PROBLEM 13-2C

(a) Mar. 1 Treasury Stock (5,000 X $6) ………………… 30,000

Cash …………………………………………… 30,000

June 1 Cash (1,000 X $10) ……………………………… 10,000

Sept. 1 Cash (2,000 X $9) …………………………..…… 18,000

Treasury Stock (2,000 X $6) ………….. 12,000

Paid-in Capital from Treasury

Stock (2,000 X $3) …………………….. 6,000

(b)

Paid-in Capital from Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

June 1

J12

4,000

4,000

Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Mar. 1

J12

30,000

30,000

PROBLEM 13-2C (Continued)

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

100,000

(c) CHENG CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $1 par,

400,000 shares issued and

399,000 outstanding …………… $ 400,000

Additional paid-in capital

Retained earnings ………………………………. 150,000

Total paid-in capital and

retained earnings………… 1,059,000

PROBLEM 13-3C

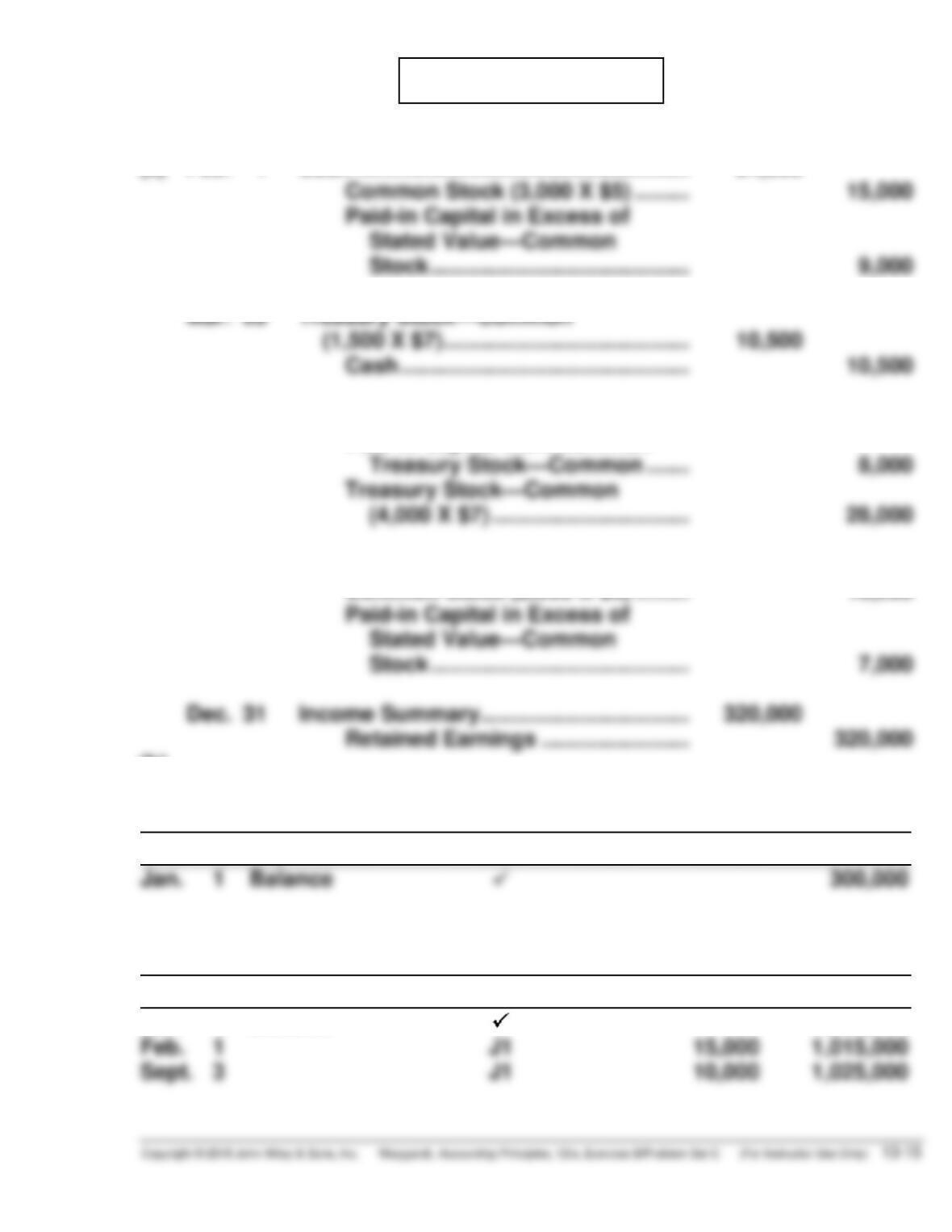

(a) Feb. 1 Cash ……………………………………………… 24,000

Common Stock (3,000 X $5) ……… 15,000

Paid-in Capital in Excess of

Mar. 20 Treasury Stock—Common

(1,500 X $7) …………………………………. 10,500

Cash ……………………………………….. 10,500

June 14 Cash ……………………………………………… 36,000

Paid-in Capital from Common

Sept. 3 Patent ……………………………………………. 17,000

Common Stock (2,000 X $5) ……… 10,000

Paid-in Capital in Excess of

Retained Earnings …………………… 320,000

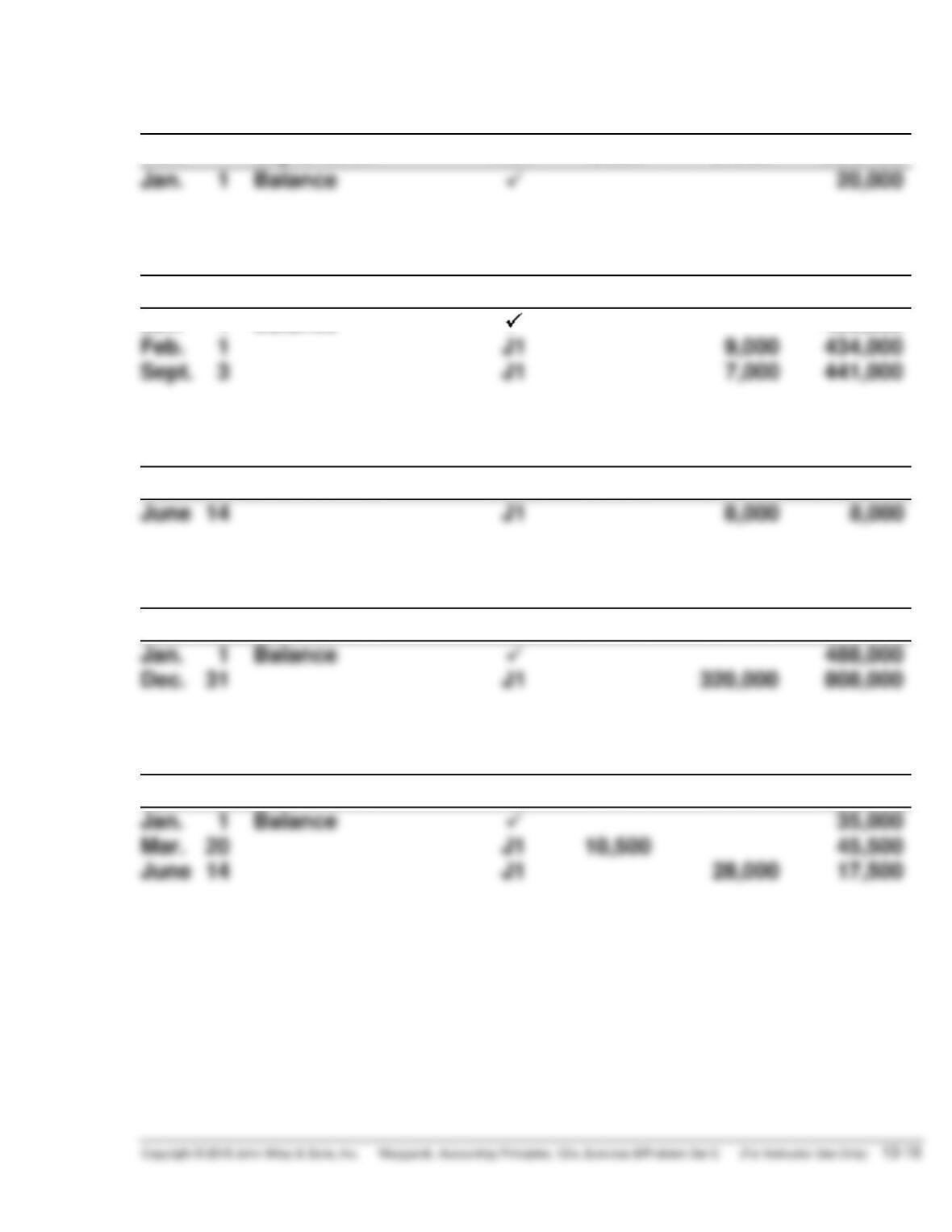

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

300,000

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

1,000,000

PROBLEM 13-3C (Continued)

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

20,000

Paid-in Capital in Excess of Stated Value—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Paid-in Capital from Treasury Stock—Common

Date

Explanation

Ref.

Debit

Credit

Balance

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Treasury Stock—Common

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 13-3C (Continued)

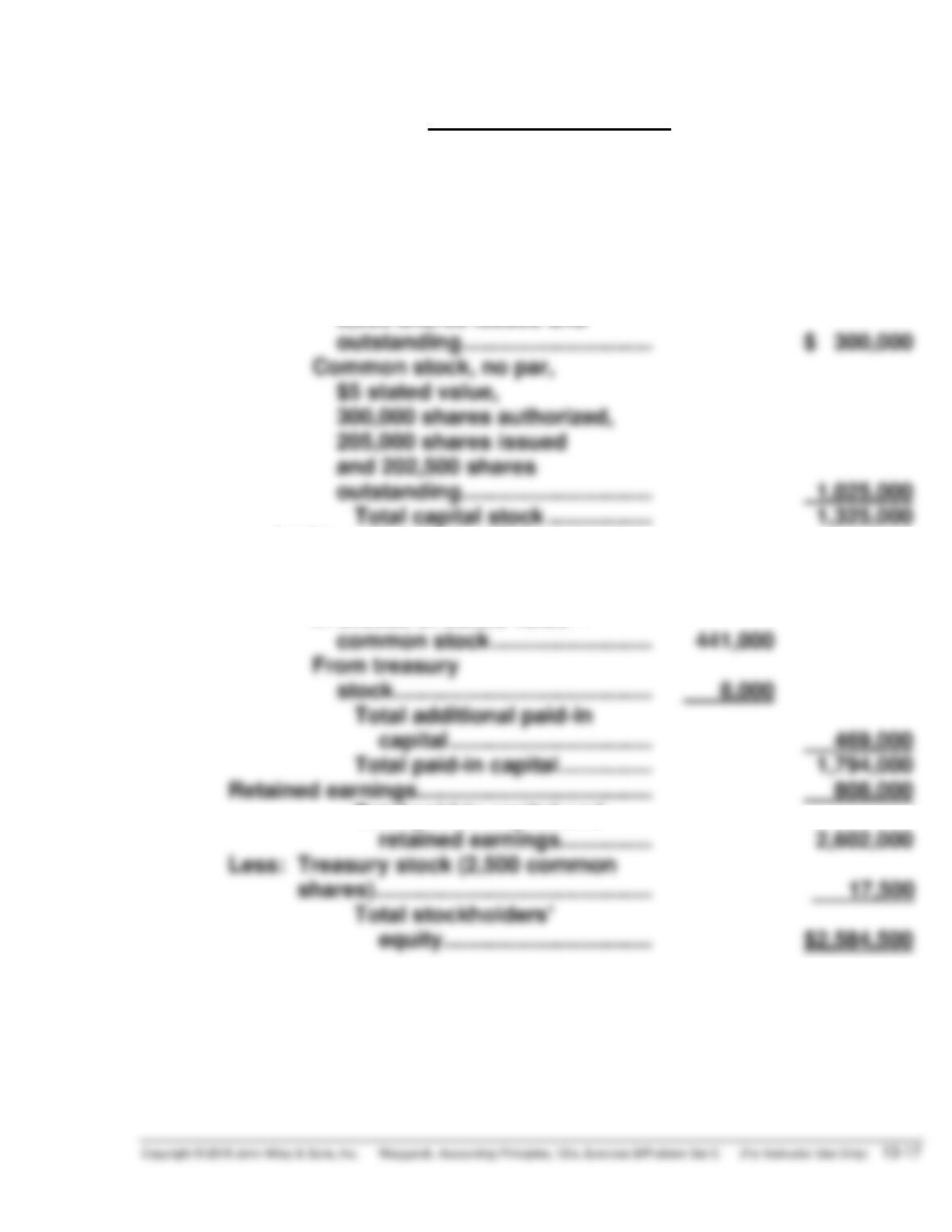

(c) REYES CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

10% Preferred stock, $100

par value, noncumulative,

5,000 shares authorized,

3,000 shares issued and

outstanding …………………………. $ 300,000

Total capital stock …………….. 1,325,000

Additional paid-in capital

In excess of par—

preferred stock ……………………. $ 20,000

In excess of stated value—

Retained earnings ……………………………….. 808,000

Total paid-in capital and

retained earnings …………… 2,602,000

Less: Treasury stock (2,500 common

shares) ……………………………………… 17,500

PROBLEM 13-4C

(a) Feb. 1 Land ………………………………………………… 65,000

Preferred Stock (1,000 X $30) ……… 30,000

Paid-in Capital in Excess of

Par—Preferred Stock

($65,000 – $30,000) …………………. 35,000

Mar. 1 Cash (2,000 X $60) ……………………………. 120,000

(2,000 X $30) ………………………….. 60,000

July 1 Cash (20,000 X $5.80) ……………………….. 116,000

Common Stock (20,000 X $2) ……… 40,000

Paid-in Capital in Excess of

Par—Common Stock

($116,000 – $40,000) ……………….. 76,000

Dec. 1 Cash (10,000 X $6) ……………………………. 60,000

Common Stock (10,000 X $2) ……… 20,000

Paid-in Capital in Excess of

PROBLEM 13-4C (Continued)

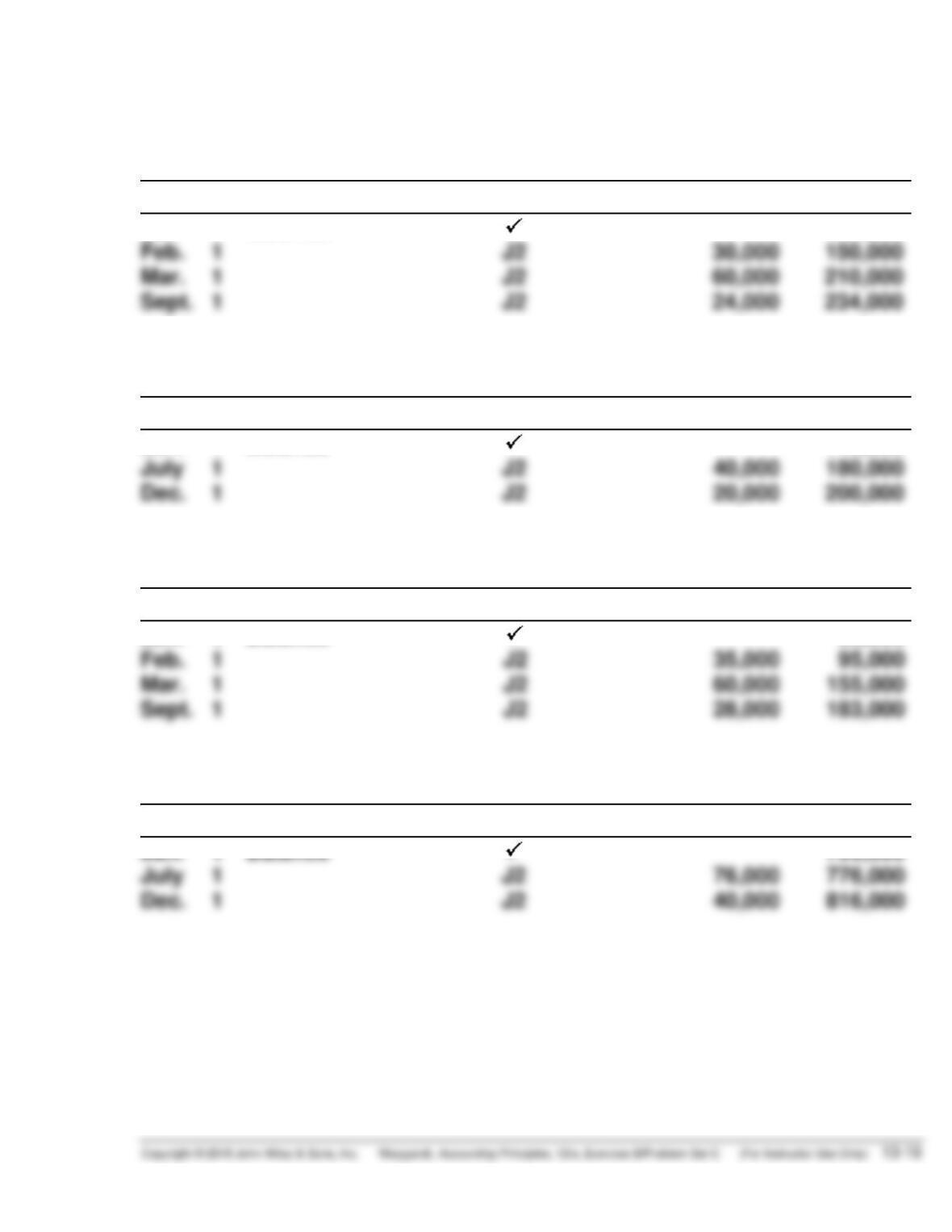

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

120,000

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

140,000

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Feb. 1

Balance

J2

35,000

60,000

95,000

Paid-in Capital in Excess of Par—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

700,000

PROBLEM 13-4C (Continued)

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

(c) KWUN CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

Preferred stock,

$30 par value, 10%,

10,000 shares authorized,

Total capital stock …………… 434,000

Additional paid-in capital

In excess of par—

preferred ……………………………. $183,000

In excess of par—common …….. 816,000

PROBLEM 13-5C

HITE CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100

par value, noncumulative,

4,000 shares issued

Additional paid-in capital

In excess of par—

preferred stock ……………………. $288,400

In excess of stated value—

Retained earnings ……………………………….. 876,000

Total paid-in capital and

retained earnings …………… 3,460,400

PROBLEM 13-6C

(a) (1) Land ………………………………………………….. 296,000

Preferred Stock (2,400 X $100) ……… 240,000

Paid-in Capital in Excess of Par—

Preferred Stock ………………………… 56,000

(3) Treasury Stock—Common

(1,500 X $24) …………………………………… 36,000

Cash …………………………………………… 36,000

PROBLEM 13-6C (Continued)

(b) MORITZ CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $100

par value, noncumulative,

Common stock, no par, $5

stated value, 2,000,000

shares authorized, 400,000

Additional paid-in capital

In excess of par—

preferred stock …………………. $ 56,000

In excess of stated value—

Retained earnings …………………………….. 560,000

Total paid-in capital and

retained earnings ………… 8,058,000