CHAPTER 13

SOLUTIONS TO PROBLEMS: SET B

PROBLEM 13-1B

(a) Jan. 10 Cash (100,000 X $3) ………………………….. 300,000

Common Stock (100,000 X $2) ……. 200,000

Paid-in Capital in Excess of

Stated Value—Common

Stock (100,000 X $1) ……………….. 100,000

Apr. 1 Land ………………………………………………… 75,000

Common Stock (25,000 X $2) ……… 50,000

Paid-in Capital in Excess of

Stated Value—Common

Stock ($75,000 – $50,000) ……….. 25,000

Aug. 1 Organization Expense ………………………. 50,000

Common Stock (10,000 X $2) ……… 20,000

Paid-in Capital in Excess of

Stated Value—Common

Stock ($50,000 – $20,000) ……….. 30,000

PROBLEM 13-1B (Continued)

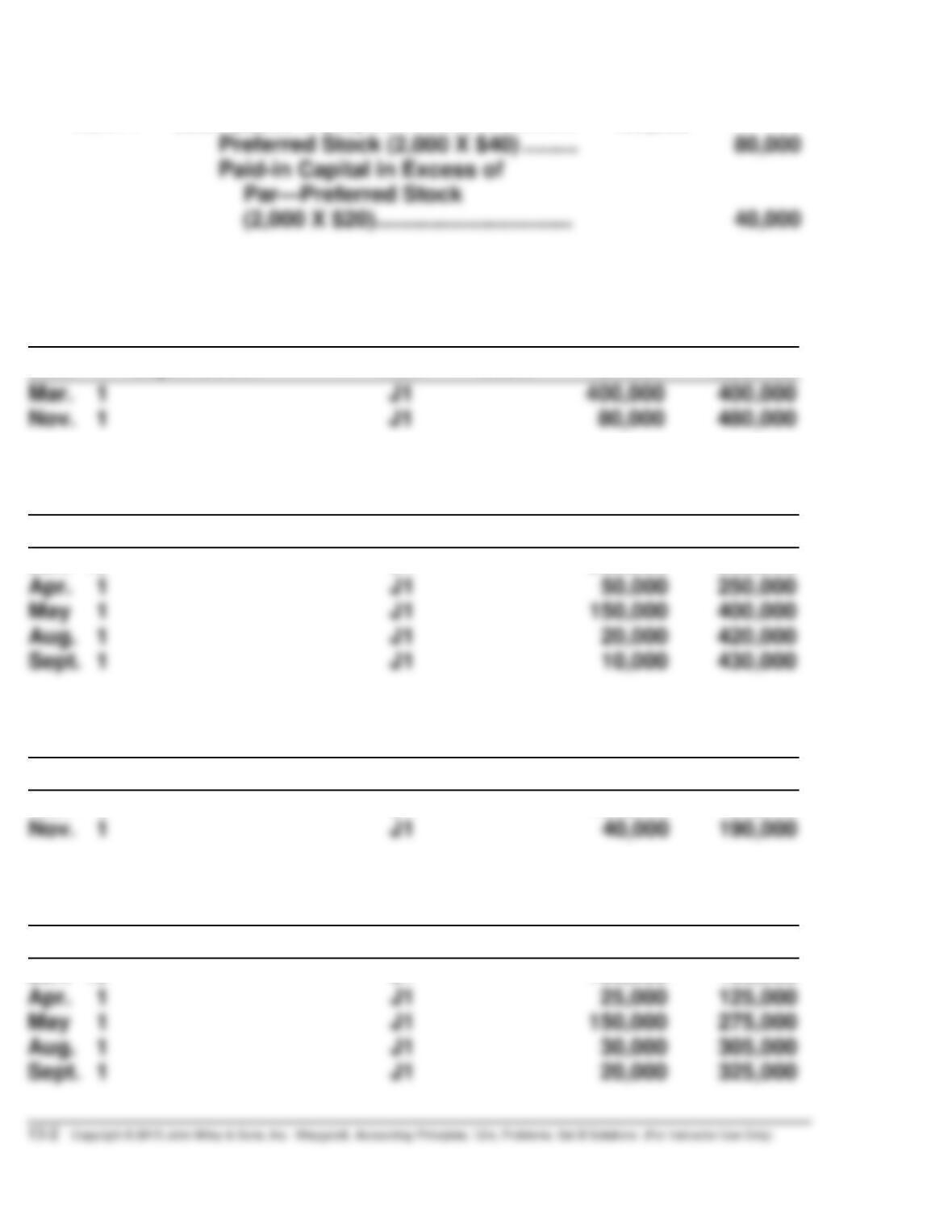

Nov. 1 Cash (2,000 X $60) ……………………………. 120,000

Preferred Stock (2,000 X $40) ……… 80,000

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Mar. 1

Nov. 1

J1

J1

400,000

80,000

400,000

480,000

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 1

J1

10,000

430,000

Jan. 10

J1

200,000

200,000

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Nov. 1

J1

Mar. 1

J1

150,000

150,000

Paid-in Capital in Excess of Stated Value—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 1

J1

325,000

Jan. 10

Apr. 1

J1

J1

100,000

25,000

100,000

125,000

PROBLEM 13-1B (Continued)

(c) MENDOZA CORPORATION

Paid-in capital

Capital stock

6% Preferred stock,

$40 par value,

Common stock, no par,

$2 stated value,

500,000 shares authorized,

Additional paid-in capital

In excess of par—

preferred stock ………………………… $190,000

In excess of stated value—

PROBLEM 13-2B

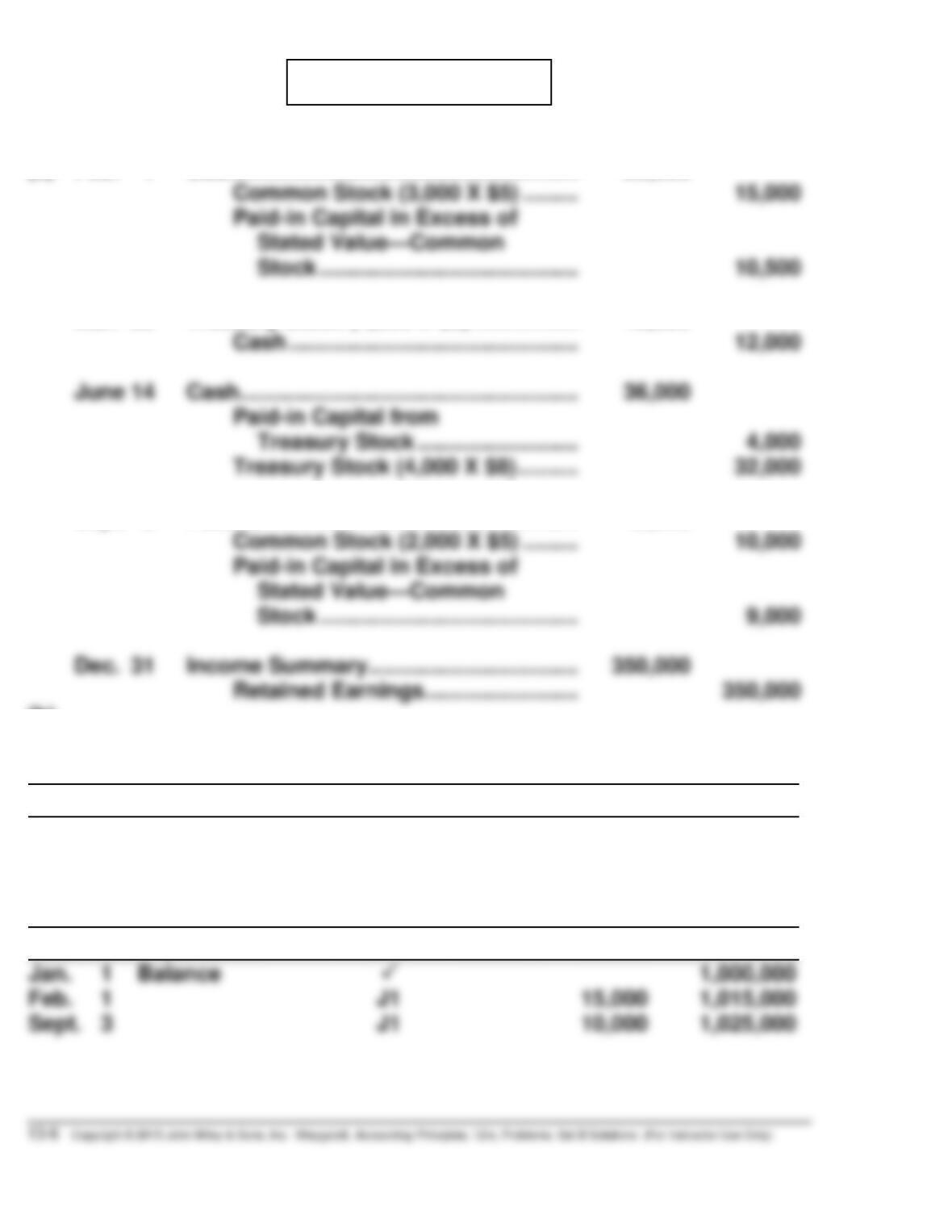

(a) Mar. 1 Treasury Stock (5,000 X $7) ………………… 35,000

Cash …………………………………………… 35,000

June 1 Cash (1,000 X $10) …………………………..…. 10,000

Sept. 1 Cash (2,000 X $9) ……………………………….. 18,000

Treasury Stock (2,000 X $7) ………….. 14,000

Paid-in Capital from Treasury

Stock (2,000 X $2) …………………….. 4,000

31 Income Summary ……………………………….. 80,000

Retained Earnings ……………………….. 80,000

(b)

Paid-in Capital from Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

June 1

J12

3,000

3,000

Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Mar. 1

June 1

J12

J12

35,000

7,000

35,000

28,000

PROBLEM 13-2B (Continued)

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

100,000

(c) HAWTHORNE CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $1 par,

400,000 shares issued and

399,000 outstanding …………… $ 400,000

Additional paid-in capital

In excess of par—

common stock …………………… $500,000

PROBLEM 13-3B

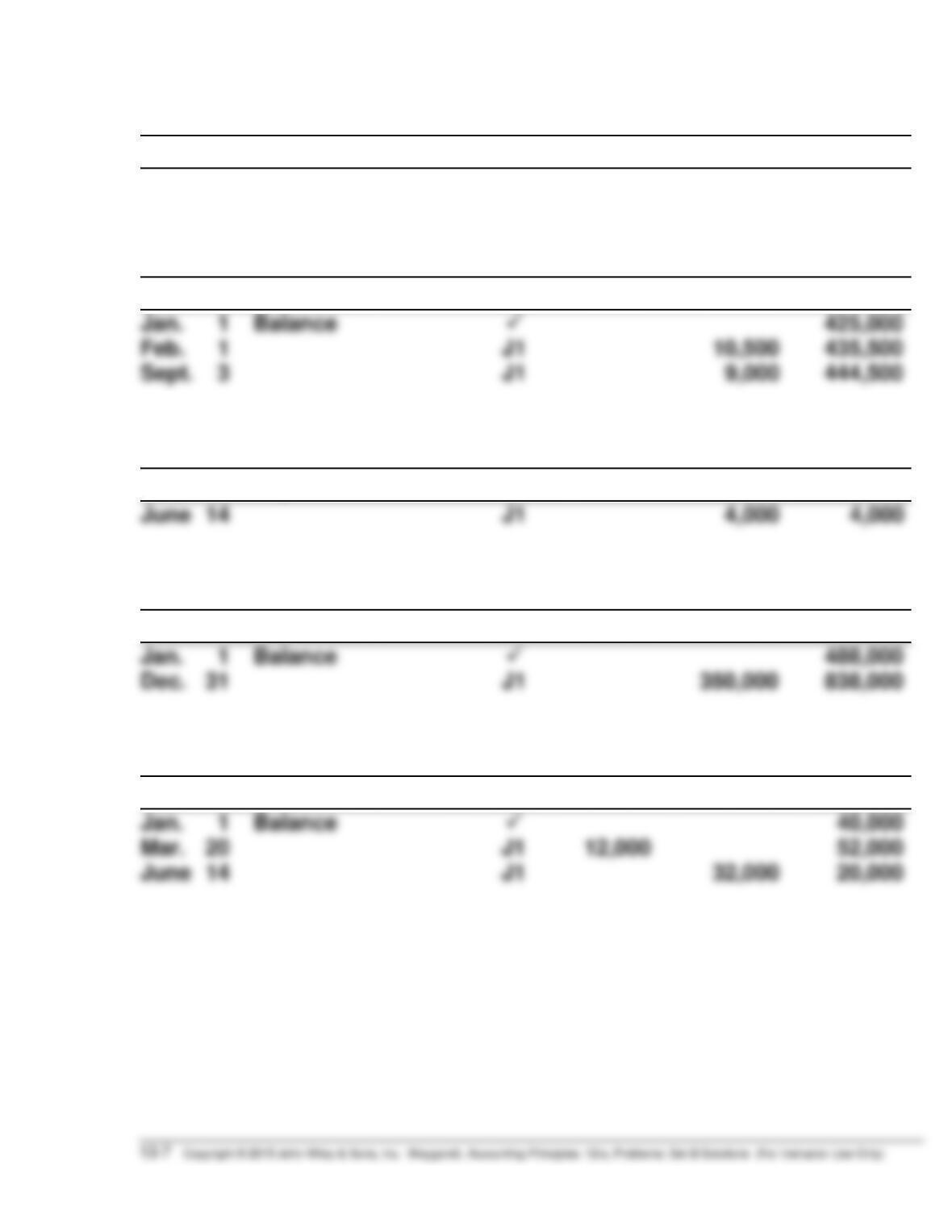

(a) Feb. 1 Cash ………………………………………………. 25,500

Common Stock (3,000 X $5) ……… 15,000

Paid-in Capital in Excess of

Mar. 20 Treasury Stock (1,500 X $8) …………….. 12,000

Cash ……………………………………….. 12,000

June 14 Cash ………………………………………………. 36,000

Sept. 3 Patents ………………………………………….. 19,000

Common Stock (2,000 X $5) ……… 10,000

Paid-in Capital in Excess of

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

300,000

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 13-3B (Continued)

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

20,000

Paid-in Capital in Excess of Stated Value—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Sept. 3

444,500

Paid-in Capital from Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

June 14

J1

4,000

4,000

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Dec. 31

838,000

Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

June 14

20,000

PROBLEM 13-3B (Continued)

(c) LORE CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

10% Preferred stock, $100

par value, noncumulative,

5,000 shares authorized,

3,000 shares issued and

outstanding …………………………. $ 300,000

Additional paid-in capital

In excess of par—

preferred stock ……………………. $ 20,000

In excess of stated value—

common stock …………………….. 444,500

From treasury stock ………………… 4,000

Less: Treasury stock (2,500 common

shares) ……………………………………… 20,000

Total stockholders’

PROBLEM 13-4B

(a) Feb. 1 Land ………………………………………………… 65,000

Preferred Stock (1,000 X $40) ……… 40,000

Paid-in Capital in Excess of

Mar. 1 Cash (2,000 X $60) ……………………………. 120,000

Preferred Stock (2,000 X $40) ……… 80,000

Paid-in Capital in Excess of

July 1 Cash (20,000 X $5.80) ……………………….. 116,000

Common Stock (20,000 X $5) ……… 100,000

Paid-in Capital in Excess of

Sept. 1 Patent (800 X $65) …………………………….. 52,000

Preferred Stock (800 X $40) ………… 32,000

Paid-in Capital in Excess of

Par—Preferred Stock

(800 X $25) …………………………….. 20,000

PROBLEM 13-4B (Continued)

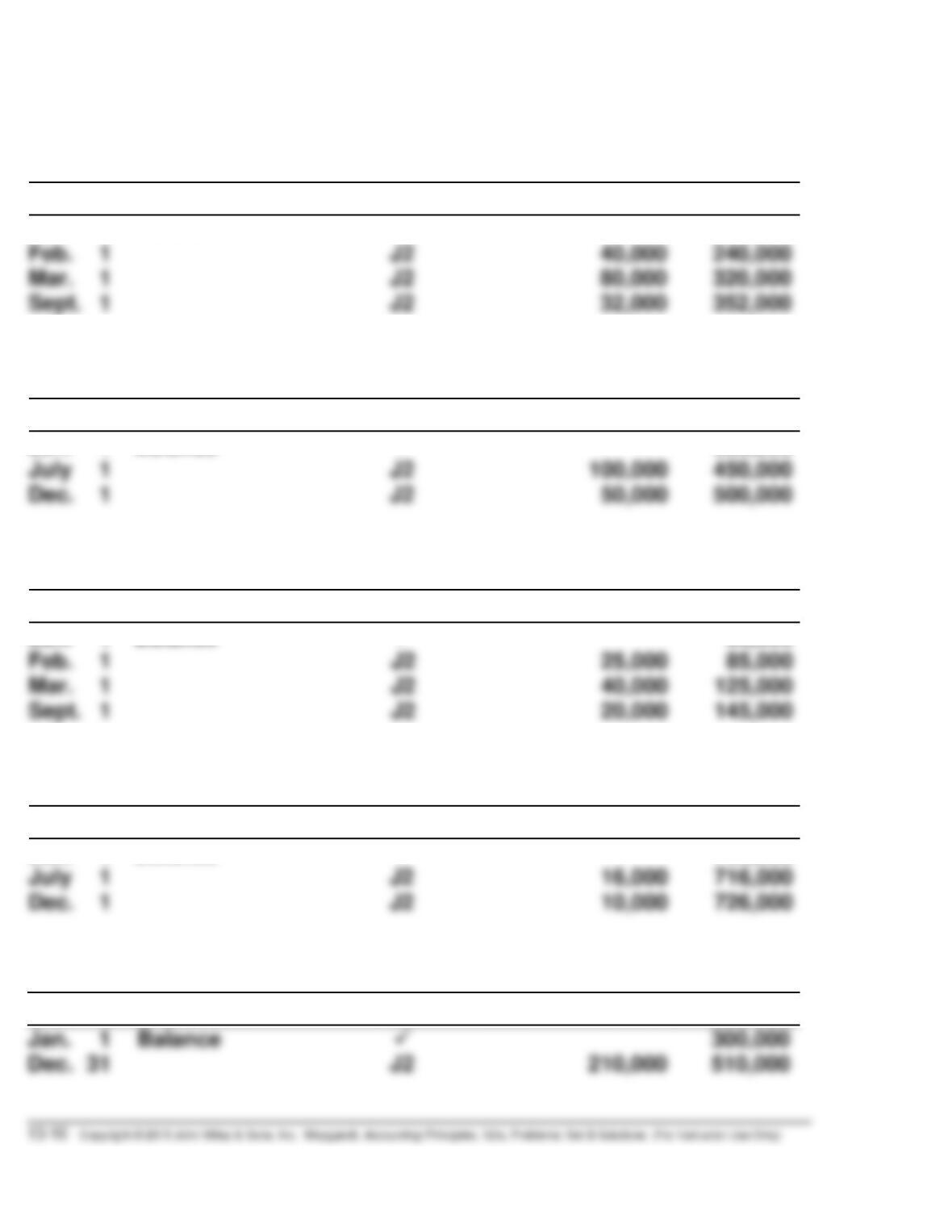

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Feb. 1

Mar. 1

J2

240,000

Jan. 1

Balance

200,000

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

July 1

Balance

J2

100,000

350,000

450,000

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Mar. 1

40,000

125,000

Jan. 1

Feb. 1

Balance

J2

25,000

60,000

85,000

Paid-in Capital in Excess of Par—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

July 1

J2

16,000

716,000

Jan. 1

Balance

700,000

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Dec. 31

Balance

J2

210,000

300,000

510,000

PROBLEM 13-4B (Continued)

(c) GERSTNER CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

10%, Preferred stock,

$40 par value,

10,000 shares authorized,

8,800 shares issued

Additional paid-in capital

In excess of par—preferred …….. $145,000

In excess of par—

common stock ……………………. 726,000

PROBLEM 13-5B

ALPERS CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100

par value, noncumulative,

Additional paid-in capital

In excess of par—

preferred stock …………………… $288,400

In excess of stated value—

Retained earnings ………………………………. 826,000

Total paid-in capital and

retained earnings ………….. 3,310,400

PROBLEM 13-6B

(a) (1) Land ………………………………………………….. 296,000

Preferred Stock (2,400 X $100) ……… 240,000

(2) Cash (400,000 X $16) …………………………... 6,400,000

Common Stock (400,000 X $5) ………. 2,000,000

(3) Treasury Stock (1,500 X $22) ……………….. 33,000

Cash …………………………………………… 33,000

(4) Cash (500 X $28) …………………………………. 14,000

PROBLEM 13-6B (Continued)

(b) KINGSLEY CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100

par value, noncumulative,

40,000 shares authorized,

2,400 shares issued and

Additional paid-in capital

In excess of par—

preferred stock …………………. $ 56,000

In excess of stated value—

Retained earnings …………………………….. 560,000

Total paid-in capital and