13

Planning and Budgeting

Solutions to Review Questions

13–1.

Next period’s budget has more detail because it is closer in time than the longer-range

13–2.

13–3.

Answers will vary, but examples include:

13–4.

The master budget links long-term objectives and short-term, tactical plans.

Organization goals are broad-based statements of purpose. Strategic plans take the

broad-based statements and expresses them in terms of detailed steps needed to attain

13–5.

Because middle management has better knowledge about operations at lower levels in

the organization, and because budgets are usually used to evaluate performance or

13–6.

Budgeting aids in coordination in a number of ways. By relating sales forecasts to

production activities it is possible to reduce the likelihood of over– or under-production. It

13–7.

Participative budgeting is a process that uses inputs from lower- or middle-management

13–8.

13–9.

13–10.

Solutions to Critical Analysis and Discussion Questions

13–11.

13–12.

Answers will vary. Two possible reasons are (1) smaller firms have less of a “cushion”

13–13.

The earlier the budgeting process is started, the earlier the company will understand

13–14.

Because inventories would be eliminated, the timing of purchases would be closer to

13–15.

The purpose of tying spending to budgets is to ensure that the wishes of the legislature

13–16.

Planning communicates the goals of the organization and can be used to coordinate the

activities of different units in the organization. The control purpose of the budget is to

13–17.

It is common to start the budgeting process with a sales forecast because sales are

13–18.

In organizations where spending is literally tied to the budget, managers often spend

13–19.

A positive balance at the end of the budgeting period does not ensure that there is

13–20.

Answers will vary. Many people will submit a budget in excess of their best guess. Part

13–21.

Answers will vary. Some basic factors are the nature of the product and the nature of

the market. For products that are well established (mature), there might be enough data

Solutions to Exercises

13–22. (15 min.) Estimate Sales Revenues: Stubs-R-Us.

.80

=

market volume in the coming year (as a percent of last year)

.95

=

number of sales in the coming year (as a percent of last year)

13–23. (15 min.) Estimate Sales Revenues: Friendly Financial.

Portfolio

Amount

Interest

Rate

Income

(thousands)

Home equity loans ………………………………………

Securities …………………………………………………..

13–24. (15 min.) Estimate Sales Revenues: Larson, Inc.

Market size last year

=

85,000 units ÷ 0.2

= 425,000 units

Market size next year

=

1.15 x 425,000 units

Company share

=

16% x 488,750 units

=

78,200 units

13–25. (15 min.) Estimate Production Levels: Offenbach & Son.

Offenbach & Son

Production Budget

For the Year Ended December 31

(in units)

Expected sales revenue …………………………………………….

225,000

units

Less: Beginning inventory of finished goods …………………

13–26. (15 min.) Estimate Sales Levels Using Production Budgets: Sunset

Motors, Inc.

Sunset Motors, Inc.

Sales Budget

For the Year Ended December 31

(in units)

units

13–27. (15 min.) Estimate Inventory Levels Using Production Budgets: Flex-Tite.

Flex-Tite

Sales Budget

For the Year Ended December 31

(in units)

Expected sales ………………………………………………………………

900,000

units

Plus: Desired ending inventory (1/12 x 900,000 x 130%) ……..

units

13–28. (15 min.) Estimate Production Levels: Capacity Constraints: Waterloo,

Ltd..

a.

Waterloo Ltd.

Sales Budget

For the Year Ended December 31

(in units)

Expected sales …………………………………………………………

660,000

units

units

13–29. (15 min.) Estimate Production and Materials Requirements: Wyoming

Machines.

a.

Wyoming Machines

Casings Plant

Production Budget

For the Year Ended December 31

(in units)

Expected sales ……………………………………………………………………..

160,000

units

Add: Desired ending inventory of finished goods ……………………….

Total needs ………………………………………………………………………….

Less: Beginning inventory of finished goods ……………………………..

Units to be produced ……………………………………………………………..

units

b.

Wyoming Machines

Casings Plant

Direct Materials Requirements

For the Year Ended December 31

(in units)

Units to be produced ……………………………………………………………….

145,000

Direct materials needed per unit …………………………..…………………..

x 6

ounces

Total production needs (amount per unit times 145,000 units) ………

870,000

ounces

(2 months ÷ 12 months)

x 160,000 x 6 …………………………….

Total direct materials needs ……………………………………………………..

Less: Beginning inventory of materials ……………………………………….

Direct materials to be purchased……………………………………………….

ounces

=

Sales + EB

=

Usage + EB

(6 x 145,000) + (2 ÷ 12) x 160,000 x 6 oz.

13–30. (25 min.) Estimate Purchases And Cash Disbursements: Midland

Company.

a. and b. Midland Company

Merchandise Purchases Budget

For the Period Ended March 31

(in units)

January

February

March

Estimated sales revenue ……………………………..

12,400

17,800

13,200

Total merchandise needs ………………………….

57,600

57,800

44,200

Less: Beginning inventory …………………………….

45,200

Estimated cost per unit ………………………………..

13–31. (25 min.) Estimate Purchases And Cash Disbursements: Lakeside

Components.

a. Lakeside Components

Merchandise Purchase Budget

For the Period Ended July 31

(in units)

June

July

Estimated sales ………………………………………….

12,900

10,500

Total merchandise needs …………………………….

23,400

21,600

Merchandise to be purchased ……………………….

11,400

11,100

b. Payments for these purchases are made as follows:

Month of Delivery

Month of Payment

Total

May

June

July

June ………………………………………………………….

13–32. (15 min.) Estimate Cash Disbursements: Cascade, Ltd.

Cascade, Ltd.

Schedule of Cash Disbursements

For the Period Ended March 31

Payments for purchases prior to February …………………

$ 67,500

Payments for February purchases …………………………...

March purchases ……………………………………………………

Total cash disbursements ……………………………………….

13–33. (15 min.) Estimate Cash Collections: Minot Corporation.

Minot Corporation

Schedule of Cash Collections

For the Month Ended August 31

Collections in August for sales prior to July …………………..

$ 14,400

July sales ………………………………………………………………..

August sales ……………………………………………………………

13–34. (20 min.) Estimate Cash Collections: Ewing Company.

Ewing Company

Schedule of Cash Collections

For the Month Ended September 30

September

June sales ………………………………………………….

$ 5,700a

July sales …………………………………………………..

9,600b

August sales ………………………………………………

September sales …………………………………………

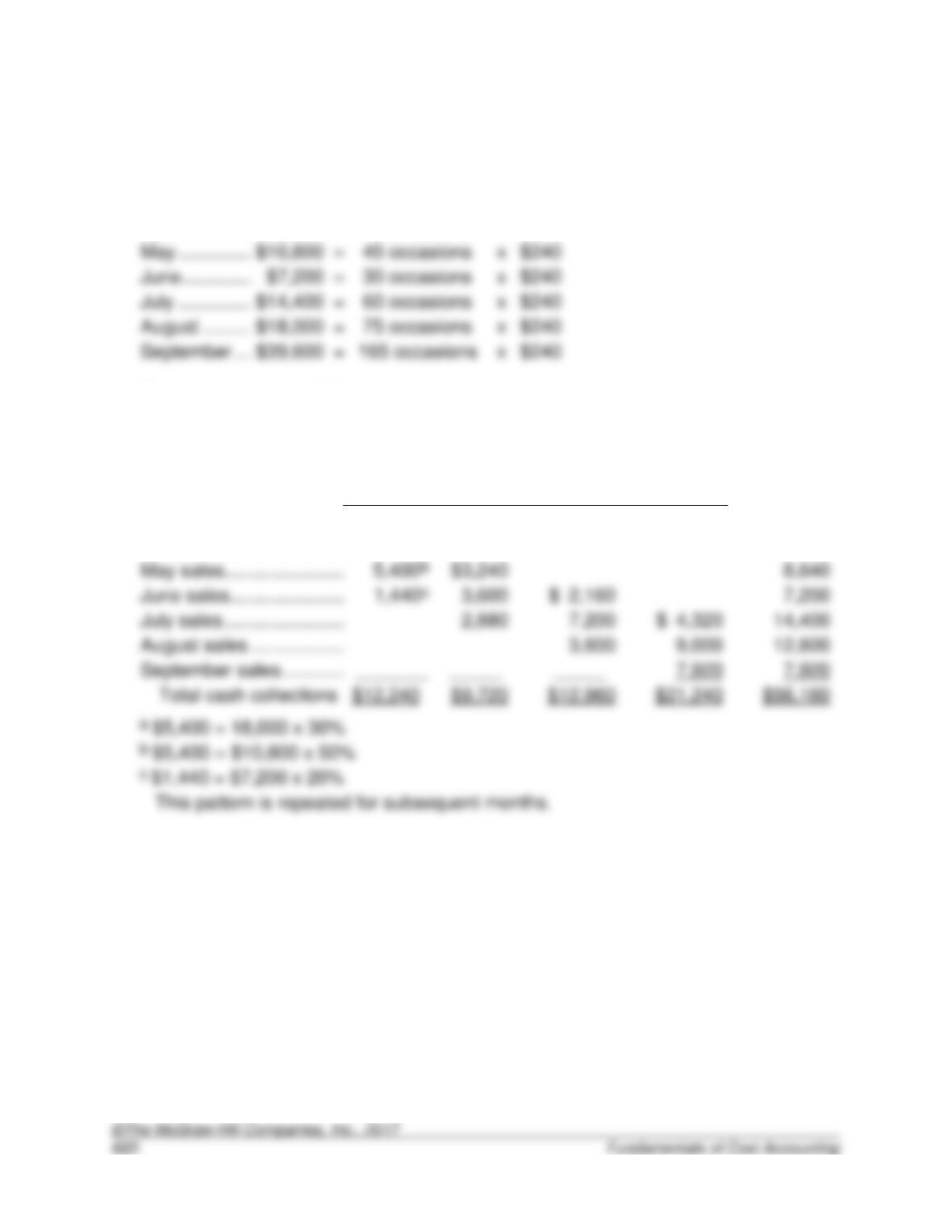

13–35. (30 min.) Estimate Cash Receipts: Scare-2-B-U.

a. Revenues are as follows:

April ………………………………………………………….

$18,000

=

75 occasions

x

$240

May …………………………………………………………..

=

45 occasions

x

$240

July …………………………………………………………..

=

60 occasions

x

$240

August ………………………………………………………

$18,000

=

75 occasions

x

$240

b. Cash receipts are as follows:

Scare-2-B-U

Multiperiod Schedule of Cash Receipts

Cash Receipts in Month of:

Total Cash

Receipts for

April

May

June

July

Period

April sales ………………………………………………….

$ 5,400a

$ 5,400

June sales………………………………………………….

July sales …………………………………………………..

2,880

September sales …………………………………………

_______

_____

7,920

7,920

13–36. (30 min.) Estimate Cash Receipts: Varmit-B-Gone.

Revenues are as follows:

March …..

$28,800

=

0.6 calls

x

600 subscribers

x

$80

April …….

50,400

=

0.9 calls

x

700 subscribers

x

$80

June …….

=

2.5 calls

x

x

$80

July ……..

=

3.0 calls

x

x

$80

Collections of these revenues are expected according to the following schedule:

Varmit-B-Gone

Multiperiod Schedule of Cash Receipts

Cash Receipts in Month of:

Total Cash

Receipts

May

June

July

August

for Period

March sales …………………………..………………….. ($15,000)

April sales …………………………………………………. ($27,000)

June sales…………………………………………………. ($187,500)

July sales ………………………………………………….. ($225,000)

13–37. (30 min.) Prepare Budgeted Financial Statements: Varmit-B-Gone.

Varmit-B-Gone

Budgeted Income Statement

For the Month of September

Calculations

Sales revenue …………………………………………….

$207,360

(90% x 1,500) x (80% x 2.4) x $80

Less service costs:

Variable costs ………………………………………….

$ 17,280

(.72a x $24,000)

Maintenance and repair …………………………….

(1.01 x $22,000)

Depreciation ……………………………………………

(no change)

Total service costs ………………………………………

Marketing and administrative:

Marketing (variable) …………………………………

(.72a x $14,500)

Administrative (fixed) ……………………………….

(1.05 x $55,000)

Total marketing and administrative costs ………..

Total costs ………………………………………………….

$149,690

13–38. (15 min.) Prepare Budgeted Financial Statements: Cycle-1

Cycle-1

Budgeted Income Statement

November

Calculations

Sales revenue (360 units @ $540/unit) ………….

$194,400

($180,000 x 1.20 x .90)

Less

Manufacturing costs:

Variable ……………………………………………….

Depreciation (fixed) ………………………………

(unchanged)

Total manufacturing costs …………………………….

Gross profit margin ………………………………………

Less:

Marketing and Administrative

Fixed costs (cash) ………………………………..

Depreciation (fixed) ………………………………

(unchanged)

Total marketing and administrative costs ………..

13–39. (15 min.) Prepare Budgeted Financial Statements: Carreras Café.

Carreras Café

Budgeted Income Statement

June

Calculations

($15 x 4,200 x 0.60 x 1.25)

Sales revenue

Less

Service costs:

Food ……………………………………………………

($16,800 x 0.60)

($5,750 x 0.60)

Fixed service costs ………………………………

(unchanged)

Total service costs ………………………………………

Gross profit margin ………………………………………

Less:

Marketing and Administrative

Marketing (variable) ……………………………..

Administrative ……………………………………..

(unchanged)

Total marketing and administrative costs ………..

13–40. (15 min.) Budgeting in a Service Organization: Executive Solutions.

Executive Solutions

Budgeted Income Statement

May and June

May

June

Revenues:

Managers (@ $900) …………………………...

$1,080,000

$675,000

Staff (@ $450) …………………………..……….

2,880,000

2,025,000

Total revenue ………………………………..

Manager compensation (@ $225) …………

$1,740,000

SG&A ……………………………………………….

Marketing ………………………………………….

$2,865,000

13–41. (15 min.) Budgeting in a Service Organization: Jolly Cleaners.

Jolly Cleaners

Budgeted Income Statement

April

April

Revenues:

Commercial (48 @ $1,400) ……………………………….

$67,200

(a)

Residential (176 @ $300) …………………………………

52,800

(b)

Total revenue ……………………………………………..

$120,000

Expenses:

Cleaner compensation (4,160 hours @ $15) ……….

(c)

(c)

SG&A …………………………………………………………….

30,000

(d)

Other expenses ……………………………………………….

(d)

Total expenses …………………………..……………….

13–42. (15 min.) Budgeting in a Service Organization: Solving for Unknown: Jolly

Cleaners.

The contribution margin for a residential client is:

The contribution margin for a commercial client is:

To check:

Jolly Cleaners

Budgeted Income Statement

July

July

Revenues:

Commercial (50 @ $1,400) ……………………………….

$70,000

(a)

Residential (170 @ $300) …………………………………

51,000

(b)

Total revenue ……………………………………………..

Expenses:

Cleaner compensation (4,200 hours @ $15) ……….

(c)

Supplies (4,200 hours @ $5) …………………………….

21,000

(c)

SG&A …………………………………………………………….

(d)

Other expenses ……………………………………………….

(d)

Total expenses …………………………..……………….

13–43. (15 min.) Incentives and Sales Forecasts—Ethical Issues: Northwest

Hardware.

a. One explanation is that Lloyd has better (more specific) local knowledge about

b. The first explanation is the same as in requirement (a); Lloyd has better information.

13–44. (15 min.) Budget Revisions—Ethical Issues: Galaxy Electronics.

a. Elizabeth is probably hoping that because the company is committed to the aircraft

guidance program, it will not cut funding for that program and she can protect the other

projects, including her favorite.

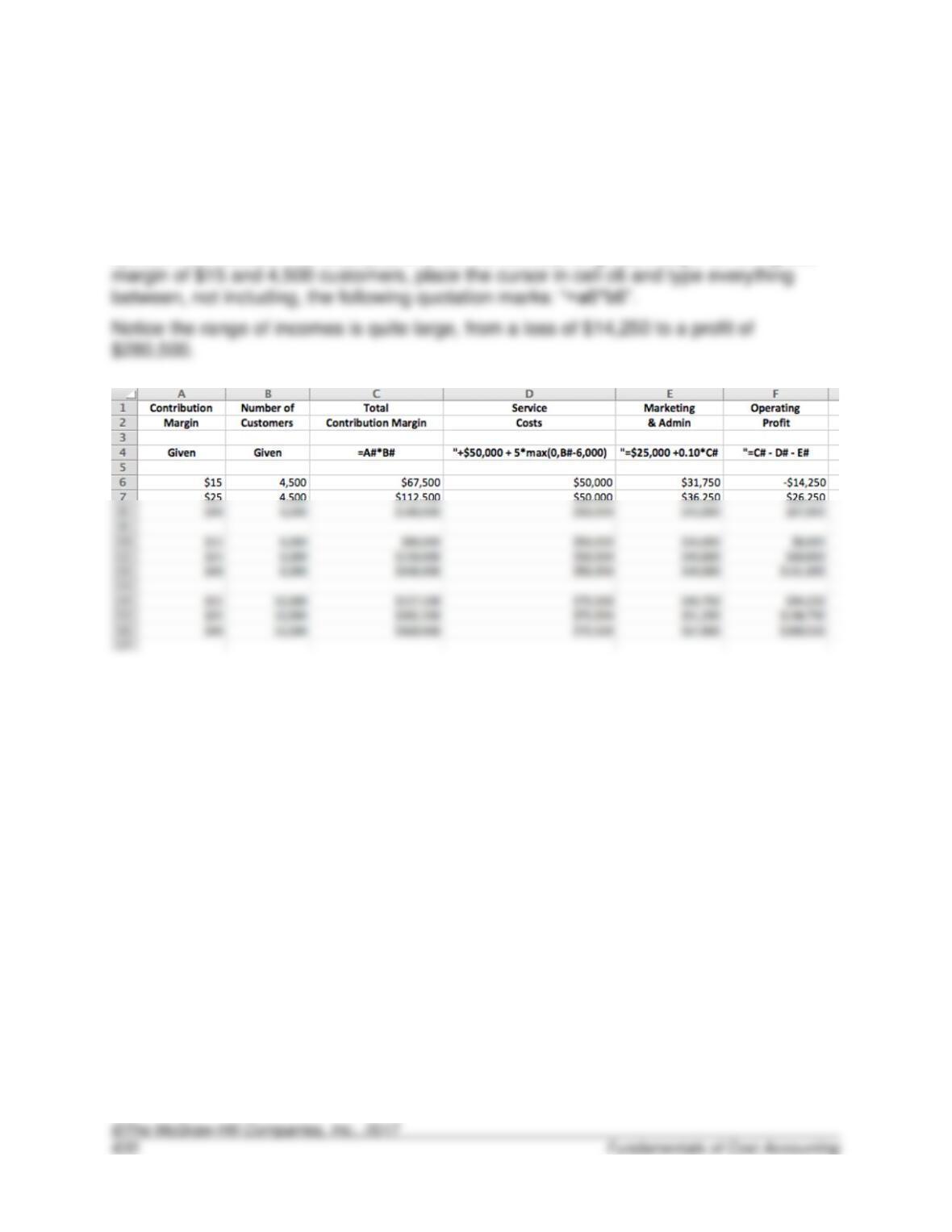

13–45. (15 min.) Sensitivity Analysis: Sanjana’s Sweet Shoppe.

The following is an Excel screenshot of the spreadsheet. In typing the formulas, shown

in row 2, do not enter the opening quote (“). Replace the “#” in the formula with the

13–46. (15 min.) Sensitivity Analysis: Classic Limo, Inc.

The following is an Excel screenshot of the spreadsheet. In typing the formulas, shown

in row 2, do not enter the opening quote (“). Replace the “#” in the formula with the

specific row number. For example, to enter the formula for gross margin for unit gross

Solutions to Problems

13–47. (30 min.) Prepare Budgeted Financial Statements: Pepper Products.

Pepper Products

Budgeted Income Statement

For Year 2

Calculations

Sales revenue …………………………………………….

$3,113,625a

$2,850,000 x 0.95 x 1.15

Manufacturing costs:

Materials …………………………………………………

$168,000 x 0.95 x 1.12

Other variable costs ………………………………….

$142,400 x 0.95 x 0.90

Fixed cash costs ………………………………………

$327,600 x 1.04

Depreciation (fixed) …………………………………

$999,000 (unchanged)

Total manufacturing costs …………………………….

Marketing and administrative costs:

Marketing (variable, cash) ………………………..

$422,400 x 0.95

Marketing depreciation ……………………………..

$149,600 (unchanged)

Administrative (fixed, cash) ……………………….

Administrative depreciation ……………………….

Total marketing and administrative costs ………..

Total costs ………………………………………………….

13–48. (10 min.) Estimate Cash from Operations: Pepper Products.

Pepper Products

Cash Basis Budgeted Income Statement

For Year 2

Sales revenue …………………………………………….

$3,113,625

Manufacturing costs (cash):

Materials …………………………………………………

$ 178,752

Other variable costs ………………………………….

Fixed cash costs ………………………………………

Total cash manufacturing costs……………………..

$ 641,208

Marketing and administrative costs:

Marketing (variable, cash) ………………………..

Administrative (fixed, cash) ……………………….

Total cash marketing and administrative costs ..

Total cash costs ………………………………………….

13–49. (30 min.) Prepare Budgeted Financial Statements: Gulf States

Manufacturing.

Gulf States Manufacturing

Budgeted Income Statement

For Year 2

Calculations

Sales revenue …………………………………………….

$2,781,000

$2,500,000 x 1.08 x 1.03

Manufacturing costs:

Materials …………………………………………………

$ 457,920

$400,000 x 1.08 x 1.06

Variable cash costs ………………………………….

$545,000 x 1.08 x 0.95

Fixed cash costs ………………………………………

$216,000 x 0.91

Depreciation (fixed) …………………………………

$267,000 – $29,100 + $42,000

Total manufacturing costs …………………………….

$1,493,550

Marketing and administrative costs:

Marketing (variable, cash) ………………………..

$285,000 x 1.08

Marketing depreciation ……………………………..

Administrative (fixed, cash) ……………………….

$270,300 x 1.10

Administrative depreciation ……………………….

Total marketing and administrative costs ………..

Total costs ………………………………………………….

13–50. (10 min.) Estimate Cash from Operations: Gulf States Manufacturing.

Gulf States Manufacturing

Cash Basis Budgeted Income Statement

For Year 2

Sales revenue …………………………………………….

$2,781,000

Manufacturing costs:

Materials …………………………………………………

$ 457,920

Variable cash costs ………………………………….

559,170

Fixed cash costs ………………………………………

Total manufacturing costs …………………………….

$1,213,650

Marketing and administrative costs:

Marketing (variable, cash) ………………………..

Administrative (fixed, cash) ……………………….

Total cash marketing and administrative costs ..

Total cash costs ………………………………………….

13–51. (25 min.) Prepare A Production Budget: EcoSacks.

EcoSacks

Production Budget

Coming Year

(in units)

Expected Sales ………………………………………………..

540,000

units

Add: Desired ending inventory of finished goods …..

210,000

Less: Beginning inventory of finished goods …………

120,000

Units to be produced …………………………………………

630,000

units

Alternative method:

First, compute the estimated production:

P

=

Sales + EB – BB

P

=

Sales + (210,000 – 120,000)

=

units

Next estimate the costs:

Direct materials

Cotton 630,000 x 1 yard x $4.00 x 1.20 …………..

$3,024,000

$5,670,000

Overhead:

Indirect labor ……………………………………………….

630,000 x $0.60

$ 378,000

Indirect materials …………………………………………

630,000 x $0.20

Equipment costs ………………………………………….

Building occupancy ……………………………………..

13–52. (25 min.) Prepare A Production Budget: Haggstrom, Inc.

Haggstrom, Inc.

Production Budget

Year 2

(in units)

Expected Sales ………………………………………………..

210,000

units

Add: Desired ending inventory of finished goods …..

Less: Beginning inventory of finished goods …………

Alternative method:

First, compute the estimated production:

P

=

Sales + EB – BB

P

=

Sales + (10,000 – 20,000)

=

units

Next estimate the costs:

Direct materials

Steel 200,000 x 3 pounds x $0.50 x 0.90 ………..

Alloy 200,000 x 0.5 pounds x $2.00 ……………….

Indirect materials …………………………………………

Indirect labor ……………………………………………….

Plant and equipment depreciation ………………….

Miscellaneous ……………………………………………..

©The McGraw-Hill Companies, Inc., 2017

Solutions Manual, Chapter 13 637

13–53. (25 min.) Sales Expense Budget: SPU, Ltd.

Budgeted

Item

January

Adjustments

Typical Month

Sales commissions ……………………………………..

$364,500

x

1.14 x 0.90

=

$373,977

Sales staff salaries ………………………………………

86,400

x

1.06

=

91,584

x

Building lease payment ………………………………..

=

Utilities ………………………………………………………

x

1.03

=

11,433

x

Depreciation ……………………………………………….

33,750

+

=

34,192

Marketing consultants …………………………..……..

+

$64,500

=

13–54. (30 min.) Budgeted Purchases And Cash Flows: Mast Corporation.

BB + P

=

Sales + EB

(120% x 11,900) + P

=

11,900 + (120% x 11,400)

=

11,900 + 13,680

=

11,900 + 13,680 – 14,280

=

11,300 units

BB + P

=

Sales + EB

(120% x 11,400) + P

=

11,400 + (120% x 12,000)

=

11,400 + 14,400

=

11,400 + 14,400 – 13,680

=

12,120 units

c. $691,896

x

13–54. (continued)

e. 49,040

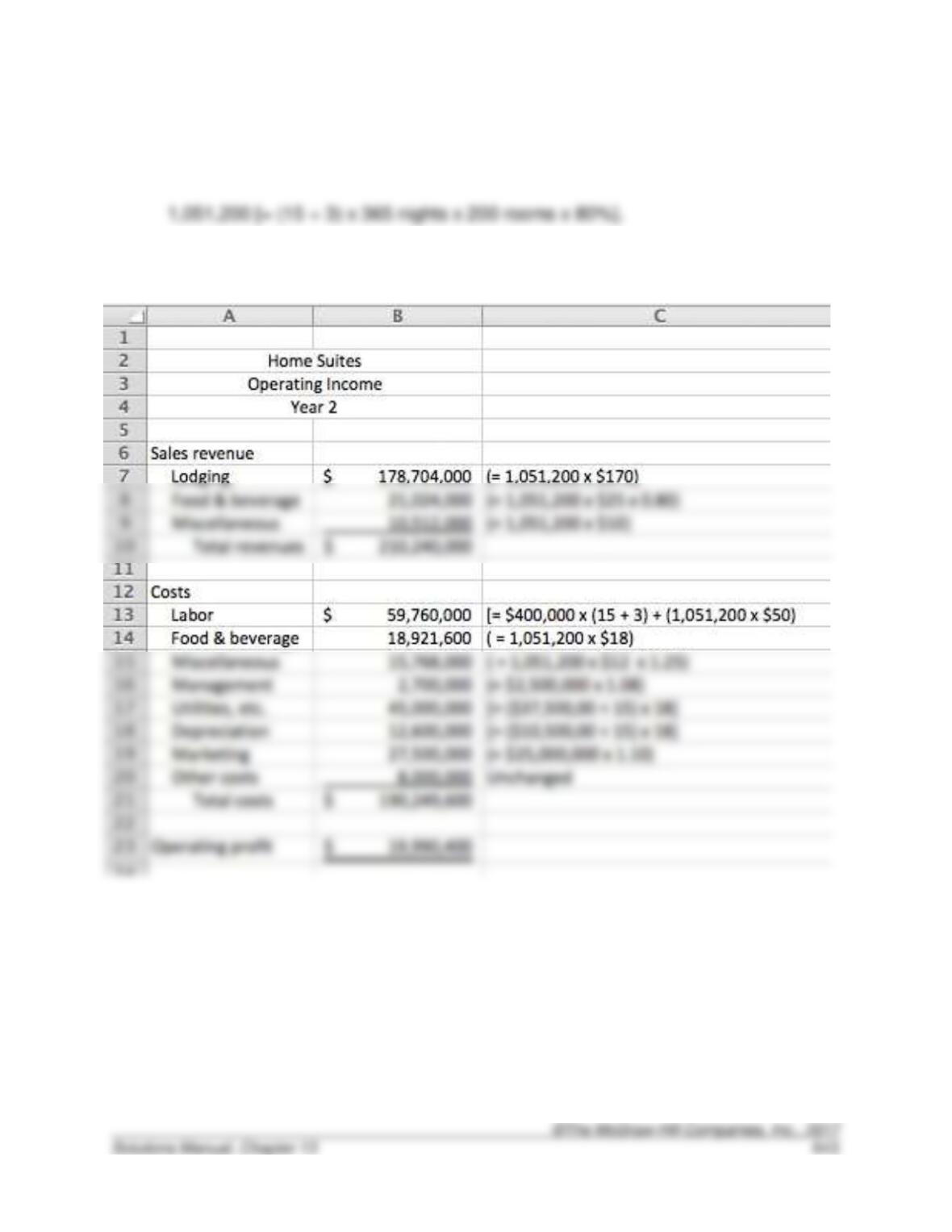

13–55. (45 min.) Prepare Budgeted Financial Statements: HomeSuites.

It is useful to calculate some variable costs per night and property in Year 1:

Average variable labor cost per night:

For Year 2, the estimated number of nights is:

13–55. (continued)

13–56. (30 min.) Budgeted Purchases And Cash Flows: Home Suites.

a. Under the “High Price” strategy, the number of nights will be:

The estimated budget is:

13-56. (continued)

a. Under the “High Occupancy” strategy, the number of nights will be:

The estimated budget is:

13–56. (continued)

13–57. (40 min.) Comprehensive Budget Plan: Brighton, Inc.

a. (1)

Brighton, Inc.

Schedule Computing Production

Budget (Units)

For April, May, and June

April

May

June

Budgeted sales—Units ………………………………..

600,000

450,000

600,000

Total to be accounted for ……………………………..

690,000

570,000

720,000

Less inventory on hand at beginning of month ..

120,000

120,000

(2)

Schedule Computing Raw Materials Inventory

Purchase Budget (Pounds)

For April and May

April

May

Budgeted production—Pounds (1/4 lb. per Unit)a …..

142,500

120,000

Inventory required at end of monthb ……………………..

48,000

60,000

Total to be accounted for …………………………………….

13–57. (continued)

b.

Brighton, Inc.

Projected Income Statement

For the Month of May

Sales revenue (450,000 Units at $4) …………………………………

$1,800,000

Less: Cash discounts on Sales …………………………………………

$ 18,000

Estimated bad debts (1/2 percent of gross sales) ………………

9,000

27,000

Net Sales ………………………………………………………………………

$1,773,000

Fixed Cost …………………………………………………………………..

Gross profit on sales ………………………………………………………..

Expenses:

Selling (10 percent of gross sales) …………………………………

Administrative ($165,000 per month) ………………………………

Interest expense (.01 x $500,000) ………………………………….

13–58. (60 min.) Comprehensive Budget Plan: Panther Corporation

Panther Corporation

Budgeted Income Statement

(in thousands)

Actual

For the Year Ended

December 31,

(Year 1)

Budgeted

For the Year Ended

December 31,

(Year 2)

Revenue:

Sales revenue ………………………………………

Other income ……………………………………….

Total Revenue …………………………………..

Expenses:

Cost of goods manufactured &

sold:

Materials ……………………………………………..

$ 528,000

$ 852,000

Direct labor …………………………………………..

Variable overhead …………………………………

(Depreciation and other)……………………..

Beginning inventory ………………………………….

Ending inventory ………………………………………

Marketing:

Salaries …………………………..…………………..

Commissions ……………………………………….

Promotions and advertising…………………….

Administrative:

Salaries …………………………..…………………..

$ 56,000

$ 64,000

Travel ………………………………………………….

Office costs ………………………………………….

Total expenses ……………………………………..

13–58. (continued)

Panther Corporation

Budgeted Balance Sheet

(in thousands)

Budgeted

December 31,

Year 2

Current Assets

Cash ………………………………………………………

$ 4,800

Accounts receivable …………………………………

320,000

Inventory …………………………………………………

Income tax receivable ……………………………….

Total current assets ………………………………

$794,200

Plant and equipment ……………………………………

520,000

Less: Accumulated depreciation …………………

164,000

Total assets ………………………………………….

Current liabilities

Accounts payable …………………………………….

Accrued payable ………………………………………

Notes payable ………………………………………….

200,000

Total current liabilities …………………………...

$473,000

Shareholders’ equity

Common stock …………………………………………

280,000

Retained earnings ……………………………………

Total shareholders’ equity ………………………

13–58. (continued)

a Inventory

Units:

Added to inventory 450,000 – 400,000 …………..

units

Ending inventory …………………………..…………….

units

Cost:

Manufacturing costs …………………………………

$2,295,000

Units manufactured ………………………………….

Cost per unit ($2,295,000 450,000) …………

Ending units …………………………………………….

b Income tax:

Sales & other income …………………………………..

$2,436,000

Cost of goods sold ………………………………………

$2,028,000

Selling expense ………………………………………….

General & administrative expense …………………

Total cost………………………………………………..

$2,462,000

Tax loss …………………………………………………….

Tax rate …………………………………………………….

Cash revenue

Annual membership fees ……………………………..

$804,430

Solutions to Integrative Case

13–59. (40 min.) Prepare Cash Budget for Service Organization: Cortez Beach

Yacht Club.

The income statement is on a cash basis, hence we start with a budgeted income

statement.

a. Cortez Beach Yacht Club

Budgeted Statement of Income (Cash Basis)

For the Year 10

Cash costs

Manager’s salary and benefits ($72,000 x 1.15) ……………………………….

$ 82,800

Regular employees’ wages and benefits ($380,000 x 1.15) ……………….

437,000

Lesson and class employee wages and benefits (given) …………………….

Supplies ($32,000 x 1.25) ……………………………………………………………..

Utilities (heat and light) ($44,000 x 1.25) …………………………………………

Miscellaneous ($4,000 x 1.25) ……………………………………………………….

Total cash expenses ……………………………………………………….…………

Cash income …………………………………………………………………………………..

Additional Cash Flows

Cash payments:

Mortgage payment ………………………………………………………………………..

$ 60,000

Accounts payable balance at 10/31/Year 9 ………………………………………

Accounts payable on equipment at 10/31/Year 9 ………………………………

Planned new equipment purchase ………………………………………………….

Total cash payments ………………………………………………………………….

Cash inflows from income statement ………………………………………………….

150,513

Beginning cash balance (including petty cash) …………………………..………..

13-59. (continued)

b. Operating problems that Cortez Beach Yacht Club could experience in Year 10

include:

• The lessons and classes contribution to cash decreased because the projected

c. The manager’s concern with regard to the Board’s expansion goals is justified. The

Year 10 budget projections show only a minimal increase in the cash balance. The

total cash available is well short of the cash needed for the land purchase over and