25 Minutes, Medium

a.

Cash flows from operating activities:

Net income 928,000$

Add: Depreciation expense 49,000$

Increase in accounts payable to suppliers 5,000

Increase in accrued interest payable 2,000 56,000

Subtotal 984,000$

Less: Increase in accounts receivable 10,000$

PROBLEM 13.5B

ROYCE INTERIORS, INC.

For the Year Ended December 31, 2018

Partial Statement of Cash Flows

ROYCE INTERIORS, INC.

(INDIRECT)

Increase in accrued interest receivable 4,000

Increase in inventories 25,000

45 Minutes, Strong

a.

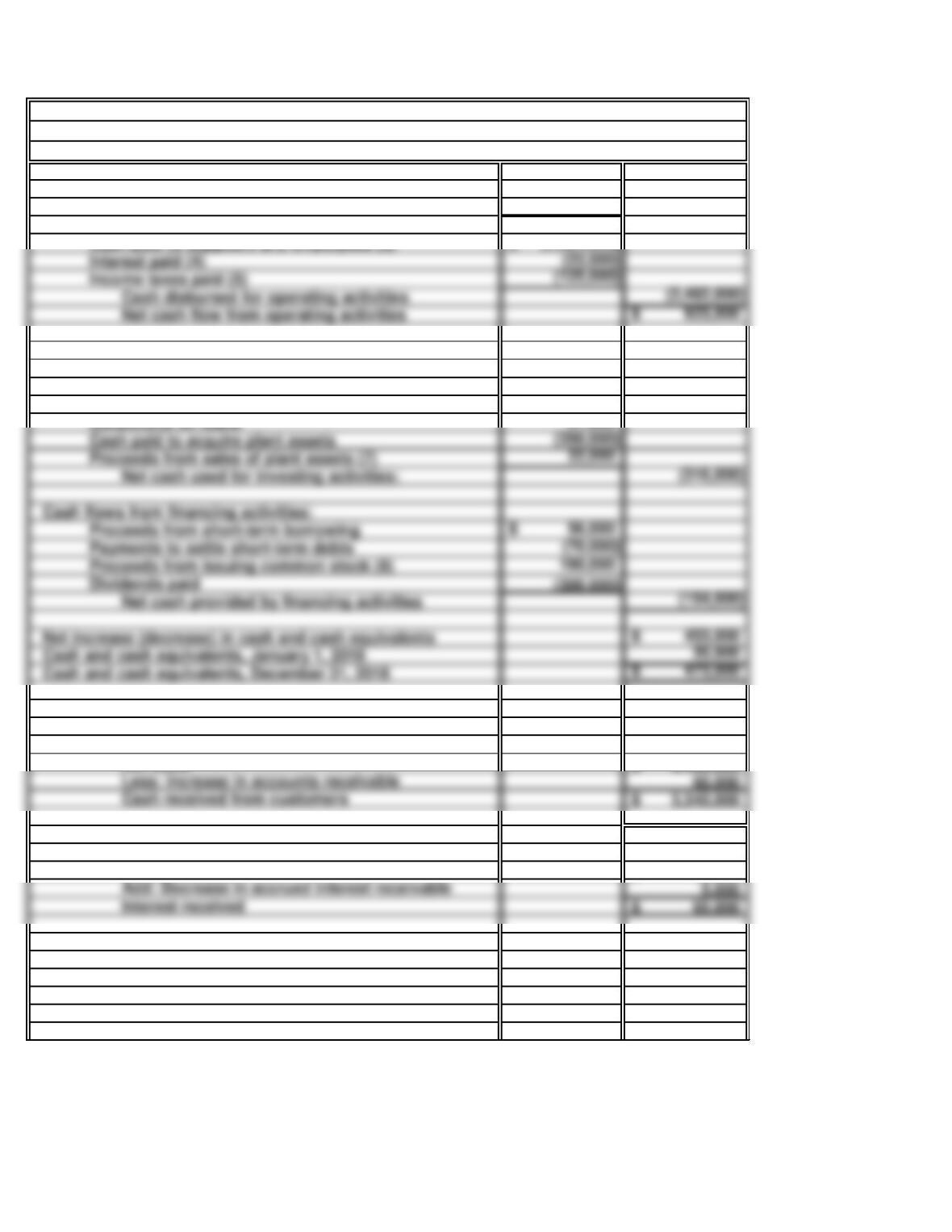

Cash flows from operating activities:

Cash received from customers (1) 3,340,000$

Interest received (2) 65,000

Cash provided by operating activities 3,405,000

Cash paid to suppliers and employees (3) (2,334,000)$

Cash flows from investing activities:

Purchases of marketable securities (50,000)$

Proceeds from sales of marketable securities (6) 65,000

Loans made to borrowers (30,000)

Collections on loans 27,000

Cash paid to acquire plant assets (350,000)

Proceeds from sales of plant assets (7) 22,000

Proceeds from short-term borrowing 56,000$

Payments to settle short-term debts (70,000)

Proceeds from issuing common stock (8) 160,000

Net increase (decrease) in cash and cash equivalents 453,000$

Supporting computations:

(1)

Net sales 3,400,000$

Less: increase in accounts receivable 60,000

Cash received from customers 3,340,000$

(2) Interest received:

Interest income 60,000$

Interest received 65,000$

Cash received from customers:

PROBLEM 13.6B

FOXBORO TECHNOLOGIES

For the Year Ended December 31, 2018

Statement of Cash Flows

FOXBORO TECHNOLOGIES

Interest paid (4) (23,000)

Income taxes paid (5) (125,000)

Net cash flow from operating activities 923,000$

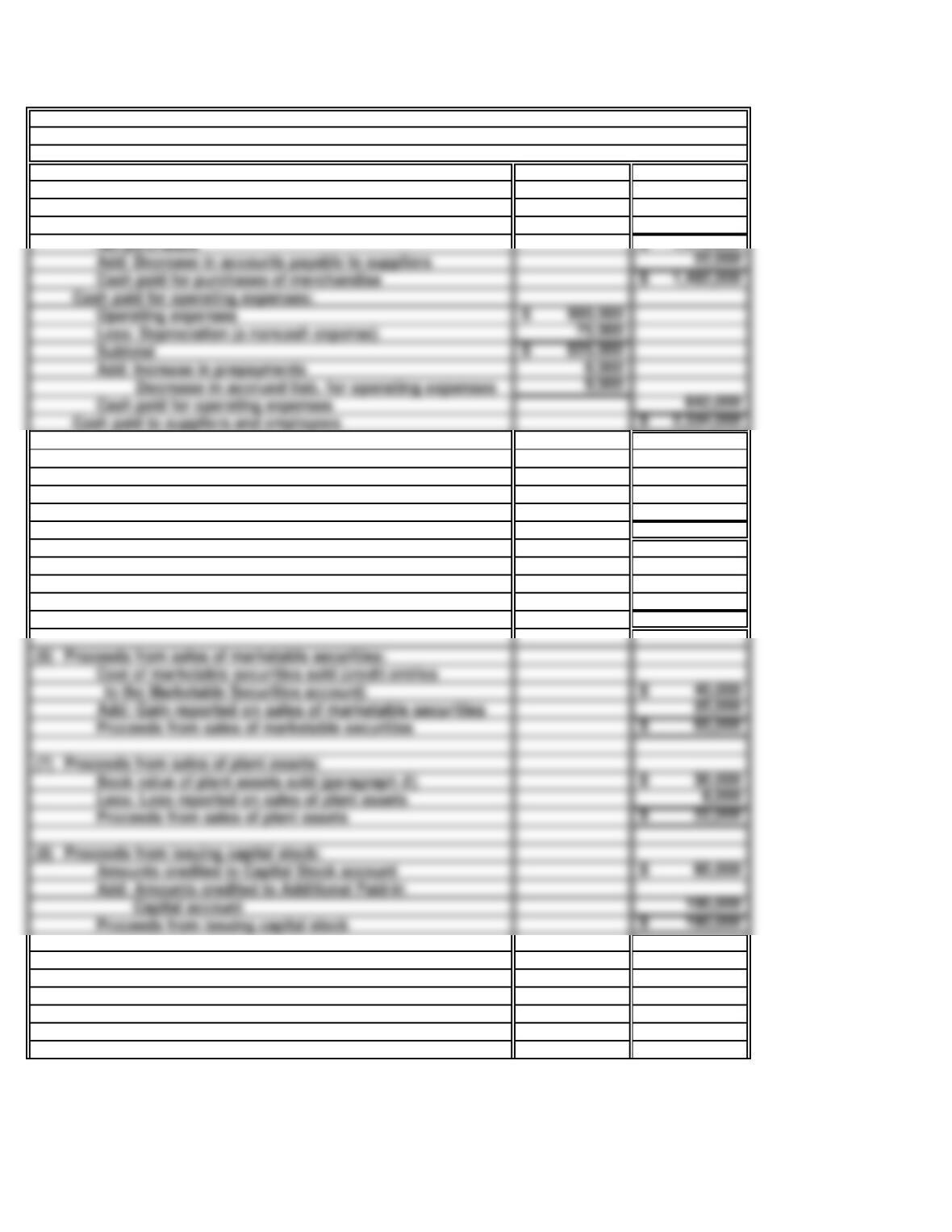

(3) Cash paid to suppliers and employees:

Cost of goods sold 1,500,000$

Less: Decrease in inventory 30,000

(4) Interest paid:

Interest expense 27,000$

Less: Increase in accrued interest payable 4,000

Interest paid 23,000$

(5) Income taxes paid:

Income tax expense 115,000$

Add: Decrease in income taxes payable 10,000

Income taxes paid 125,000$

(6) Proceeds from sales of marketable securities:

Cost of marketable securities sold (credit entries

to the Marketable Securities account) 40,000$

Proceeds from sales of marketable securities 65,000$

(7) Proceeds from sales of plant assets:

Proceeds from sales of plant assets 22,000$

(8) Proceeds from issuing capital stock:

Amounts credited to Capital Stock account 60,000$

Add: Amounts credited to Additional Paid-in

Proceeds from issuing capital stock 160,000$

Cash paid for purchases of merchandise:

PROBLEM 13.6B

FOXBORO TECHNOLOGIES

(continued)

Net purchases 1,470,000$

Operating expenses 900,000$

Less: Depreciation (a noncash expense) 75,000

Add: Increase in prepayments 8,000

Cash paid for operating expenses 842,000

●

●

c.

On the contrary, the fact that cash flows from investing and financing activities are negative

attests to the strength of the cash position of the company. The amount of cash increased

PROBLEM 13.6B

FOXBORO TECHNOLOGIES (concluded)

In addition to cost of goods sold, operating expenses required the payment of a

$1,500,000. The primary reasons for the difference are as follows:

40 Minutes, Strong

a.

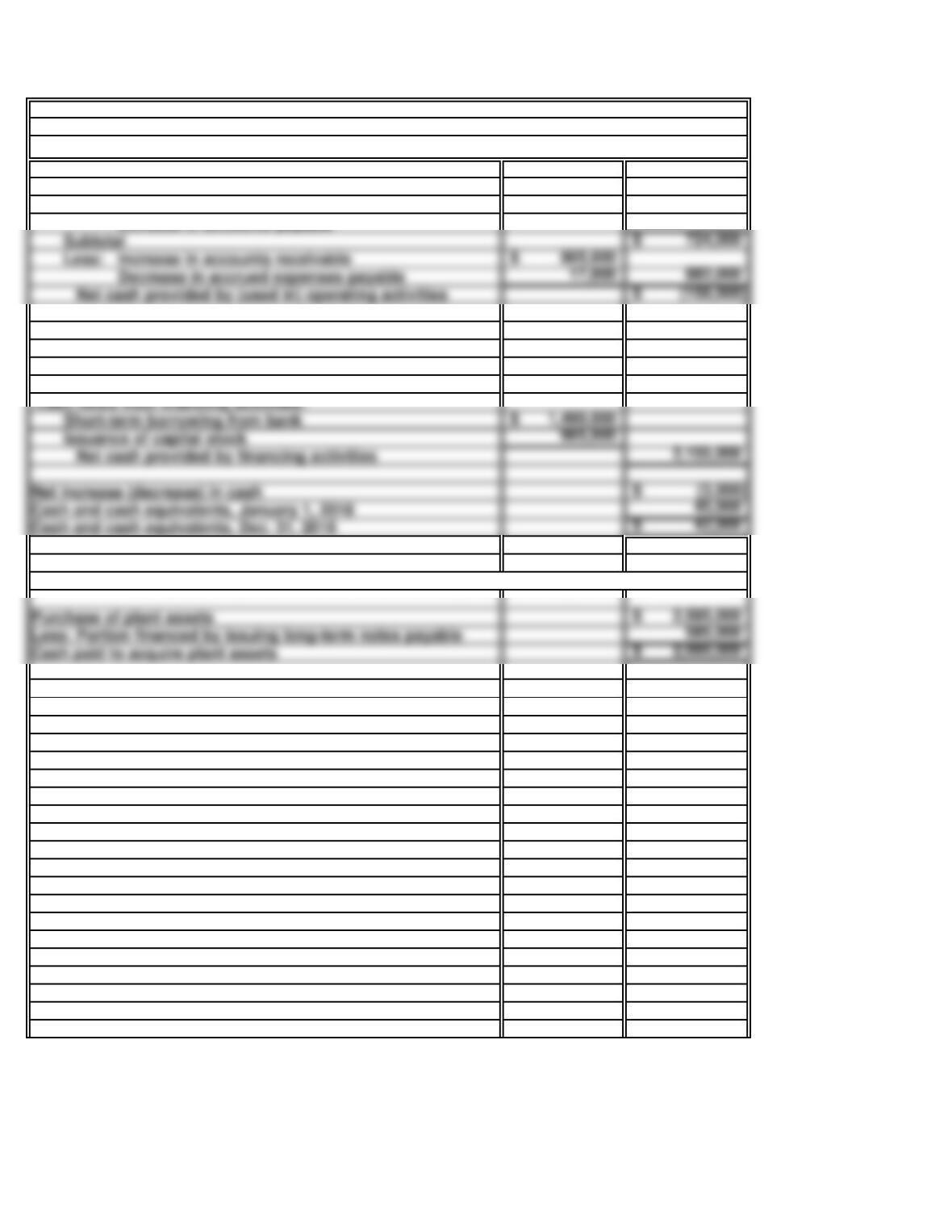

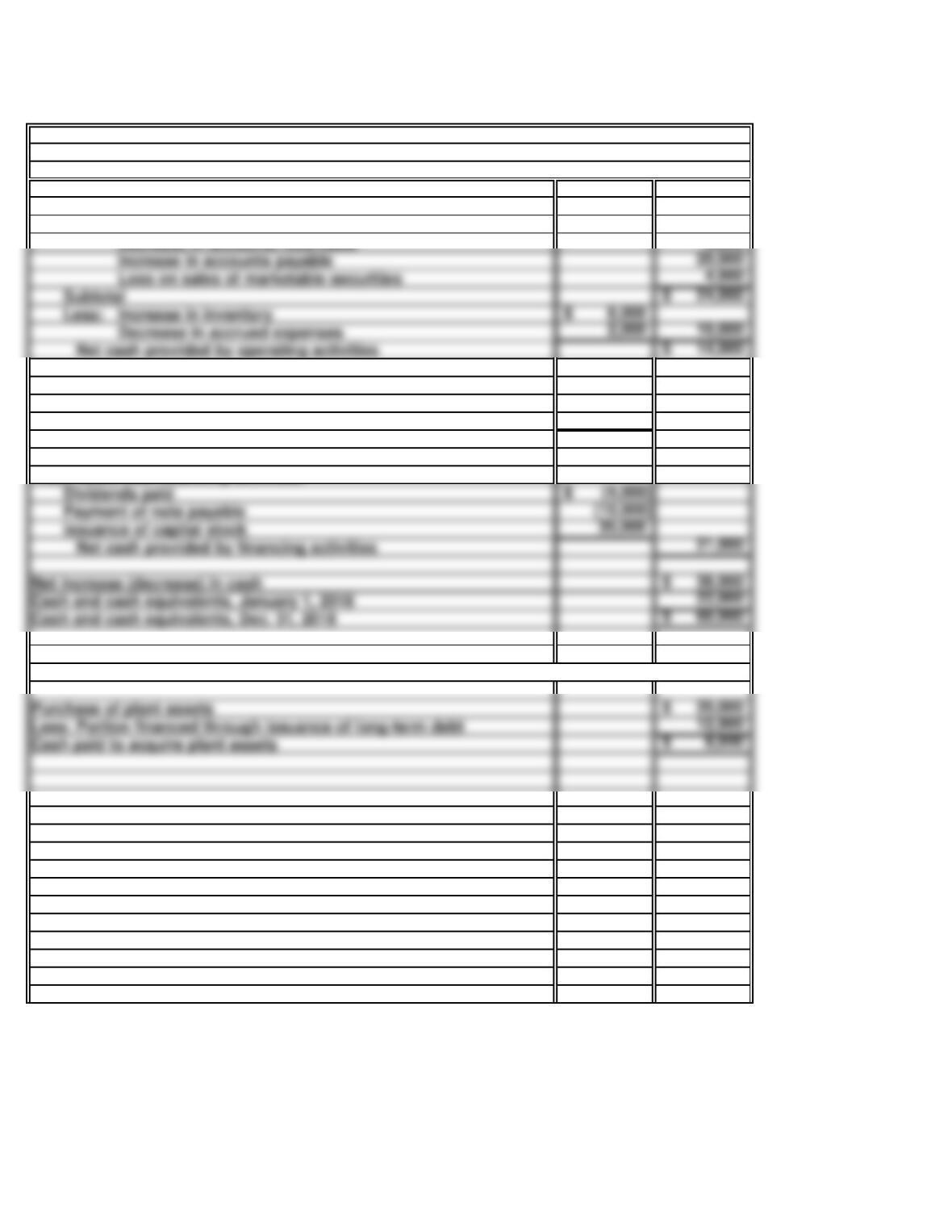

Cash flows from operating activities:

Net income 562,000$

Add: Depreciation expense 125,000

Increase in accounts payable 37,000

Cash flows from investing activities:

Cash paid to acquire plants assets (see schedule) (2,000,000)$

Net cash used for investing activities (2,000,000)

Cash flows from financing activities:

Short-term borrowing from bank 1,490,000$

Supplementary Schedule: Noncash Investing and Financing Activities

PROBLEM 13.7B

LGIN

For the Year Ended December 31, 2018

Statement of Cash Flows

LGIN

Less: Increase in accounts receivable 865,000$

Decrease in accrued expenses payable 17,000 882,000

Net cash provided by (used in) operating activities (158,000)$

b.

c.

LGIN does not appear headed for insolvency. First, the company has a $4.5 million line of

PROBLEM 13.7B

LGIN (concluded)

LGIN’s credit sales resulted in $865,000 in new receivables, which were uncollected as of

year-end. These credit sales all were included in the computation of net income, but those

cash” to finance their growth.

60 Minutes, Strong

a.

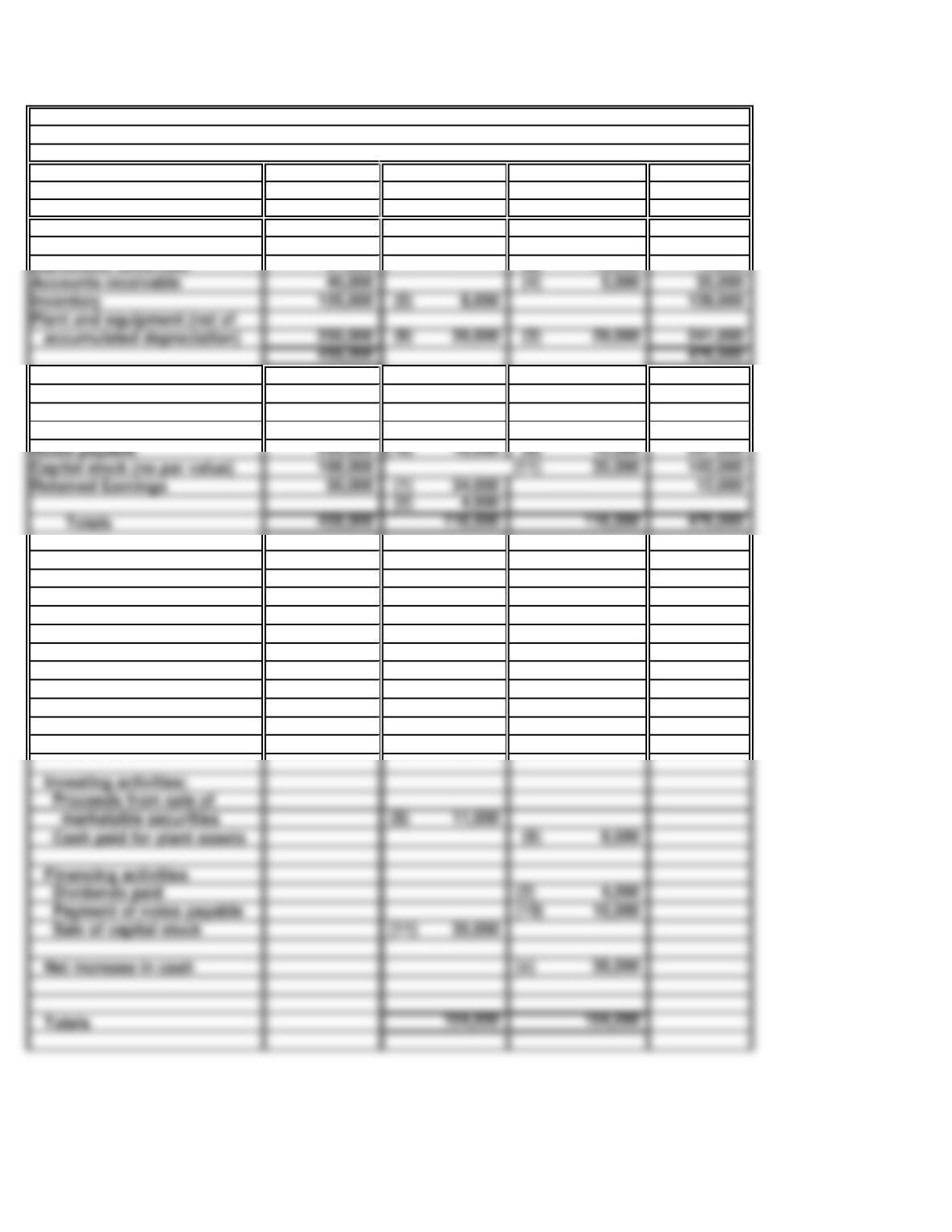

Balance sheet effects:

Beginning Ending

Balance Balance

Cash and cash equivalents 22,000 (x) 38,000 60,000

27,000 (8) 15,000 12,000

Liabilities & Owners’ Equity

50,000 (6) 20,000 70,000

16,000 (7) 2,000 14,000

50,000 (1) 34,000 12,000

Totals

Capital stock (no par value)

Retained Earnings

Notes payable

Cash effects:

Operating activities:

(1) 34,000

(3) 29,000

(4) 5,000

Increase in inventory (5) 8,000

(6) 20,000

(7) 2,000

(8) 4,000

(8) 11,000

Cash paid for plant assets (9) 8,000

Net increase in cash (x) 38,000

Sale of capital stock

Dividends paid

Payment of notes payable

marketable securities

Proceeds from sale of

Loss on sale of marketable

securities

Net loss

Depreciation expense

Decrease in accrued

expenses payable

Decrease in accounts rec.

Increase in accounts pay.

Marketable securities

Sources

Uses

Accounts payable

Accrued expenses payable

PURCELLS, INC.

PROBLEM 13.8B

Changes

Changes

PURCELLS, INC.

Worksheet for a Statement of Cash Flows

Assets

For the Year Ended December 31, 2018

Debit

Credit

40,000 (4) 5,000 35,000

Plant and equipment (net of

accumulated depreciation)

Accounts receivable

PROBLEM 13.8B

PURCELLS, INC.

(continued)

b.

Cash flows from operating activities:

Net loss (34,000)$

Add: Depreciation expense 29,000

Cash flows from investing activities:

Proceeds from sales of marketable securities 11,000$

Cash paid to acquire plants assets (see supplementary schedule) (8,000)

Net cash provided by investing activities 3,000

Cash flows from financing activities:

Dividends paid (4,000)$

Payment of note payable (10,000)

issuance of capital stock 35,000

Net cash provided by financing activities 21,000

Net increase (decrease) in cash 38,000$

Supplementary Schedule: Noncash Investing and Financing Activities

PURCELLS, INC.

For the Year Ended December 31, 2018

Statement of Cash Flows

Less: Increase in inventory 8,000$

Net cash provided by operating activities 14,000$

c.

d.

e.

f.

This company is contracting its operations (or collapsing). Its investment in marketable

securities, receivables, and plant assets all are declining. Further, the income statement

The company’s principal revenue source—sales of Pulsas—is declining. If nothing is done,

it is likely that the annual net losses will increase, and that operating cash flows soon will

Purcells, Inc. has substantially more cash than it did a year ago. Nonetheless, the

PROBLEM 13.8B

PURCELLS, INC. (continued)

Purcells, Inc. achieved its positive cash flow from operating activities basically by

liquidating assets and by not paying its bills. It has converted most of its accounts

receivable into cash, which probably means that credit sales have declined substantially

•

PROBLEM 13.8B

PURCELLS, INC. (concluded)

If management decides to continue business operations, it should take the following actions:

Expand the company’s product lines! The Pulsas alone can no longer support profitable

operations. Also, dependency upon a single product—especially a faddish product with a

•

•

•

•

25 Minutes, Strong

a.

b.

Two of the unusual factors appearing in the current statement of cash flows should be

considered in assessing the company’s ability to pay future dividends. First, the company

SOLUTIONS TO CASES

ANOTHER LOOK AT ALLISON CORPORATION

CASE 13.1

Based on past performance, it does not appear that Allison Corporation can continue to pay

annual dividends of $40,000 without straining the cash position of the company. In a typical

15 Minutes, Easy

a.

b.

Week 4: $100 ($60 + $100 − $30 − $20 − $10)

Week 2: $20 [$(20) + $100 − $30 − $20 − $10]

Week 3: $60 ($20 + $100 − $30 − $20 − $10)

In Week 1 you have two problems. The first is that you do not have enough cash to pay your

rent on Wednesday. But you will by Friday, so your payment may be a couple of days late.

(But what’s going to happen next month? Is there some “handwriting on the wall”?)

CASE 13.2

Ending cash balances:

CASH BUDGETING FOR YOU AS A STUDENT

Cash

Increase No effect No effect

b. (1)

(2)

(3)

(4)

If the costs of producing inventory are rising, use of the FIFO (first-in, first-out)

Changing from an accelerated method to the straight-line method of depreciation will

Requiring dealers to pay more quickly will speed up cash collections from customers,

proposal upon net income; see discussion in paragraph (4), part b.

Net Cash Flows from

Operating Activities

Net Income

CASE 13.3

LOOKIN’ GOOD?

45 Minutes, Medium

a.

(1)

Proposals

Increase No effect No effect

No effect Increase Increase

(or decrease)* (or decrease)*

No effect No effect Increase

(3)

(4)

(6)

(7)

(2)

(5)

(5)

(6)

(7)

CASE 13.3

LOOKIN’ GOOD? (concluded)

Passing up cash discounts will delay many cash outlays by about 20 days. In the long run,

Incurring short-term interest charges of 10% to replace long-term interest charges of 13%

Dividend payments do not enter into the determination of net income or net cash flow from

15 Minutes, Easy

a.

c. (1)

d.

CASE 13.4

PEAK PRICING

In the opinion of the authors, peak pricing normally is an ethical business practice. But

there are exceptions, and management should think carefully about its responsibilities.

The statement is not valid because it addresses only the peak-period aspect of a peak-pricing

Hotels in Palm Springs charge their highest daily rates during the sunny but

b.

The alternative to peak pricing is a single all-the-time price. In this case, excess demand is

20 Minutes, Medium

IMPROVING THE STATEMENT OF CASH FLOWS

CASE 13.5

The first four parts of this case have no written requirements. Part (d) requires students to

write a synopsis, based on their research in the Securities & Exchange Commission’s (SEC)

web site, of a speech given by SEC staff member Scott Taub, in which he makes a specific

reference to the statement of cash flows.

Following are several points that are appropriate for inclusion in the student’s response to

this case:

ETHICS, FRAUD & CORPORATE GOVERNANCE

Improvement can come by looking at reporting as a communications exercise rather

than a compliance exercise.

30 Minutes, Medium

CASE 13.6

FROM TWO COMPANIES

INTERNET

c.

Based on the following information from the 2015 financial statements

of the two companies, Amazon’s positive cash flow from operations in 2015 exceeded

d.

e.

Companies that may have negative cash flows from operations are companies that are

Companies with established products or services in established industries will often

COMPARING CASH FLOW INFORMATION

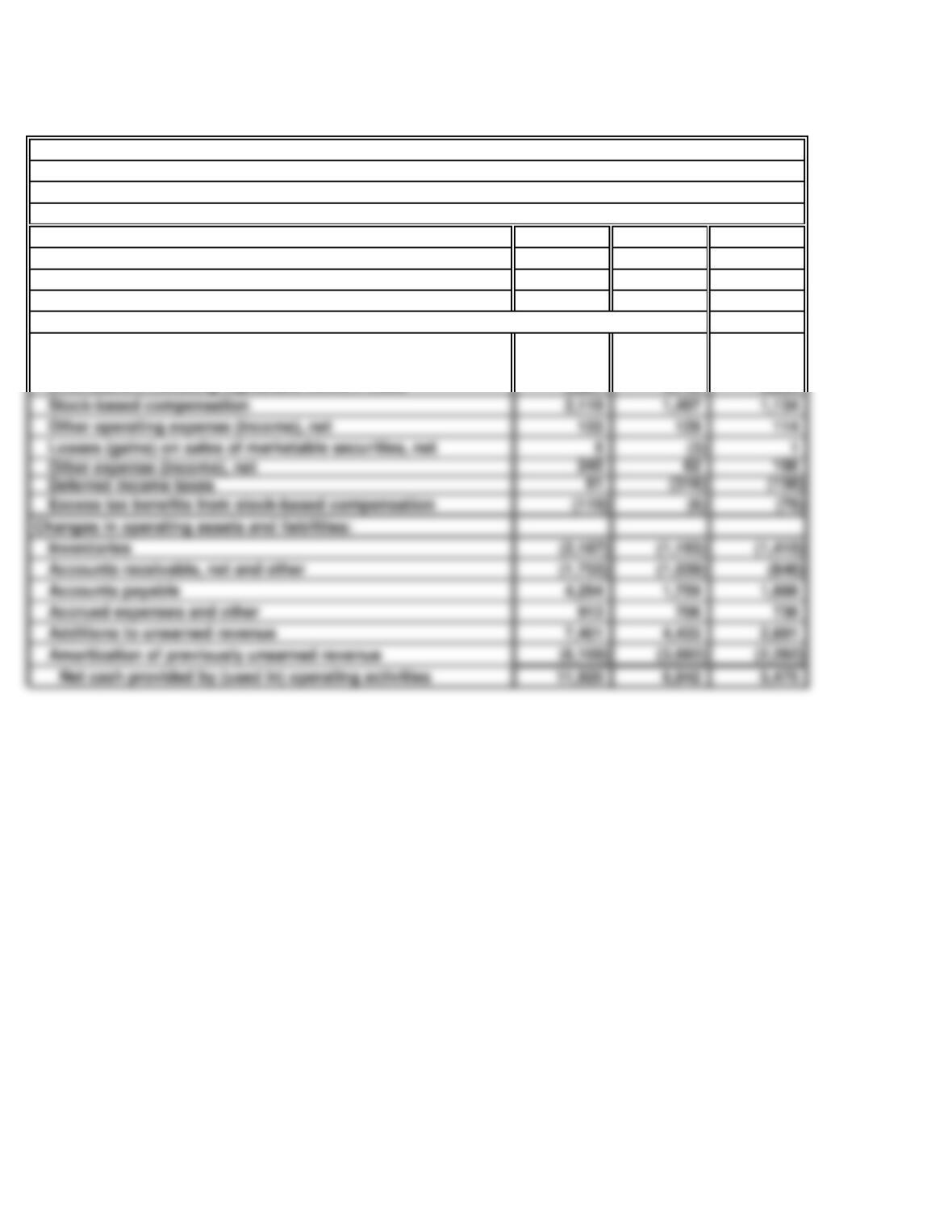

b.

2015 2014 2013

OPERATING ACTIVITIES

Consolidated net income 7,366$ 7,124$ 8,626$

Depreciation and amortization 1,970 1,976 1,977

Stock-based compensation expense 236 209 227

(in millions)

THE COCA-COLA COMPANY AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

Year ended December 31

Deferred income taxes 73 (40) 648

Foreign currency adjustments (137) 415 168

Other operating charges 929 761 465

Net change in operating assets and liabilities (157) (439) (932)

(in millions)

2015 2014 2013

CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD 14,557$ 8,658$ 8,084$

OPERATING ACTIVITIES:

Net income (loss) 596 (241)$ 274$

Adjustments to reconcile net income (loss) to net cash from operating activities:

6,281 4,746 3,253

Depreciation of property and equipment, including internal-

use software and website development, and other

amortization, including capitalized content costs

AMAZON.COM, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

Year ended December 31

(in millions)