CHAPTER 13

Financial Analysis: The Big Picture

Learning Objectives

1. Explain the concepts of sustainable income and quality of earnings.

2. Apply horizontal analysis and vertical analysis.

3. Analyze a company’s performance using ratio analysis.

Summary of Questions by Learning Objectives and Bloom’s Taxonomy

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Item

LO

BT

Questions

1.

1

C

6.

2

C

11.

3

C

16.

3

C

20.

3

C

2.

1

C

7.

2

C

12.

3

K

17.

3

C

21.

3

C

3.

1

C

8.

2

AP

13.

3

C

18.

3

C

22.

3

AP

4.

1

AP

9.

3

C

14.

3

C

19.

3

C

5.

1

C

10.

2

K

15.

3

C

Brief Exercises

1.

1

AP

4.

2

AP

7.

2

AP

10.

3

AP

13.

3

AN

2.

1

AP

5.

2

AP

8.

2

AP

11.

3

AN

14.

3

AN

3.

1

C

6.

2

AP

9.

2

AP

12.

3

AN

15.

3

AN

Do It! Exercises

1.

1

AP

2.

2

AP

3.

3

C

Exercises

1.

1

AP

3.

2

AP

6.

2

AP

9.

3

AP

12.

3

AP

2.

1

AP

4.

2

AP

7.

3

AP

10.

3

AP

13.

3

AP

5.

2

AP

8.

3

AP

11.

3

AP

Problems: Set A

1.

2, 3

AN

2.

3

AP

3.

3

AN

4.

3

AN

5.

3

AN

*Continuing Cookie Solutions for this chapter are available online.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare vertical analysis and comment on profitability.

Moderate

20–30

2A

Compute ratios from balance sheet and income

statements.

Moderate

20–30

3A

Perform ratio analysis, and discuss change in

financial position and operating results.

Moderate

20–30

4A

Compute ratios; comment on overall liquidity and

profitability.

Moderate

40–50

5A

Compute selected ratios, and compare liquidity,

profitability, and solvency for two companies.

Moderate

50–60

ANSWERS TO QUESTIONS

1. Sustainable income is defined as the most likely level of income to be obtained in the future. It is

the amount of regular income that a company can expect to earn from its normal operations.

LO 1 BT: C Difficulty: Medium TOT: 3 min. AACSB: None AICPA FC: Reporting

2. This would not be considered a favorable trend for Hogan Inc. The relevant earnings per share

figures are the $3.26 in 2016 and the $2.99 in 2017. These figures indicate that, unless there was

a sale of common stock, the earnings from the continuing operations of the company decreased

LO 1 BT: AN Difficulty: Medium TOT: 4 min. AACSB: Analytic AICPA FC: Reporting

3. Companies report a change from FIFO to average cost pricing for inventory retroactively. That is,

they report both the current period and any previous periods reported on the face of the state–

4. Apple reported “Other comprehensive income” of $1,553 millions for year ended September 27,

2014. “Comprehensive income” was more than “Net income” by 3.9% [($41,063 – $39,510) ÷

5. (1) Use of alternative accounting methods. Variations among companies in the application of

generally accepted accounting principles may hamper comparability.

(2) Use of pro forma income measures that do not follow GAAP. Pro forma income is calculated by

(3) Improper revenue and expense recognition. Many high–profile cases of inappropriate accounting

6. (a) During a period of inflation, net income will be less under the LIFO inventory costing method

than it will be using the FIFO method because LIFO results in the larger cost of goods sold

amount.

7. Horizontal analysis (also called trend analysis) measures the dollar and percentage increase or

decrease of an item over a period of time. In this approach, the amount of the item on one state–

8. (a) $300,000 X 1.245 = $373,500, 2017 net income.

9. (a) Gina is not correct. There are three characteristics: liquidity, profitability, and solvency.

(b) The three parties are not primarily interested in the same characteristics of a company. Short-

10. (a) Comparison of financial information can be made on an intracompany basis, an inter-

company basis, and an industry average basis.

1. An intracompany basis compares the same item with prior periods, or with other

financial items in the same period.

2. An intercompany basis compares the same item with other companies’ published reports.

3. The industry average compares the item with the industry average as compiled by

Dun & Bradstreet or by trade associations.

11. (a) Liquidity ratios: Working capital, current ratio, inventory turnover, days in inventory, accounts

12. Tina is correct. A single ratio by itself may not be very meaningful and is best interpreted by

comparison with (1) past ratios of the same company, (2) ratios of other companies, or (3) industry

13. (a) Liquidity ratios measure the short-term ability of the company to pay its maturing obligations

and to meet unexpected needs for cash.

14. Working capital and the current ratio both relate current assets to current liabilities. Working

capital produces a dollar amount that indicates the difference between current assets and current

15. Handi Mart does not necessarily have a problem. The accounts receivable turnover can be

misleading in that some companies encourage credit and revolving charge sales and slow

16. (a) Asset turnover.

(b) Inventory turnover and days in inventory.

17. The price earnings (P-E) ratio is a reflection of investors’ assessments of a company’s future

earnings. The P-E ratio takes into account such factors as relative risk, stability of earnings,

18. The payout ratio is cash dividends declared on common stock divided by net income. In a growth

19. (a) The increase in the profit margin is good news because it means that a greater percentage

of net sales is going towards income.

(b) The decrease in inventory turnover signals bad news because it is taking the company longer

to sell the inventory and consequently there is a greater chance of inventory obsolescence.

20.

Return on assets

(7.6%)

=

Net Income

Average Total Ass ets

21. (a) Times interest earned, which is an indication of the company’s ability to meet interest charges,

and the debt to assets ratio, which indicates the company’s ability to withstand losses without

impairing the interests of creditors.

22.

–Net income Preferred dividends

Average common shares outstanding

= Earnings per share.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 13-1

FLORES CORPORATION

Partial Income Statement

Discontinued operations: Loss on disposal of

BRIEF EXERCISE 13-2

SILVA CORPORATION

Partial Statement of Comprehensive Income

Income before income taxes ……………………………………………….. $450,000

Income tax expense ($450,000 X 25%) …………………………………. 112,500

BRIEF EXERCISE 13-3

The change in inventory pricing for Bryce should be reported retroactively.

That is, it should report both the current period and previous periods

BRIEF EXERCISE 13-4

Horizontal analysis:

Increase

or (Decrease)

Dec. 31, 2017

Dec. 31, 2016

Amount

Percentage*

Accounts receivable

$ 460,000

$ 400,000

$ 60,000

15%

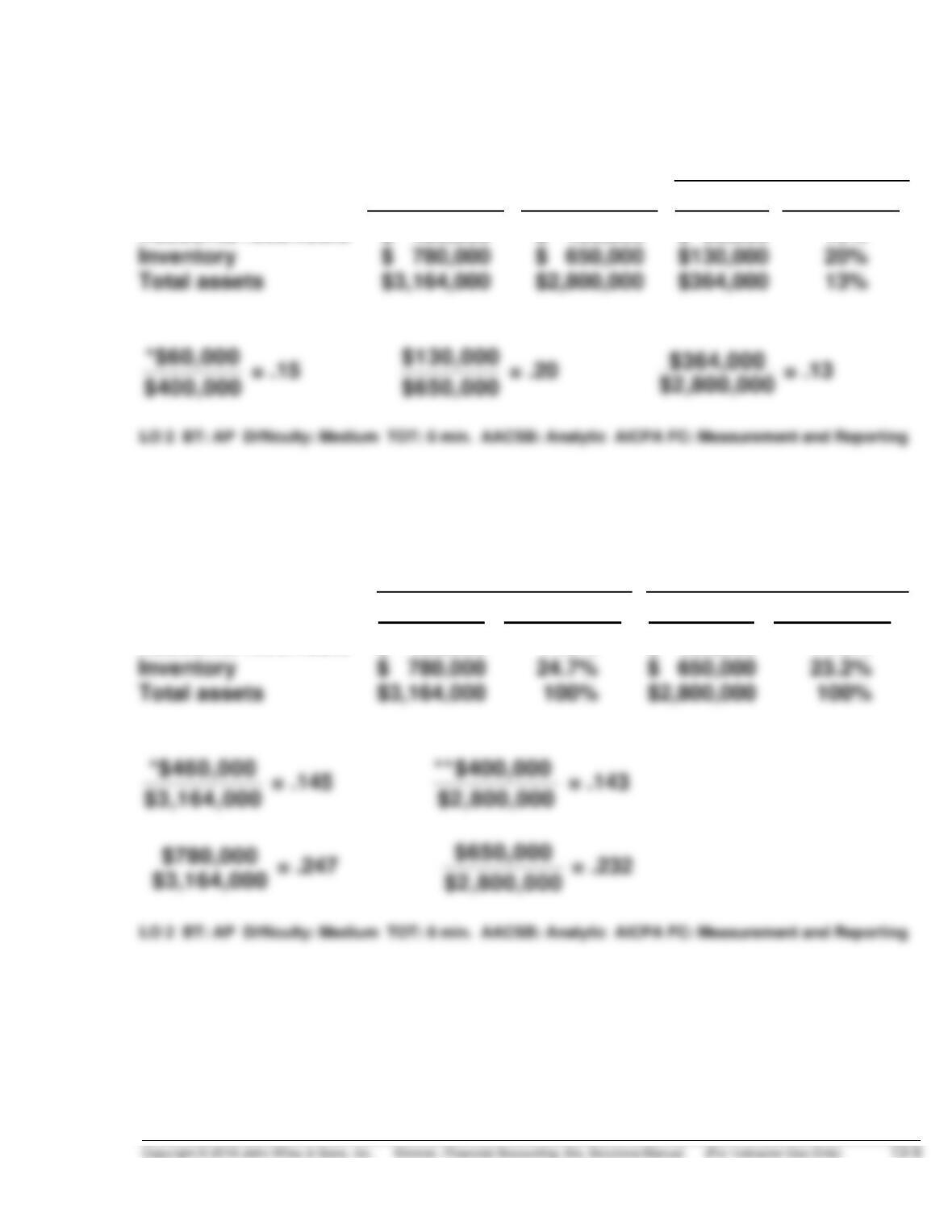

BRIEF EXERCISE 13-5

Vertical analysis:

Dec. 31, 2017

Dec. 31, 2016

Amount

Percentage*

Amount

Percentage**

Accounts receivable

$ 460,000

14.5%

$ 400,000

14.3%

BRIEF EXERCISE 13-6

2017

2016

2015

Net income

$518,400

$485,000

$500,000

Increase or (Decrease)

Amount

Percentage*

BRIEF EXERCISE 13-7

2017

2016

Increase

Net income

$382,800

X

16%

.16 =

$382,800 – X

BRIEF EXERCISE 13-8

2017

2016

2015

Sales revenue

Cost of goods sold

100.0

60.5

100.0

62.9

100.0

64.8

BRIEF EXERCISE 13-9

Comparing the percentages presented results in the following conclusions:

The net income for Phoenix increased in 2016 because of the combination

of an increase in sales and a decrease in both cost of goods sold and

BRIEF EXERCISE 13-10

Current ratio:

2017 2016

BRIEF EXERCISE 13-11

Accounts receivable turnover =

Net credit sales

Average net accounts receivable

2017

2016

(b)

Average collection period

365

365

BRIEF EXERCISE 13-12

(a) Inventory turnover =

Cost of goods sold

Average inventory

(b) Days in inventory

365

4.8

= 76 days

365

5.0

= 73 days

BRIEF EXERCISE 13-13

(a) Asset turnover =

Net sales

Average total assets

(b) Profit margin =

Net income

Net sales

BRIEF EXERCISE 13-14

Payout ratio =

Cash dividends declared on common stock

Net income

.18 =

X

$72,000

BRIEF EXERCISE 13-15

Free Cash Flow

= Cash provided by operating activities –

Capital expenditures – Cash dividends

SOLUTIONS TO DO IT! EXERCISES

DO IT! 13-1

HRABIK CORPORATION

Partial Statement of Comprehensive Income

Income before income taxes ………………………………….. $500,000

Income tax expense ………………………………………………. 100,000

Income from continuing operations ……………………….. 400,000

DO IT! 13-2

Increase in 2017

Amount Percent

Current assets $ (20,000) (9.1)% [($ 200,000 – $ 220,000) ÷ $ 220,000]

DO IT! 13-3

2017 2016

(a) Current ratio:

(b) Inventory turnover:

$955/ [($460 + $390) ÷ 2)] = 2.25 times

(c) Profit margin ratio:

$294 ÷ $3,800 = 7.7%

(d) Return on assets:

$294/[($2,340 + $2,210) ÷ 2)] = 12.9%

(e) Return on common stockholders’ equity:

$294/[($1,030 + $1,040) ÷ 2)] = 28.4%

(f) Debt to assets ratio:

$1,310 ÷ $2,340 = 56.0%

SOLUTIONS TO EXERCISES

EXERCISE 13-1

(a) HAAS CORPORATION

Partial Statement of Comprehensive Income

For the Year Ended October 31, 2017

Income before income taxes ………………………………………….. $540,000

Income tax expense ($540,000 X 20%) …………………………….. 108,000

(b) To: Chief Accountant

From: Your name, Independent Auditor

After reviewing your income statement for the year ended 10/31/17, we

believe it is misleading for the following reasons:

EXERCISE 13-2

TRAYER CORPORATION

Partial Statement of Comprehensive Income

For the Year Ended December 31, 2017

Income from continuing operations …………………. $290,000

Discontinued operations

Loss from operations, net of $2,000

income tax savings ……………………………….. $ 8,000