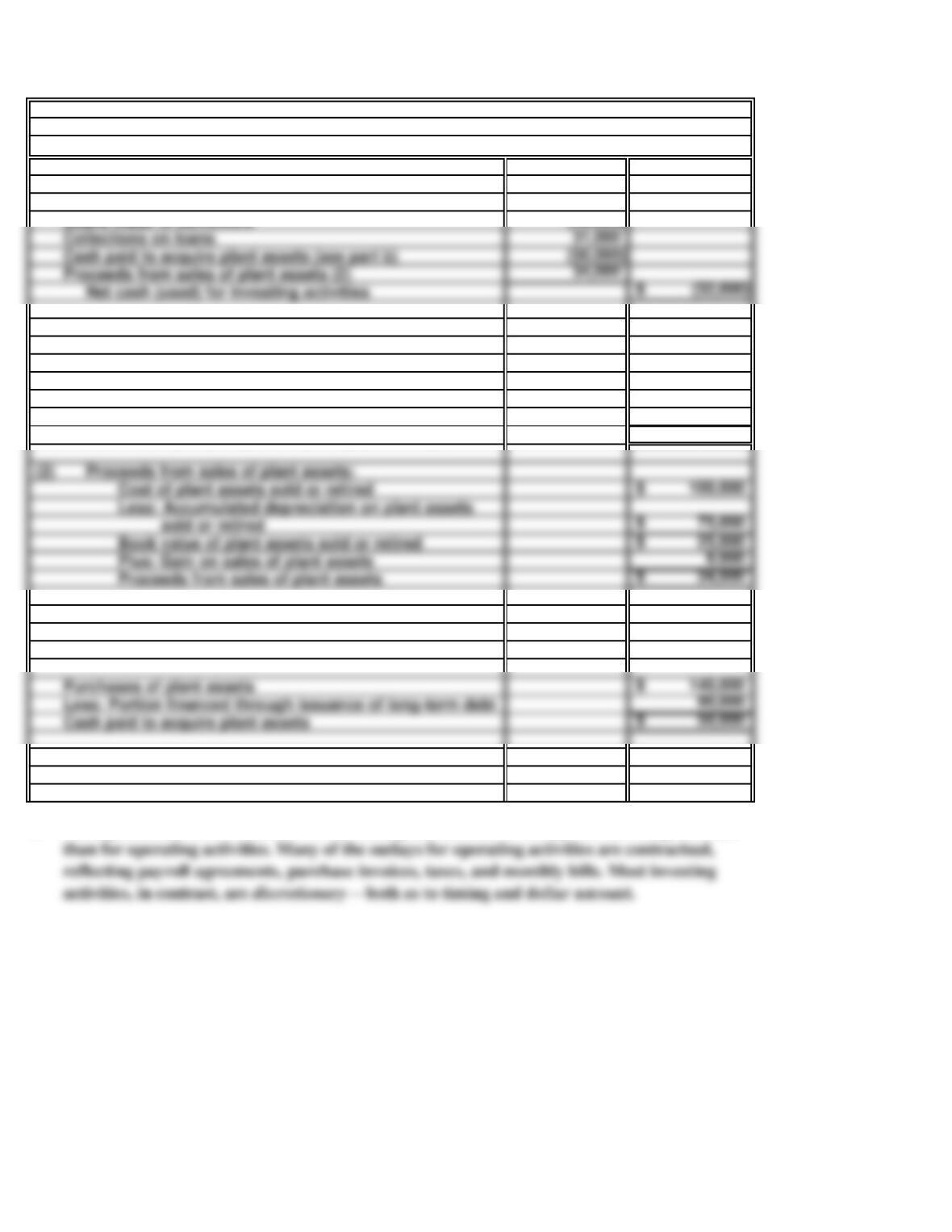

Cash flows from investing activities:

Purchases of marketable securities (75,000)$

Proceeds from sales of marketable securities (1) 132,000

Loans made to borrowers (210,000)

Supporting computations:

(1) Proceeds from sales of marketable securities:

Cost of securities sold (credit entries to

Marketable Securities account) 90,000$

Add: Gain on sales of marketable securities 42,000

Proceeds from sales of marketable securities 132,000$

(2) Proceeds from sales of plant assets:

Cost of plant assets sold or retired 120,000$

Less: Accumulated depreciation on plant assets

sold or retired 75,000

Less: Loss on sales of plant assets 33,000

Proceeds from sales of plant assets 12,000$

Schedule of noncash investing and financing activities:

Purchases of plant assets 196,000$

c.

Cash must be generated to cover the company’s investment needs through operating or

PROBLEM 13.2A

HAMPTON, INC.

For the Year Ended December 31, Current Year

Partial Statement of Cash Flows

HAMPTON, INC.

Collections on loans 162,000

Cash paid to acquire plant assets (see part b) (60,000)

25 Minutes, Easy

a.

Cash flows from investing activities:

Purchases of marketable securities (78,000)$

Proceeds from sales of marketable securities (1) 46,000

Loans made to borrowers (55,000)

Supporting computations:

(1) Proceeds from sales of marketable securities:

Cost of securities sold (credit entries to

Marketable Securities account) 62,000$

Less: Loss on sales of marketable securities 16,000

Proceeds from sales of marketable securities 46,000$

(2) Proceeds from sales of plant assets:

Cost of plant assets sold or retired 140,000$

Less: Accumulated depreciation on plant assets

Add: Gain on sales of plant assets 12,000

Proceeds from sales of plant assets 52,000$

Schedule of noncash investing and financing activities:

Purchases of plant assets 170,000$

c.

Management has more control over the timing and amount of outlays for investing activities

than for operating activities. Many of the outlays for operating activities are contractual,

PROBLEM 13.3A

HOLMES EXPORT CO.

For the Year Ended December 31, Current Year

Partial Statement of Cash Flows

HOLMES EXPORT CO.

Collections on loans 62,000

Cash paid to acquire plant assets (see part b) (60,000)

30 Minutes, Medium

a.

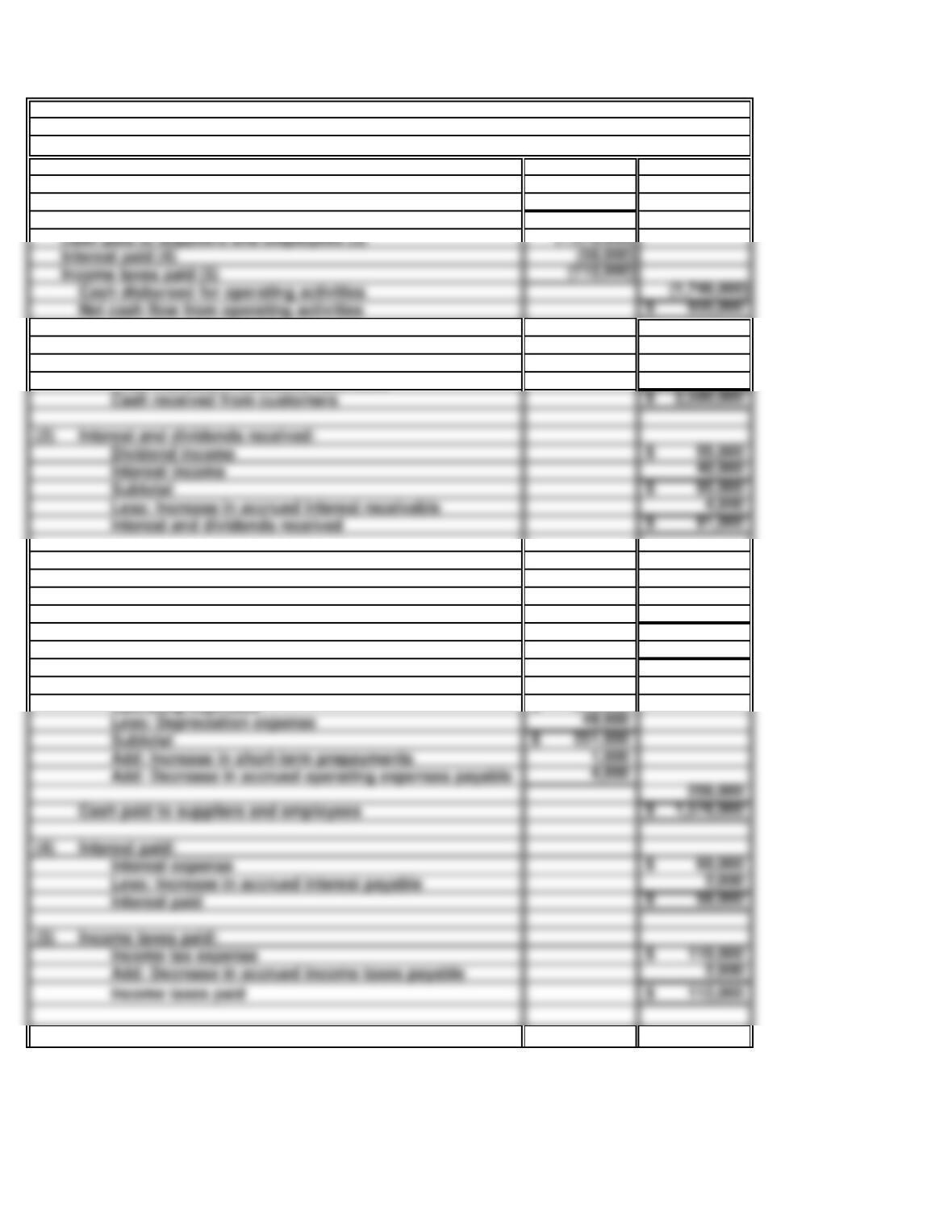

Cash flows from operating activities:

Cash received from customers (1) 2,920,000$

Interest and dividends received (2) 171,000

Cash provided by operating activities 3,091,000$

(1) Cash received from customers:

Net sales 2,850,000$

Add: Decrease in accounts receivable 70,000

Cash received from customers 2,920,000$

(2) Interest and dividends received:

Dividend income (cash basis) 104,000$

Interest income 70,000

Subtotal 174,000$

Less: Increase in accrued interest receivable 3,000

Interest and dividends received 171,000$

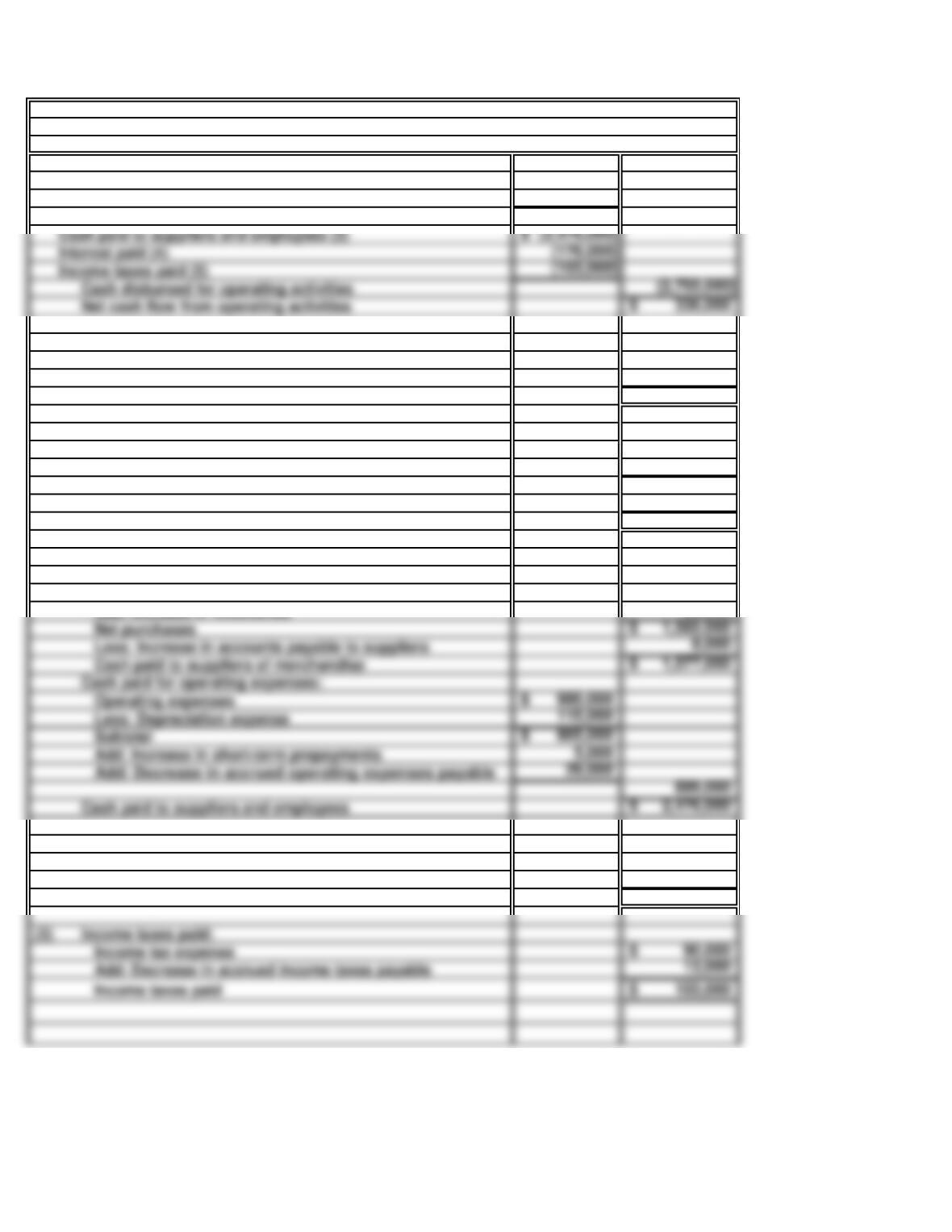

(3) Cash paid to suppliers and employees:

Cost of goods sold 1,550,000$

Add: Increase in inventories 35,000

Net purchases 1,585,000$

Cash paid to suppliers of merchandise 1,577,000$

Operating expenses 980,000$

Less: Depreciation expense 115,000

Add: Increase in short-term prepayments 5,000

Cash paid for operating expenses:

Cash paid to suppliers and employees

(4) Interest paid:

Interest expense 185,000$

Less: Increase in accrued interest payable 9,000

Interest paid 176,000$

(5) Income taxes paid:

Income tax expense 90,000$

Add: Decrease in accrued income taxes payable 13,000

Cash paid to suppliers of merchandise:

PROBLEM 13.4A

TREECE, INC.

For the Year Ended December 31, 2018

Partial Statement of Cash Flows

TREECE, INC.

Interest paid (4) (176,000)

Income taxes paid (5) (103,000)

Net cash flow from operating activities 336,000$

PROBLEM 13.4A

TREECE, INC. (concluded)

b.

In addition to more aggressive collection of accounts receivable, management could increase

cash flows from operations by (only two required):

25 Minutes, Medium

Cash flows from operating activities:

Net income 223,000$

Add: Depreciation expense 115,000$

Decrease in accounts receivable 70,000

Increase in accounts payable to suppliers 8,000

PROBLEM 13.5A

TREECE, INC.

For the Year Ended December 31, 2018

Partial Statement of Cash Flows

TREECE, INC. (INDIRECT)

Less: Increase in accrued interest receivable 3,000$

Increase in inventories 35,000

Increase in short-term prepayments 5,000

45 Minutes, Strong

a.

Cash flows from operating activities:

Cash received from customers (1) 3,140,000$

Interest received (2) 42,000

Cash provided by operating activities 3,182,000

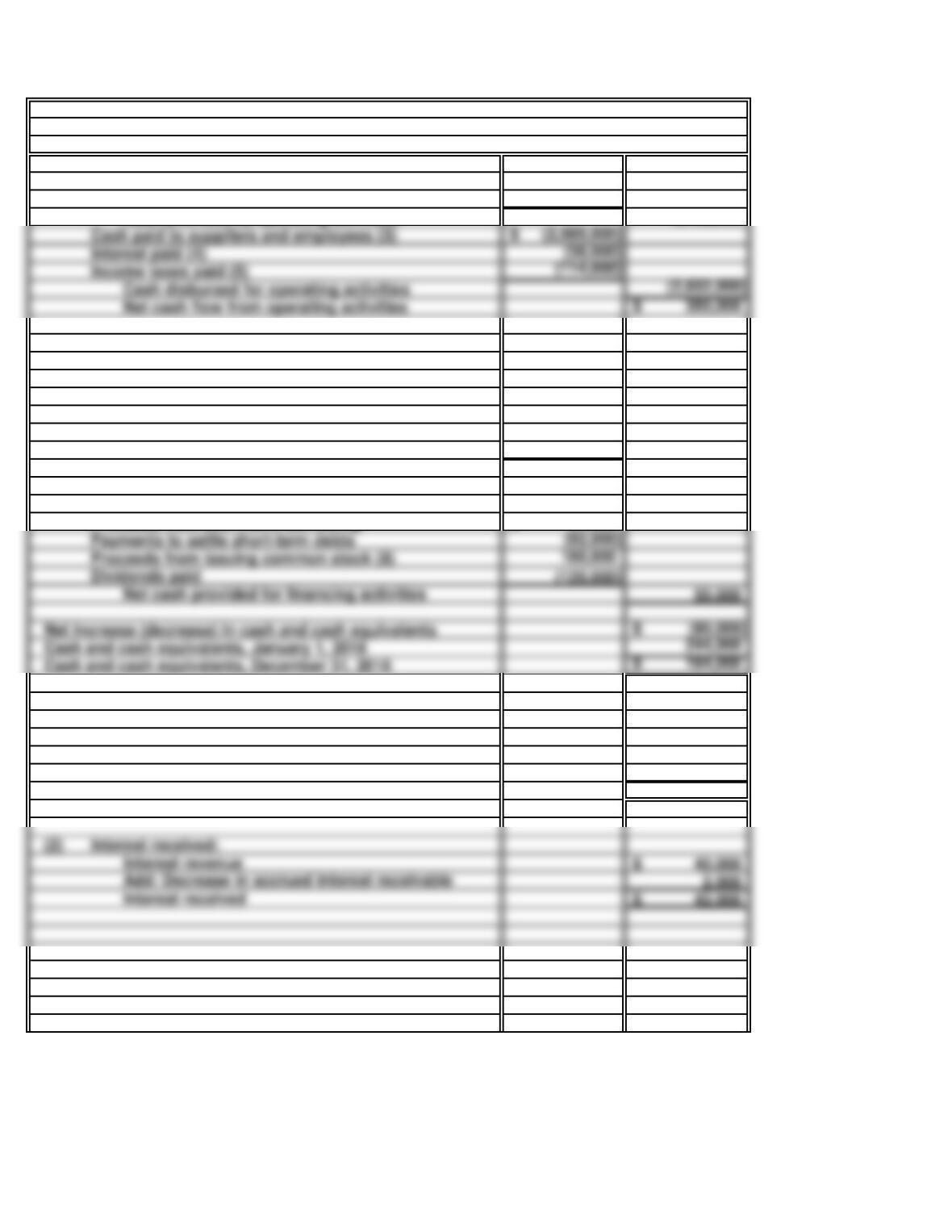

Cash flows from investing activities:

Purchases of marketable securities (60,000)$

Proceeds from sales of marketable securities (6) 72,000

Loans made to borrowers (44,000)

Collections on loans 28,000

Cash paid to acquire plant assets (500,000)

Proceeds from sales of plant assets (7) 24,000

Net cash used in investing activities: (480,000)

Cash flows from financing activities:

Proceeds from short-term borrowing 82,000$

Payments to settle short-term debts (92,000)

Proceeds from issuing common stock (8) 180,000

Net cash provided for financing activities 50,000

Net increase (decrease) in cash and cash equivalents (80,000)$

Supporting computations:

(1)

Net sales 3,200,000$

Less: increase in accounts receivable 60,000

Cash received from customers 3,140,000$

(2) Interest received:

Interest received 42,000$

Cash received from customers:

PROBLEM 13.6A

21st CENTURY TECHNOLOGIES

For the Year Ended December 31, 2018

Statement of Cash Flows

21st CENTURY TECHNOLOGIES

Cash paid to suppliers and employees (3) (2,680,000)$

Interest paid (4) (38,000)

Income taxes paid (5) (114,000)

Net cash flow from operating activities 350,000$

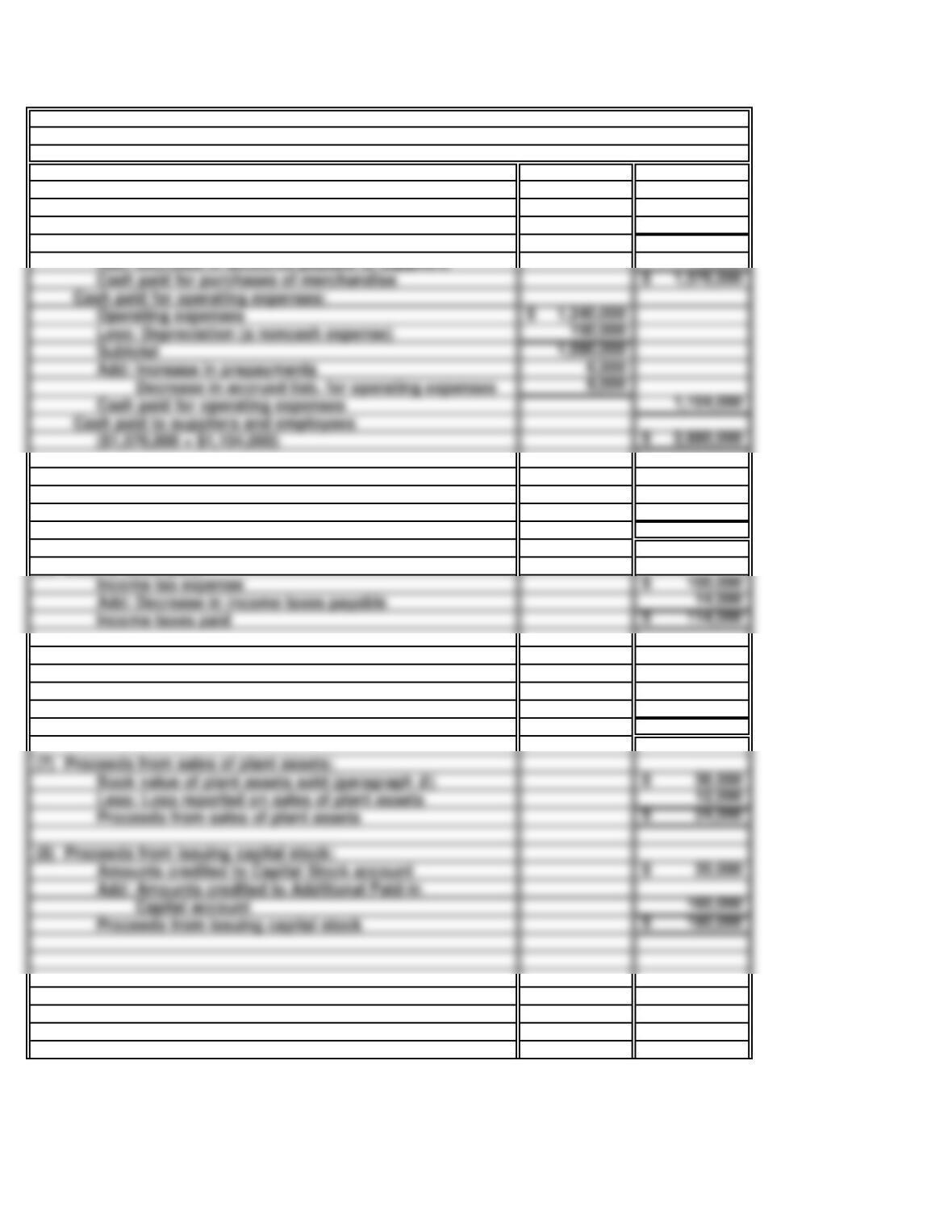

(3) Cash paid to suppliers and employees:

Cost of goods sold 1,620,000$

Less: Decrease in inventory 60,000

Net purchases 1,560,000

Add: Decrease in accounts payable to suppliers 16,000

(4) Interest paid:

Interest expense 42,000$

Less: Increase in accrued interest payable 4,000

Interest paid 38,000$

(5) Income taxes paid:

Income tax expense 100,000$

Add: Decrease in income taxes payable 14,000

Income taxes paid 114,000$

(6) Proceeds from sales of marketable securities:

Cost of marketable securities sold (credit entries

to the Marketable Securities account) 38,000$

Add: Gain reported on sales of marketable securities 34,000

Proceeds from sales of marketable securities 72,000$

(7) Proceeds from sales of plant assets:

Less: Loss reported on sales of plant assets 12,000

Proceeds from sales of plant assets 24,000$

(8) Proceeds from issuing capital stock:

Amounts credited to Capital Stock account 20,000$

Proceeds from issuing capital stock 180,000$

Cash paid for purchases of merchandise:

PROBLEM 13.6A

21st CENTURY TECHNOLOGIES

(continued)

a.

Operating expenses 1,240,000$

Less: Depreciation (a noncash expense) 150,000

Cash paid for operating expenses 1,104,000

($1,576,000 + $1,104,000) 2,680,000$

b. (1)

c.

To the extent that receivables increase, the company has not yet collected cash from its

PROBLEM 13.6A

21st CENTURY TECHNOLOGIES (concluded)

The primary reason why cash provided by operating activities substantially exceeded net

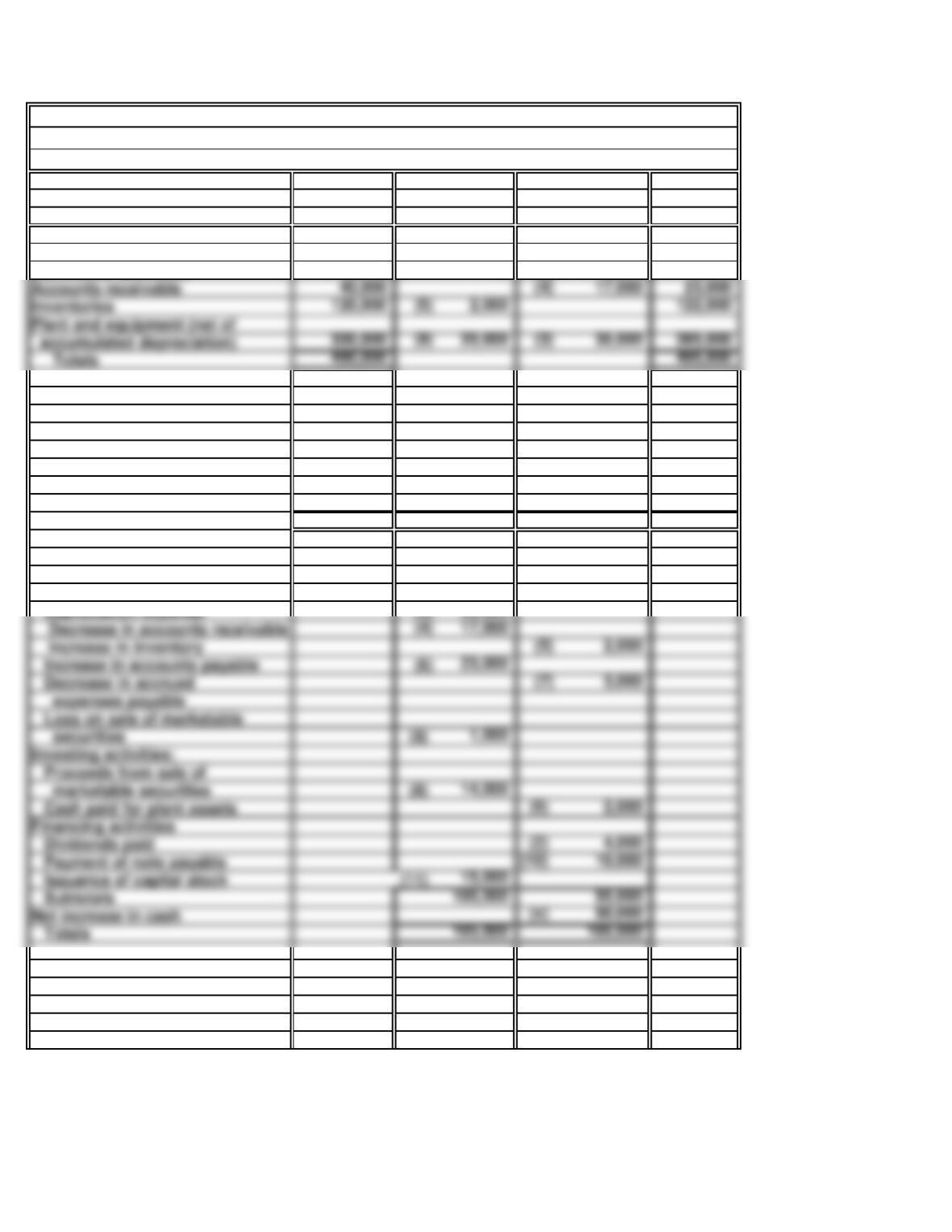

60 Minutes, Strong

a.

Balance sheet effects:

Beginning Ending

Balance Balance

Cash and cash equivalents 80,000

(x)

43,000 37,000

Accounts receivable 100,000 (3) 750,000 850,000

Cash effects:

Operating activities:

Net income (1) 440,000

Depreciation expense (2) 147,000

Increase in accounts receivable (3) 750,000

Increase in accounts payable (4) 33,000

Decrease in accrued

13,000

Investing activities:

Cash paid for plant assets

Financing activities:

Short-term borrowing

Issuance of capital stock

Subtotals 2,570,000 2,613,000

Net decrease in cash

PROBLEM 13.7A

Changes

Credit

Changes

Effect of Transactions

SATELLITE WORLD

Sources

Uses

SATELLITE WORLD

Worksheet for a Statement of Cash Flows

For the Year Ended December 31, 2018

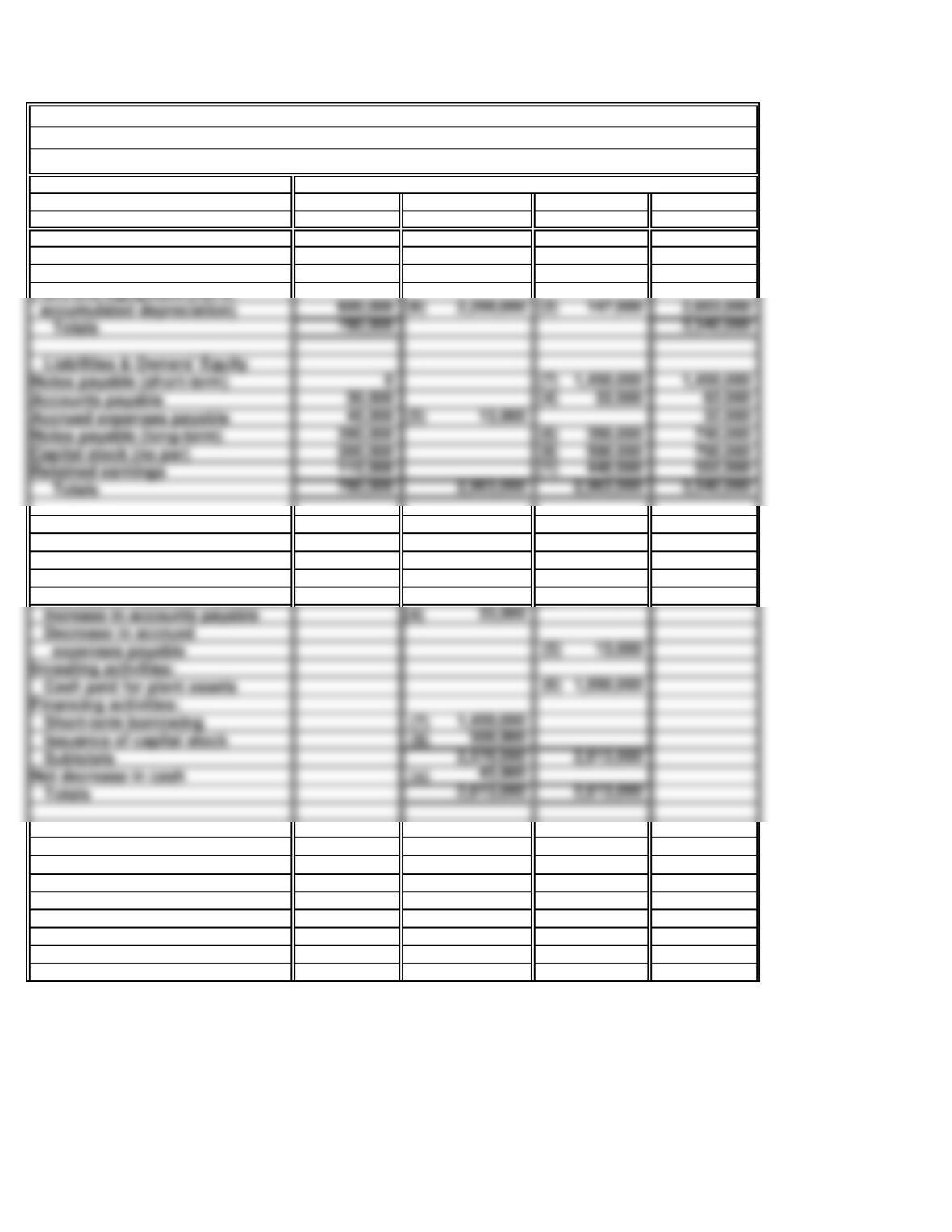

Assets

Debit

Plant and equipment (net of

Liabilities & Owners’ Equity

Notes payable (short-term) 0 (7) 1,450,000 1,450,000

Accounts payable 30,000 (4) 33,000 63,000

Accrued expenses payable 45,000 (5) 13,000 32,000

Notes payable (long-term) 390,000 (6) 350,000 740,000

Capital stock (no par) 200,000 (8) 500,000 700,000

b.

Cash flows from operating activities:

Net income 440,000$

Add: Depreciation expense 147,000

Increase in accounts payable 33,000

Subtotal 620,000$

Less: Increase in accounts receivable 750,000$

Cash flows from financing activities:

Short-term borrowing from bank 1,450,000$

Issuance of capital stock 500,000

Net cash provided by financing activities 1,950,000

Purchase of plant assets 2,200,000$

Supplementary Schedule: Noncash Investing and Financing Activities

PROBLEM 13.7A

SATELLITE WORLD

For the Year Ended December 31, 2018

Statement of Cash Flows

SATELLITE WORLD (continued)

Decrease in accrued expenses payable 13,000 763,000

Net cash provided by (used in) operating activities (143,000)$

Cash flows from investing activities:

Cash paid to acquire plants assets (see schedule) 1,850,000$

Net cash used for investing activities (1,850,000)

c.

d.

Satellite World does not appear headed for insolvency. First, the company has a $5.5

PROBLEM 13.7A

SATELLITE WORLD (concluded)

Satellite World’s credit sales resulted in $750,000 in new receivables, which were

uncollected as of year-end. These credit sales all were included in the computation of net

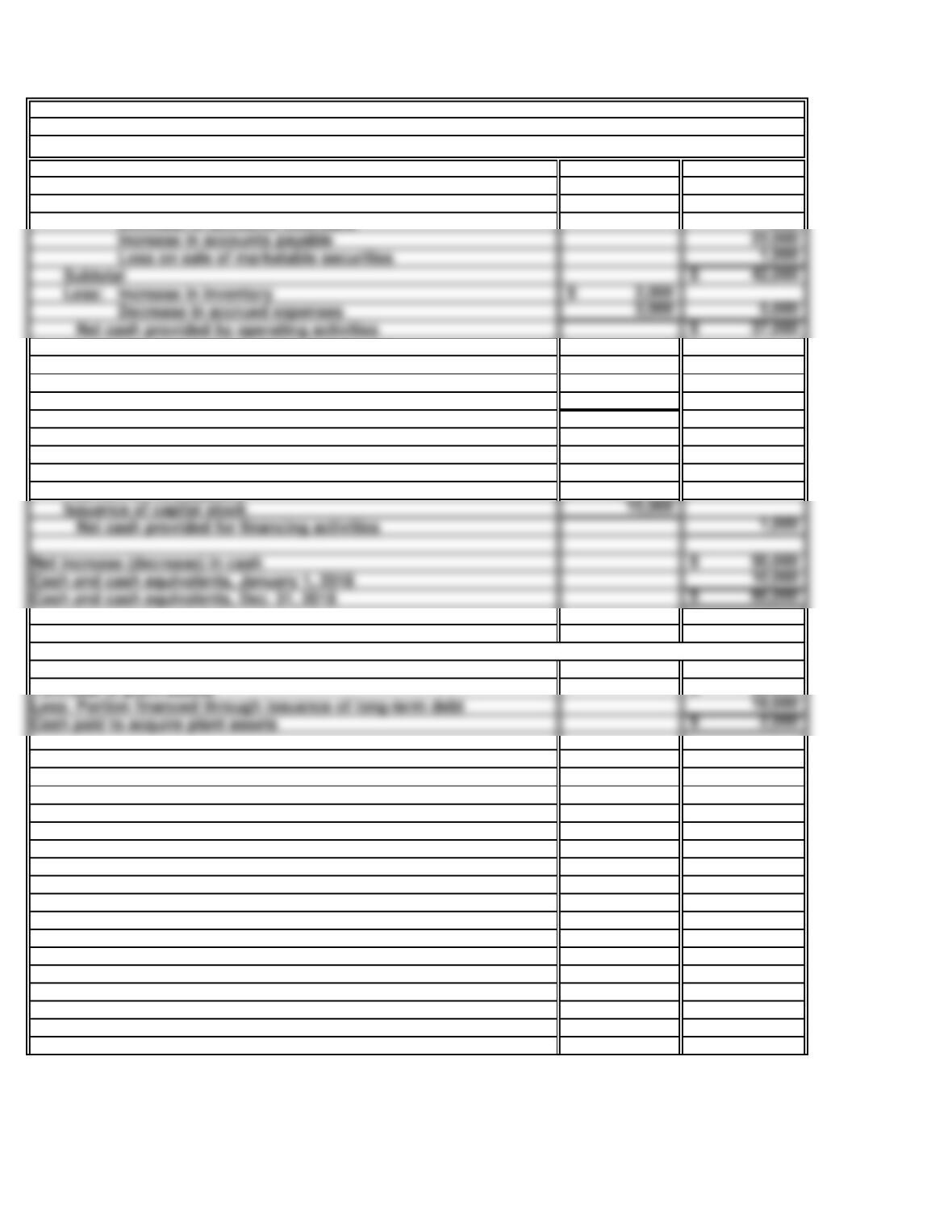

60 Minutes, Strong

a.

Balance sheet effects:

Beginning Ending

Balance Balance

Cash and cash equivalents 10,000 (x) 50,000 60,000

Marketable securities 20,000 (8) 15,000 5,000

Liabilities & Owners’ Equity

Accounts payable 50,000 (6) 23,000 73,000

Accrued expenses payable 17,000 (7) 3,000 14,000

Notes payable 245,000 (10) 10,000 (9) 18,000 253,000

Capital stock 120,000 (11) 15,000 135,000

Retained earnings 58,000 (1) 34,000 20,000

(2) 4,000

Totals 490,000 123,000 123,000 495,000

Cash effects:

Operating activities:

Net loss (1) 34,000

Depreciation expense (3) 35,000

Decrease in accounts receivable (4) 17,000

Increase in inventory (5) 2,000

Increase in accounts payable

Decrease in accrued (7) 3,000

Loss on sale of marketable

Investing activities:

Proceeds from sale of

marketable securities (8) 14,000

Cash paid for plant assets (9) 2,000

Financing activities

Dividends paid (2) 4,000

Payment of note payable

Issuance of capital stock (11) 15,000

Subtotals 105,000 55,000

Net increase in cash (x) 50,000

Totals 105,000 105,000

Sources

Uses

MIRACLE TOOL, INC.

Worksheet for a Statement of Cash Flows

For the Year Ended December 31, 2018

Assets

Debit

PROBLEM 13.8A

Changes

Credit

Changes

MIRACLE TOOL, INC.

Accounts receivable 40,000 (4) 17,000 23,000

Plant and equipment (net of

accumulated depreciation) 300,000 (9) 20,000 (3) 35,000 285,000

Totals 490,000 495,000

b.

Cash flows from operating activities:

Net loss (34,000)$

Add: Depreciation expense 35,000

Decrease in accounts receivable 17,000

Cash flows from investing activities:

Proceeds from sale of marketable securities 14,000$

Cash paid to acquire plants assets (see supplementary schedule) (2,000)

Net cash used in investing activities 12,000

Cash flows from financing activities:

Dividends paid (4,000)$

Payment of note payable (10,000)

Issuance of capital stock 15,000

Net cash provided for financing activities 1,000

Purchase of plant assets 20,000$

Supplementary Schedule: Noncash Investing and Financing Activities

PROBLEM 13.8A

MIRACLE TOOL, INC.

For the Year Ended December 31, 2018

Statement of Cash Flows

MIRACLE TOOL, INC. (continued)

Increase in accounts payable 23,000

Less: Increase in inventory 2,000$

Net cash provided by operating activities 37,000$

c.

d.

e.

f.

The company’s principal revenue source—sales of tools—is declining. If nothing is done, it

is likely that the annual net losses will increase, and that operating cash flows will turn

PROBLEM 13.8A

MIRACLE TOOL, INC. (continued)

This company is contracting its operations. Its investment in marketable securities,

Miracle Tool, Inc. has substantially more cash than it did a year ago. Nonetheless, the

Miracle Tool, Inc. achieved its positive cash flow from operating activities basically by

liquidating assets and by not paying its bills. It has converted most of its accounts

•

PROBLEM 13.8A

MIRACLE TOOL, INC. (concluded)

If management decides to continue business operations, it should consider taking the following

actions:

Expand the company’s product lines! The combination tool alone can no longer support

profitable operations. Also, dependency upon a single product—especially a faddish

•

•

•

•

improve profitability, but will help cash flows. (As explained above, the company’s current

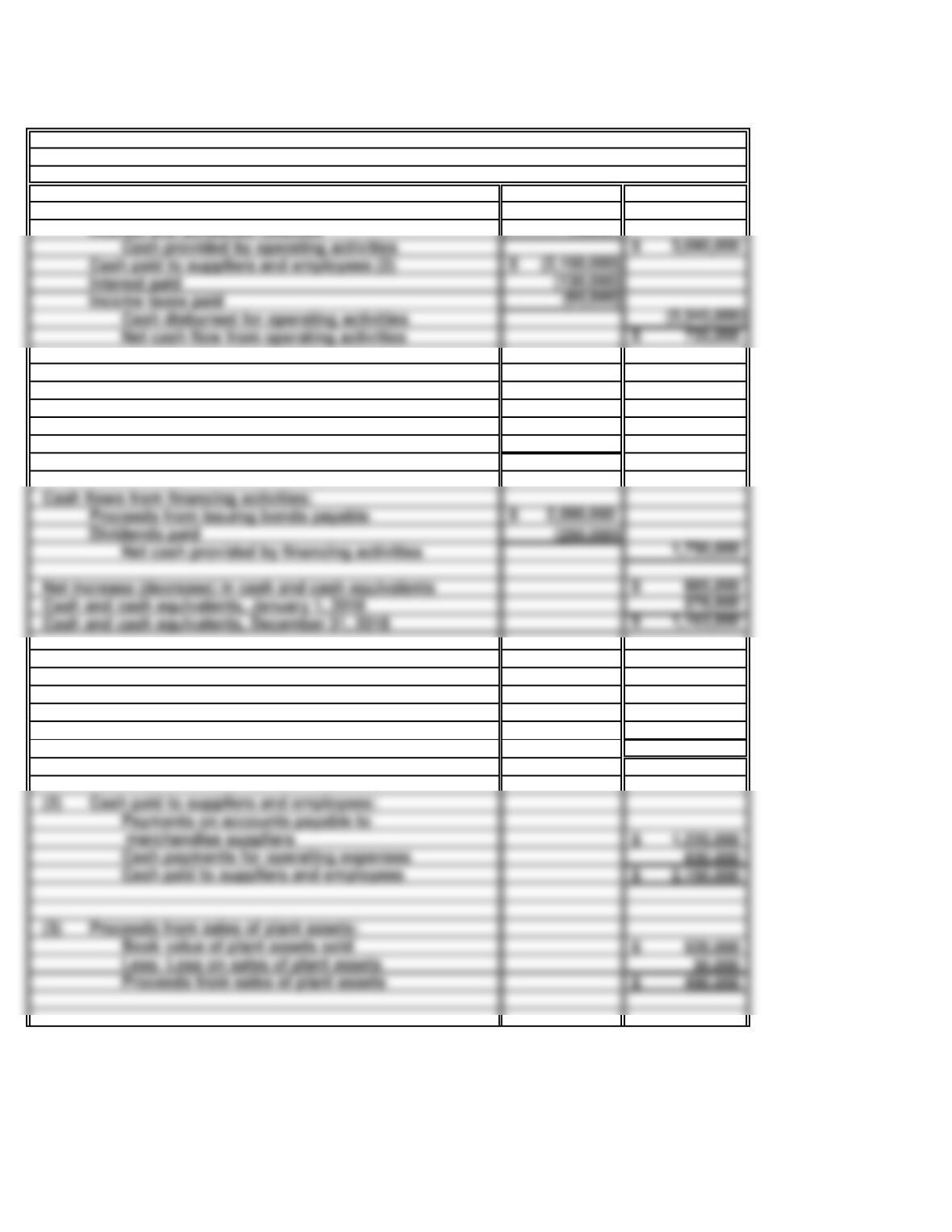

30 Minutes, Medium

a.

Cash flows from operating activities:

Cash received from customers (1) 3,040,000$

Interest and dividends received 40,000

Cash flows from investing activities:

Loans made to borrowers (690,000)$

Collections on loans 300,000

Cash paid to acquire plant assets (1,700,000)

Proceeds from sales of plant assets (3) 490,000

Net cash used for investing activities: (1,600,000)

Proceeds from issuing bonds payable 2,000,000$

Supporting computations:

(1)

Cash sales 230,000$

Collections on accounts receivable 2,810,000

Cash received from customers 3,040,000$

(2) Cash paid to suppliers and employees:

Cash payments for operating expenses 930,000

Cash paid to suppliers and employees 2,150,000$

(3) Proceeds from sales of plant assets:

Book value of plant assets sold 520,000$

Less: Loss on sales of plant assets 30,000

Proceeds from sales of plant assets 490,000$

SOLUTIONS TO PROBLEM SET B

Note to instructor: The transfer from the money market fund to the general bank account is not

considered a cash receipt because a money market fund is a cash equivalent.

Cash received from customers:

PROBLEM 13.1B

WELCH COMPANY

For the Year Ended December 31, Current Year

Statement of Cash Flows

WELCH COMPANY

Cash paid to suppliers and employees (2) (2,150,000)$

Interest paid (130,000)

Income taxes paid (65,000)

Net cash flow from operating activities 735,000$

25 Minutes, Easy

a.

Cash flows from investing activities:

Purchases of marketable securities (65,000)$

Proceeds from sales of marketable securities (1) 89,000

Supporting computations:

(1) Proceeds from sales of marketable securities:

Cost of securities sold (credit entries to

Marketable Securities account) 74,000$

Add: Gain on sales of marketable securities 15,000

Proceeds from sales of marketable securities 89,000$

(2) Proceeds from sales of plant assets:

Cost of plant assets sold or retired 150,000$

Less: Accumulated depreciation on plant assets

Less: Loss on sales of plant assets 10,000

Proceeds from sales of plant assets 80,000$

b.

Schedule of noncash investing and financing activities:

Purchases of plant assets 245,000$

Less: Portion financed through issuance of long-term debt 160,000

Cash paid to acquire plant assets 85,000$

c.

Cash must be generated to cover the company’s investment needs through operating or financing

PROBLEM 13.2B

MARY’S FASHIONS

For the Year Ended December 31, Current Year

Partial Statement of Cash Flows

MARY’S FASHIONS

Loans made to borrowers (175,000)

Collections on loans 50,000

Cash paid to acquire plant assets (see part b) (85,000)

Proceeds from sales of plant assets (2) 80,000

25 Minutes, Easy

a.

Cash flows from investing activities:

Purchases of marketable securities (59,000)$

Proceeds from sales of marketable securities (1) 52,000

Supporting computations:

(1) Proceeds from sales of marketable securities:

Cost of securities sold (credit entries to

Marketable Securities account) 60,000$

Less: Loss on sales of marketable securities 8,000

Proceeds from sales of marketable securities 52,000$

(2) Proceeds from sales of plant assets:

Cost of plant assets sold or retired 100,000$

Less: Accumulated depreciation on plant assets

Plus: Gain on sales of plant assets 9,000

Proceeds from sales of plant assets 34,000$

b.

Schedule of noncash investing and financing activities:

c.

Management has more control over the timing and amount of outlays for investing activities

PROBLEM 13.3B

RPZ IMPORTS

For the Year Ended December 31, Current Year

Partial Statement of Cash Flows

RPZ IMPORTS

Loans made to borrowers (40,000)

Collections on loans 31,000

30 Minutes, Medium

a.

Cash flows from operating activities:

Cash received from customers (1) 2,590,000$

Interest and dividends received (2) 91,000

Cash provided by operating activities 2,681,000$

(1) Cash received from customers:

Net sales 2,600,000$

Less: Increase in accounts receivable 10,000

Cash received from customers 2,590,000$

(2) Interest and dividends received:

Dividend income 55,000$

Interest income 40,000

Less: Increase in accrued interest receivable 4,000

Interest and dividends received 91,000$

(3) Cash paid to suppliers and employees:

Cost of goods sold 1,300,000$

Add: Increase in inventories 25,000

Net purchases 1,325,000$

Less: Increase in accounts payable to suppliers 5,000

Cash paid to suppliers of merchandise 1,320,000$

Operating expenses 300,000$

Less: Depreciation expense 49,000

Add: Increase in short-term prepayments 1,000

Add: Decrease in accrued operating expenses payable 4,000

(4) Interest paid:

Interest expense 60,000$

Less: Increase in accrued interest payable 2,000

Interest paid 58,000$

(5) Income taxes paid:

Income tax expense 110,000$

Add: Decrease in accrued income taxes payable 2,000

Cash paid to suppliers and employees

Cash paid to suppliers of merchandise:

Cash paid for operating expenses:

PROBLEM 13.4B

ROYCE INTERIORS, INC.

For the Year Ended December 31, 2018

Partial Statement of Cash Flows

ROYCE INTERIORS, INC.

Cash paid to suppliers and employees (3) (1,576,000)

Income taxes paid (5) (112,000)

PROBLEM 13.4B

ROYCE INTERIORS, INC. (concluded)

b.

Management could increase cash flows from operations by (only two required):

Reducing the amount of inventories being held.

More aggressive collection of accounts receivable.

Reducing the amount of short-term prepayments of expenses.