1. No. Common stock with a higher par is not necessarily a better investment than common

stock with a lower par because par is an amount assigned to the shares.

2. The broker is not correct. Corporations are not legally liable to pay dividends until the

dividends are declared. If the company that issued the preferred stock has operating losses,

6. The primary purpose of a stock split is to bring about a reduction in the market price per

share and thus to encourage more investors to buy the company’s shares.

7. a. It has no effect on revenue or expense.

b. It reduces stockholders’ equity by $3,000,000.

8. a. It has no effect on revenue.

b. It increases stockholders’ equity by $3,750,000.

CHAPTER 13

CORPORATIONS: ORGANIZATION, STOCK

DISCUSSION QUESTIONS

TRANSACTIONS, AND DIVIDENDS

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

PE 13-1A

Amount distributed…………………………

…

$ 45,000 $ 123,000 $130,000

Preferred dividend (50,000 shares)………

…

(45,000) (105,000) (75,000)

Common dividend (100,000 shares)……… $0 $ 18,000 $ 55,000

*

Year 1 dividends in arrears of $30,000 ($75,000** – $45,000) plus Year 2 dividends of $75,000

**

$75 par × 50,000 shares × 2% = $75,000

PE 13-1B

Amount distributed…………………………

…

$ 35,000 $ 6,300 $ 80,500

Preferred dividend (14,000 shares)………

…

(18,200) (6,300) (30,100)

Common dividend (70,000 shares)………

…

$ 16,800 $0 $ 50,400

PE 13-2A

May 23 Cash (45,000 shares × $16)

Common Stock (45,000 shares × $4)

Paid-In Capital in Excess of Stated Value—

Common Stock [45,000 shares × ($16 – $4

)

)

Year 1 Year 2 Year 3

Year 1 Year 2 Year 3

PRACTICE EXERCISES

180,000

540,000

720,000

*

**

*

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

PE 13-2B

Jan. 22 Cash 750,000

Common Stock (125,000 shares × $6) 750,000

Feb. 14 Cash 2,560,000

Preferred Stock (32,000 shares × $80) 2,560,000

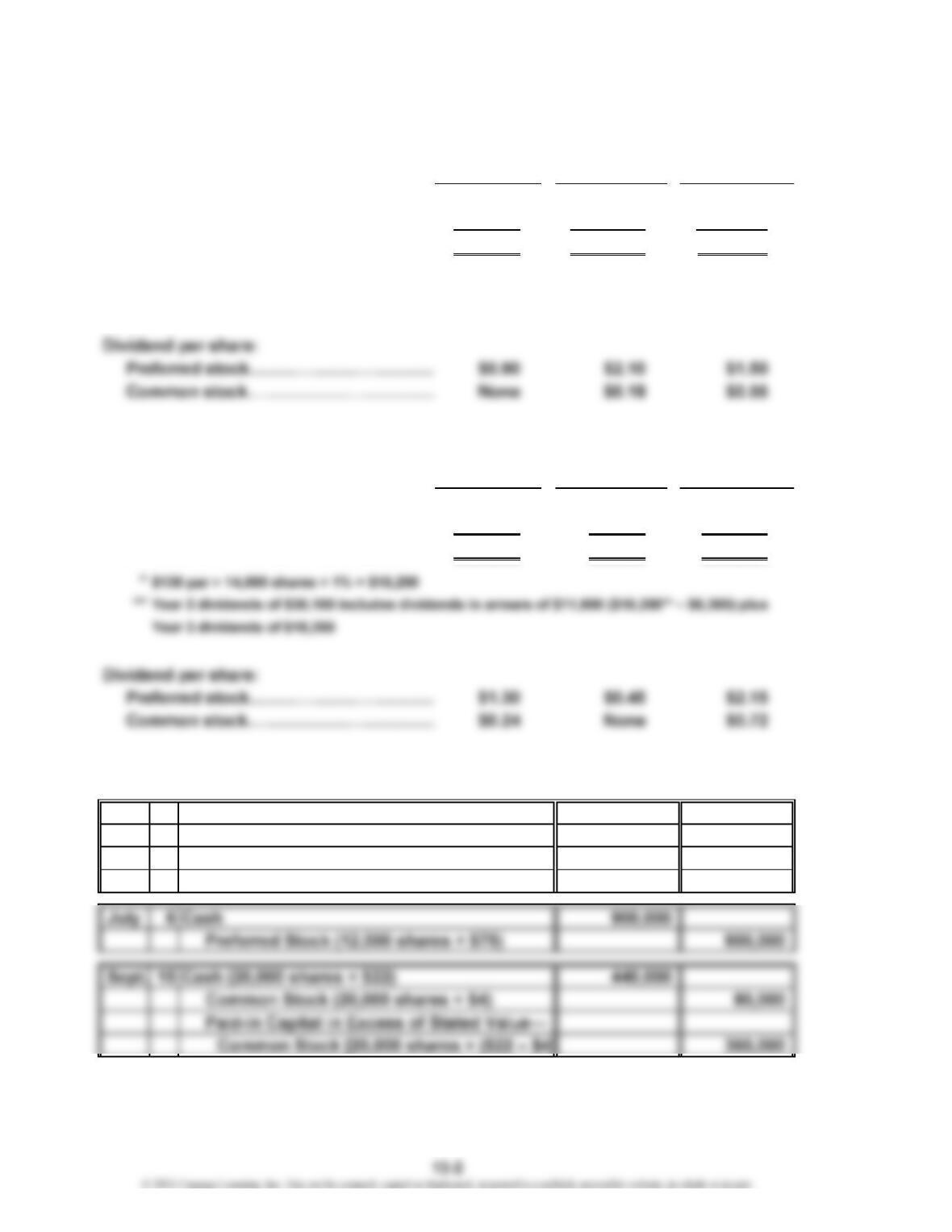

PE 13-3A

Feb. 28 Cash Dividends 428,000

Cash Dividends Payable 428,000

PE 13-3B

Feb. 1 Cash Dividends 195,000

Cash Dividends Payable 195,000

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

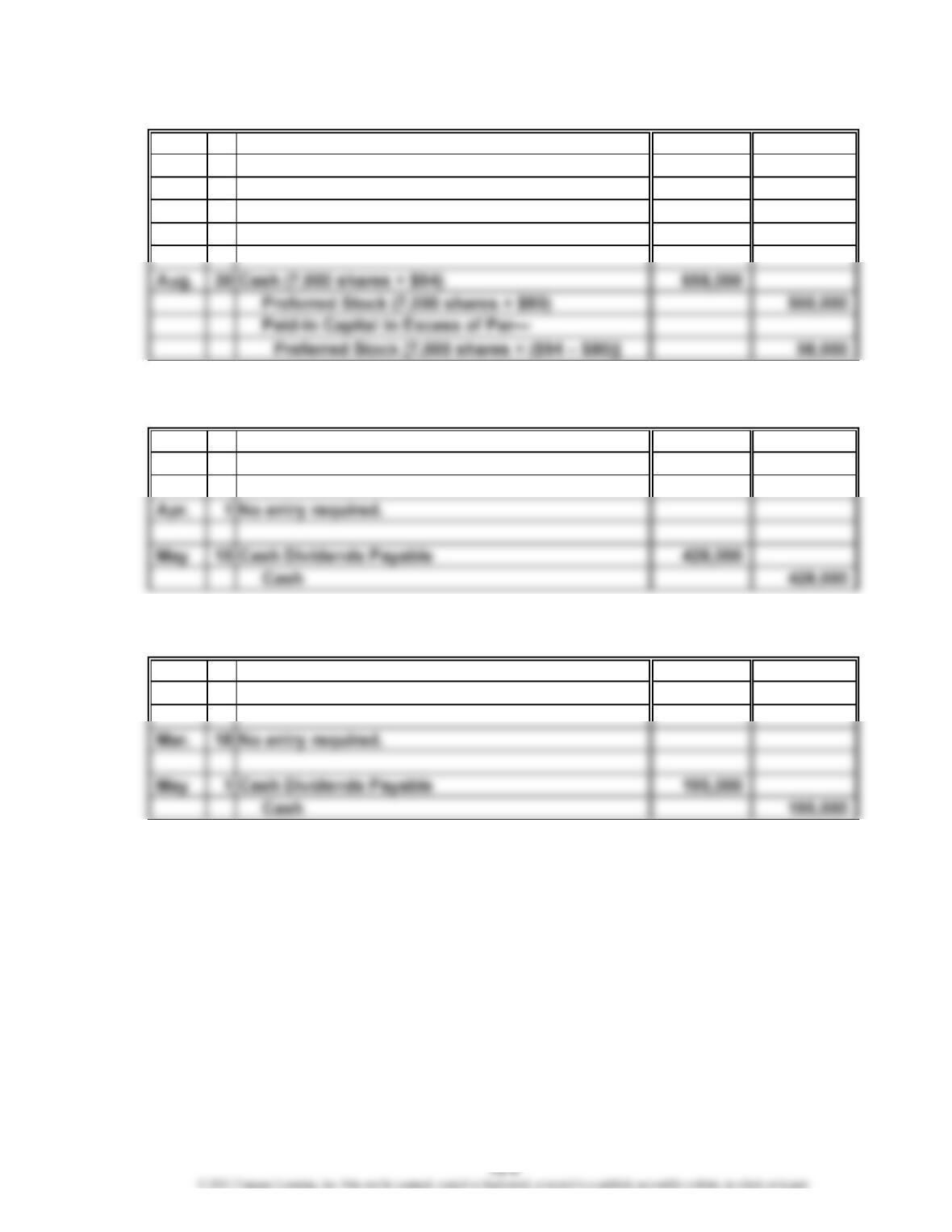

PE 13-4A

Sept. 2 Stock Dividends (900,000 shares × 3% × $44) 1,188,000

Stock Dividends Distributable

(27,000 shares × $26) 702,000

Paid-In Capital in Excess of Par—

Common Stock [$27,000 shares × ($44 – $26)] 486,000

PE 13-4B

June 8 Stock Dividends (370,000 shares × 5% × $51) 943,500

Stock Dividends Distributable

(18,500 shares × $27) 499,500

Paid-In Capital in Excess of Par—

Common Stock [18,500 shares × ($51 – $27)] 444,000

PE 13-5A

Jan. 31 Treasury Stock (18,700 shares × $45) 841,500

Cash 841,500

Oct. 4 Cash (8,100 shares × $37) 299,700

Paid-In Capital from Sale of

Treasury Stock [8,100 shares × ($45 – $37)] 64,800

Treasury Stock (8,100 shares × $45) 364,500

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

PE 13-5B

May 27 Treasury Stock (64,000 shares × $12) 768,000

Cash 768,000

Nov. 14 Cash (23,000 shares × $9) 207,000

Paid-In Capital from Sale of Treasury

Stock [23,000 shares × ($12 – $9)] 69,000

Treasury Stock (23,000 shares × $12) 276,000

PE 13-6A

Paid-in capital:

Common stock, $3 par (200,000

shares authorized, 90,000 shares

issued) $ 270,000

Excess over par 1,196,000

PE 13-6B

Paid-in capital:

Common stock, $120 par (500,000

shares authorized, 212,500 shares

issued) $25,500,000

Excess over par 7,230,000

Stockholders’ Equity

Stockholders’ Equity

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

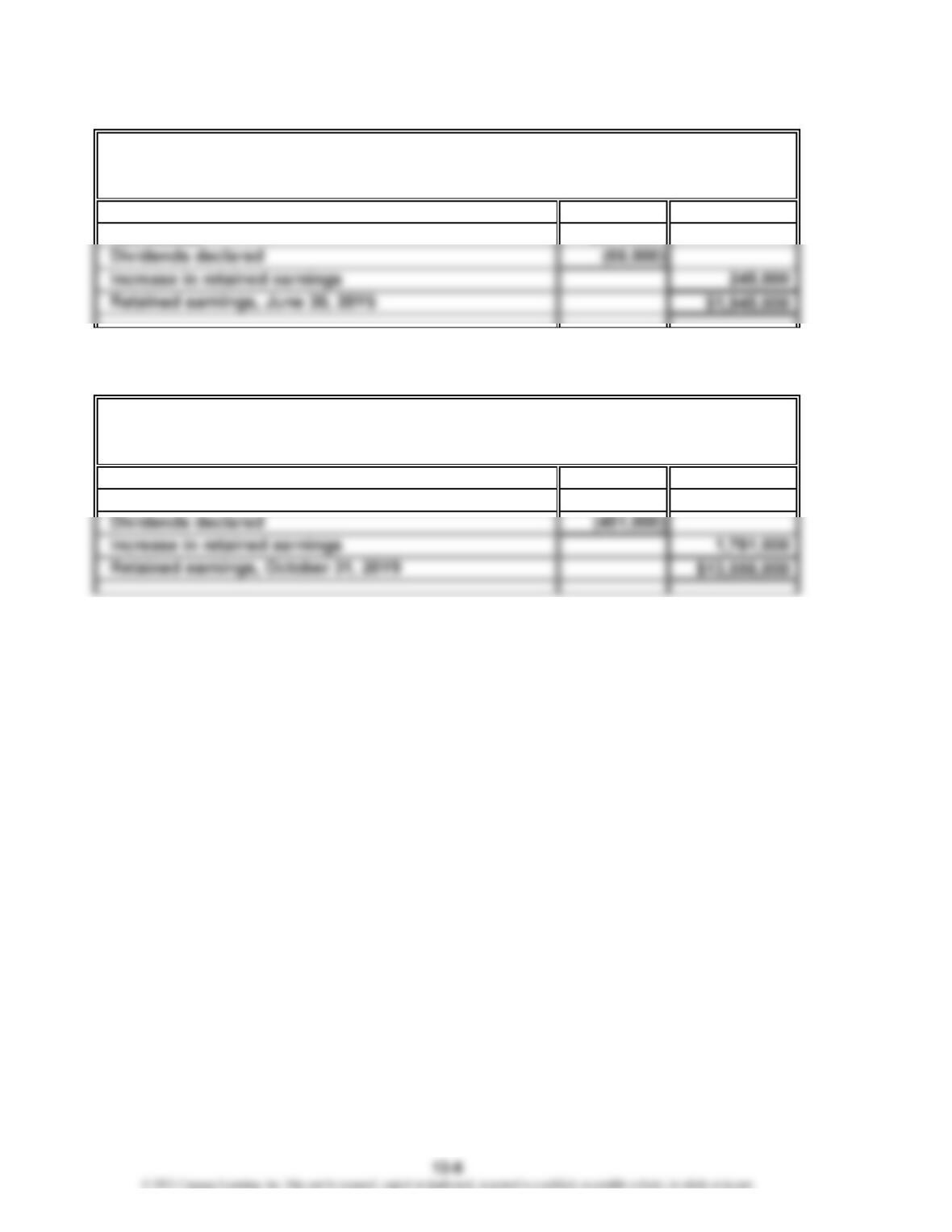

PE 13-7A

Retained earnings, July 1, 20Y4 $1,700,000

Net income

PE 13-7B

Retained earnings, November 1, 20Y8 $11,775,000

Net income

Seismic Inc.

Retained Earnings Statement

For the Year Ended June 30, 20Y5

Haggen Cruises Inc.

$311,000

Retained Earnings Statement

For the Year Ended October 31, 20Y9

$2,232,000

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

PE 13-8A

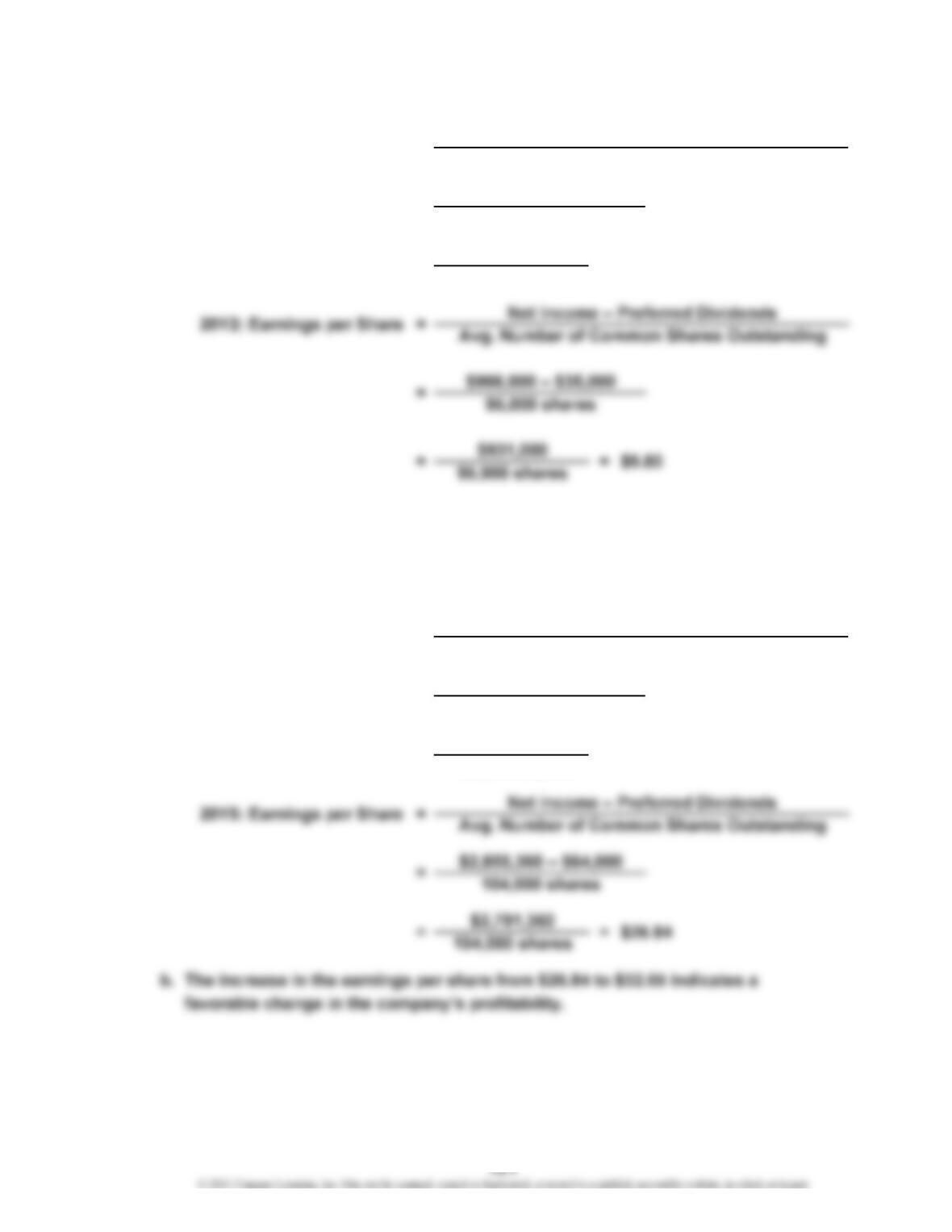

b. The decrease in the earnings per share from $9.80 to $9.25 indicates an

unfavorable change in the company’s profitability.

PE 13-8B

=$4,243,200 – $64,000

128,000 shares

=$4,179,200 = $32.65

128,000 shares

a. 20Y6: Earnings per Share = Net Income – Preferred Dividends

Avg. Number of Common Shares Outstanding

=20Y3: Earnings per Sharea. Avg. Number of Common Shares Outstanding

Net Income – Preferred Dividends

=$775,000 – $35,000

80,000 shares

$9.25= 80,000 shares

$740,000 =

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-1

Amount distributed……………

…

$49,000 $132,000 $146,000 $160,000

Preferred dividend (current)…

…

$49,000 $ 84,000 $ 84,000 $ 84,000

Common dividend………………

…

$— $ 13,000 $ 62,000 $ 76,000

Common shares outstanding…

…

100,000 100,000 100,000

Common dividend per share…

…

$ 0.13 $ 0.62 $ 0.76

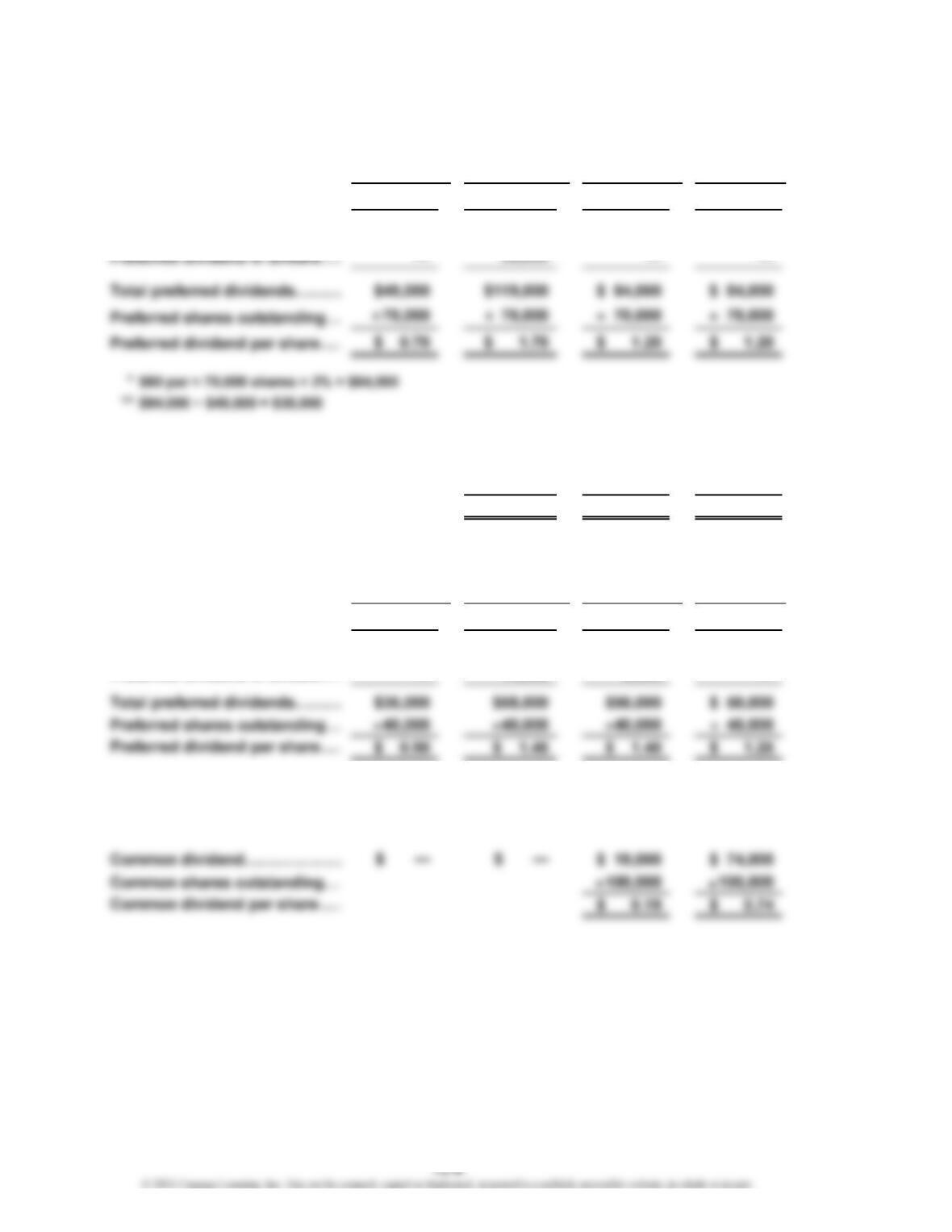

Ex. 13-2

Amount distributed……………

…

$36,000 $58,000 $75,000 $124,000

Preferred dividend (current)…

…

$36,000 $44,000 $50,000 $ 50,000

…

*

Pay dividend in arrears first; $44,000 = $58,000 – $14,000

**

$125 par × 40,000 shares × 1% = $50,000; $50,000 − $36,000 = $14,000

…

…

…

EXERCISES

1st Year 2nd Year 3rd Year 4th Year

2nd Year 3rd Year 4th Year1st Year

*

÷÷÷

*

**

…

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-3

a. Oct. 31 Cash (320,000 shares × $12) 3,840,000

Common Stock (320,000 shares × $5) 1,600,000

Paid-In Capital in Excess of Par—Common

Stock [320,000 shares × ($12 – $5)] 2,240,000

b. $7,080,000 ($1,600,000 + $2,240,000 + $2,700,000 + $540,000)

Ex. 13-4

a. Feb. 12 Cash (1,000,000 shares × $1.20) 1,200,000

Common Stock (1,000,000 shares × $0.25) 250,000

Paid-In Capital in Excess of Stated Value—

Common Stock [1,000,000 shares ×

($1.20 – $0.25)] 950,000

b. $1,410,000 ($250,000 + $950,000 + $150,000 + $60,000)

Ex. 13-5

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-6

a. Cash 100,000

Common Stock (100,000 shares × $1) 100,000

c. Land 60,000

Building 225,000

Interest Payable* 5,200

Mortgage Note Payable 180,000

Common Stock (99,800 shares × $1) 99,800

*

An acceptable alternative would be to credit Interest Expense.

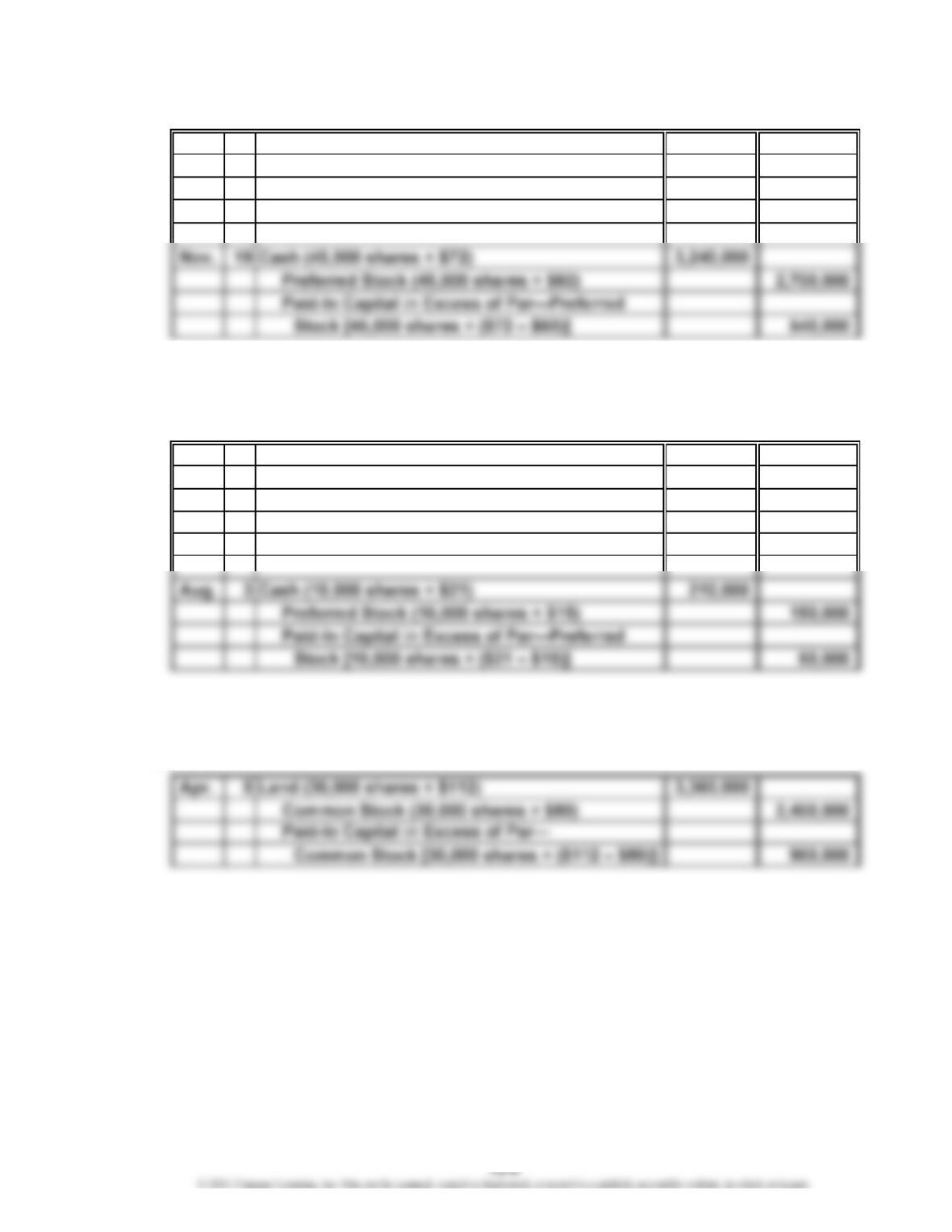

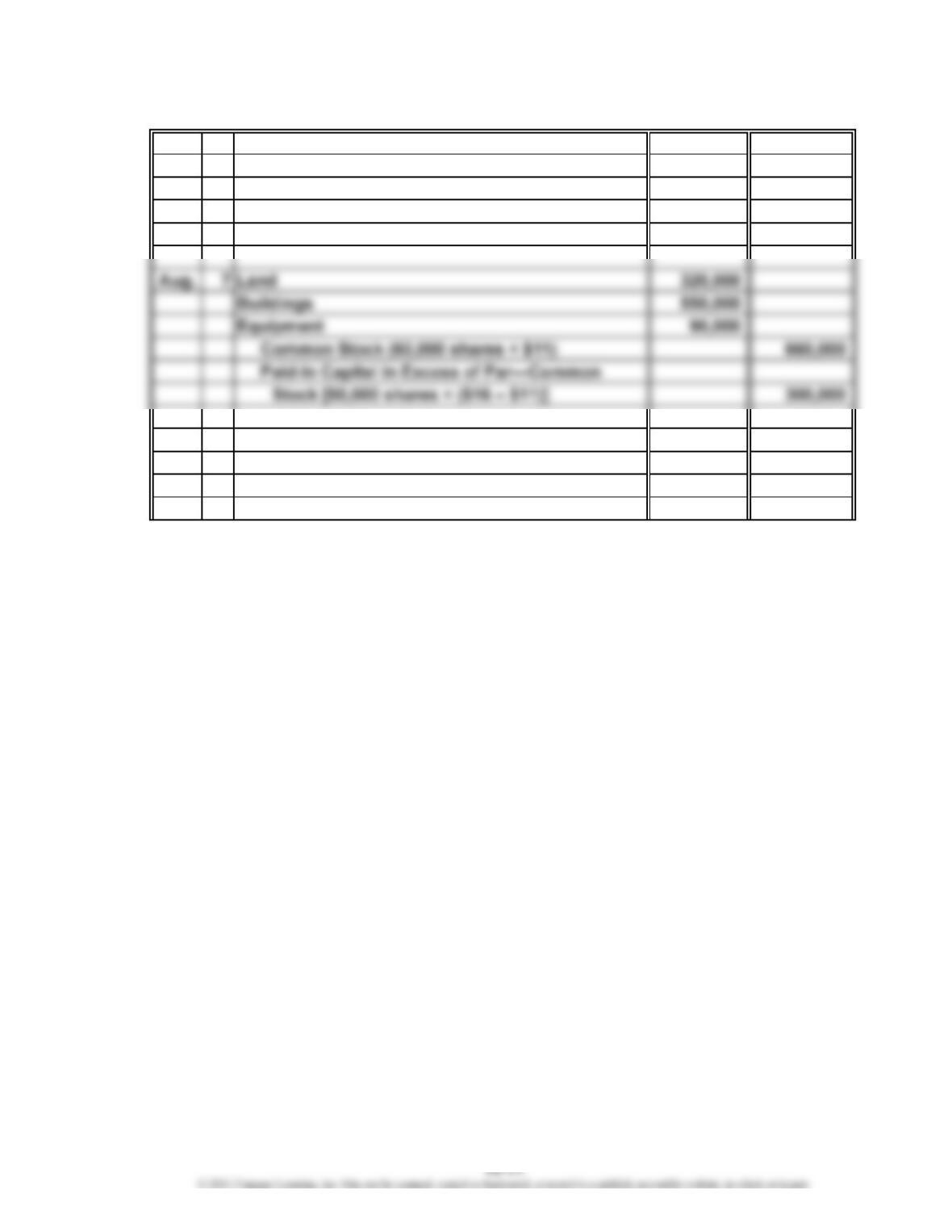

Ex. 13-7

Oct. 1 Buildings 2,380,000

Land 840,000

Preferred Stock (35,000 shares × $80) 2,800,000

Paid-In Capital in Excess of Par—Preferred

Stock [35,000 shares × ($92 – $80)] 420,000

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

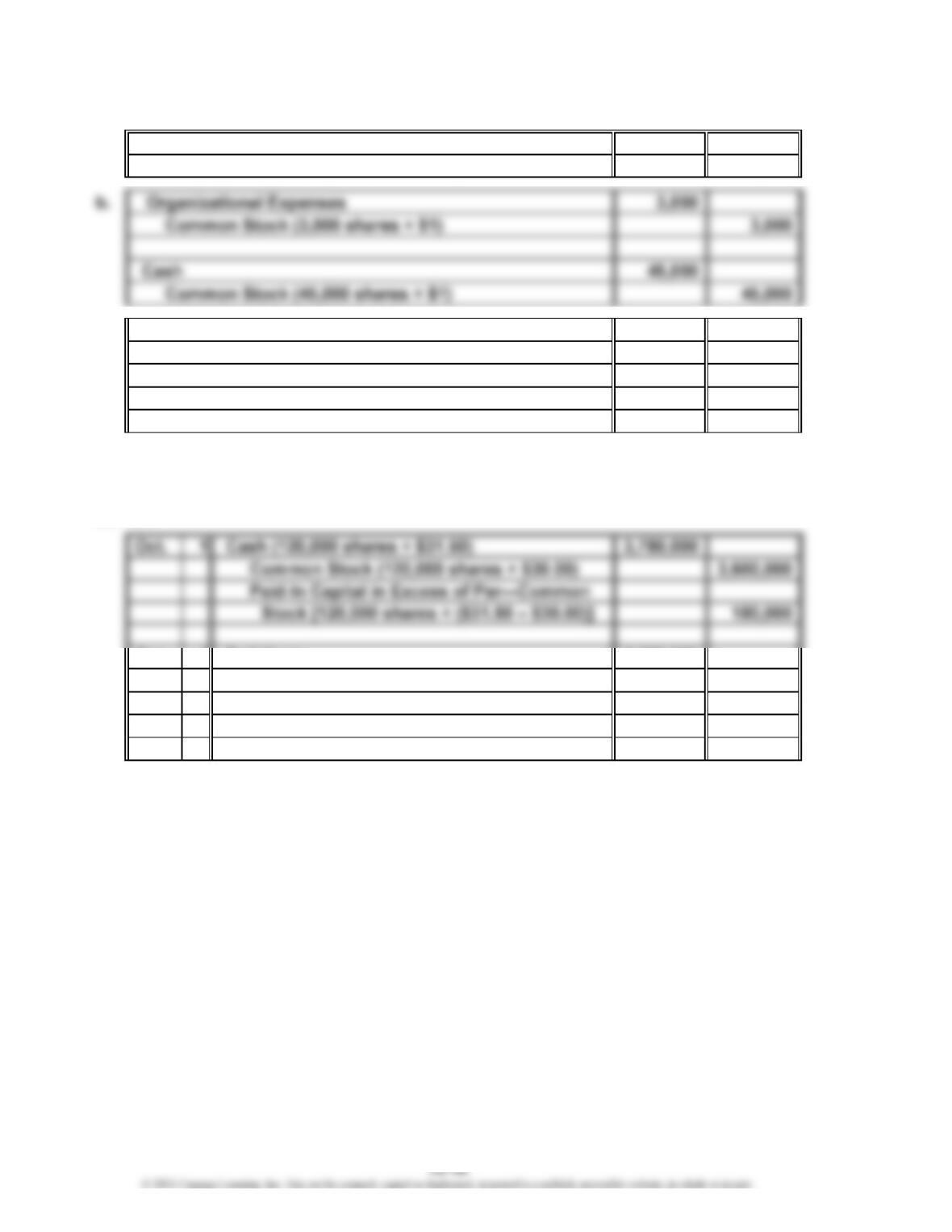

Ex. 13-8

1 Cash 2,860,000

Common Stock (260,000 shares × $11) 2,860,000

1 Organizational Expenses 22,000

Common Stock (2,000 shares × $11) 22,000

20 Cash (30,000 shares × $74) 2,220,000

Preferred Stock (30,000 shares × $70) 2,100,000

Paid-In Capital in Excess of Par—Preferred

Stock [30,000 shares × ($74 – $70)] 120,000

Sept.

July

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-9

12 Cash Dividends 135,000

Cash Dividends Payable 135,000

Ex. 13-10

(2) Stock Dividends Distributable 64,000

Common Stock 64,000

b. (1) $4,000,000 ($3,200,000 + $800,000)

(2)

(3) $29,600,000 ($4,000,000 + $25,600,000)

Ex. 13-11

a. 105,000 shares (35,000 × 3)

b. $90 per share ($270 ÷ 3)

Ex. 13-12

Assets Liabilities

(1) Authorizing and issuing stock

certificates in a stock split 0 0

(2) Declaring a stock dividend 0 0

Jan.

$25,600,000

Stockholders’

Equity

0

0

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

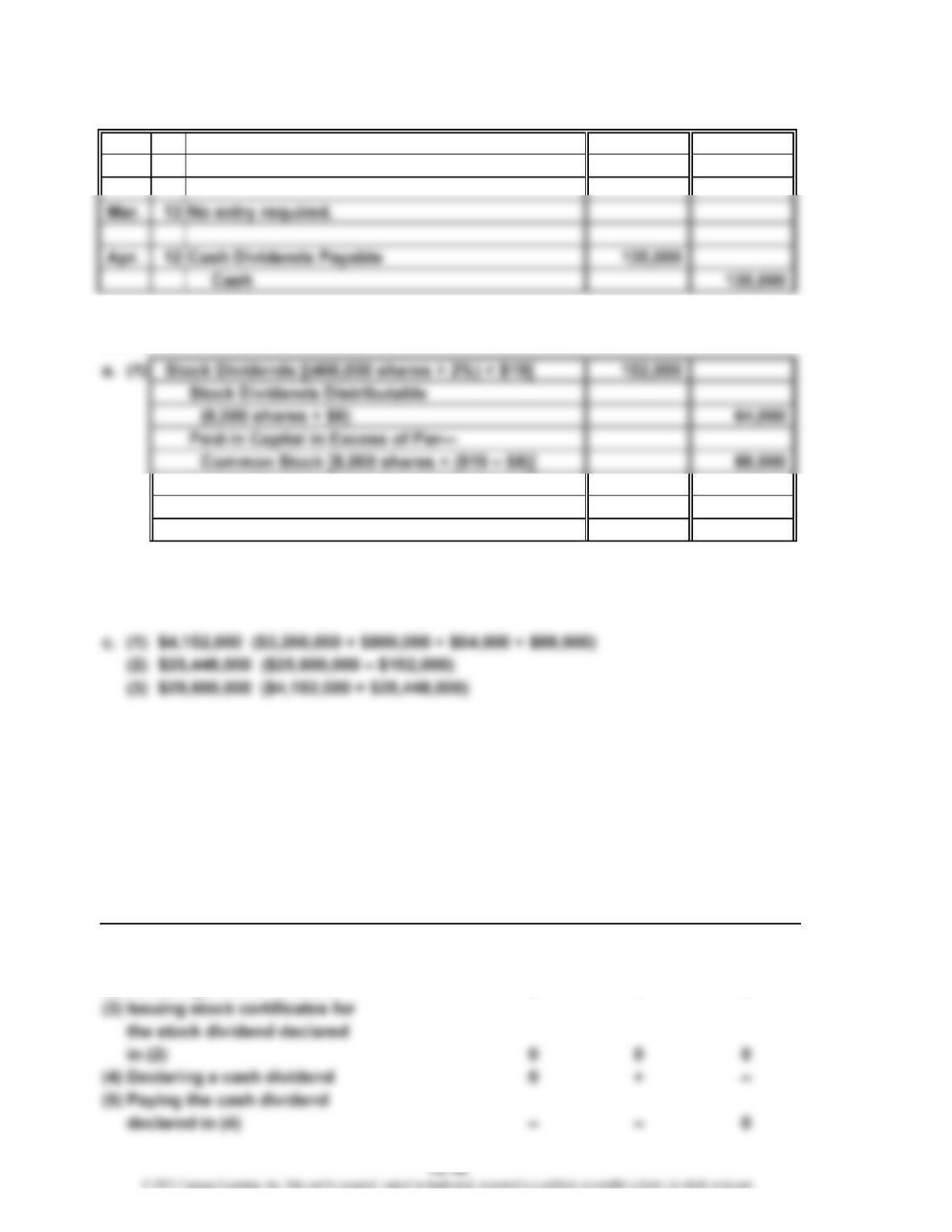

Ex. 13-13

Jan. 8 No entry required. The stockholders’ ledger would

be revised to record the increased number of

shares held by each stockholder.

July 1 Cash Dividends Payable 55,500

Cash 55,500

31 Stock Dividends (150,000 shares × 5% ×

$52 = $390,000) 390,000

Stock Dividends Distributable

(7,500 shares × $40) 300,000

Paid-In Capital in Excess of Par—Common Stock

[7,500 shares × ($52 – $40)] 90,000

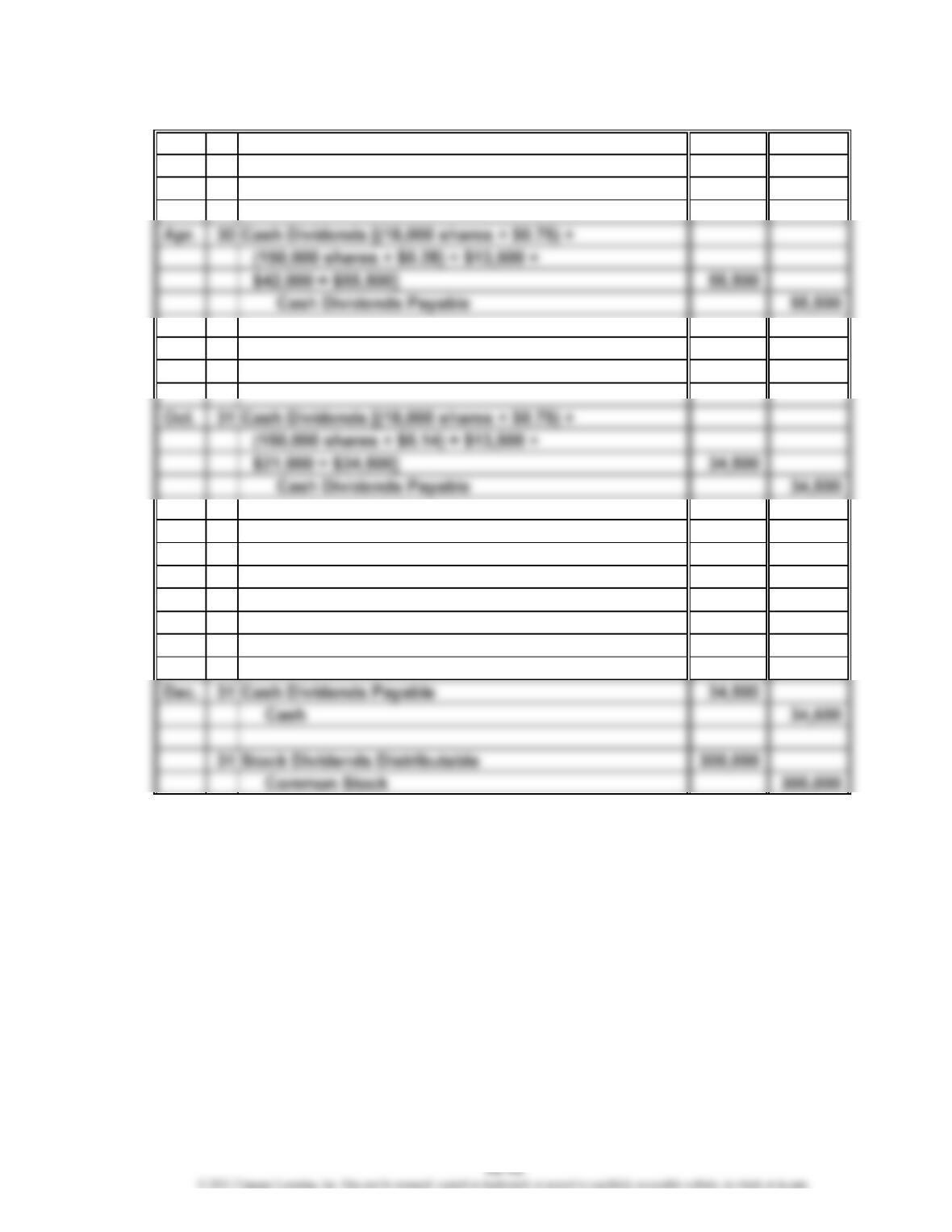

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-14

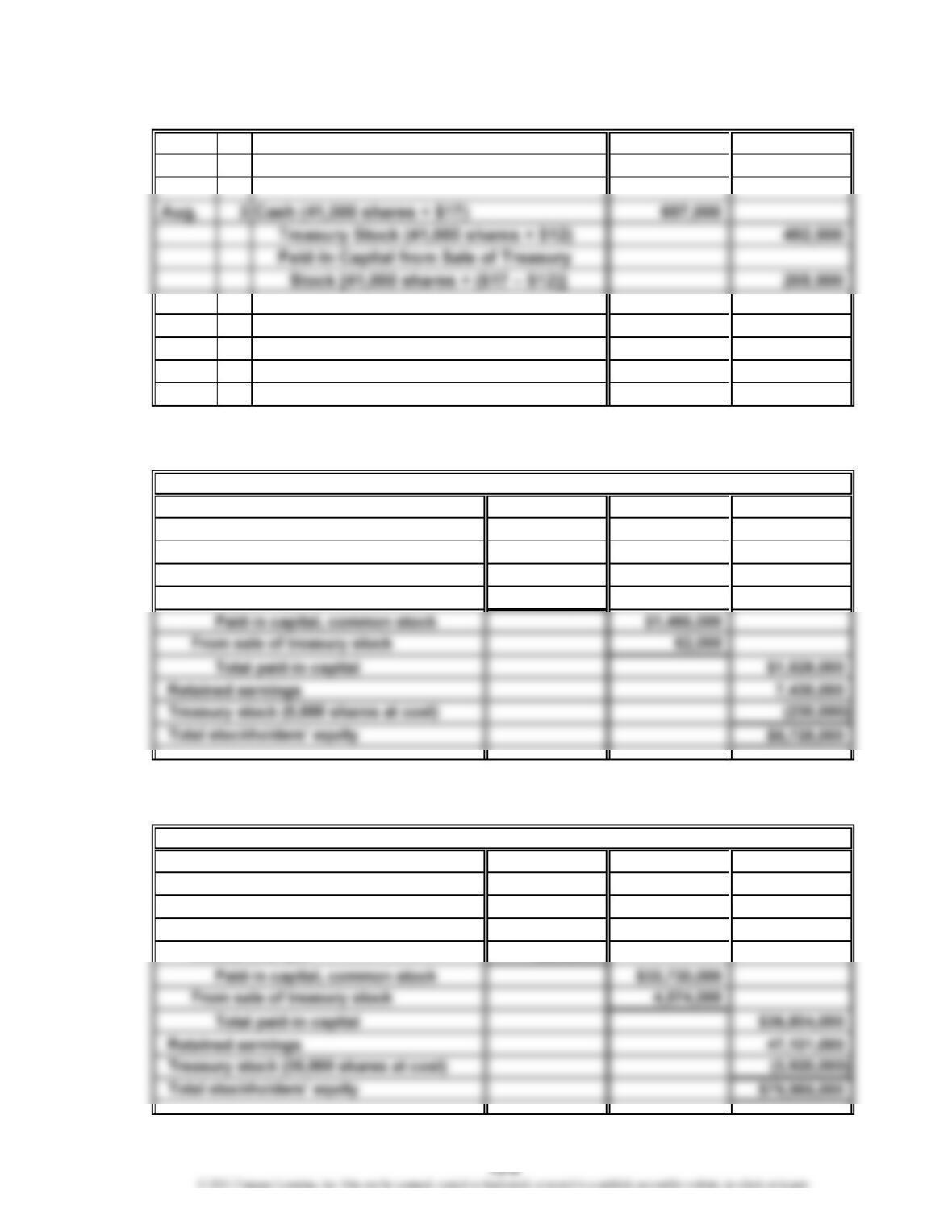

a. 11 Treasury Stock (180,000 shares × $17) 3,060,000

Cash 3,060,000

22 Cash (30,000 shares × $15) 450,000

Paid-In Capital from Sale of Treasury

Stock [30,000 shares × ($17 – $15)] 60,000

Treasury Stock (30,000 shares × $17) 510,000

b. $210,000 ($270,000 – $60,000) credit

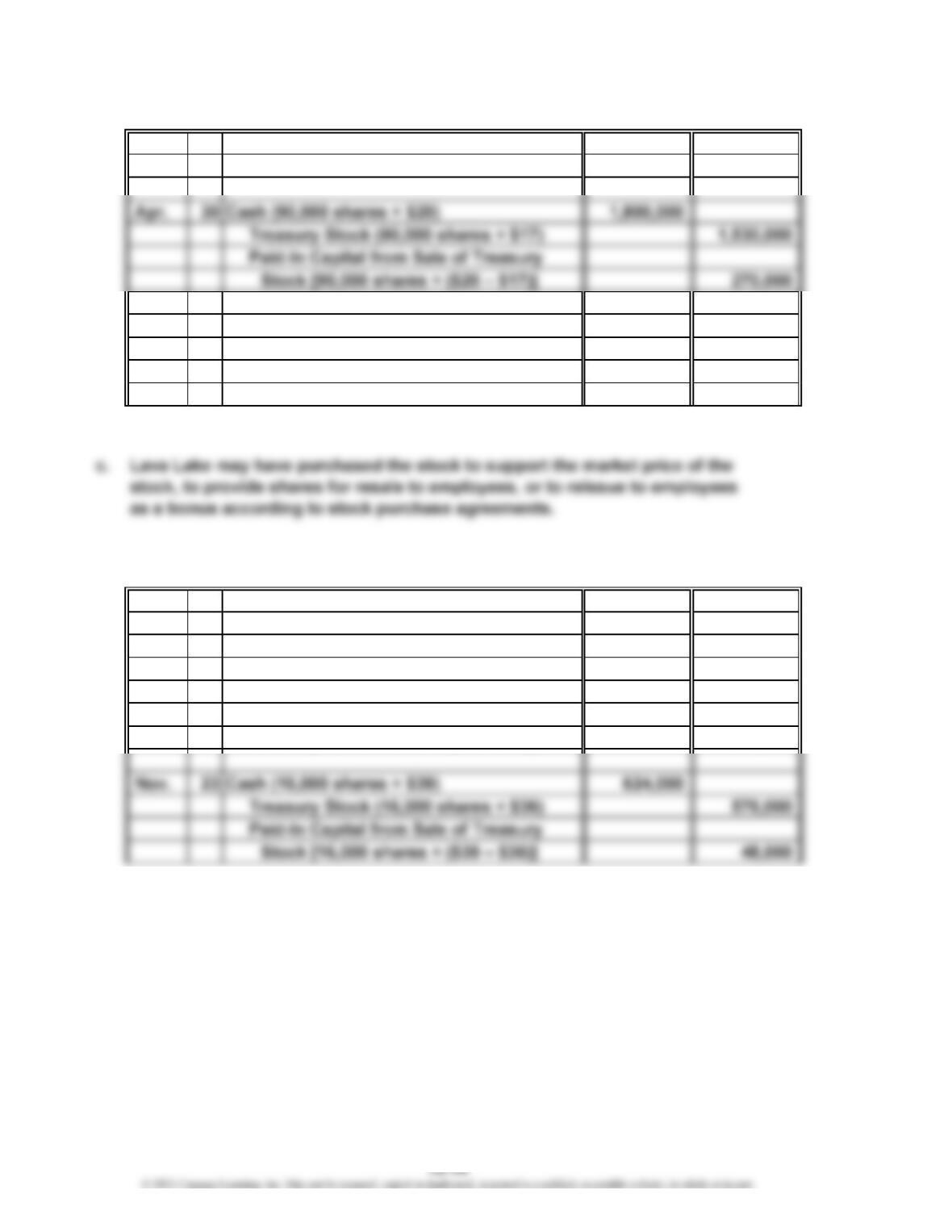

Ex. 13-15

a. 31 Treasury Stock (42,000 shares × $36) 1,512,000

Cash 1,512,000

14 Cash (19,000 shares × $43) 817,000

Treasury Stock (19,000 shares × $36) 684,000

Paid-In Capital from Sale of Treasury

Stock [19,000 shares × ($43 – $36)] 133,000

b. $181,000 ($133,000 + $48,000) credit

c. $252,000 [(42,000 shares − 19,000 shares − 16,000 shares) × $36]

d. The balance in the treasury stock account is reported as a deduction from the

total of the paid-in capital and retained earnings.

June

Jan.

Aug.

Feb.

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

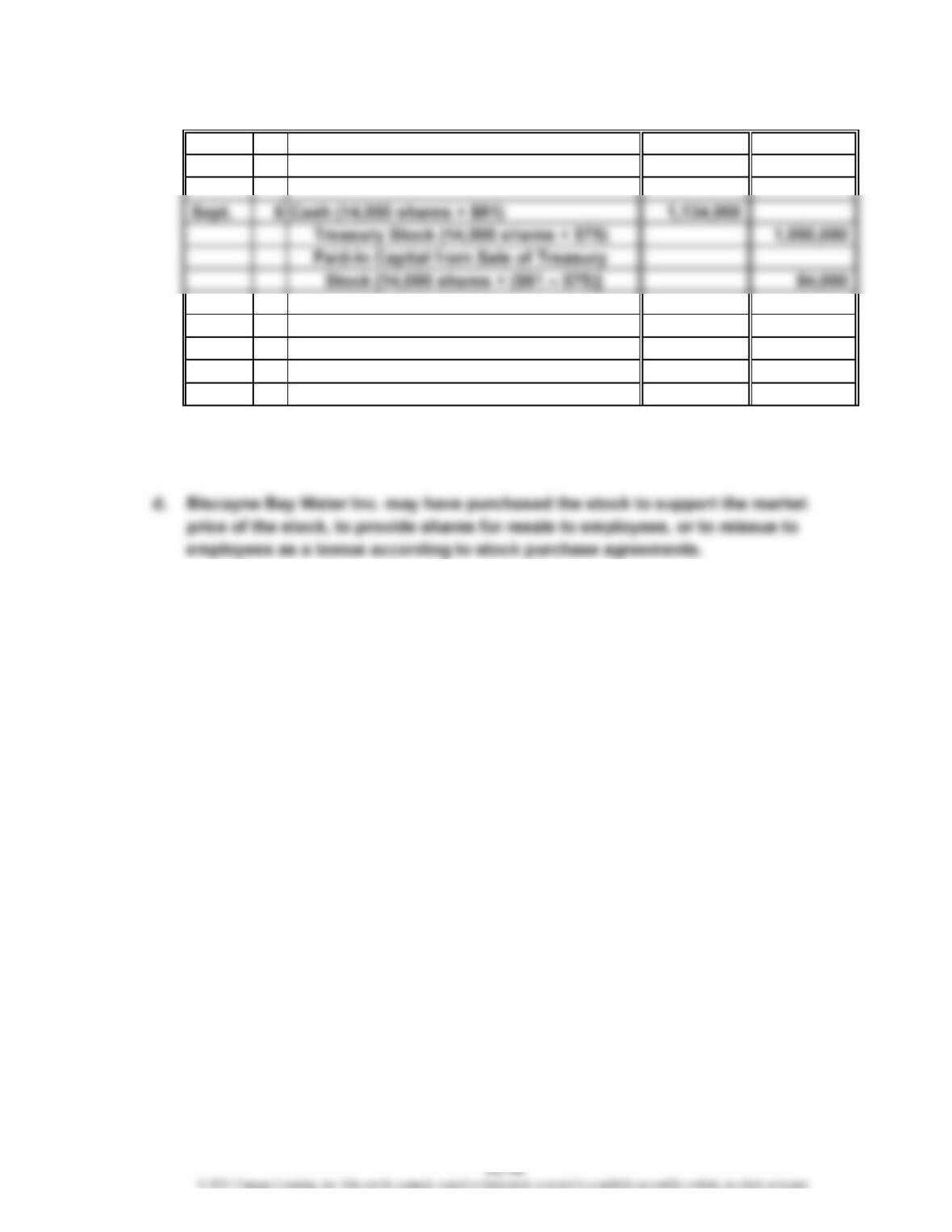

Ex. 13-16

a. 14 Treasury Stock (23,500 shares × $75) 1,762,500

Cash 1,762,500

30 Cash (9,500 shares × $72) 684,000

Paid-In Capital from Sale of Treasury

Stock [9,500 shares × ($75 – $72)] 28,500

Treasury Stock (9,500 shares × $75) 712,500

b. $55,500 ($84,000 – $28,500) credit

c. Stockholders’ Equity section

Nov.

May

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

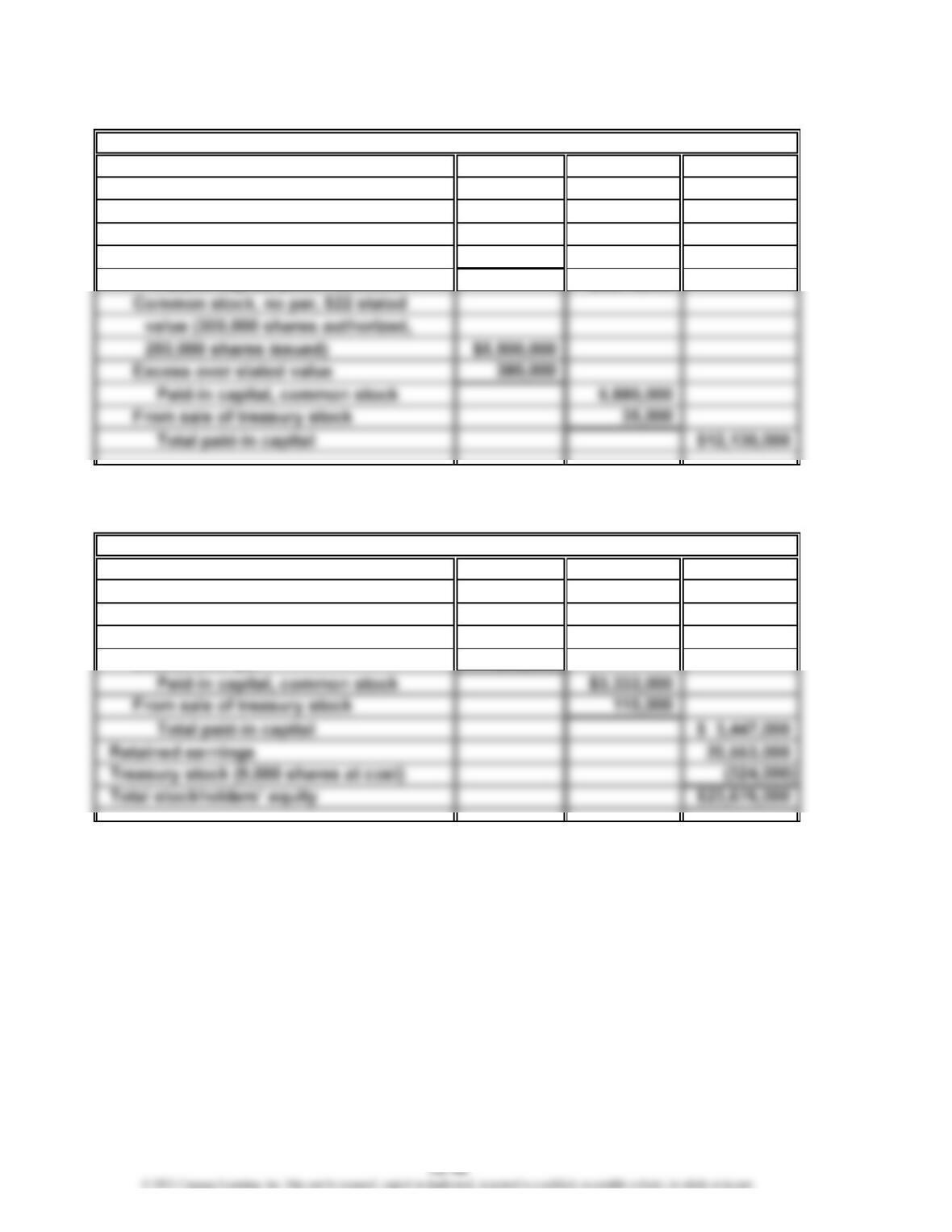

Ex. 13-17

Paid-in capital:

Preferred 2% stock, $110 par

(100,000 shares authorized,

55,000 shares issued) $6,050,000

Excess over par 165,000

Paid-in capital, preferred stock $6,215,000

Ex. 13-18

Paid-in capital:

Common stock, $45 par

(80,000 shares authorized,

68,000 shares issued) $3,060,000

Excess over par 272,000

Stockholders’ Equity

Stockholders’ Equity

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-19

Paid-in capital:

Preferred 1% stock, $150 par

(50,000 shares authorized,

48,000 shares issued) $ 7,200,000

Excess over par 384,000

Paid-in capital, preferred stock $ 7,584,000

Common stock, $36 par

Ex. 13-20

Retained earnings, February 1, 20Y1 $29,842,000

Net income $ 4,082,000

Stockholders’ Equity

Pressure Pumps Corporation

Retained Earnings Statement

For the Year Ended January 31, 20Y2

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-21

a. 1. Retained earnings is not part of paid-in capital.

2. The cost of treasury stock should be deducted from the total stockholders’

equity.

3. Dividends payable should be included as part of current liabilities and not

as part of stockholders’ equity.

b. A corrected Stockholders’ Equity section of the balance sheet using Method 1 of

Exhibit 8 is as follows:

Paid-in capital:

Preferred 2% stock, $60 par

(94,000 shares authorized

and issued) $5,640,000

Excess over par 375,000

Paid-in capital, preferred stock $6,015,000

Common stock, $10 par (750,000

shares authorized, 619,000

Stockholders’ Equity

CHAPTER 13 Corporations: Organization, Stock Transactions, and Dividends

Ex. 13-22

Paid-In

Common Capital

Stock, in Excess Retained

$40 par of Par Earnings

Balance, Jan. 1, 20Y9 $4,800,000 $ 960,000 $11,375,000

as treasury stock

Net income 3,780,000

Dividends (276,000)

Balance, Dec. 31, 20Y9 $6,000,000 $1,260,000 $14,879,000

Ex. 13-23

$17,135,000

I-Cards Inc.

Statement of Stockholders’ Equity

For the Year Ended December 31, 20Y9

Total

(276,000)

(552,000)

3,780,000

$21,587,000

Treasury

Stock

$(552,000)

$(552,000)

—