13–1

CHAPTER 13

UNDERSTANDING THE ISSUES

1. Partnerships are generally less formal than

other types of organizations and yet it is

important to consider a number of factors in

a partnership agreement. Individual part-

double taxation.

2. The use of a salary or bonus as a means of

allocating profits would be appropriate

when there is a desire to reward partners

3. Unless the profit-sharing agreement states

otherwise, all provisions of the agreement

should be satisfied except the final alloca-

tion of any remaining profits. Rather than

4. Generally speaking, a partner’s capital ac-

count would be debited for the following:

their share of any partnership losses, the

closing of the drawing account to capital,

and any withdrawals whose amount is

Ch. 13—Exercises 13–2

EXERCISES

EXERCISE 13-1

1. Investors in a partnership are not issued stock and have a capital balance rather than a

capital stock at par value account. Regarding the question of legal liability, a partnership is

2. A partnership is not a separate distinct taxable entity for income tax purposes; therefore,

the balance sheet would have no income tax accruals and the income statement would not

3. Salaries in a partnership are considered to be an allocation component for the purpose of

allocating profits rather than an expense of the partnership. The absence of a salary ex-

4. As is the case with salaries, interest on capital balances is a component for the purpose of

allocating profits rather than an actual expense of the partnership. If consideration is con-

veyed to a partner in an amount equal to their interest on invested capital, the consideration

EXERCISE 13-2

The students should employ the typical elements of a memo and be in good form. The content

should reflect a number of concerns. The agreement appears to be reasonably clear in

language and content. However, certain aspects do not seem to be equitable, including the

following:

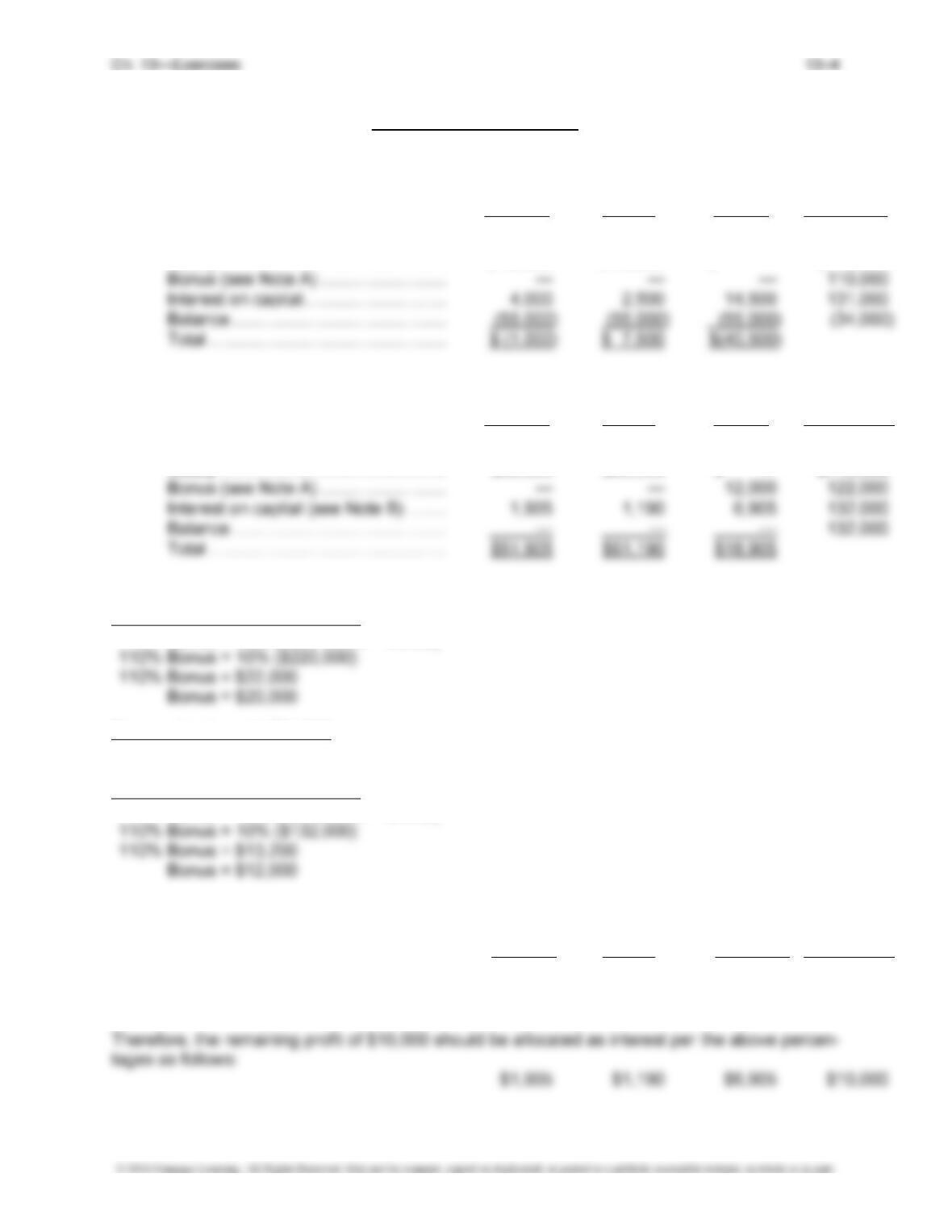

EXERCISE 13-3

(1) Allocation of $220,000 of Partnership Income

Cumulative

Johnson Larson Kragen Total

Profit and loss percentage ……………. 1/3 1/3 1/3

Salary ………………………………………… $50,000 $60,000 $ — $110,000

Exercise 13-3, Concluded

(2) Allocation of $34,000 of Partnership Loss

Cumulative

Johnson Larson Kragen Total

Profit and loss percentage ……………. 1/3 1/3 1/3

Salary ………………………………………… $ 50,000 $ 60,000 $ — $110,000

(3) Allocation of $132,000 of Partnership Income

Cumulative

Johnson Larson Kragen Total

Profit and loss percentage ……………. 1/3 1/3 1/3

Salary ………………………………………… $50,000 $60,000 $ — $110,000

Note A: Calculation of Annual Bonus

Bonus when Income Is $220,000

Bonus = 10% (Net Income – Bonus)

Bonus when Loss Is $34,000

No bonus is due since there is a loss versus income.

Bonus when Income Is $132,000

Bonus = 10% (Net Income – Bonus)

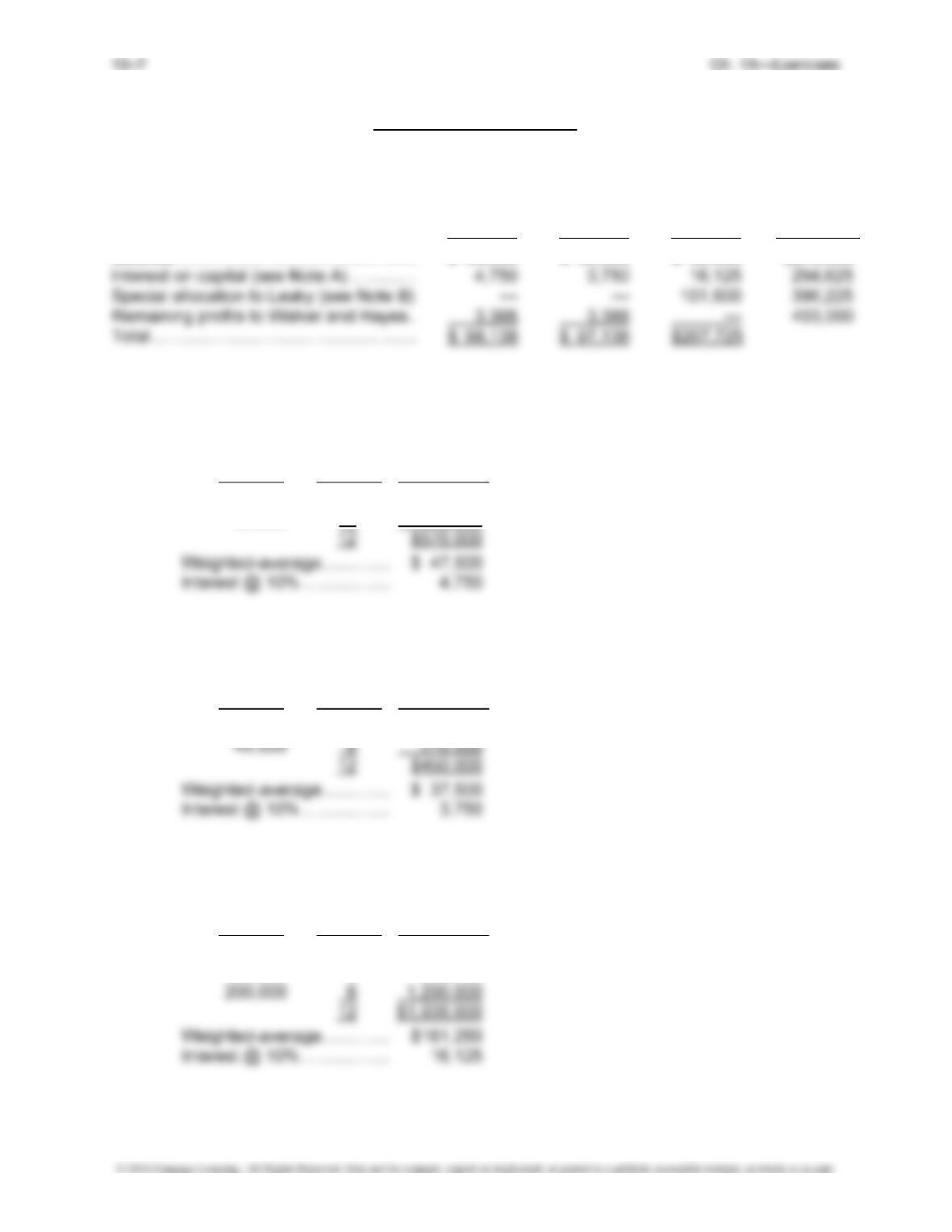

Note B: Stated Interest on Capital

Cumulative

Johnson Larson Kragen Total

Dollar …………………………………………. $4,000 $2,500 $14,500 $21,000

Percent of total ……………………………. 19.05% 11.90% 69.05% 100.00%

13–5 Ch. 13—Exercises

EXERCISE 13-4

1. The best way to measure invested capital is to use a weighted average. This will result in

proper consideration of varying levels of capital over time. In this particular case, it is antic-

ipated that significant capital contributions will be made over the first 18 months of opera-

2. The interest rate on invested capital should reflect the risk associated with the investment

in the partnership. Obviously, the higher the risk the higher the interest rate. However, a

proper assessment of the risk/return relationship may not be easy, and other alternative re-

turns on investment may be a good proxy for the interest rate. For example, the rate a bank

3. Capital balances reflect book values, not fair market values; therefore, the proposed buyout

provision seems inadequate. Given the nature of the proposed partnership business, metal

fabricating, there will be many assets whose book value does not equate to their fair market

4. Salaries are a component of a profit- or loss-sharing agreement and are not the same as

drawings. It is the drawings that are paid out over some period of time. Therefore, it is

5. Clearly, calculating a bonus as a percentage of income is the easiest method. However, it

Exercise 13-4, Concluded

6. Individual partners contribute to a partnership in a variety of ways, and a profit- or loss-

sharing agreement hopefully recognizes this by virtue of using a variety of provisions such

as interest on invested capital, salaries, bonuses, etc. Satisfying each provision to the

EXERCISE 13-5

Allocation of third year income based on original profit allocation:

Cumulative

Walker

Hayes Leaky Total

Salaries …………………………………………… $ 90,000 $ 90,000 $ 70,000 $250,000

Bonuses ………………………………………….. 11,000 11,000 11,000 283,000

Allocation of third year income based on revised profit allocation and combined income of

$353,000:

Cumulative

Walker

Hayes Leaky Total

Salaries …………………………………………… $ 90,000 $ 90,000 $ 90,000 $270,000

Exercise 13-5, Continued

Allocation of third year income based on revised profit allocation and combined income of

$403,000:

Cumulative

Walker

Hayes Leaky Total

Salaries …………………………………………… $ 90,000 $ 90,000 $ 90,000 $270,000

Note A: Interest on Weighted-Average Capital, Walker

Number

Amount of Months Weighted

Invested Invested Dollars

$40,000 6 $240,000

55,000 6

330,000

Interest on Weighted-Average Capital, Hayes

Number

Amount of Months Weighted

Invested Invested Dollars

$30,000 6 $180,000

Interest on Weighted-Average Capital, Leaky

Number

Amount of Months Weighted

Invested Invested Dollars

$ 60,000 3 $ 180,000

185,000 3 555,000

Exercise 13-5, Concluded

Note B: Special Allocation to Leaky

If Leaky had joined with the outside investor and the net income was a minimum of $100,000,

the allocation of profits would have been as follows:

Outside Cumulative

Leaky

Investor Total

Salaries …………………………………………… $ 60,000 $ — $ 60,000

If Leaky had joined with the outside investor and the net income was a minimum of $150,000,

the allocation of profits would have been as follows:

Outside Cumulative

Leaky

Investor Total

Salaries …………………………………………… $ 60,000 $ — $ 60,000

Interest on capital ……………………………… — 6,250 66,250

Author’s Note:

In addition to the above quantitative analysis there are other factors to consider such as the

following:

• Relative to the original partnership agreement, Hayes is not gaining significantly from the

proposed new arrangement.

• Hayes is being allocated interest on their capital including the required investment of

$15,000. What other alternatives might Hayes have for this capital? Could they earn more

than what is being offered in the revised agreement?

13–9 Ch. 13—Exercises

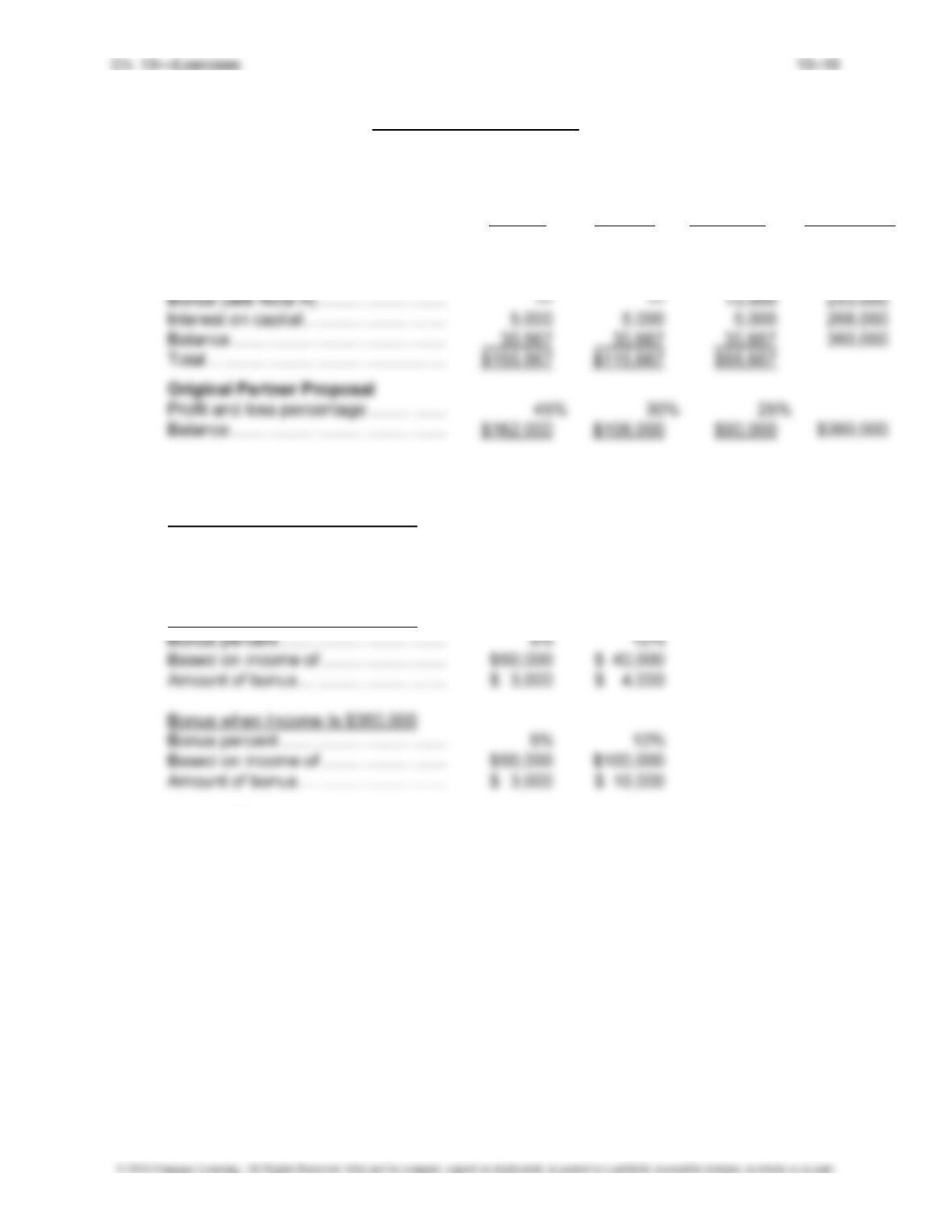

EXERCISE 13-6

Year 1—Allocation of $250,000 of Partnership Income

Cumulative

Banyan Schultz Witkowski Total

Witkowski Proposal

Profit and loss percentage ……………. 1/3 1/3 1/3

Salary ………………………………………… $120,000 $80,000 $40,000 $240,000

Bonus (see Note A) ……………………… — — 2,500 242,500

Year 2—Allocation of $300,000 of Partnership Income

Cumulative

Banyan Schultz Witkowski Total

Witkowski Proposal

Profit and loss percentage ……………. 1/3 1/3 1/3

Salary ………………………………………… $120,000 $80,000 $40,000 $240,000

Bonus (see Note A) ……………………… — — 7,000 247,000

Interest on capital ………………………… 5,000 5,000 5,000 262,000

Exercise 13-6, Concluded

Year 3—Allocation of $360,000 of Partnership Income

Cumulative

Banyan Schultz Witkowski Total

Witkowski Proposal

Profit and loss percentage ……………. 1/3 1/3 1/3

Salary ………………………………………… $120,000 $ 80,000 $40,000 $240,000

Note A: Calculation of Annual Bonus

Bonus when Income Is $250,000

Bonus percent …………………………….. 5% 10%

Based on income of …………………….. $ 50,000 $ —

Amount of bonus …………………………. $ 2,500 $ —

Bonus when Income Is $300,000

It appears that Witkowski would be well advised to accept the original partners’ proposal during

the initial 3-year term. If income can continue to grow at a 20% rate, only then may Witkowski’s

proposal prove to be the most advantageous. Certainly, the assumption of an annual growth

rate of 20% should be viewed with skepticism.

EXERCISE 13-7

Allocation of $168,000 of Partnership Income

Cumulative

Moore Probst Tanski Total

Profit and loss percentage ……………. 20% 40% 40%

Interest on capital (see Note A) …….. $23,125 $ 1,500 $ 1,500 $ 26,125

Note A: Interest on Weighted-Average Capital, Moore

Number

Amount of Months Weighted

Invested Invested Dollars

$250,000 3 $ 750,000

225,000 9

2,025,000

Interest on Weighted-Average Capital, Probst

Interest on Weighted-Average Capital, Tanski

Number

Amount of Months Weighted

Invested Invested Dollars

$40,000 3 $120,000

Exercise 13-7, Concluded

Note B: Calculation of Annual Bonus

Bonus When Income Is $168,000

Bonus (B) = 20% × (Net Income – Bonus)

1.20% B = 20% × $168,000

EXERCISE 13-8

1. Interest on capital is intended to reward those partners who have significant capital

investments in the partnership. In a capital intensive business, such as the proposed

company, capital is an important driver of income. To the extent that the capital invested by

2. Although mathematically more rigorous, the purpose of calculating a bonus on net income

after the bonus is to insure that a bonus is not being accrued on the bonus itself. If the

3. Drawing and capital is not the same thing although in combination, they represent total

capital. Generally a drawing account is used to record withdrawals of capital not

contributions of capital and/or the allocation of profits or losses. The use of a drawing

4. In its purest sense, a salary to a partner is considered as a component of the profit and loss

agreement. Obviously salaries reported as W-2 wages represent that portion of the

5. Although this is possible to do, normally the percentage allocation for profits and losses are

the same. Practically speaking, it would be unusual to think of a situation where a partner’s

6. A partnership is characterized by unlimited liability and the partners are personally liable,

jointly and severally. This would be the case if the erection component of the business were

7. If the attorney were a limited partner in a limited partnership, their obligation for partnership

8. Being a partner would expose the attorney to more potential risk than an outside lender of

capital. As a partner they could be held personally liable for the obligations of the

EXERCISE 13-9

(1)

Allocation of Profits Based on Alternative A

Assumed income level ……………………… $500,000 $560,000 $600,000

Salary ……………………………………………. $120,000 $120,000 $120,000

Interest (Note A) ……………………………… 5,500 5,500 5,500

Exercise 13-9, Continued

Cash Distributions

Date—End of Amount

Quarter 1 ……………………………………….. $ 30,000

Quarter 2 ……………………………………….. 30,000

Quarter 3 ……………………………………….. 30,000

Note A: Amount Number of Weighted

Invested Months Invested Dollars

$100,000 3 $300,000

70,000 3 210,000

Allocation of Profits Based on Alternative B

Assumed income level ……………………… $500,000 $560,000 $600,000

Salary ……………………………………………. $ 96,000 $ 96,000 $ 96,000

Interest (Note B) ……………………………… 10,000 10,000 10,000

Cash Distributions

Date—End of Amount

Quarter 1 ……………………………………….. $ —

Quarter 2 ……………………………………….. 24,000

Quarter 3 ……………………………………….. 24,000

Quarter 4 ……………………………………….. 24,000

Quarter 1 next year ………………………….. 60,000

Exercise 13-9, Concluded

Note B: Amount Number of Weighted

Invested Months Invested Dollars

$100,000 12 $1,200,000

Weighted-average ……………………. $100,000

Interest @ 10% ………………………… 10,000

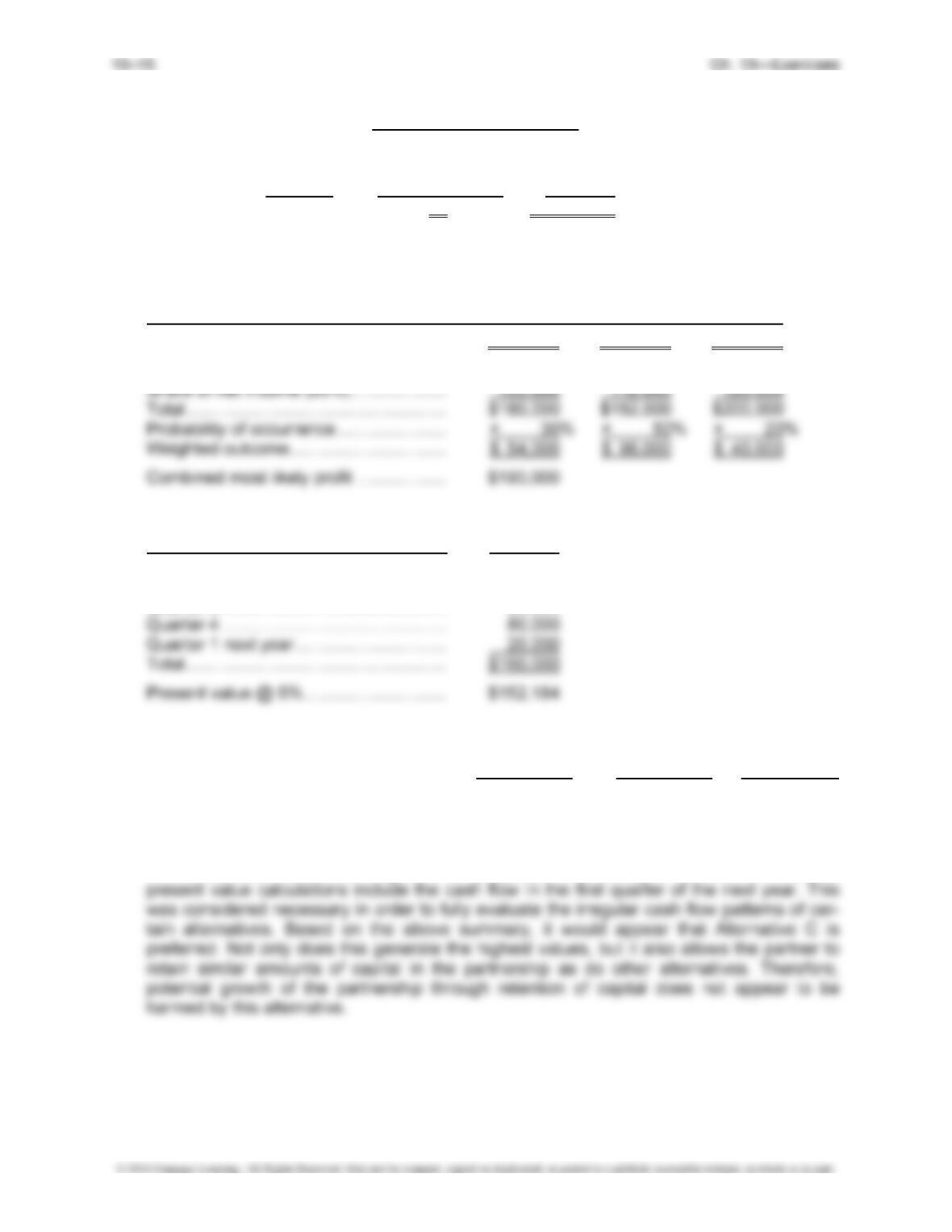

Allocation of Profits Based on Alternative C

Assumed income level ……………………… $500,000 $560,000 $600,000

Salary ……………………………………………. $ 80,000 $ 80,000 $ 80,000

Cash Distributions

Date—End of Amount

Quarter 1 ……………………………………….. $ 20,000

Quarter 2 ……………………………………….. 20,000

Quarter 3 ……………………………………….. 20,000

(2) Summary of above calculations:

Alternative A Alternative B Alternative C

Combined most likely profit ………………. $180,500 $161,000 $190,000

Net present value ……………………………. 143,479 124,556 152,184

An initial investment of $100,000 is required, regardless of which alternative is selected.

Therefore, this investment is ignored for purposes of selecting an alternative. Also, all