Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

1. Always use references to assumption cells in the formulas. For example, the cash sales row formulas should be that column’s sales times cell

D6 (e.g., in February, cash sales cell has this formula: =E19*$D$6

4. Tentative cash balance = beginning balance + cash sales that month + collections of prior month’s cash sales – current expenditures:

=D18+D20+D21-D22

5. Amount borrowed = zero if tentative balance >= desired balance, otherwise the amount of the shortfall: =IF(D23>=D24,0,(D24-D23))

7. Loan repayment is calculated as the excess of cash available over desired ending balance, but never more than the amount of the loan.

Ch 13: Expenditure Cycle

Problem 13-6 continued

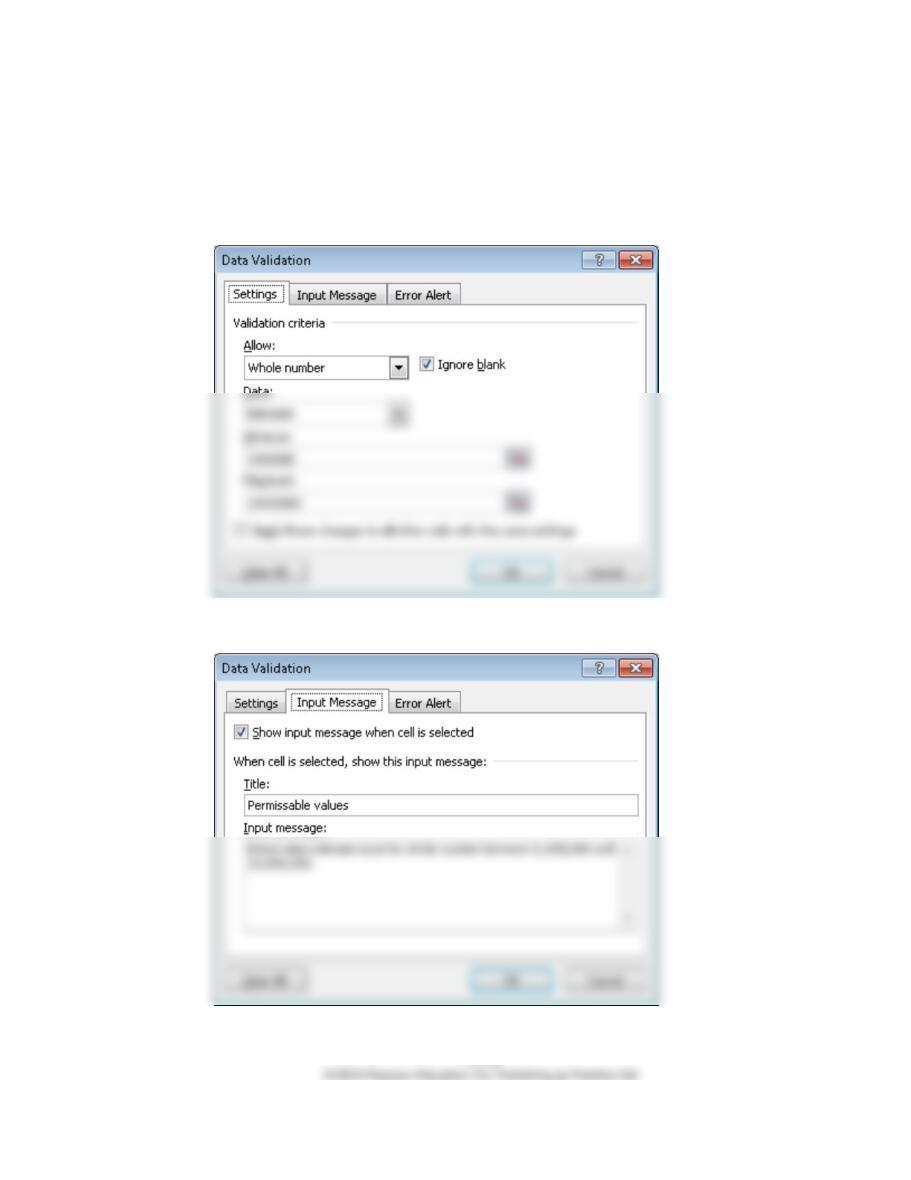

f. Add appropriate data validation controls to ensure spreadsheet accuracy.

The solutions manual for chapter 10 discussed data validation controls in detail. Possible

solutions include the following:

1. Limit initial sales to the range $1,000,000 - $10,000,000

Also, include an appropriate input message:

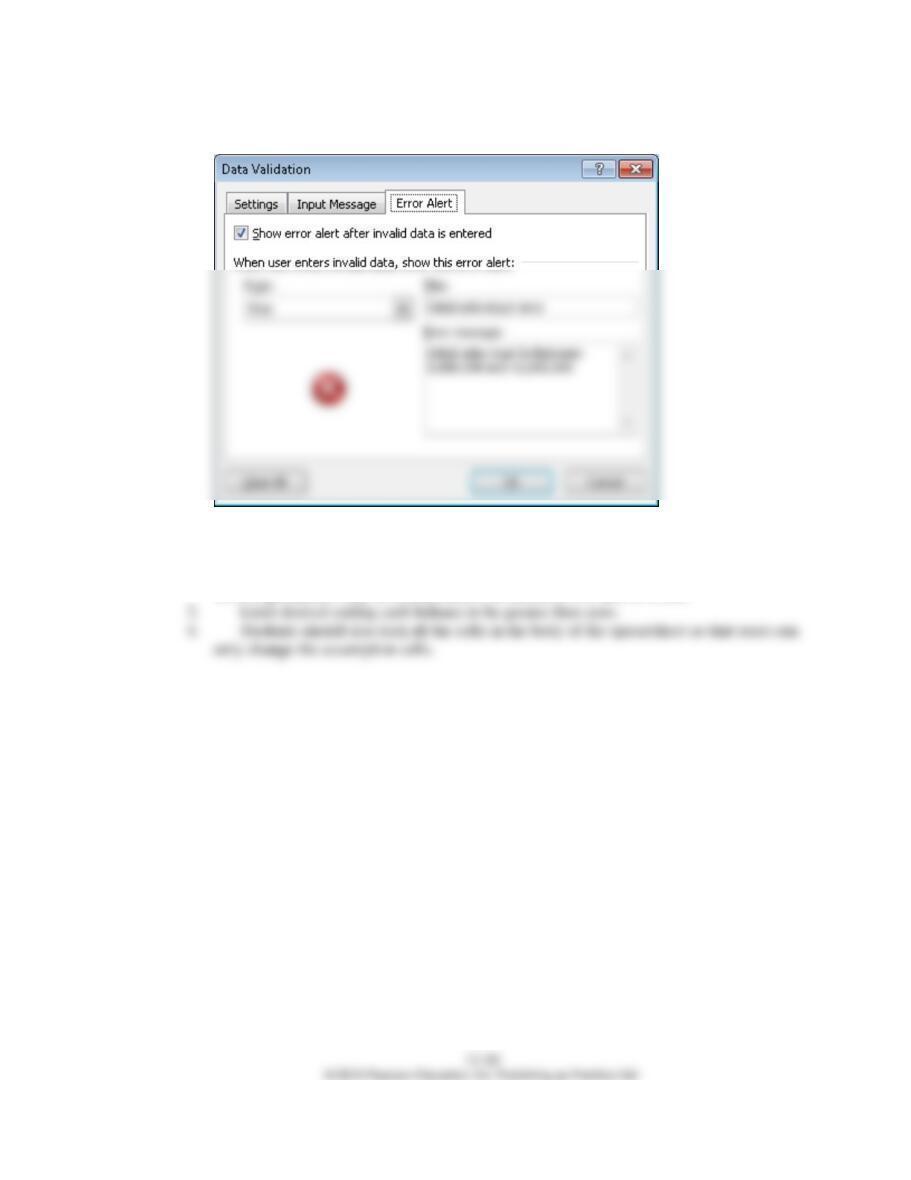

And an appropriate error message:

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

2. Limit the sales growth, the percentage of sales made for cash, the percentages collected in

subsequent months, the percentage never collected, and expenditures as a percentage of sales

to reasonable ranges. For example, sales growth may be constrained to be between 1% and

10%; expenditures may be constrained to be between 50% and 90%, etc.

Ch 13: Expenditure Cycle

13.7 For each of the following activities, identify the data that must be entered by the

employee performing that activity and list the appropriate data entry controls:

a. Purchasing agent generating a purchase order

Data that must be entered

Appropriate Data Entry Edit Controls

User ID

Validity check

Compatibility test (is user authorized to perform this task?)

Password

Validity check

Compatibility test (is user authorized to perform this task?)

Notes:

1. All other fields on the sample purchase order (see Figure 13-5) can be completed by

the system.

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

b. Receiving clerk completing a receiving report

Data that must be entered

Appropriate Data Entry Edit Controls

User ID

Validity check

Compatibility test (is user authorized to perform this task?)

Password

Validity check

Compatibility test (is user authorized to perform this task?)

Supplier name

Choose from pull-down list of approved suppliers

Purchase Order number

Choose from pull-down list of open purchase orders from

that supplier

Notes:

1. All other fields on the sample receiving report (see Figure 13-6) can be completed by

the system.

Ch 13: Expenditure Cycle

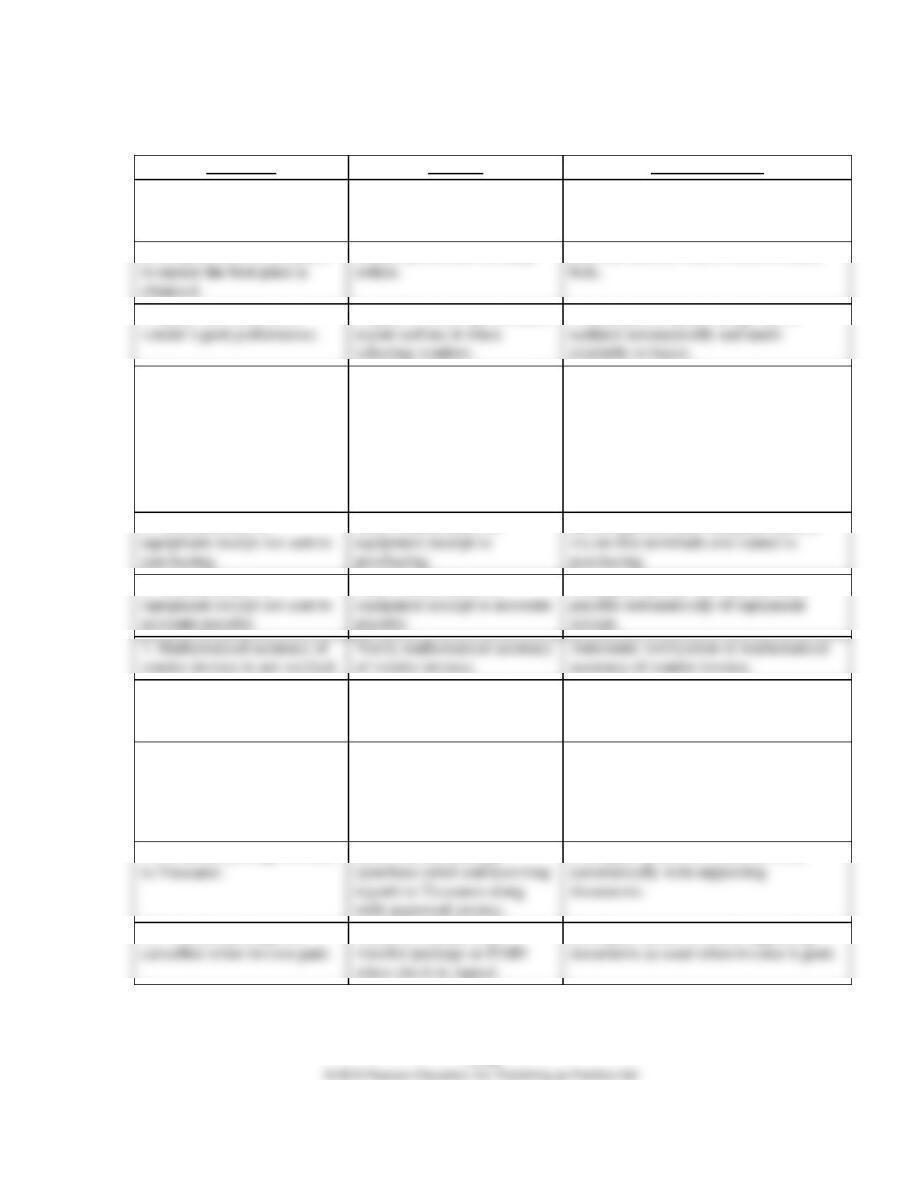

13.8 The following list identifies several important control features. For each control, (1)

describe its purpose and (2) explain how it could be best implemented in an

integrated ERP system.

a. Cancellation of the voucher package by the cashier after signing the check

b. Separation of duties of approving invoices for payment and signing checks

Item

Part I - Purpose

Part II – ERP System Control

a.

Prevent resubmission of invoices

for double payment

Control field in supplier invoice record to indicate

the document has been used

Control field in purchase order and receiving report

records to indicate the document has been used to

d.

Verify the accuracy of recorded

amounts and detect losses.

Still need to count physical inventory periodically.

e.

Prevent large disbursements for

questionable reasons.

Still need two signatures.

f.

Verifies that items received were

placed in inventory and were not

stolen.

Receiving clerks enter that goods were transferred to

inventory.

Inventory clerks acknowledge receipt of goods via

terminals. System configured so that voucher

package requires that the receiving report include the

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

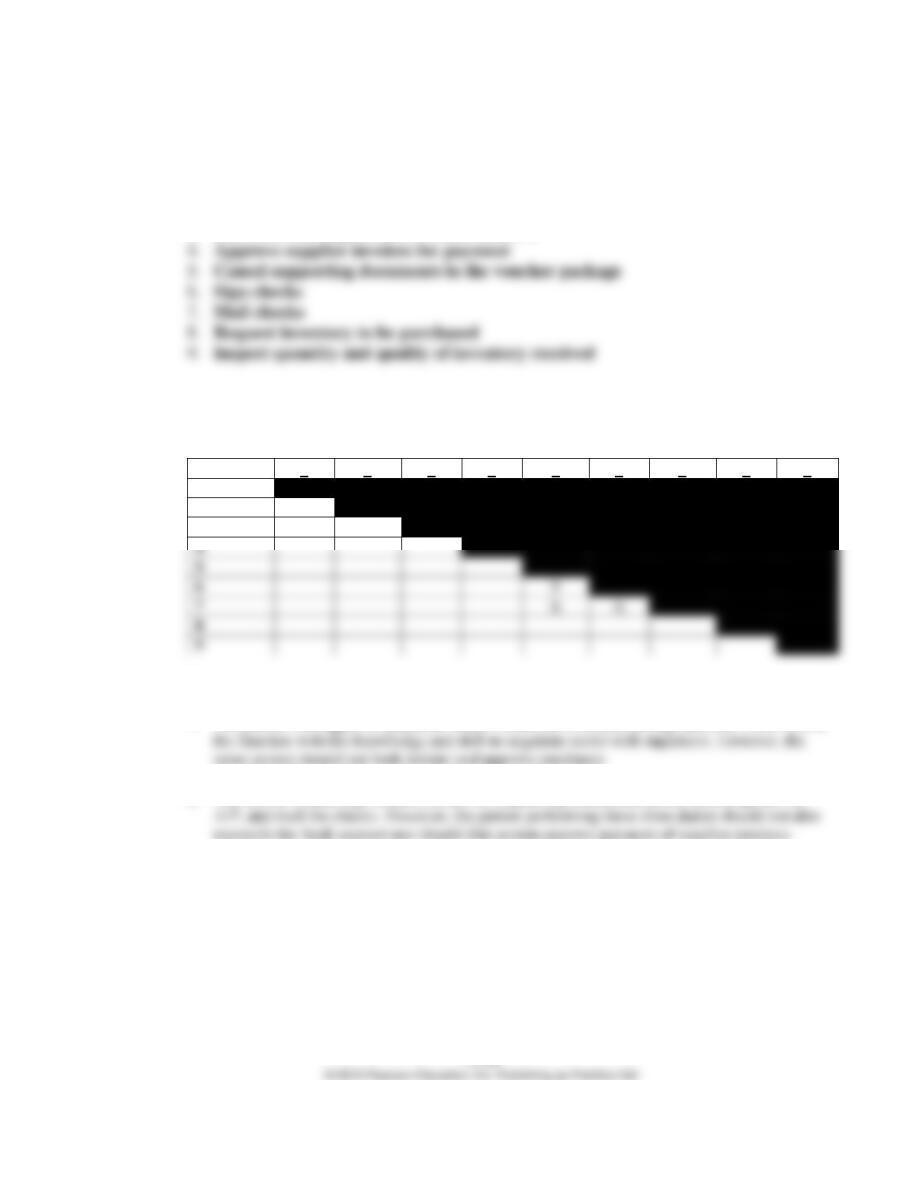

13.9 For good internal control, which of the following duties can be performed by the

same individual?

1. Approve purchase orders

2. Negotiate terms with suppliers

3. Reconcile the organization’s bank account

The cells in the following table marked with an X indicate duties that can be performed by the

same individual without creating an internal control weakness:

Duty

1

2

3

4

5

6

7

8

9

1

2

X

3

Rationale:

1. The person who approves purchase orders should be in the purchasing function, which is also

2. The cashier should sign checks, cancel the supporting documents before returning them to

Ch 13: Expenditure Cycle

13.10 Last year the Diamond Manufacturing Company purchased over $10 million worth

of office equipment under its “special ordering” system, with individual orders

ranging from $5,000 to $30,000. Special orders are for low-volume items that have

been included in a department manager’s budget. The budget, which limits the

types and dollar amounts of office equipment a department head can requisition, is

approved at the beginning of the year by the board of directors. The special

ordering system functions as follows:

Purchasing A purchase requisition form is prepared and sent to the purchasing

department. Upon receiving a purchase requisition, one of the five purchasing

Receiving The receiving department gets a copy of each purchase order. When

equipment is received, that copy of the purchase order is stamped with the date and,

if applicable, any differences between the quantity ordered and the quantity

received are noted in red ink. The receiving clerk then forwards the stamped

purchase order and equipment to the requisitioning department head and verbally

notifies the purchasing department that the goods were received.

Treasurer Checks received daily from the accounts payable department are

sorted into two groups: those over and those under $10,000. Checks for less than

$10,000 are machine signed. The cashier maintains the check signature machine’s

key and signature plate and monitors its use. Both the cashier and the treasurer sign

all checks over $10,000.

a. Describe the weaknesses relating to purchases and payments of “special orders”

forms in place of paper documents). (CPA Examination, adapted)

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

Weakness

Control

Effect of new IT

1. Buyer does not verify that

the department head’s request

is within budget.

Compare requested amounts

to total budget and YTD

expenditures.

System can automatically compare the

requested amount to the remaining

budget.

2. No procedures established

Solicit quotes/bids for large

EDI and Internet can be used to solicit

3. Buyer does not check

Prepare a vendor performance

Vendor performance ratings can be

4. Blind counts not made by

receiving.

Black out quantities ordered

on copy of Purchase Order

sent to receiving

Provide incentives if

discrepancies between

packing slip and actual

delivery are detected.

Do not permit receiving clerks to access

quantities on purchase orders.

Request bar coding or RFID tagging of

all items and use readers to check in all

deliveries.

Still provide incentives to detect

discrepancies.

5. Written notice of

Send written notice of

Receiving data and comments entered

6. Written notice of

Send written notice of

Configure system to notify accounts

8. Invoice quantity not

compared to receiving report

quantity.

Compare/verify invoiced

quantity with quantity

received.

System verifies invoice quantity with

quantity received.

9. Notification of

acceptability of equipment

from requesting department

not obtained prior to

recording payable.

Obtain confirmation from

requisitioner of the

acceptability of equipment

ordered prior to recording

payable.

Configure system to require confirmation

of equipment acceptability prior to

approving invoice for payment.

10. Voucher package not sent

Send voucher package

Configure system to match invoices

11. Voucher package not

Treasurer should mark

Configure system to mark supporting

Ch 13: Expenditure Cycle

12. No mention of bank

reconciliation.

Bank account should be

reconciled by someone other

than Accounts Payable or the

treasurer.

Bank account should be reconciled by

someone other than Accounts Payable or

the treasurer.

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

13.11 The ABC Company performs its expenditure cycle activities using its integrated

ERP system as follows:

• Employees in any department can enter purchase requests for items they note as

being either out of stock or in small quantity.

• The company maintains a perpetual inventory system.

• Receiving department employees have read-only access to outstanding purchase

orders. Usually, they check the system to verify existence of a purchase order

prior to accepting delivery, but sometimes during rush periods they unload

trucks and place the items in a corner of the warehouse where they sit until there

is time to use the system to retrieve the relevant purchase order. In such cases, if

employee counts the quantity removed and enters that information in an online

terminal located in the storeroom.

• Occasionally, special items are ordered that are not regularly kept as part of

inventory, from a specialty supplier who will not be used for any regular

purchases. In these cases, an accounts payable clerk creates a one-time supplier

Ch 13: Expenditure Cycle

check. Checks are printed on dedicated printer located in the treasurer’s

department, using special stock paper that is stored in a locked cabinet

accessible only to the treasurer and cashier. The paper checks are sent to

accounts payable to be mailed to suppliers.

Identify weaknesses in ABC’s expenditure cycle procedures, explain the resulting

problems, and suggest how to correct those problems.

Weakness/Problem

Applicable Control

Purchase requests are not reviewed and

approved prior to submission. This can

result in ordering unnecessary items.

Purchase requisitions should be reviewed and

approved by the originating department’s

manager prior to being processed.

timely manner.

Any purchasing agent can add new

suppliers to the approved supplier master

file without approval. As a result, the

approved supplier master file may

contain unreliable or non-existent

suppliers.

Restrict the number of employees who can

make changes to the approved supplier list.

Periodically print a report of all changes and

review them to ensure that they have all been

approved.

Selection of suppliers is based solely on

price. As a result, inferior quality

products could be purchased, resulting in

increased costs due to warranty repairs,

scrap, or rework.

Criteria for selecting suppliers should include

information on supplier reliability and

product quality.

The system should be configured to track

actual supplier performance against promised

delivery dates.

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

Receiving department employees inform

purchasing of discrepancies between

quantities received and ordered greater

than 5%. They may fail to do this during

busy periods, resulting in failure to

timely resolve problems.

Configure the system to compare quantities

received to quantities ordered. The system

should send discrepancies exceeding a

tolerable deviation directly to the purchasing

manager.

The identity of employees removing

inventory from the storeroom is not

recorded. This makes it difficult to

investigate the cause of any discrepancies

between recorded and actual counts of

inventory.

The identity of employees removing

inventory should be recorded. This can be

done either by swiping an ID badge or by

entering a user ID in an online terminal.

There is no indication that supporting

documents in the voucher package are

marked “cancelled” or “paid” after being

used to issue a check. This can result in

duplicate payments.

The system should be configured to mark

supporting documents in a voucher package

as PAID when used to generate a check or

EFT payment.

Checks are returned to accounts payable

to be mailed to suppliers. This provides

an opportunity to intercept and alter a

check.

Checks should be mailed by the cashier or the

cashier’s assistant.

Ch 13: Expenditure Cycle

13.12 Alden, Inc. has hired you to review its internal controls for the purchase, receipt,

storage, and issuance of raw materials. You observed the following:

• Raw materials, which consist mainly of high-cost electronic components, are

kept in a locked storeroom. Storeroom personnel include a supervisor and four

clerks. All are well trained, competent, and adequately bonded. Raw materials

are removed from the storeroom only upon written or oral authorization by a

production supervisor.

a. Describe the weaknesses that exist in Alden’s expenditure cycle.

b. Suggest control procedures to overcome the weaknesses noted in part a.

Weaknesses

Recommended Improvements

1. Raw materials may be removed

from the storeroom upon oral

authorization from one of the

production foremen.

Raw materials should be removed from the storeroom only

upon written authorization from an authorized production

foreman.

Authorization forms should be prenumbered and accounted

for, list quantities and job or production number, and be

signed and dated.

materials.

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

3. Raw materials are purchased at

a predetermined reorder level and

in predetermined quantities. Since

production levels may often vary

during the year, quantities ordered

may be either too small or too

great for the current production

demands.

Requests for purchases of raw materials should come from

Production department management and be based on

production schedules and quantities on hand per the

perpetual records.

5. Raw materials are always

purchased from the same vendor.

The purchasing department should obtain competitive bids

on all purchases over a specified amount.

7. There is no inspection of the

merchandise received. Since high-

cost electronic components usually

must meet certain specifications,

they should be tested for these

requirements when received.

The goods need to be inspected for quality standards

promptly upon receipt.

Ch 13: Expenditure Cycle

c. Discuss how those control procedures would be best implemented in an

integrated ERP system using the latest developments in IT.

(CPA Examination, adapted)

• The system can be configured to restrict access to only the information needed to perform

assigned functions. For example, the receiving dock employees would not be able to

create purchase orders, nor see the quantity ordered.

• The system can automatically maintain the perpetual inventory records. Periodic physical

counts of inventory will continue to be necessary, however, and any discrepancies with

recorded amounts investigated.

• The company should adopt either MRP or JIT inventory to improve the efficiency of

ordering inventory.

Ch. 13: The Expenditure Cycle: Purchasing and Cash Disbursements

SUGGESTED ANSWERS TO THE CASES

CASE 13-1 RESEARCH PROJECT: IMPACT OF IT ON EXPENDITURE

CYCLE ACTIVITIES, THREATS, AND CONTROLS

Search popular business and technology magazines (Business Week, Forbes,

Fortune, CIO, etc.) to find an article about an innovative use of IT that can be used

to improve one or more activities in the expenditure cycle. Write a report that:

a. Explains how IT can be used to change expenditure cycle activities

b. Discusses the control implications. Refer to Table 13-2 and explain how the new

procedure changes the threats and appropriate control procedures for

mitigating those threats.