395

CHAPTER 13

BUDGETING AND STANDARD COST SYSTEMS

CLASS DISCUSSION QUESTIONS

1. The three major objectives of budgeting are

(1) to establish specific goals for future oper-

ations, (2) to direct and coordinate plans to

achieve the goals, and (3) to periodically

compare actual results with the goals.

4. Budgeting more resources for travel than

requested by department personnel is an ex-

ample of budgetary slack.

5. A budget that is set too loosely may fail to moti–

vate managers and employees to perform effi–

ciently. In addition, a loose budget may cause a

“spend it or lose it” mentality, where excess

budget resources are spent in order to protect

the budget from future reductions.

8. A static budget is most appropriate in situations

where costs are not variable to an underlying

activity level. As a result, it is reasonable to

plan spending on the basis of a fixed quantity

of resources for the year. This will occur in

some administrative functions, such as human

resources, accounting, or public relations.

budget preparation when large quantities of

data need to be processed. In addition, by

using computerized simulation models, man-

agement can determine the impact of various

operating alternatives on the master budget.

100% of planned production, with no idle

time or overtime, and there should be neither

excessive inventories nor inventories insuffi-

cient to fill sales orders.

12. Purchases of direct materials should be

closely coordinated with the production bud-

get so that inventory levels can be main-

tained within reasonable limits.

13. Direct materials purchases budget, direct

curities or used to reduce loans.

15. The schedule of collections from sales is

used to determine the amount of cash col-

lected from current- and prior-period sales,

based on collection history. The schedule is

used to help determine the estimated cash

receipts portion of the cash budget.

396

17. Standard costs assist in controlling costs

and in motivating managers and employees

to focus on costs.

19. Reporting by the “principle of exceptions” is

the reporting of only variances (or “excep-

tions”) between standard and actual costs to

the individual responsible for cost control.

20. There is no set time period for the revision

of standards. They should be revised when

prices, product design, labor rates, and

manufacturing methods change to such an

extent that current standards no longer rep-

resent a useful measure of performance.

22. a. The two variances in direct materials

cost are:

(1) Price

(2) Quantity

b. The price variance is the result of a

difference between the actual price and

the standard price. It may be caused by

such factors as a change in market pric-

23. The offsetting variances might have been

caused by the purchase of low-priced, infe-

rior materials. The low price of the materials

24. a. The two variances in direct labor costs

are:

(1) Rate

(2) Time

b. The direct labor cost variance is usually

under the control of the production su-

pervisor.

25. No. Even though the assembly workers are

covered by union contracts, direct labor cost

service operations. Fast-food restaurants can

use standards for evaluating the productivity of

the counter and food preparation employees.

In addition, standards could be used to plan

staffing patterns around various times of the

day (e.g., increasing staff during the lunch

hour).

27. Nonfinancial performance measures provide

managers additional measures beyond the

397

EXERCISES

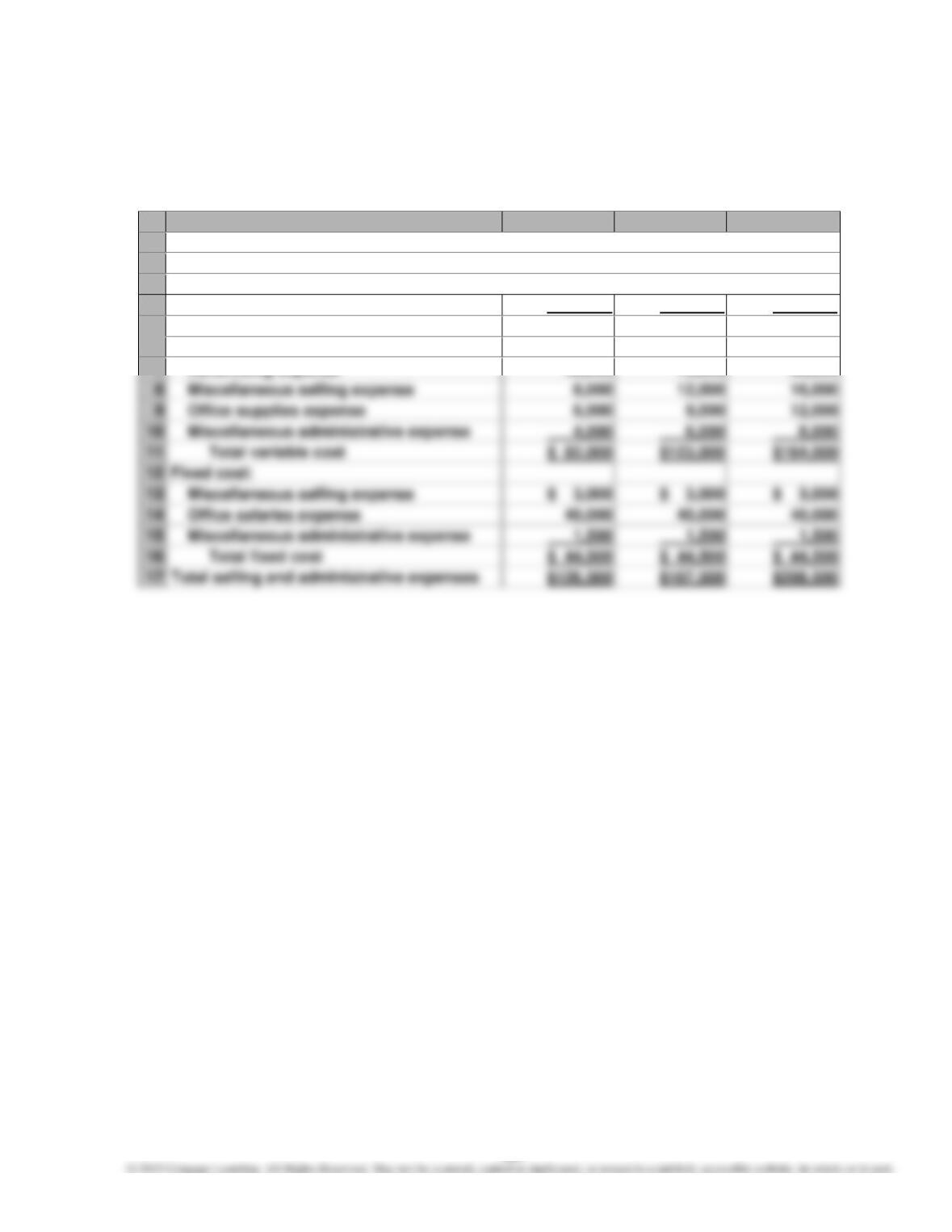

E13–1

A

B

C

D

1

HOMEPORT

2

Flexible Selling and Administrative Expenses Budget

3

For the Month Ending March 31

4

Total sales

$400,000

$600,000

$800,000

5

Variable cost:

6

Sales commissions

$ 16,000

$ 24,000

$ 32,000

7

Advertising expense

48,000

72,000

96,000

8

Miscellaneous selling expense

8,000

9

Office supplies expense

6,000

Miscellaneous administrative expense

Total variable cost

$123,000

$164,000

Fixed cost:

Miscellaneous selling expense

$ 3,000

$ 3,000

Office salaries expense

40,000

40,000

40,000

Miscellaneous administrative expense

Total fixed cost

$ 44,500

$ 44,500

Total selling and administrative expenses

$126,500

$167,500

$208,500

398

E13–2

a.

A

B

C

D

1

PAULK COMPANY—MACHINING DEPARTMENT

2

Flexible Production Budget

3

For the Three Months Ending March 31

4

January

February

March

5

Units of production

50,000

60,000

75,000

6

7

Wages

$1,680,000

$2,016,000

$2,520,000

9

Depreciation

45,000

45,000

10

Total

11

12

Supporting calculations:

13

Units of production

50,000

60,000

75,000

14

Hours per unit

× 1.4

× 1.4

× 1.4

15

Total hours of production

70,000

84,000

105,000

16

Wages per hour

× $24

× $24

× $24

17

Total wages

$1,680,000

$2,016,000

$2,520,000

18

19

Total hours of production

84,000

20

Utility cost per hour

× $1.75

× $1.75

× $1.75

21

Total utilities

b.

January February March

Total actual cost ………………………….. $ 1,854,000 $ 2,236,800 $ 2,798,000

Total flexible budget …………………….. 1,847,500 2,208,000 2,748,750

399

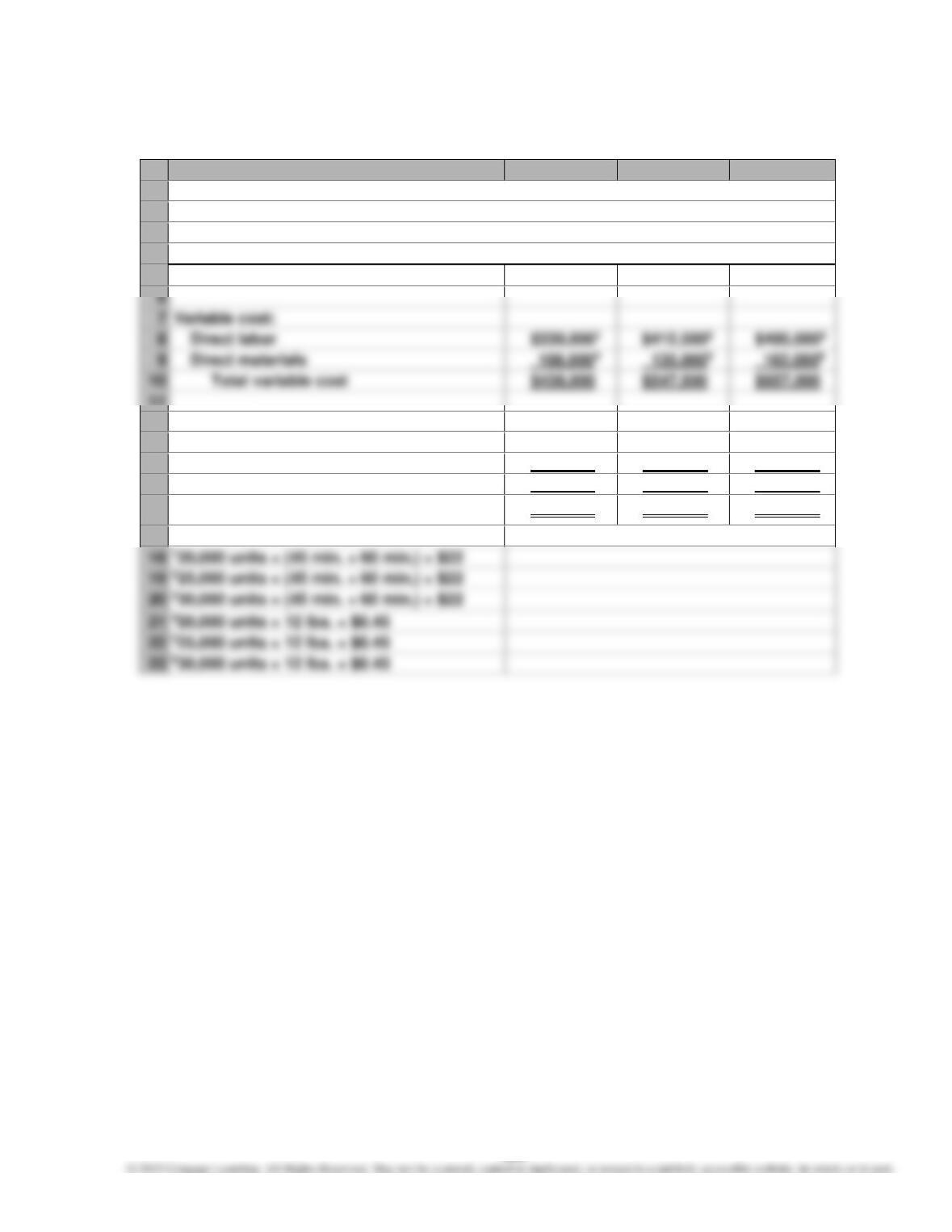

E13–3

A

B

C

D

1

STEELCASE INC.—FABRICATION DEPARTMENT

2

Flexible Production Budget

3

May

4

(Assumed Data)

5

Units of production

20,000

25,000

30,000

6

7

Variable cost:

8

Direct labor

9

Direct materials

10

Total variable cost

$438,000

$ 547,500

$ 657,000

11

12

Fixed cost:

13

Supervisor salaries

$ 175,000

$ 175,000

$ 175,000

14

Depreciation

18,000

18,000

18,000

15

Total fixed cost

$ 193,000

$ 193,000

$ 193,000

16

Total department cost

$ 631,000

$ 740,500

$ 850,000

17

18

19

21

22

23

400

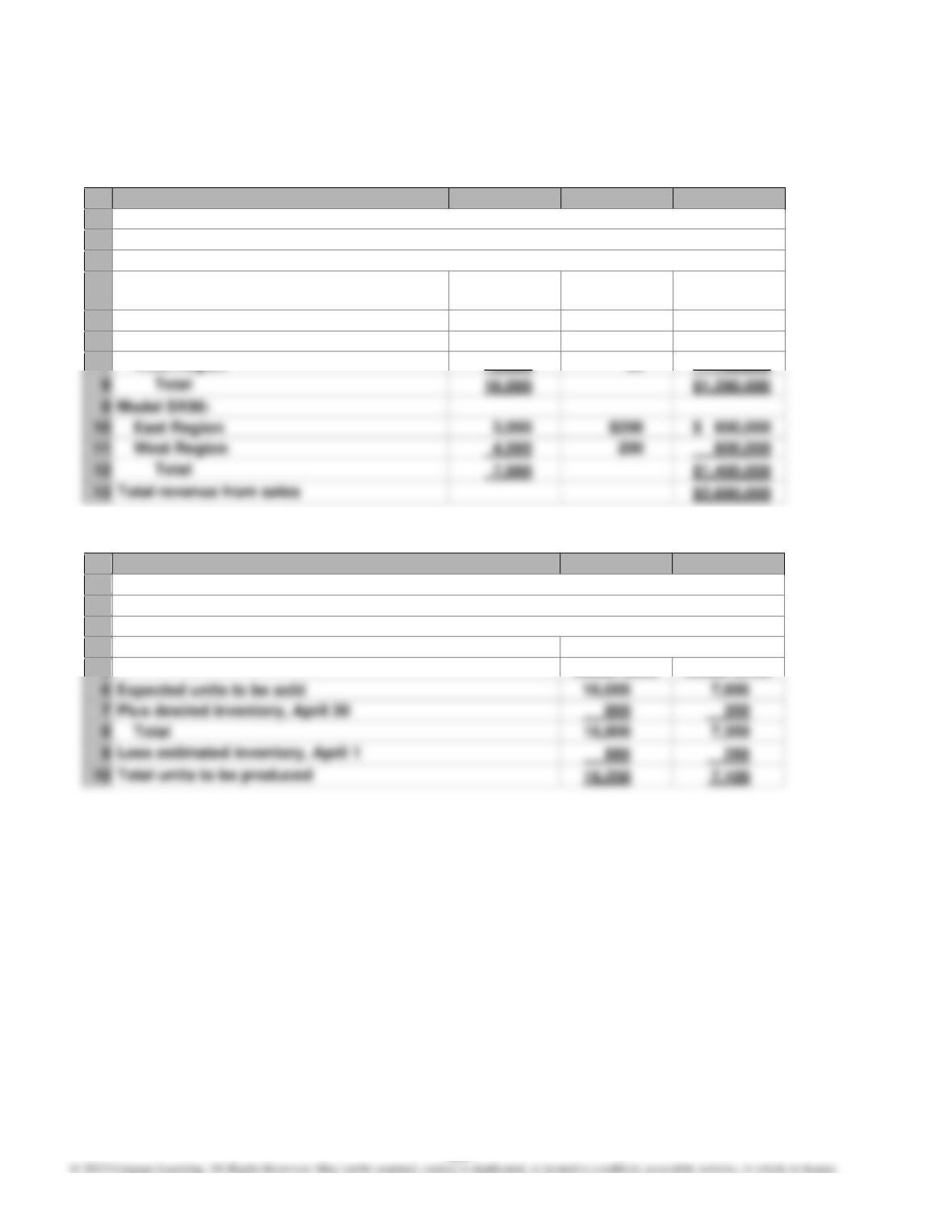

E13–4

a.

A

B

C

D

1

SURROUND AUDIO COMPANY

2

Sales Budget

3

For the Month Ending April 30

4

Product and Area

Unit Sales

Volume

Unit Selling

Price

Total Sales

5

Model SJ30:

6

East Region

7,000

$ 80

$ 560,000

7

West Region

9,000

80

720,000

9

Model SX99:

East Region

$200

$ 600,000

West Region

800,000

b.

A

B

C

1

SURROUND AUDIO COMPANY

2

Production Budget

3

For the Month Ending April 30

4

Units

5

Model SJ30

Model SX99

6

Expected units to be sold

7

Plus desired inventory, April 30

8

Total

401

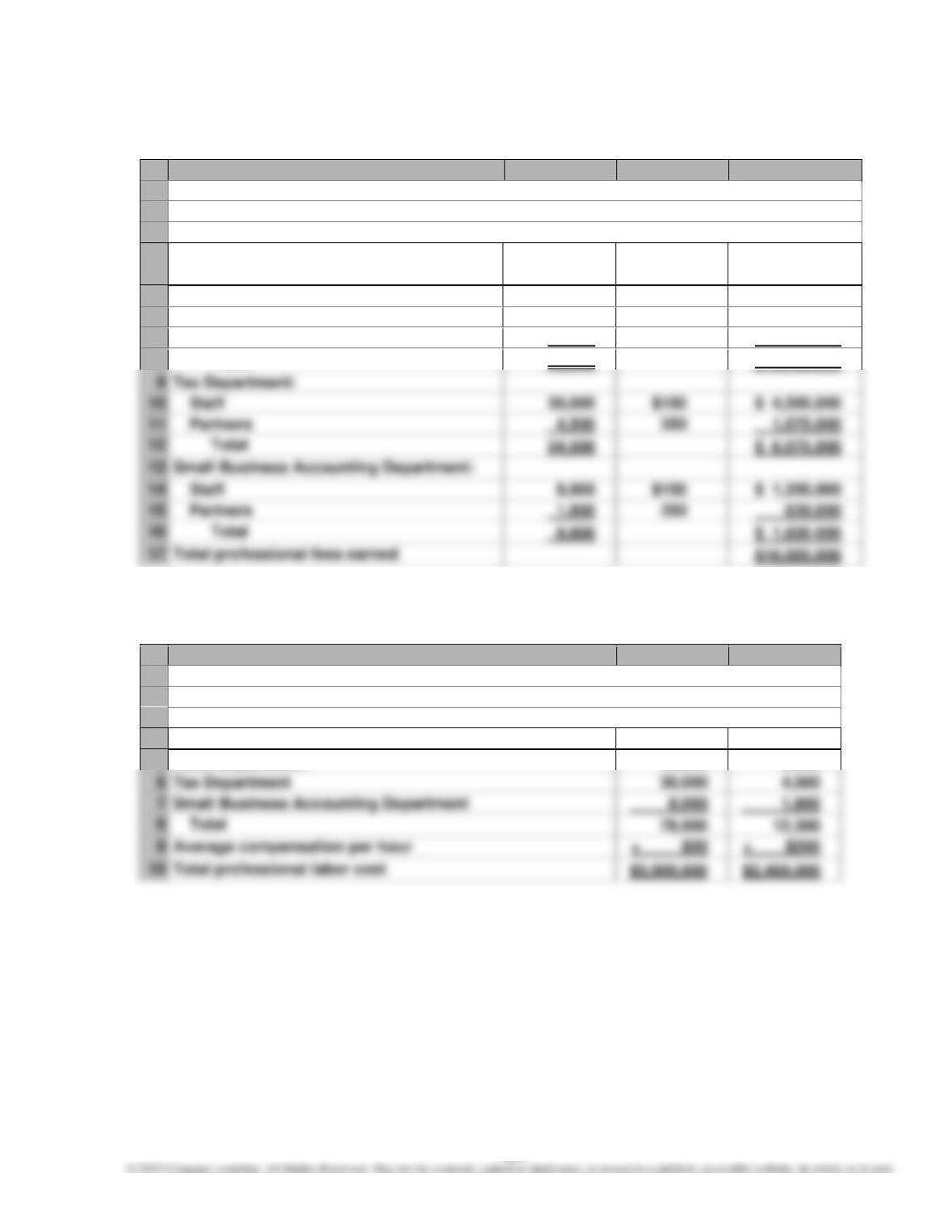

E13–5

A

B

C

D

1

SALAZAR & CRENSHAW, CPAs

2

Professional Fees Earned Budget

3

For the Year Ending July 31, 20Y6

4

Billable

Hourly

Total

Hours

Rate

Revenue

5

Audit Department:

6

Staff

40,000

$150

$ 6,000,000

7

Partners

6,000

350

2,100,000

8

Total

46,000

$ 8,100,000

9

Tax Department:

Staff

$150

$ 4,500,000

Partners

4,500

350

1,575,000

Total

34,500

$ 6,075,000

Small Business Accounting Department:

Staff

$150

$ 1,200,000

Partners

350

630,000

Total

9,800

$ 1,830.000

Total professional fees earned

E13–6

A

B

C

1

SALAZAR & CRENSHAW, CPAs

2

Professional Labor Cost Budget

3

For the Year Ending July 31, 20Y6

4

Staff

Partners

5

Audit Department

40,000

6,000

6

Tax Department

30,000

4,500

7

Small Business Accounting Department

78,000

12,300

E13–7

A

B

C

D

E

1

GINO’S FROZEN PIZZA INC.

2

Direct Materials Purchases Budget

3

For the Month Ending June 30

4

Dough

Tomato

Cheese

Total

Units required for production:

Plus desired inventory,

June 30

Total

49,000

10

Less estimated inventory,

June 1

11

Total units to be purchased

45,000

31,700

44,400

12

Unit price

× $0.90

× $1.20

× $3.00

13

Total direct materials to be

purchased

$40,500

$38,040

$133,200

$211,740

14

20

403

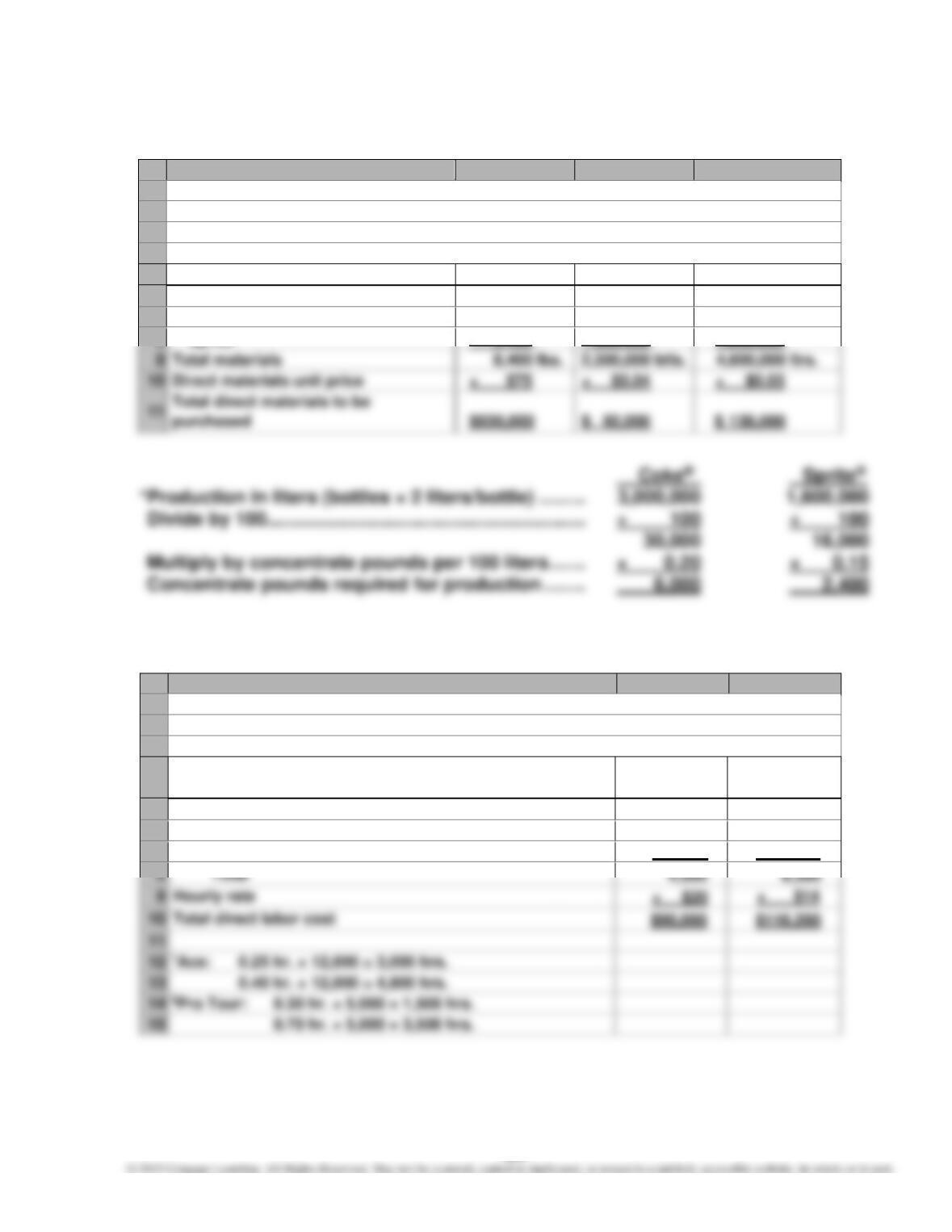

E13–8

A

B

C

D

1

COCA-COLA ENTERPRISES—DALLAS PLANT

2

Direct Materials Purchases Budget

3

For the Month Ending October 31

4

(Assumed Data)

5

Concentrate

2-Liter Bottles

Carbonated Water

6

Materials required for production:

7

Coke®

6,000* lbs.

1,500,000 btls.

3,000,000 ltrs.

8

Sprite®

2,400*

800,000

1,600,000

9

Total materials

8,400 lbs.

2,300,000 btls.

4,600,000 ltrs.

Direct materials unit price

× $75

× $0.04

× $0.03

E13–9

A

B

C

1

ISNER RACKET COMPANY

2

Direct Labor Cost Budget

3

For the Month Ending August 31

4

Forming

Assembly

Department

Department

5

Hours required for production:

6

Ace1

3,000

4,800

7

Pro Tour2

1,500

3,500

4,500

0.70 hr. × 5,000 = 3,500 hrs.

E13–10

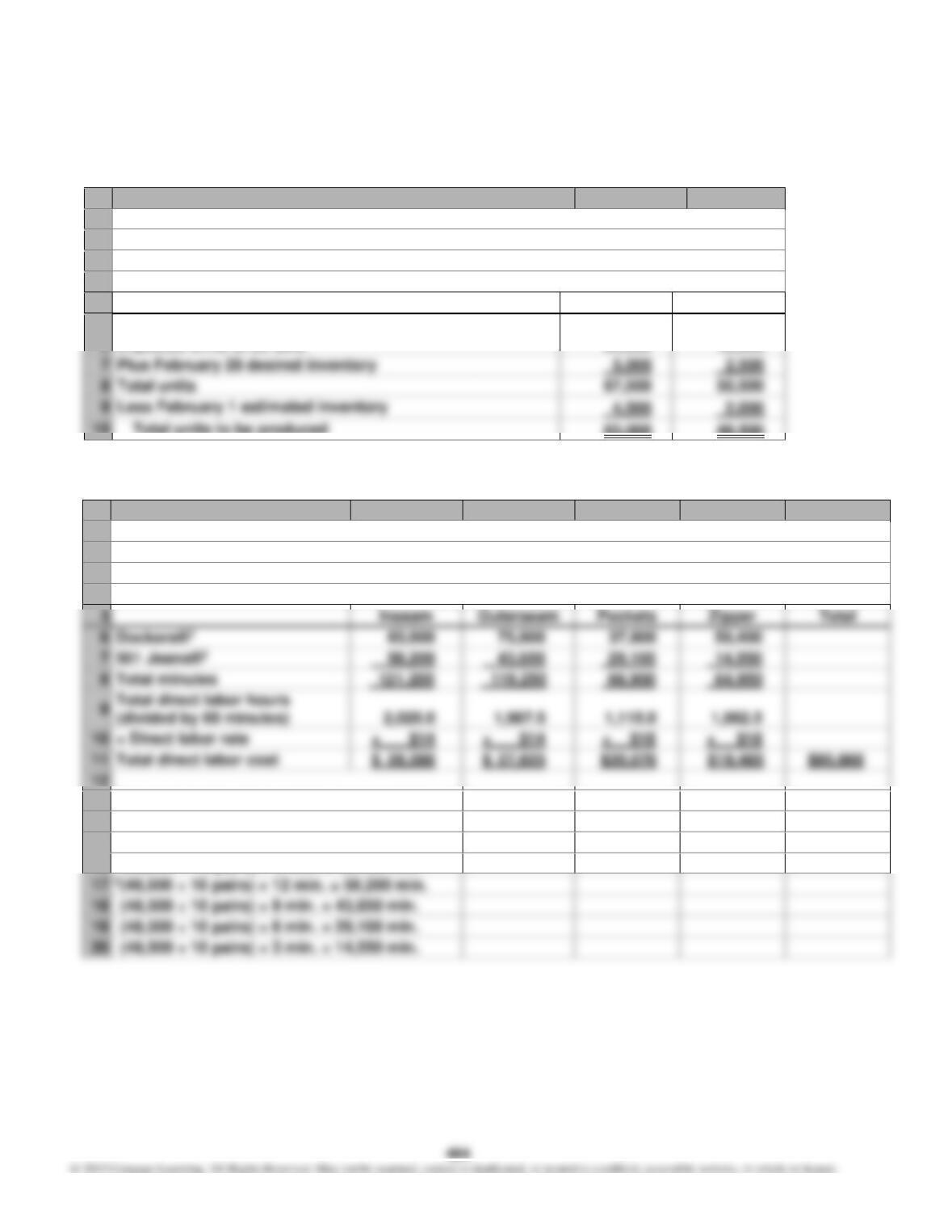

a.

A

B

C

1

LEVI STRAUSS & CO.

2

Production Budget

3

February

4

(Assumed Data)

5

Dockers®

501 Jeans®

6

Expected units to be sold

62,500

48,000

Plus February 28 desired inventory

8

Total units

67,500

50,500

Less February 1 estimated inventory

_2,000

10

Total units to be produced

63,000

48,500

b.

A

B

C

D

E

F

1

LEVI STRAUSS & CO.

2

Direct Labor Cost Budget

3

February

4

(Assumed Data)

6

63,000

75,600

37,800

50,400

7

58,200

43,650

29,100

14,550

8

Total minutes

66,900

64,950

2,020.0

1,987.5

10

× Direct labor rate

× $14

× $14

× $18

× $18

11

Total direct labor cost

$ 28,280

$ 27,825

$20,070

12

13

1(63,000 ÷ 10 pairs) × 10 min. = 63,000 min.

14

(63,000 ÷ 10 pairs) × 12 min. = 75,600 min.

15

(63,000 ÷ 10 pairs) × 6 min. = 37,800 min.

16

(63,000 ÷ 10 pairs) × 8 min. = 50,400 min.

17

2(48,500 ÷ 10 pairs) × 12 min. = 58,200 min.

18

(48,500 ÷ 10 pairs) × 9 min. = 43,650 min.

19

(48,500 ÷ 10 pairs) × 6 min. = 29,100 min.

20

(48,500 ÷ 10 pairs) × 3 min. = 14,550 min.

405

E13–11

A

B

C

1

MICKEY’S CANDY COMPANY

2

Factory Overhead Cost Budget

3

For the Month Ending November 30

4

Variable factory overhead costs:

5

Manufacturing supplies

$ 8,000

6

Power and light

36,000

7

Production supervisor wages

145,000

8

Production control salaries

40,000

Total variable factory overhead costs

Fixed factory overhead costs:

Factory insurance

$ 42,000

Factory depreciation

88,000

Total fixed factory overhead costs

130,000

Total factory overhead costs

406

E13–12

A

B

C

D

1

PUEBLO CERAMICS INC.

2

Cost of Goods Sold Budget

3

For the Month Ending April 30

4

Finished goods inventory, April 1

$ 10,000

5

$ 11,400

6

7

$ 13,000

8

181,000

$194,000

10

15,000

11

production

$179,000

12

Direct labor

200,000

13

Factory overhead

107,000

14

Total manufacturing costs

486,000

15

Total work in process during the period

$497,400

16

9,500

17

Cost of goods manufactured

487,900

18

Cost of finished goods available for sale

$497,900

19

Less finished goods inventory,

Less work in process inventory,

407

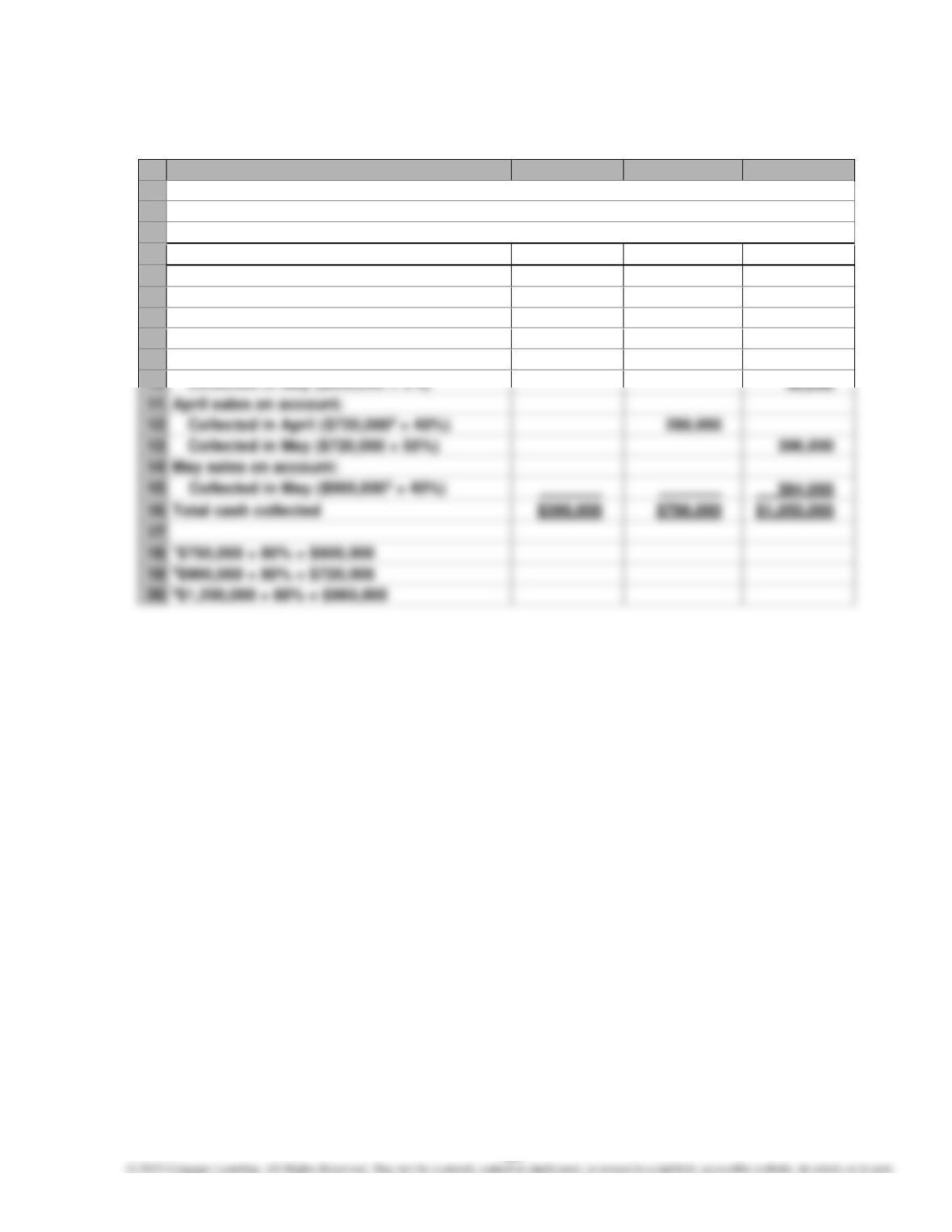

E13–13

A

B

C

D

1

FIDO & LUCY WHOLESALE INC.

2

Schedule of Collections from Sales

3

For the Three Months Ending May 31

4

March

April

May

5

Receipts from cash sales:

6

Cash sales (20% × current month’s sales)

$150,000

$180,000

$ 240,000

7

March sales on account:

8

Collected in March ($600,0001 × 40%)

240,000

9

Collected in April ($600,000 × 55%)

330,000

10

Collected in May ($600,000 × 5%)

April sales on account:

Collected in April ($720,0002 × 40%)

Collected in May ($720,000 × 55%)

May sales on account:

1$750,000 × 80% = $600,000

2$900,000 × 80% = $720,000

3$1,200,000 × 80% = $960,000

408

E13–14

A

B

C

D

1

INNOVATIVE OFFICE INC.

2

Schedule of Collections from Sales

3

For the Three Months Ending March 31, 20Y4

4

January

February

March

5

Receipts from cash sales:

6

Cash sales (30% × current month’s sales)

$ 360,000

$ 435,000

$ 480,000

7

December sales on account:

8

Collected in January (Accounts

Receivable balance)

180,000

9

January sales on account:

11

12

February sales on account:

13

14

15

March sales on account:

16

840,000

18

19

1$1,200,000 × 70% = $840,000

20

2$1,450,000 × 70% = $1,015,000

21

3$1,600,000 × 70% = $1,120,000

409

E13–15

A

B

C

D

1

PEANUT LEARNING SYSTEMS INC.

2

Schedule of Cash Payments for Selling and Administrative Expenses

3

For the Three Months Ending October 31, 20Y7

4

August

September

October

5

August expenses:

6

Paid in August ($107,0001 × 60%)

$64,200

7

Paid in September ($107,000 × 40%)

$ 42,800

8

September expenses:

9

Paid in September ($135,0002 × 60%)

81,000

$ 54,000

October expenses:

1$137,000 – $30,000 = $107,000

2$165,000 – $30,000 = $135,000

3$140,000 – $30,000 = $110,000

410

E13–16

A

B

C

D

1

REHAB PHYSICAL THERAPY INC.

2

Schedule of Cash Payments for Operations

3

For the Three Months Ending May 31

4

March

April

May

5

Payment of prior month’s expense1

$ 36,000

$ 26,300

$ 31,400

6

Payment of current month’s expense2

105,200

125,600

131,600

7

Total payment

$141,200

$151,900

$163,000

8

9

1$36,000, given as Accrued Expenses Payable, March 1

$26,300 = ($140,000 – $8,500) × 20%

$31,400 = ($165,500 – $8,500) × 20%

$125,600 = ($165,500 – $8,500) × 80%

$131,600 = ($173,000 – $8,500) × 80%

Note: Insurance and depreciation are expenses that do not result in cash pay-

ments in March, April, and May.

E13–17

A

B

C

D

E

1

HANDY DAN TOOLS INC.

2

Capital Expenditures Budget

3

For the Four Years Ending December 31, 20Y5–20Y8

4

20Y5

20Y6

20Y7

20Y8

5

Building

$5,000,000

$4,000,000

$ 2,250,0001

6

Equipment

3,600,000

$500,000

500,000

7

Information systems

324,0002

8

Total

$5,000,000

$7,600,000

$824,000

$ 2,750,000

9

1$9,000,000 × 25% = $2,250,000

E13–18

Direct labor ………………………………………………. $21.00 × 2 hrs. $ 42.00

Direct materials ………………………………………… $9.25 × 20 bd. ft. 185.00

411

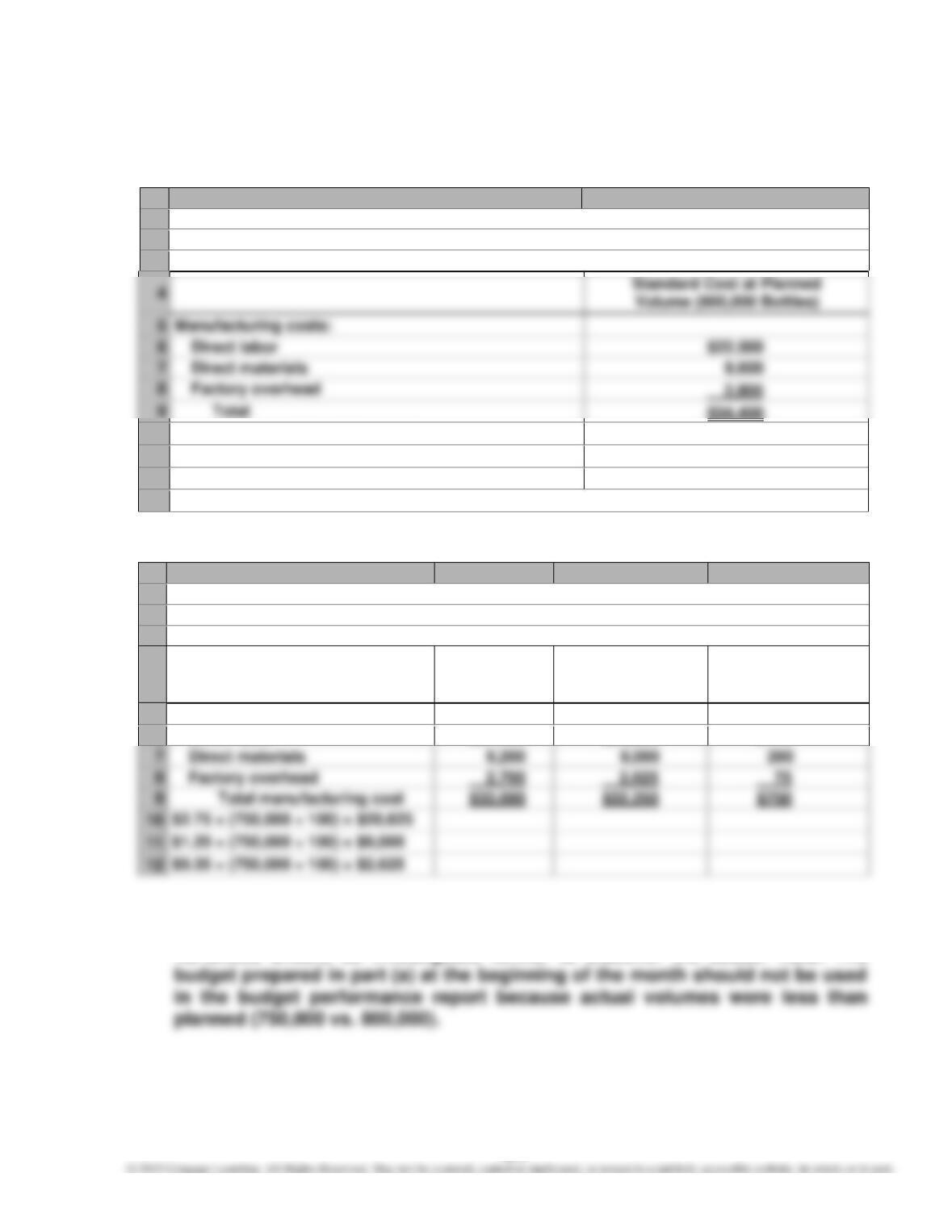

E13–19

a.

A

B

1

MCALISTERS BOTTLE COMPANY

2

Manufacturing Cost Budget

3

For the Month Ended May 31

6

Direct labor

7

Direct materials

Factory overhead

Total

10

$2.75 × (800,000 ÷ 100) = $22,000

11

$1.20 × (800,000 ÷ 100) = $9,600

12

$0.35 × (800,000 ÷ 100) = $2,800

13

Note: The cost standards are expressed as “per 100 bottles.”

b.

A

B

C

D

1

MCALISTERS BOTTLE COMPANY

2

Manufacturing Costs—Budget Performance Report

3

For the Month Ended May 31

4

Actual

Costs

Standard Cost at

Actual Volume

(750,000 bottles)

Cost Variance—

Unfavorable

(Favorable)

5

Manufacturing costs:

6

Direct labor

$21,100

$20,625

$ 475

7

8

Factory overhead

9

Total manufacturing cost

$33,000

$2.75 × (750,000 ÷ 100) = $20,625

$1.20 × (750,000 ÷ 100) = $9,000

c. McAlisters Bottle’s actual costs were $750 more than budgeted. The largest

unfavorable variance of $475 was related to direct labor. The unfavorable

variances should be investigated further to discover the cause. Note: The

E13–20

a. Price variance:

Direct Materials Price Variance = (Actual Price – Standard Price) ×

Actual Quantity

= ($3.60 per lb. – $3.85 per lb.) × 600,000 lbs.

= – $150,000 Favorable Variance

Also computed as:

Actual total direct materials cost ……………. $2,160,000

Less standard total direct materials cost … 2,233,000

Total direct materials cost variance …….. –$ 73,000 Favorable Variance

b. The direct materials price variance should normally be reported to the Pur-

chasing Department, which may or may not be able to control this variance. If

materials of the same quality were purchased from another supplier at a price

lower than the standard price, the variance was controllable. However, if the

variance resulted from a market-wide price decrease, the variance was not

subject to control.

413

E13–21

Standard direct materials for units produced (5,900 units × 2 lbs.) …… 11,800 lbs.

Using the equation for direct materials quantity variance, solve for the standard

direct materials price per pound.

Standard Price per Unit of Product = $2.05 × 2 lbs. per unit = $4.10

Alternate Solution One:

Materials used ………………………………………………………... 12,000 lbs.

Favorable price variance ………………………………………… $3,000

Alternate Solution Two:

Product finished ……………………………………………………….…. 5,900 units

Standard finished product for direct materials used

(12,000 lbs. ÷ 2 lbs.) ………………………………………………… 6,000

Deficiency of finished product for materials used ……. (100) units

414

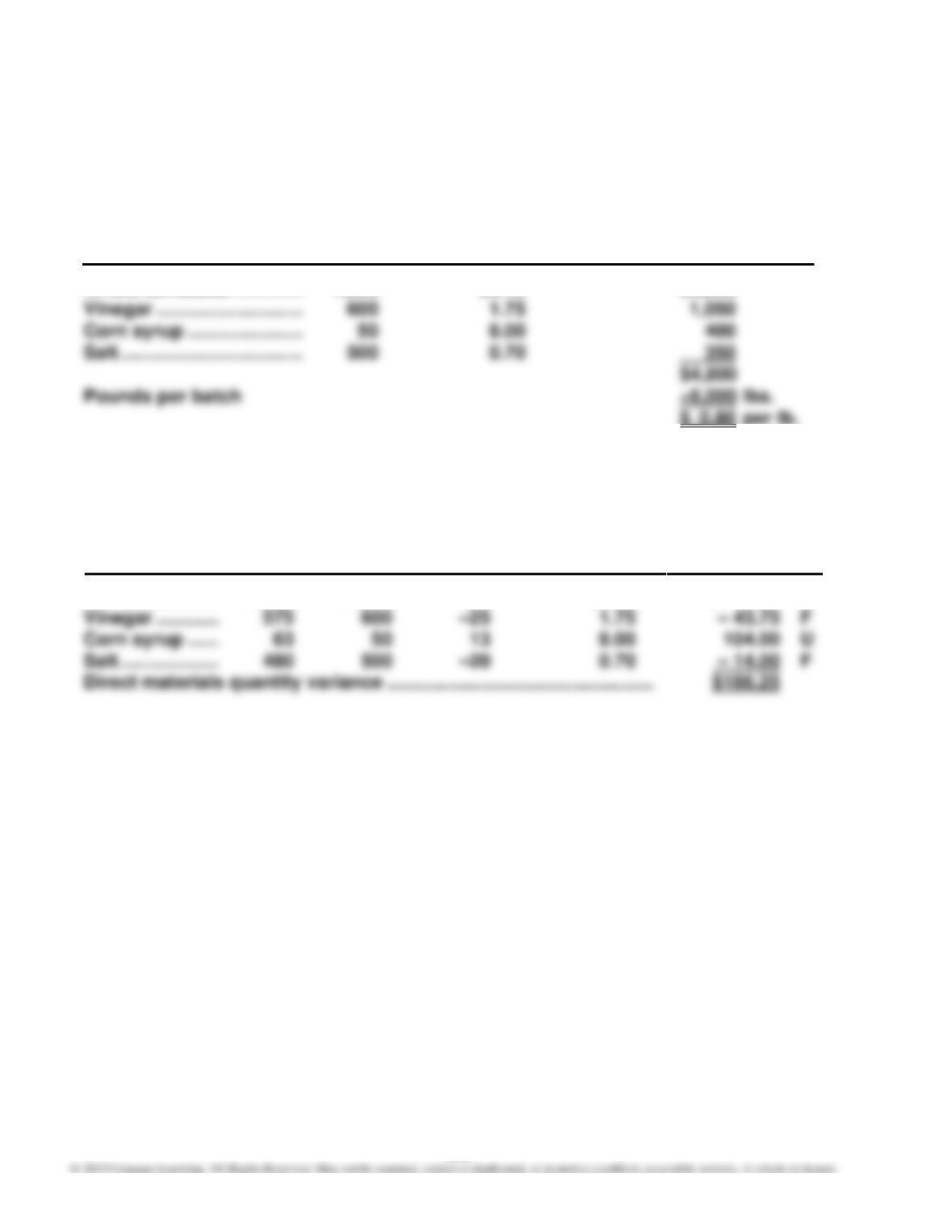

E13–22

a.

Standard Standard Standard Cost

Quantity × Price = per Batch

Whole tomatoes ………….. 7,500 $0.40 $3,000

b.

Actual

Quantity

for Batch

H3001

Standard

Quantity

per

Batch

Quantity

Difference

×

Standard

Price

=

Materials

Quantity

Variance

Tomatoes ………

7,850

7,500

350

$0.40

$ 140.00

U

Vinegar …………

–25

1.75

– 43.75

F

Corn syrup ……

8.00

104.00

U

Salt ……………….

–20

0.70

F

Direct materials quantity variance ……………………………………………