PROBLEM 13-6A

(a) (1) Land ………………………………………………….. 140,000

Preferred Stock (1,200 X $100) ……… 120,000

Paid-in Capital in Excess of Par—

Preferred Stock ………………………… 20,000

(3) Treasury Stock (1,500 X $11) ……………….. 16,500

Cash …………………………………………… 16,500

PROBLEM 13-6A (Continued)

(b) IRWIN CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

10% Preferred stock, $100

par value,

20,000 shares authorized,

1,200 shares issued and

outstanding ……………………… $ 120,000

Additional paid-in capital

In excess of par—

preferred stock ………………… $ 20,000

In excess of stated value—

common stock …………………. 1,800,000

Retained earnings ……………………………. 82,000

Total paid-in capital and

retained earnings ……….. 3,023,500

BYP 13-1 FINANCIAL REPORTING PROBLEM

(a) The common stock of Apple has no par value.

BYP 13-2 COMPARATIVE ANALYSIS PROBLEM

(a) Par value:

Coca-Cola, $0.25 per share.

PepsiCo, $0.01 2/3 per share.

BYP 13-3 COMPARATIVE ANALYSIS PROBLEM

(a) Par value:

Amazon, $0.01 per share.

Wal-Mart, $0.10 per share.

(b) Percentage of authorized shares issued:

Amazon, 483 ÷ 5,000 = 9.7%.

Wal-Mart, 3,233 ÷ 11,000 = 29.4%.

BYP 13-4 REAL-WORLD FOCUS

Answers will vary depending on the company chosen by the student.

BYP 13-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) The market price of a share of stock is caused by many factors. Among

the factors to be considered are:

(1) the corporation’s anticipated future earnings,

(2) its expected dividend rate per share,

(3) its current financial position,

Par value is the amount assigned to each share of stock in the corporate

charter. Par value may be any amount selected by the corporation.

Generally, the amount of par value is quite low because states often levy

a tax on the corporation based on par value.

(b) A corporation may acquire treasury stock to:

(1) Reissue the shares to officers and employees under bonus and stock

compensation plans.

BYP 13-5 (Continued)

Treasury stock is not an asset. If treasury stock was reported as an

asset, then unissued stock should also be shown as an asset, also an

erroneous conclusion. Rather than being an asset, treasury stock

BYP 13-6 COMMUNICATION ACTIVITY

Dear Uncle Joe:

Thanks for your recent letter and for asking me to explain four terms.

Here are my explanations:

(1) Authorized stock is the total amount of stock that a corporation is given

permission to sell as indicated in its charter. If all authorized stock is

sold, a corporation must obtain consent of the state to amend its charter

before it can issue additional shares.

(2) Issued stock is the amount of stock that has been sold either directly

to investors or indirectly through an investment banking firm.

BYP 13-7 ETHICS CASE

(a) The stakeholders in this situation are:

The director of Pigua’s R & D division.

The president of Pigua.

The shareholders of Pigua.

(b) The president is risking the environment and everything and everybody in

it that is exposed to this new chemical in order to enhance his company’s

(c) A parent company may protect itself against loss and most reasonable

BYP 13-8 ALL ABOUT YOU

(a) Ernst and Young LLP was the CPA firm that audited Apple’s financial

statements.

(b) Apple’s basic earnings per share was $40.03 and its diluted earnings

per share was $39.75.

BYP 13-9 FASB CODIFICATION ACTIVITY

(a) Common Stock is a stock that is subordinate to all other stock of the

issuer. Also called common shares.

(b) Preferred Stock is a security that has preferential rights compared to

common stock.

(c) Shares include various forms of ownership that may not take the legal

form of securities (for example, partnership interests), as well as other

interests, including those that are liabilities in substance but not in

IFRS EXERCISES

IFRS 13-1

IFRS 13-2

MEENEN CORPORATION

Partial Statement of Financial Position (Partial)

December 31, 2017

Equity

Share capital—ordinary, €10 par value,

5,000 shares issued and 4,500 shares

outstanding …………………………………………………. €50,000

IFRS 13-3

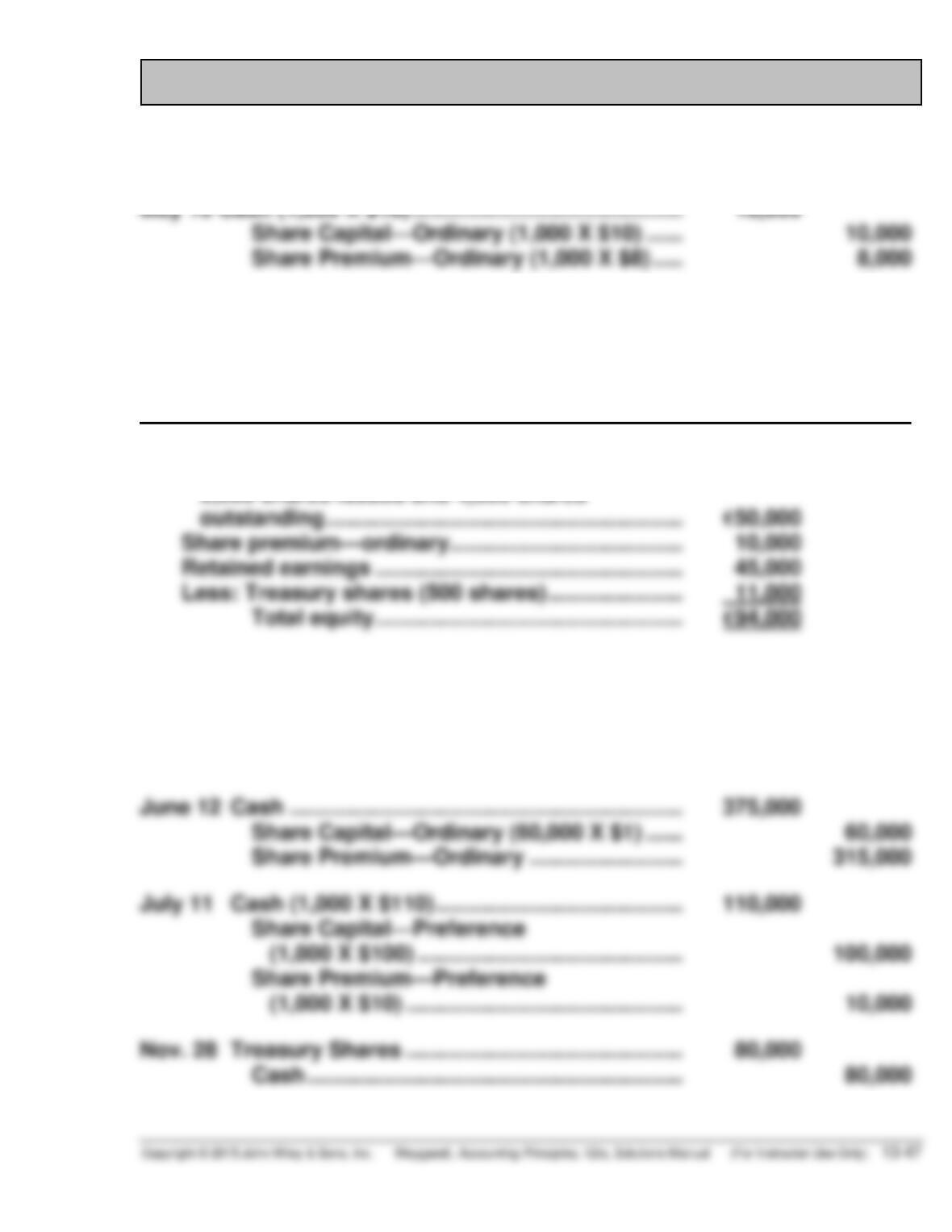

Mar. 2 Organization Expense ……………………………… 30,000

Share Capital—Ordinary (5,000 X $1) …….. 5,000

Share Premium—Ordinary ……………………. 25,000

Nov. 28 Treasury Shares ……………………………………… 80,000

Cash ……………………………………………………. 80,000

IFRS 13-4 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) (1) Total Equity …………………… €27,723,000,000