Name:

Section:

Score: See student sheet for student’s score

Scoring:

March April May

For the Three Months Ending May 31

ON

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

REHAB PHYSICAL THERAPY INC.

Schedule of Cash Payments for Operations

A red asterisk (*) will appear in the column immediately to the right of an incorrect answer.

Exercise 13-16

SOLUTION

Instructions

Name:

Section:

Score: 31%

*Since some answer boxes are correct when left blank, the beginning score is greater than 0%.

Key Code:

20Y5 20Y6 20Y7 20Y8

Capital Expenditures Budget

For the Four Years Ending December 31, 20Y5–20Y8

2

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

Exercise 13-17

Instructions

A red asterisk (*) will appear in the column immediately to the right of an incorrect answer.

HANDY DAN TOOLS INC.

Name:

Section:

Score: See student sheet for student’s score

Scoring:

*Since some answer boxes are correct when left blank, the beginning score is greater than 0%.

20Y5 20Y6 20Y7 20Y8

Capital Expenditures Budget

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

A red asterisk (*) will appear in the column immediately to the right of an incorrect answer.

ON

For the Four Years Ending December 31, 20Y5–20Y8

Exercise 13-17

SOLUTION

Instructions

HANDY DAN TOOLS INC.

Name:

Section:

Score: 0%

Key Code:

a.

b.

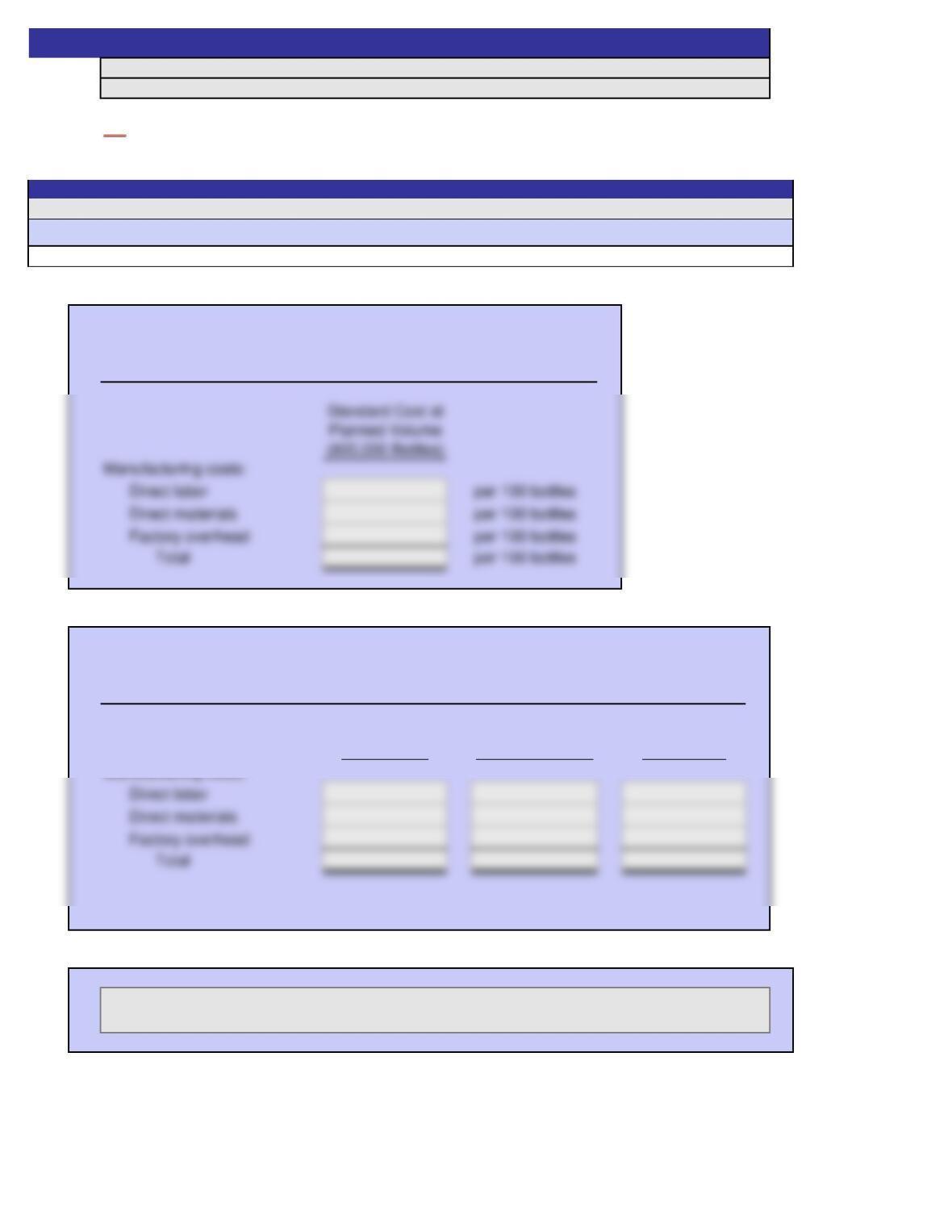

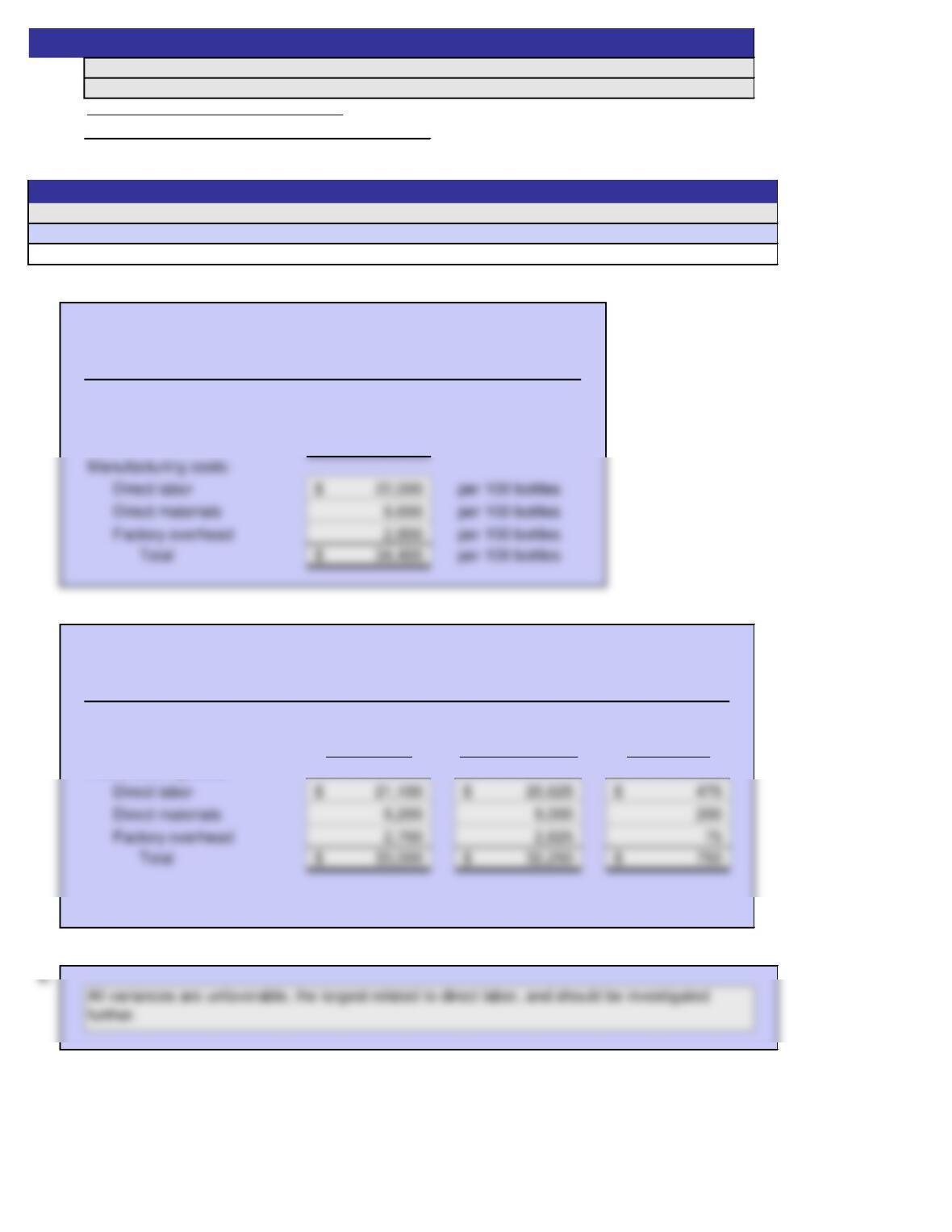

Standard Cost at Cost Variance –

Actual Volume (Favorable)

Actual Costs (750,000 Bottles) Unfavorable

Manufacturing costs:

c.

Manufacturing Costs – Budget Performance Report

For the Month Ended May 31

MCALISTERS BOTTLE COMPANY

Exercise 13-19

MCALISTERS BOTTLE COMPANY

Manufacturing Cost Budget

For the Month Ended May 31

2

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

A red asterisk (*) will appear immediately to the right of an incorrect answer.

Name:

Section

Score: See student sheet for student’s score

Scoring

a.

Standard Cost at

Planned Volume

(800,000 Bottles)

b.

Standard Cost at Cost Variance –

Actual Volume (Favorable)

Actual Costs (750,000 Bottles) Unfavorable

Manufacturing costs:

c.

MCALISTERS BOTTLE COMPANY

Manufacturing Cost Budget

For the Month Ended May 31

MCALISTERS BOTTLE COMPANY

Manufacturing Costs – Budget Performance Report

For the Month Ended May 31

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

A red asterisk (*) will appear immediately to the right of an incorrect answer.

Exercise 13-19

SOLUTION

Instructions

ON

Name:

Section:

Score: 0%

Key Code:

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

A red asterisk (*) will appear immediately beside or below an incorrect answer.

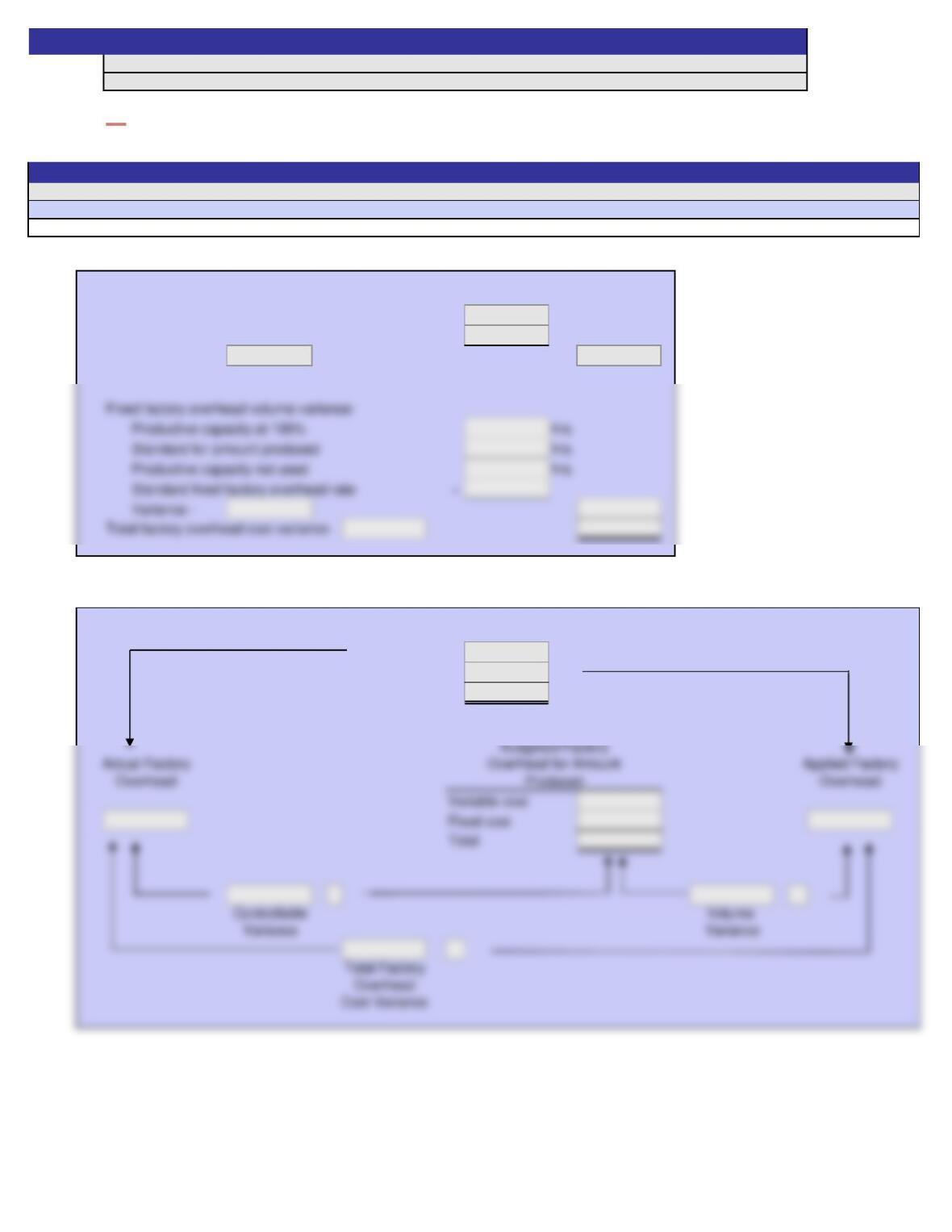

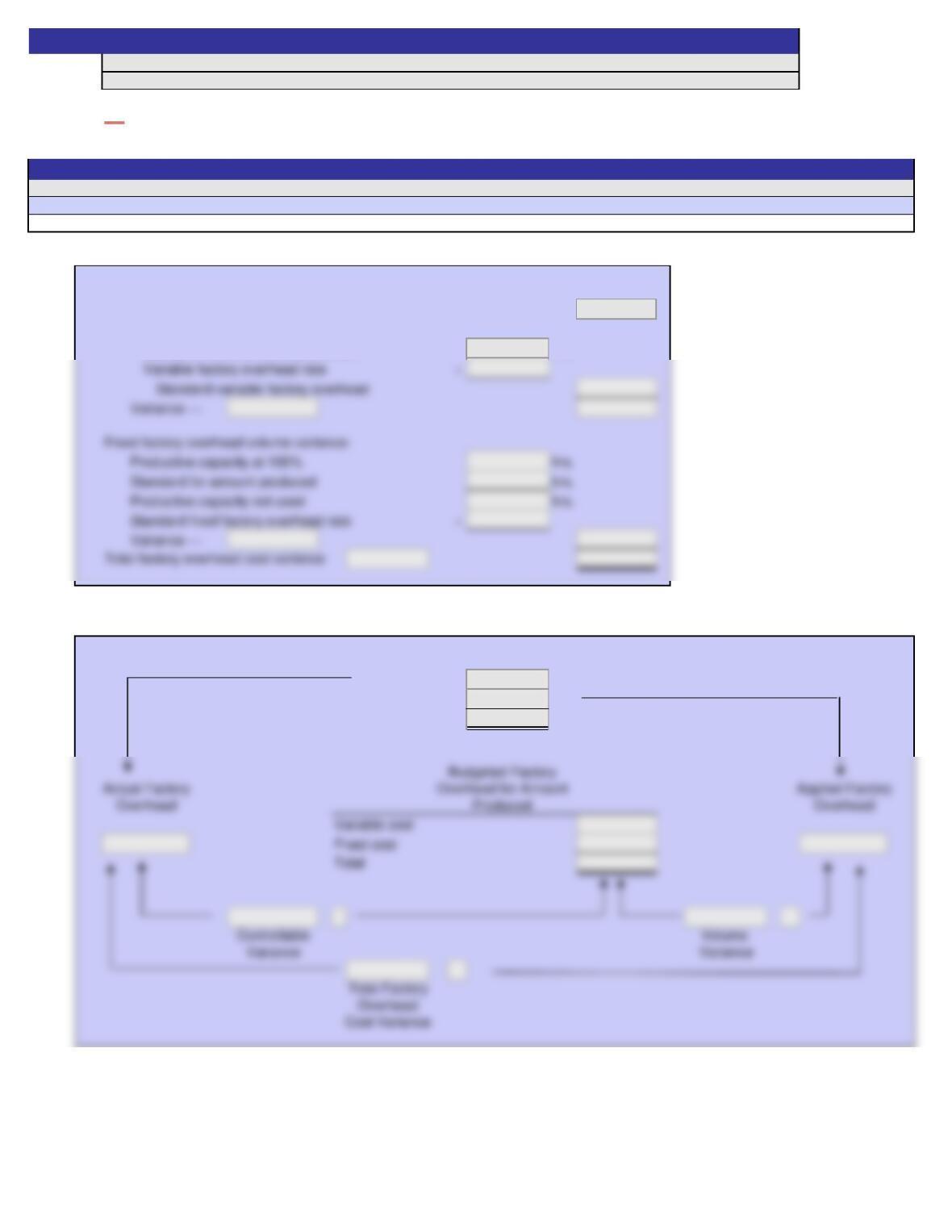

Variable overhead controllable variance:

Actual variable factory overhead cost incurred

Budgeted variable factory overhead for 8,000 hrs.

Variance –

Alternative Computation of Overhead Variances:

Actual costs

Applied costs

Balance

Exercise 13-29

Instructions

2

Productive capacity at 100%

Standard for amount produced

Productive capacity not used

Name:

Section:

Score: See student sheet for student’s score

Scoring:

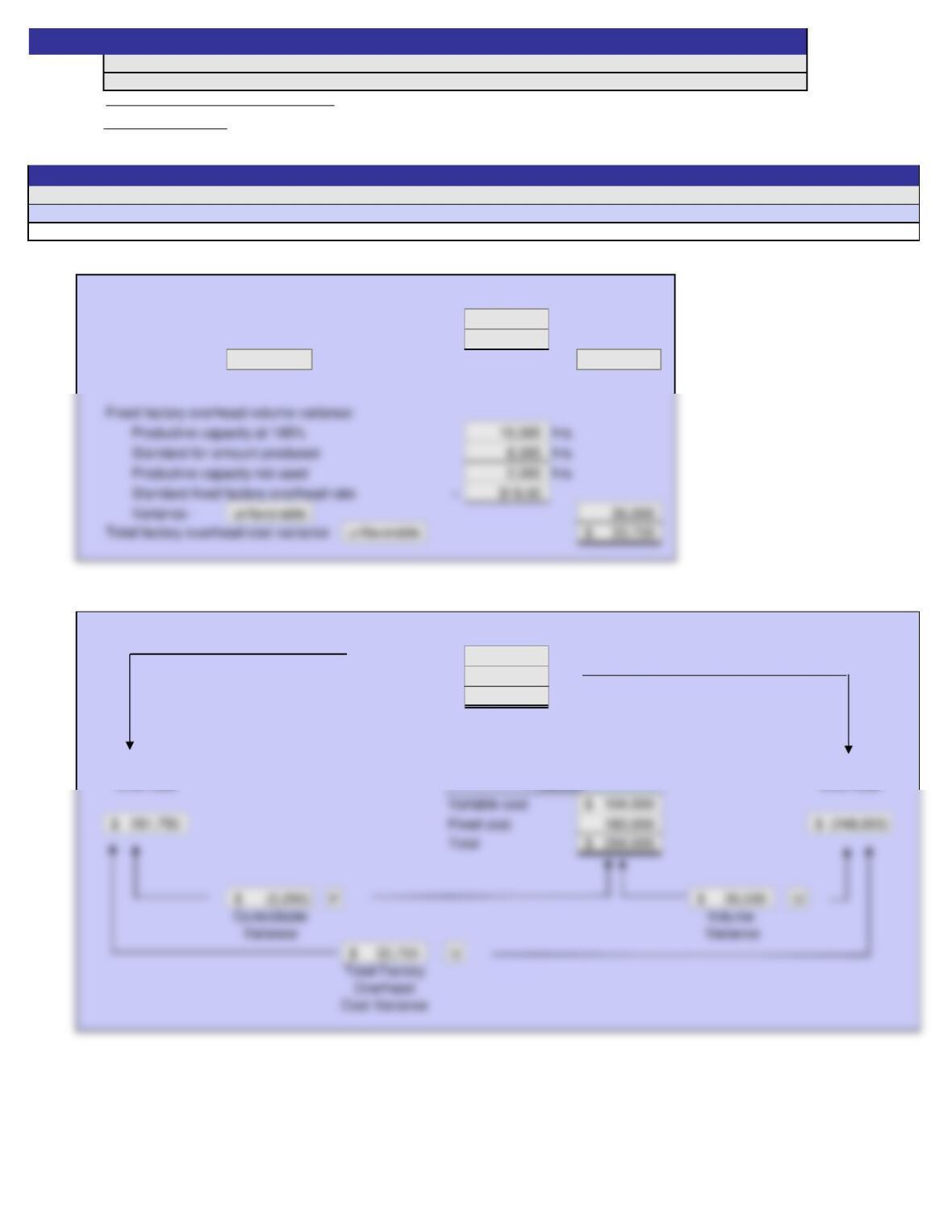

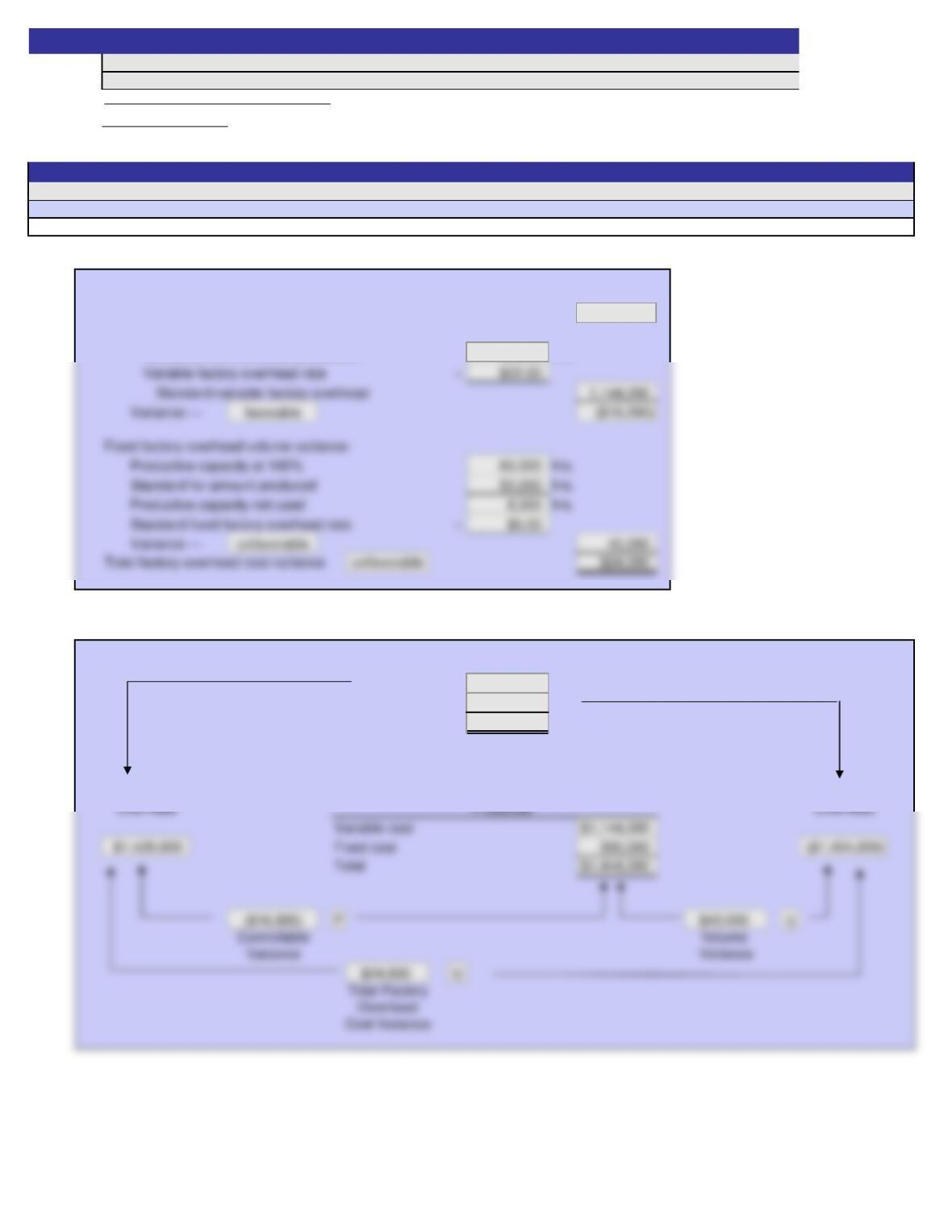

Variable overhead controllable variance:

Actual variable factory overhead cost incurred

101,750$

Budgeted variable factory overhead for 8,000 hrs.

104,000

Variance – favorable (2,250)$

Alternative Computation of Overhead Variances:

Actual costs

281,750$

Applied costs

(248,000)

Balance 33,750$

Actual Factory Applied Factory

Overhead Overhead

Produced

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

A red asterisk (*) will appear immediately beside or below an incorrect answer.

Exercise 13-29

SOLUTION

Budgeted Factory

ON

Overhead for Amount

Productive capacity at 100%

Standard for amount produced

Productive capacity not used

Name:

Section:

Score: 0%

Key Code:

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

A red asterisk (*) will appear immediately beside or below an incorrect answer.

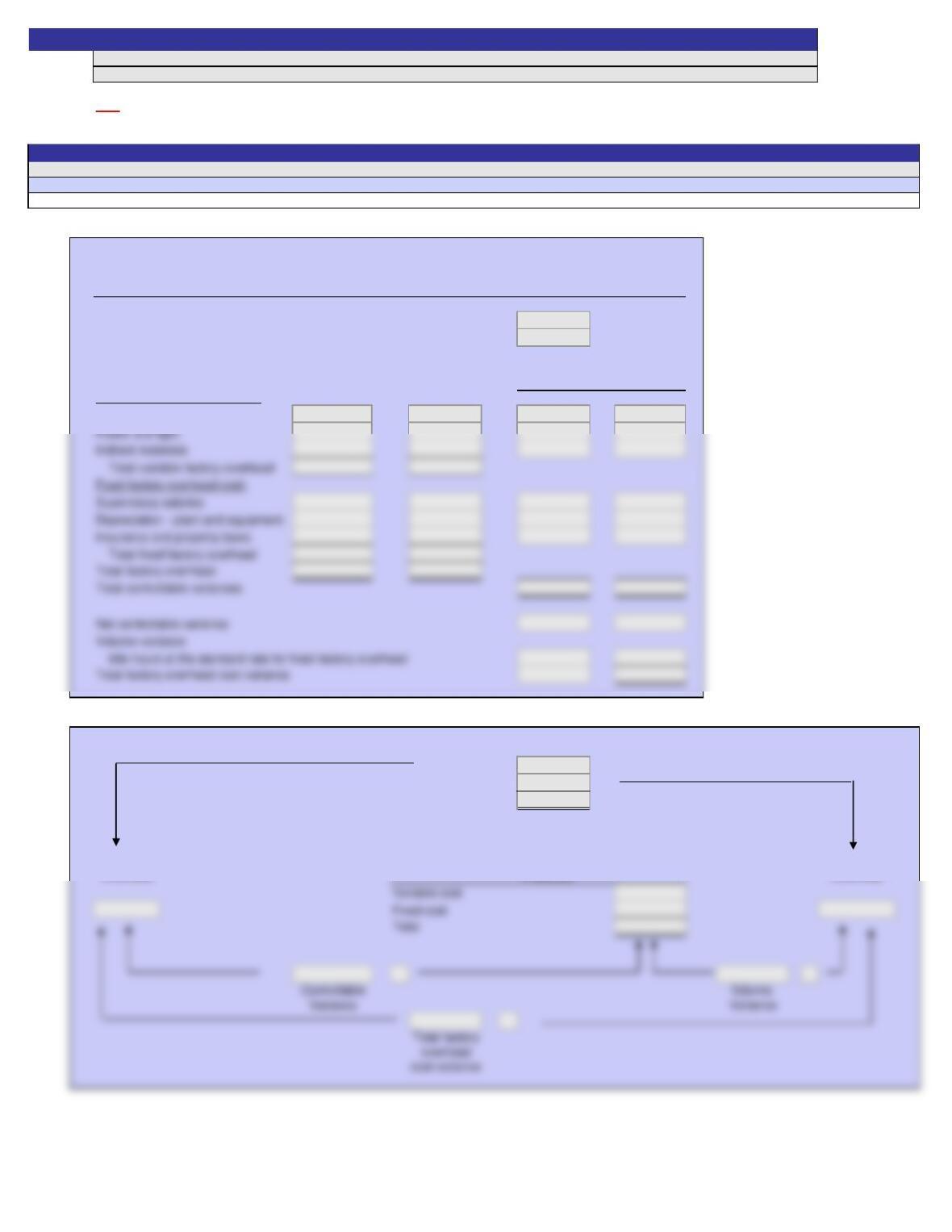

Variable overhead controllable variance:

Actual variable factory overhead cost incurred

Standard variable factory overhead at actual production:

Standard hours at actual production hrs.

Alternative Computation of Overhead Variances:

Actual costs

Applied costs

Balance

Exercise 13-30

Instructions

2

Productive capacity at 100%

Standard for amount produced

Productive capacity not used

Name:

Section:

Score:

See student sheet for student’s score

Scoring:

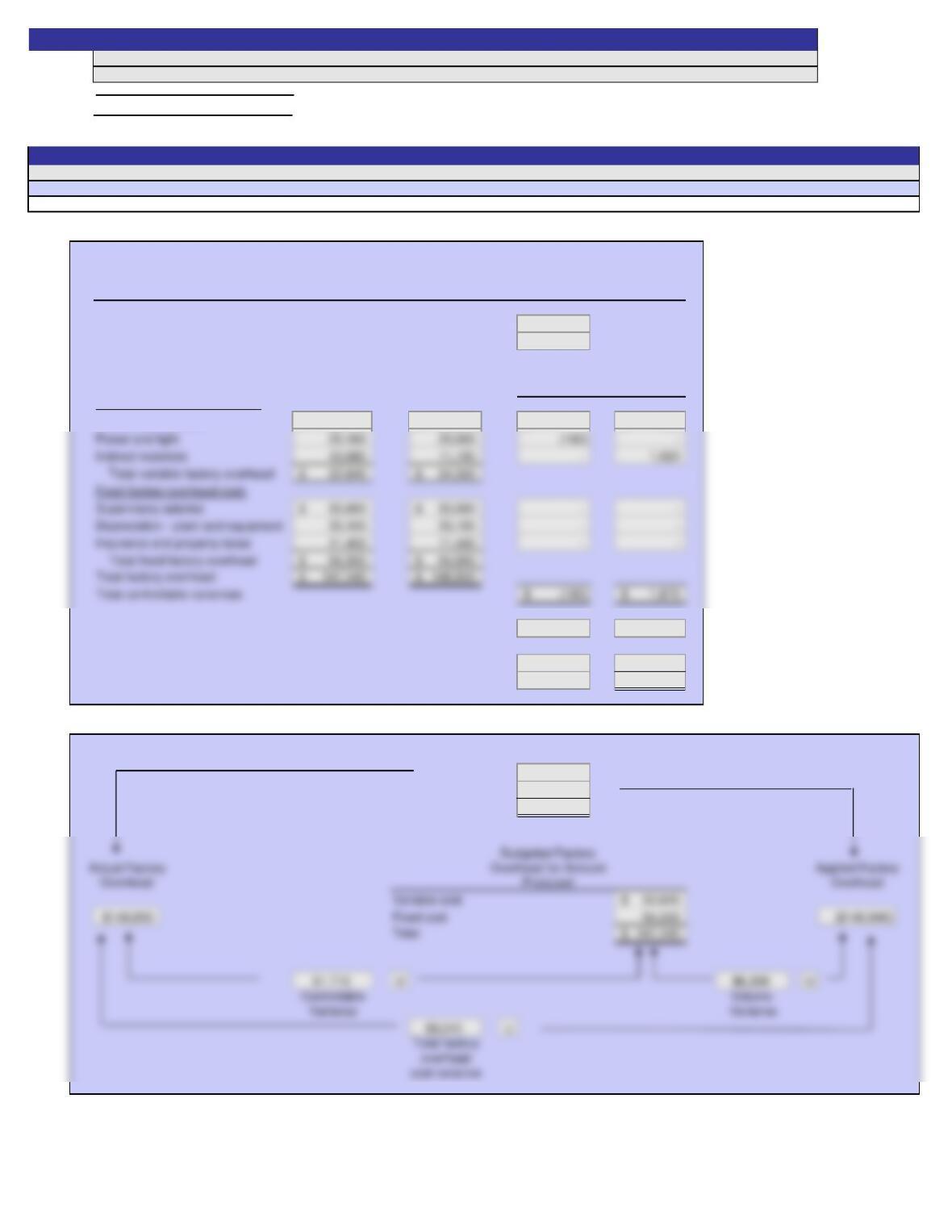

Variable overhead controllable variance:

Actual variable factory overhead cost incurred

$1,128,000

Standard variable factory overhead at actual production:

Standard hours at actual production 52,000 hrs.

Alternative Computation of Overhead Variances:

Actual costs

#########

Applied costs

(1,404,000)

Balance 24,000$

Actual Factory Applied Factory

Overhead for Amount

A red asterisk (*) will appear immediately beside or below an incorrect answer.

ON

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

Exercise 13-30

SOLUTION

Instructions

Budgeted Factory

Productive capacity at 100%

Standard for amount produced

Productive capacity not used

Name:

Section:

Score: 17%

*Since some answer boxes are correct when left blank, the beginning score is greater than 0%.

Key Code:

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

A red asterisk (*) will appear immediately beside or below an incorrect answer.

Productive capacity for the month hrs.

Actual productive capacity used for the month hrs.

Budget

(at actual

Variable factory overhead cost: production) Actual Favorable Unfavorable

Indirect factory labor

Alternative Computation of Overhead Variances:

Actual costs

Applied costs

Balance

Actual Factory Applied Factory

Overhead Overhead

Overhead for Amount

Produced

TOPEKA PLASTICS INC.

Factory Overhead Cost Variance Report—Trim Department

For the Month Ended July 31

Variances

Exercise 13-32

Instructions

2

Budgeted Factory

Name:

Section:

Score: See student sheet for student’s score

Scoring:

*Since some answer boxes are correct when left blank, the beginning score is greater than 0%.

Productive capacity for the month 30,000 hrs.

Actual productive capacity used for the month 28,000 hrs.

Budget

(at actual

Variable factory overhead cost: production) Actual Favorable Unfavorable

Indirect factory labor 22,400$ 23,250$ –$ 850$

Net controllable variance unfavorable 1,710$

Volume variance

Idle hours at the standard rate for fixed factory overhead unfavorable 6,300

Total factory overhead cost variance unfavorable 8,010$

Alternative Computation of Overhead Variances:

Actual costs

148,850$

Applied costs

(140,840)

Balance 8,010$

TOPEKA PLASTICS INC.

A red asterisk (*) will appear immediately beside or below an incorrect answer.

For the Month Ended July 31

Variances

Instructions

Answers are entered in the cells with gray backgrounds.

Cells with non-gray backgrounds are protected and cannot be edited.

Factory Overhead Cost Variance Report—Trim Department

ON

Exercise 13-32

SOLUTION