CHAPTER 13 Investments and Fair Value Accounting

Prob. 13–3B

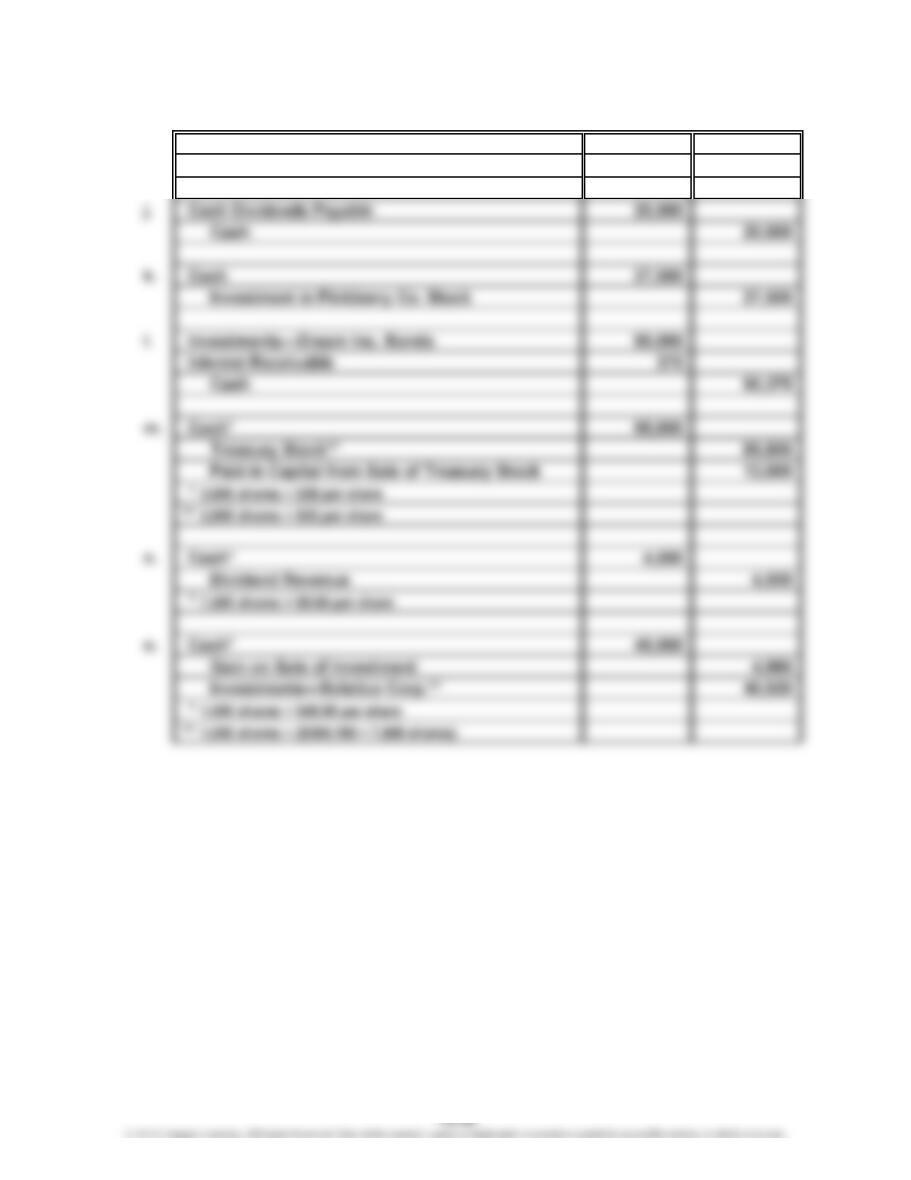

1.

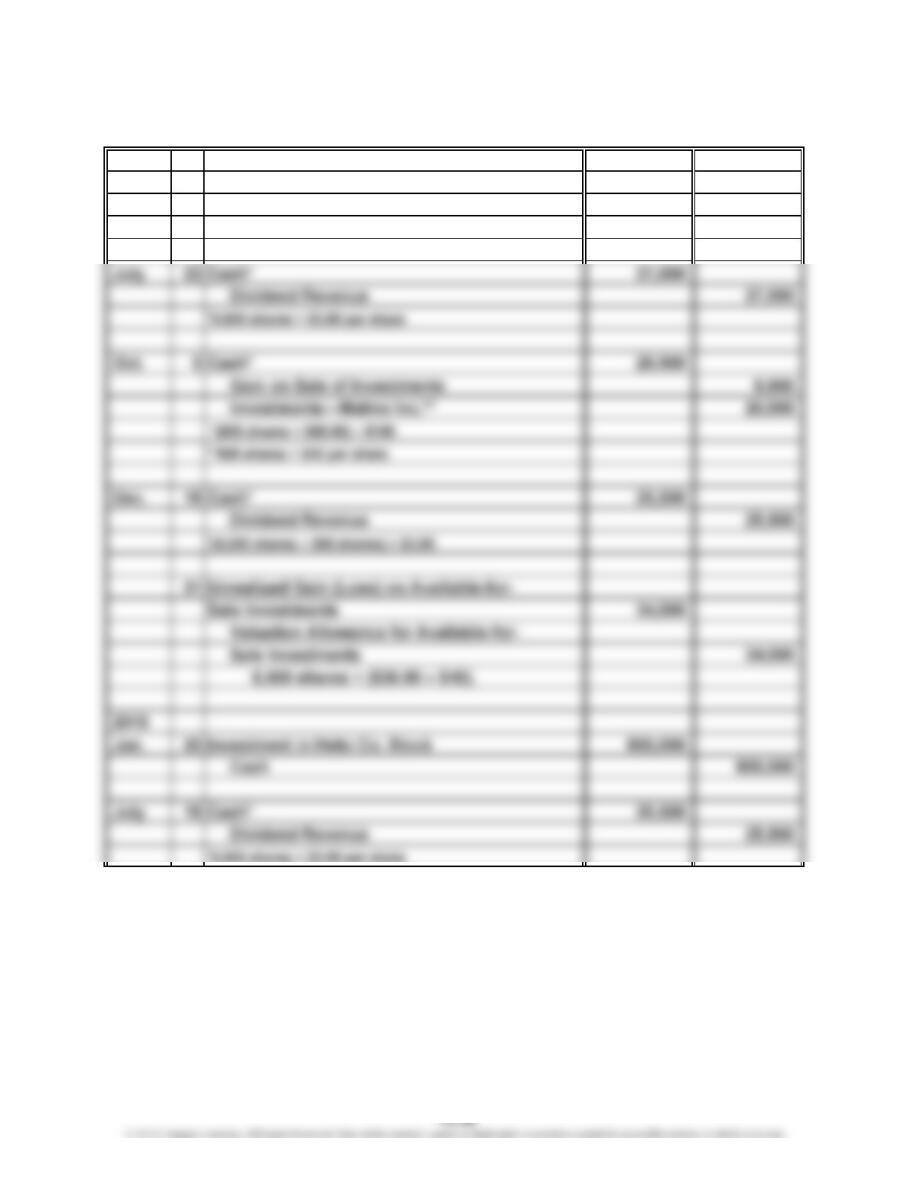

18 Investments—Malmo Inc.* 360,000

Cash 360,000

*9,000 shares × $40 per share

2014

Jan.

CHAPTER 13 Investments and Fair Value Accounting

Prob. 13–3B (Concluded)

16 Cash* 27,200

Dividend Revenue 27,200

*8,500 shares × ($3.00 + $0.20)

2.

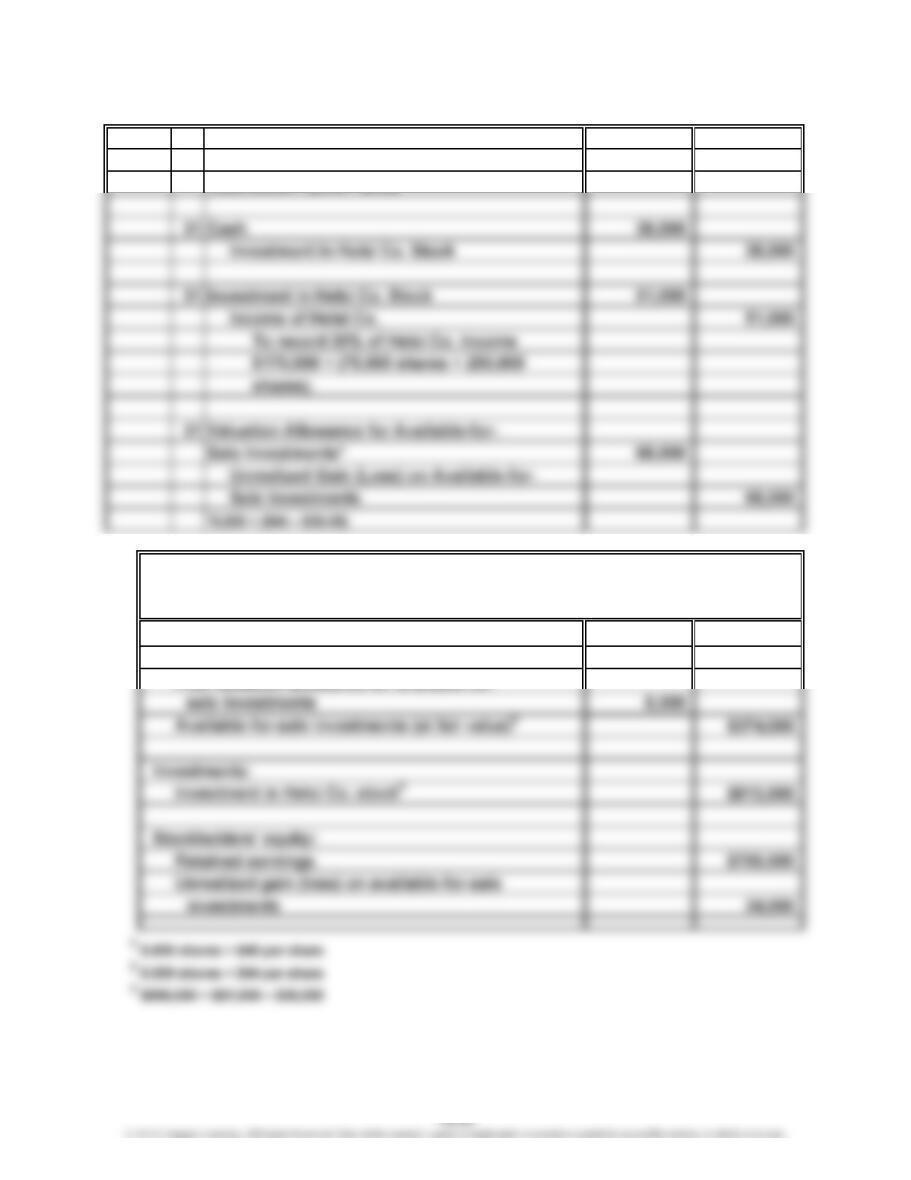

Current assets:

Available-for-sale investments (at cost)1$340,000

Plus valuation allowance for available-for-

GLACIER PRODUCTS, INC.

Balance Sheet (selected items)

December 31, 2015

Dec.

CHAPTER 13 Investments and Fair Value Accounting

Prob. 13–4B

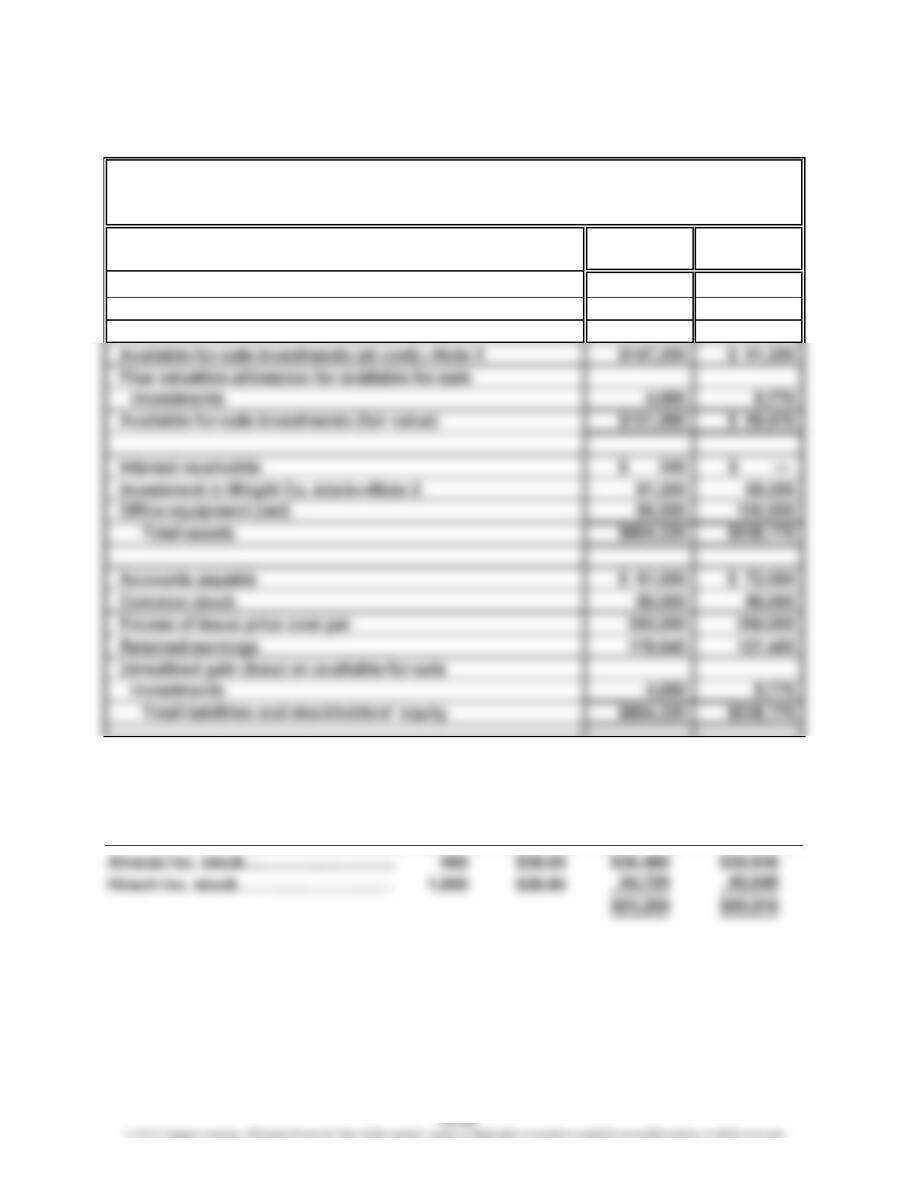

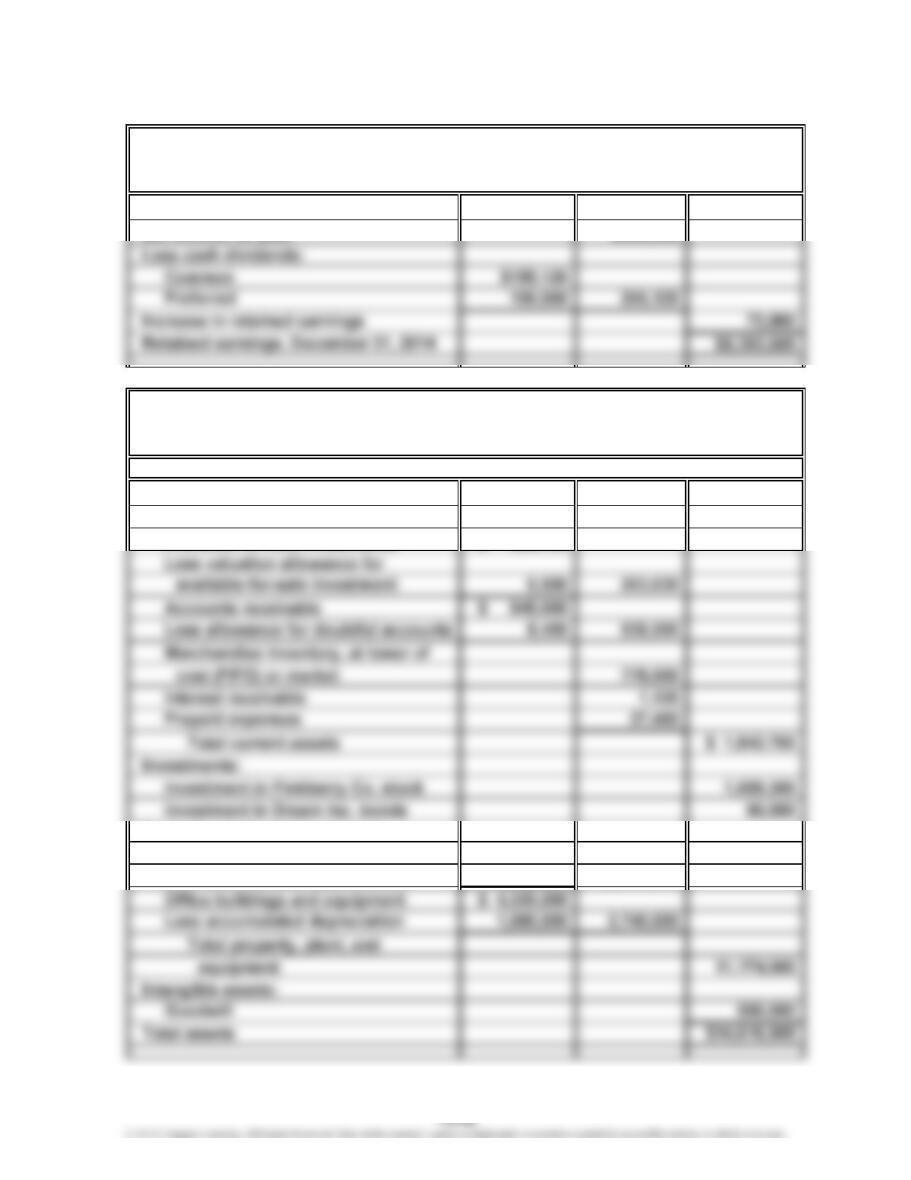

a. $147,200 (from table)

CHAPTER 13 Investments and Fair Value Accounting

Prob. 13–4B (Continued)

The completed comparative unclassified balance sheets are as follows:

Dec. 31, Dec. 31,

2015 2014

Cash $160,000 $156,000

Accounts receivable (net) 115,000 108,000

Note 1. Investments are classified as available for sale. The investments at cost

and fair value on December 31, 2014, are as follows:

No. of Cost per Total Total Fair

Shares Share Cost Value

TEASDALE, INC.

Balance Sheet

December 31, 2015 and 2014

CHAPTER 13 Investments and Fair Value Accounting

Prob. 13–4B (Concluded)

For December 31, 2015:

Market

Cost per Value per

No. of Share (or Share (or

Shares (or $100 of $100 of Total Fair

face amount) face amount) face amount) Cost Value

Alvarez Inc. stock……… 960 $38.00 $41.50 $ 36,480 $ 39,840

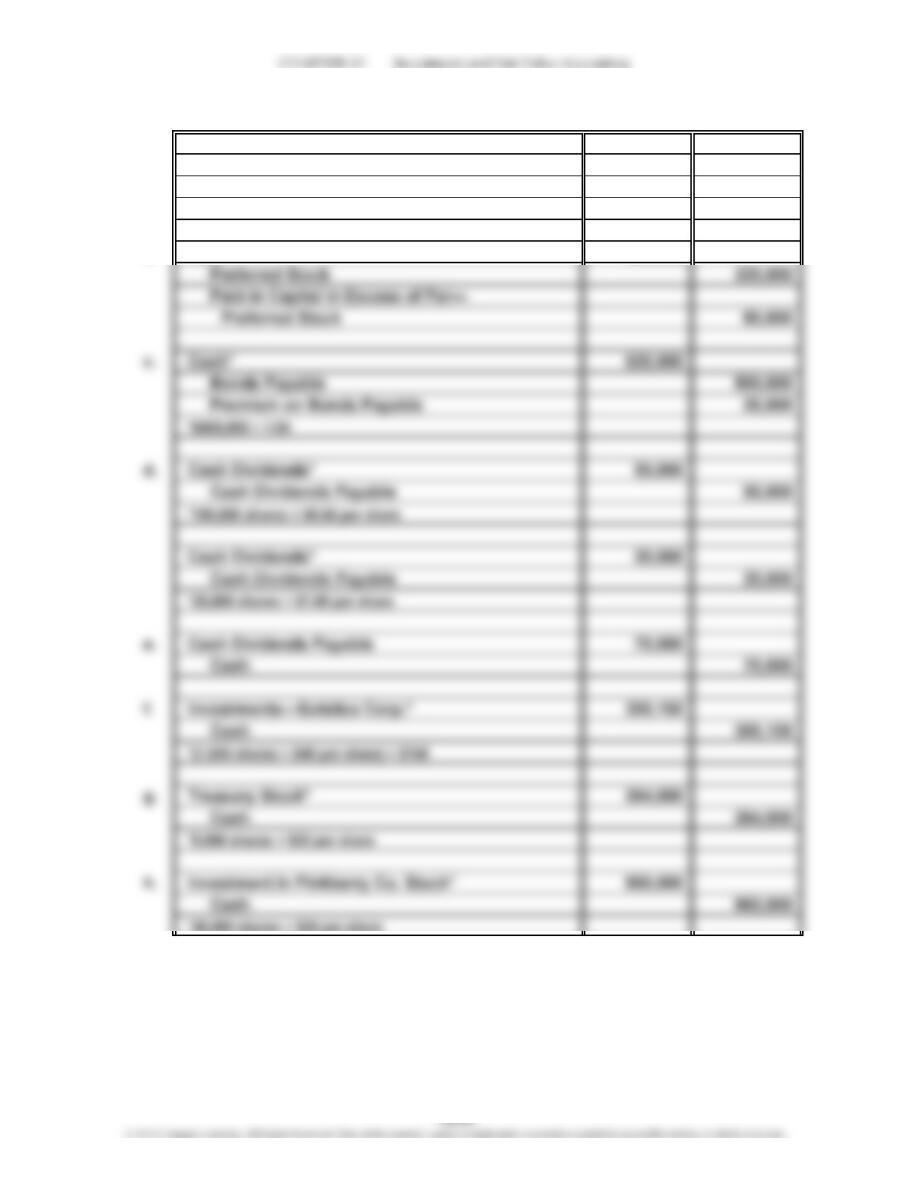

1. a. Cash 450,000

Common Stock 300,000

Paid-In Capital in Excess of Par—

Common Stock 150,000

b. Cash 400,000

COMPREHENSIVE PROBLEM 4

CHAPTER 13 Investments and Fair Value Accounting

Comp. Prob. 4 (Continued)

i. Cash Dividends 20,000

Cash Dividends Payable 20,000

CHAPTER 13 Investments and Fair Value Accounting

Comp. Prob. 4 (Continued)

p. Interest Expense 11,500

Computations:

r. Investment in Pinkberry Co. Stock* 76,800

2. a.

Sales $5,254,000

Administrative expenses:

Office salaries expense $170,000

Office rent expense 50,000

Gain on sale of investment 4,980

Interest expense (21,000) 68,000

Income before income tax $ 469,500

Income tax 140,500

Net income $ 329,000

EQUINOX PRODUCTS INC.

Income Statement

For the Year Ended December 31, 2014

CHAPTER 13 Investments and Fair Value Accounting

Comp. Prob. 4 (Continued)

b.

Retained earnings, January 1, 2014 $9,319,725

Net income for year $329,000

c.

Current assets:

Cash $ 246,000

Available-for-sale investments $ 260,130

Property, plant, and equipment:

Store buildings and equipment $12,560,000

Less accumulated depreciation 4,126,000 $8,434,000

Balance Sheet

For the Year Ended December 31, 2014

Assets

EQUINOX PRODUCTS INC.

Retained Earnings Statement

For the Year Ended December 31, 2014

EQUINOX PRODUCTS INC.

CHAPTER 13 Investments and Fair Value Accounting

Comp. Prob. 4 (Concluded)

Current liabilities:

Paid-in capital:

Preferred 5% stock, $80 par

(30,000 shares authorized;

20,000 shares issued) $1,600,000

EQUINOX PRODUCTS INC.

Stockholders’ Equity

Balance Sheet

For the Year Ended December 31, 2014

Liabilities

CHAPTER 13 Investments and Fair Value Accounting

CP 13–1

1. Under generally accepted accounting principles, the land would be reported

2. The historical cost valuation reduces the ability to compare the two companies.

In this scenario, both companies have nearly identical land holdings. Wyatt

CP 13–2

1. There is an emerging trend toward more uniform accounting standards

worldwide. This is caused by companies participating in multiple capital

markets. For example, many companies not only have their stock trade on the

New York Stock Exchange, but might also have their stock trade in London or

2. Fair value reporting for property, plant, and equipment is a very aggressive

fair value position. This is because property, plant, and equipment fair values

CASES & PROJECTS

CHAPTER 13 Investments and Fair Value Accounting

CP 13–2 (Concluded)

3. The accounting treatment for increases in fair value for property, plant, and

equipment under International Accounting Standards is similar to the

treatment for unrealized gains and losses from available-for-sale investments.

CP 13–3

Since many complex and exotic investment vehicles do not have ready market

values, management must value these investments using mathematical models,

CP 13–4

1. Look-through earnings is a Warren Buffett term. It is the GAAP net income

plus an adjustment for the equity earnings (the “forgotten-but-not-gone”

2. Buffett makes the case that there is no reason for the equity method to be used

only for 20%–50% investees, but that the rationale for the equity method applies

CP 13–5

The following are portions of Notes 3 and 4 from the financial statements dated June 30, 2011, for Microsoft.

Investment Components, Including Associated Derivatives

Cash Equity and

Cost Unrealized Unrealized Recorded and Cash Short-Term Other

(In millions) Basis Gains Losses Basis Equivalents Investments Investments

June 30, 2011

Cash $ 1,648 $ — $ — $ 1,648 $1,648 $ — $ —

NOTE 4 INVESTMENTS

CHAPTER 13 Investments and Fair Value Accounting

CP 13–5 (Concluded)

The components of other income (expense) were as follows:

$ 900 $ 843 $ 744

Note to Instructors: This solution is provided as a guide. Students may have different

numbers, depending on the date of the financial statements.

Answers in millions.

Dividends and interest

2010 2009

NOTE 3 OTHER INCOME (EXPENSE)

(In millions)

Year Ended June 30, 2011

13-50