EXERCISE 13-12

MEMO

To: President

From: Your name , Chief Accountant

Re: Questions about Stockholders’ Equity Section

Your memorandum about the stockholders’ equity section was received this

morning. I hope the following will answer your questions.

EXERCISE 13-13

ALUMINUM COMPANY OF AMERICA

Stockholders’ equity (in millions of dollars)

Paid-in capital

Capital stock

Preferred stock, $100 par value,

557,740 shares authorized,

557,649 shares issued and

546,024 shares outstanding ………………….. $ 56

Common stock, $1 par value,

1,800,000,000 shares authorized,

EXERCISE 13-14

Paid-in Capital

Account

Capital

Stock

Additional

Retained

Earnings

Other

Common Stock …………………………...

Preferred Stock …………………………..

Treasury Stock …………………………...

X

X

X

SOLUTIONS TO PROBLEMS

PROBLEM 13-1A

(a) Jan. 10 Cash (80,000 X $4) ……………………………. 320,000

Common Stock (80,000 X $2) ……… 160,000

Paid-in Capital in Excess of

Stated Value—Common

Stock (80,000 X $2) …………………. 160,000

Apr. 1 Land ………………………………………………… 85,000

Common Stock (24,000 X $2) ……… 48,000

Paid-in Capital in Excess of

Stated Value—Common

Stock ($85,000 – $48,000) ……….. 37,000

Aug. 1 Organization Expense ………………………. 30,000

Common Stock (10,000 X $2) ……… 20,000

Paid-in Capital in Excess of

Stated Value—Common

Stock ($30,000 – $20,000) ……….. 10,000

PROBLEM 13-1A (Continued)

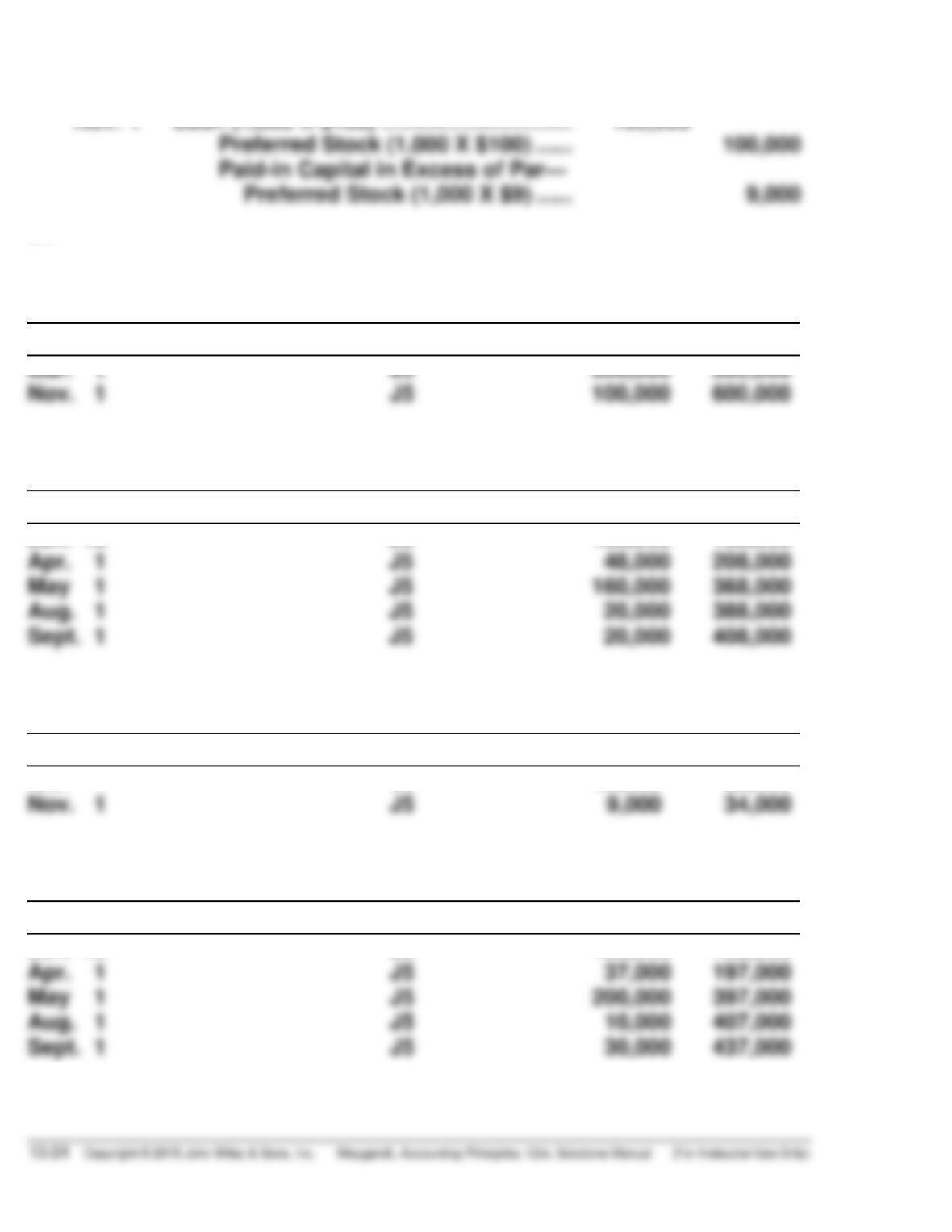

Nov. 1 Cash (1,000 X $109) …………………………. 109,000

Preferred Stock (1,000 X $100) …… 100,000

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 10

Apr. 1

J5

J5

160,000

48,000

160,000

208,000

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Mar. 1

J5

25,000

25,000

Paid-in Capital in Excess of Stated Value—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 10

Apr. 1

J5

J5

160,000

37,000

160,000

197,000

PROBLEM 13-1A (Continued)

(c) DELONG CORPORATION

Paid-in capital

Capital stock

8% Preferred stock, $100 par

value, 10,000 shares

authorized, 6,000 shares

issued and outstanding ……………… $ 600,000

Common stock, no par, $2

stated value, 500,000 shares

authorized, 204,000 shares

PROBLEM 13-2A

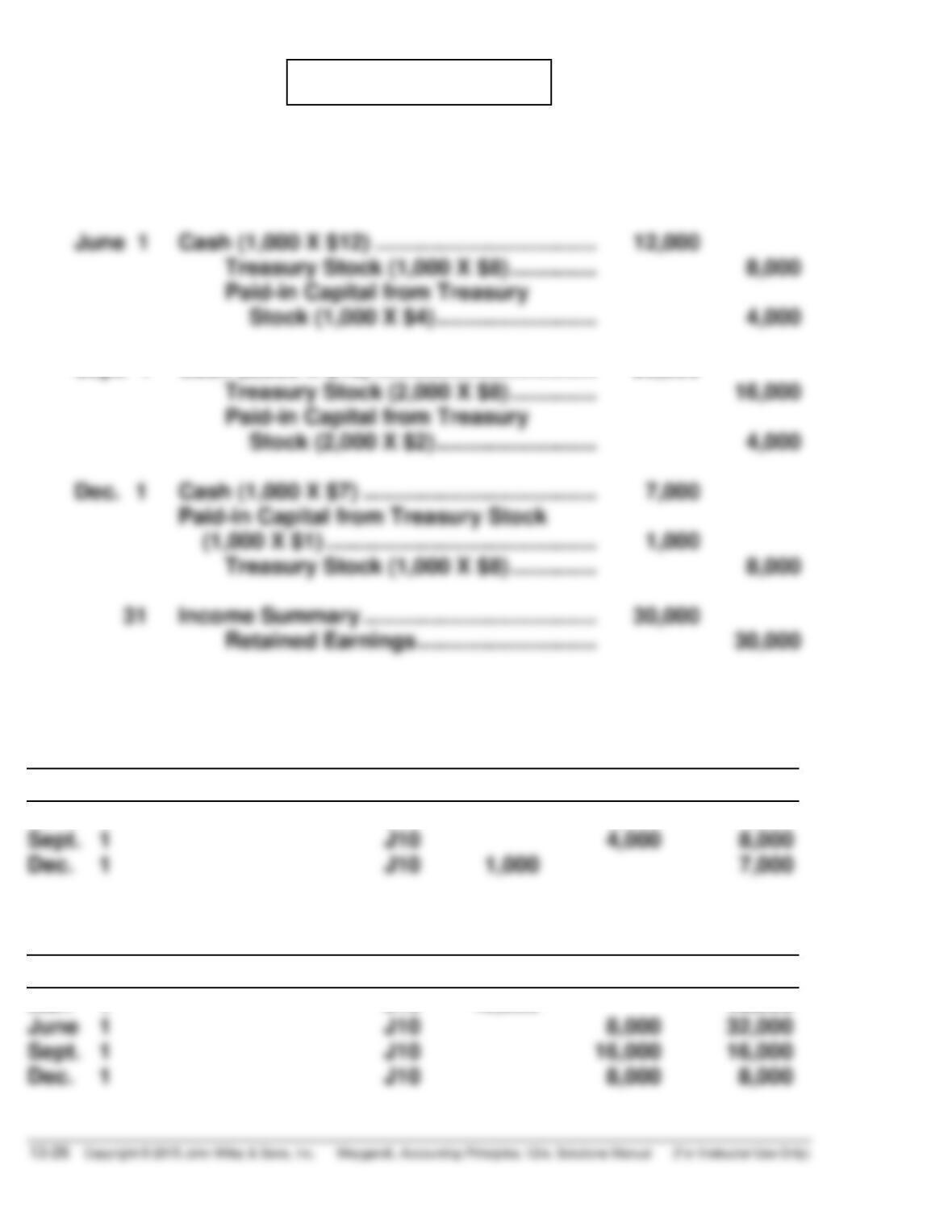

(a) Mar. 1 Treasury Stock (5,000 X $8) ………………… 40,000

Cash …………………………………………… 40,000

Sept. 1 Cash (2,000 X $10) ……………………………… 20,000

Treasury Stock (2,000 X $8) ………….. 16,000

Paid-in Capital from Treasury

Stock (2,000 X $2) …………………….. 4,000

(b)

Paid-in Capital from Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

June 1

J10

4,000

4,000

Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Mar. 1

J10

40,000

40,000

PROBLEM 13-2A (Continued)

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

100,000

(c) FECHTER CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $5 par,

100,000 shares issued and

99,000 outstanding……………… $500,000

Additional paid-in capital

In excess of par ……………………… $200,000

PROBLEM 13-3A

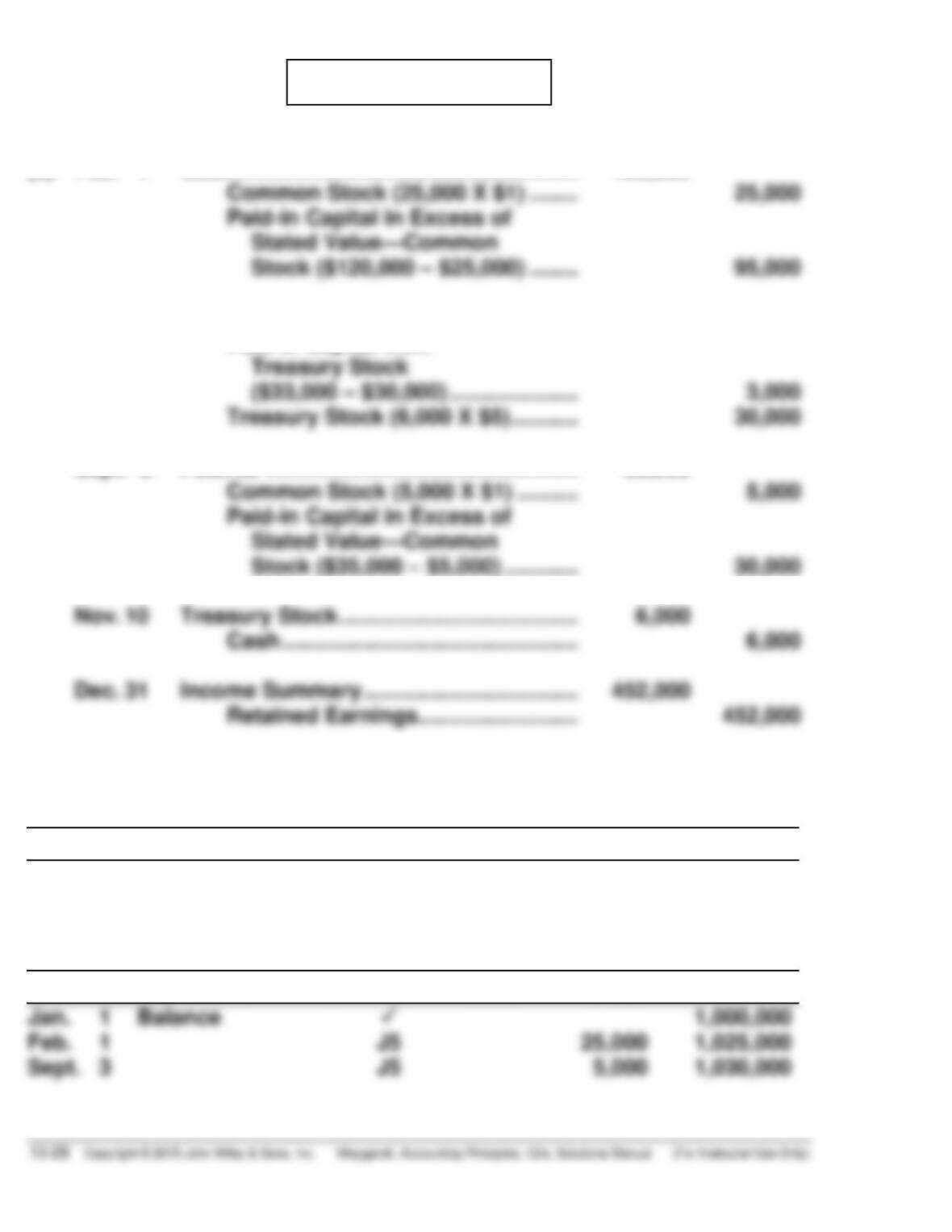

(a) Feb. 1 Cash …………………………..…………………… 120,000

Common Stock (25,000 X $1) …….. 25,000

Paid-in Capital in Excess of

Apr. 14 Cash ……………………………………………….. 33,000

Paid-in Capital from

Treasury Stock

($33,000 – $30,000) ………………… 3,000

Treasury Stock (6,000 X $5) ……….. 30,000

Sept. 3 Patents …………………………..………………. 35,000

Common Stock (5,000 X $1) ………. 5,000

Nov. 10 Treasury Stock ………………………………… 6,000

Cash ………………………………………… 6,000

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

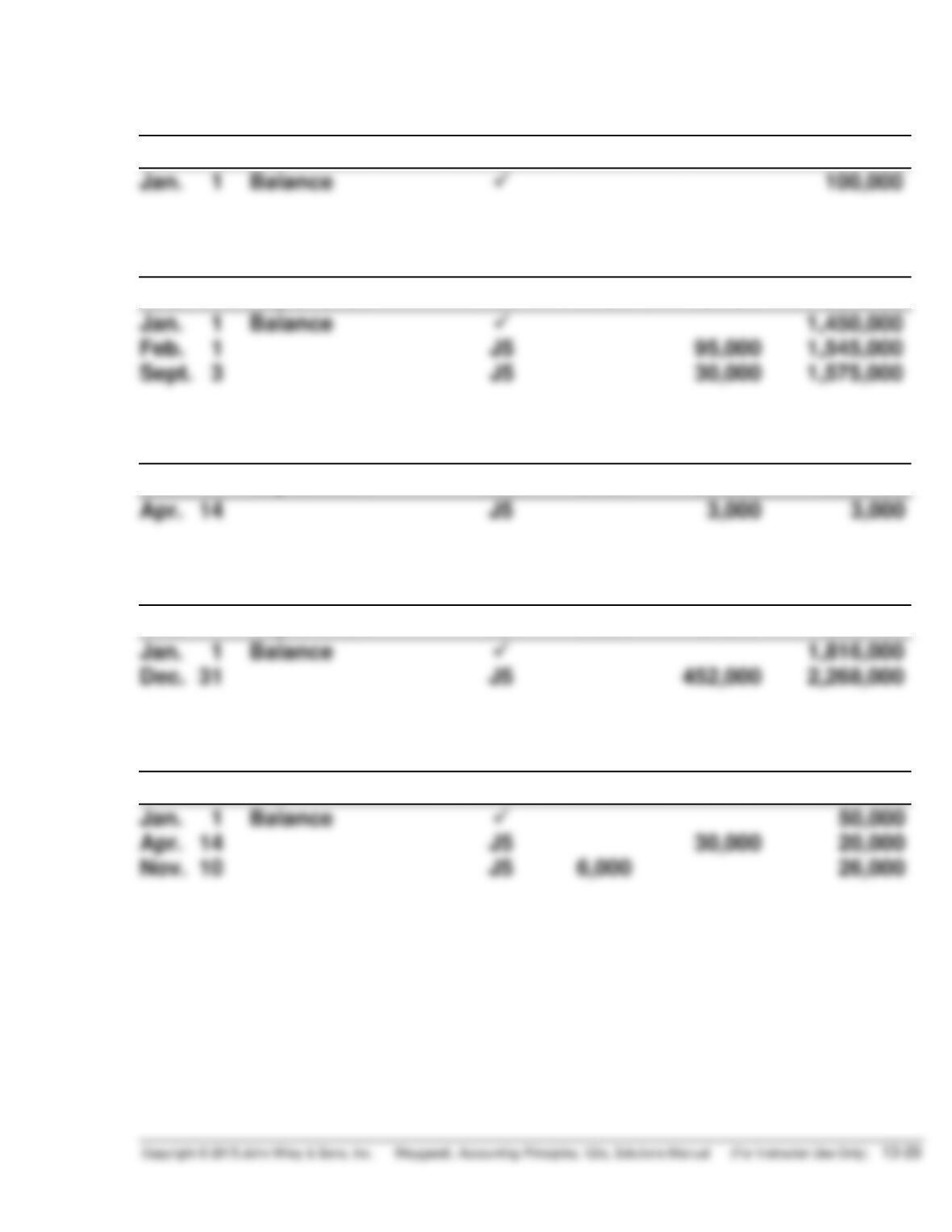

Jan. 1

Balance

400,000

Common Stock

PROBLEM 13-3A (Continued)

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

100,000

Date

Explanation

Ref.

Debit

Credit

Paid-in Capital from Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 14

J5

3,000

3,000

Retained Earnings

Date

Explanation

Debit

Credit

Balance

Jan. 1

Balance

Treasury Stock

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 13-3A (Continued)

(c) CASTLE CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $50

par value,

10,000 shares authorized,

8,000 shares issued and

outstanding ………………………. $ 400,000

Common stock, no par,

Additional paid-in capital

In excess of par—

preferred stock …………………. $ 100,000

In excess of stated value—

common stock ………………….. 1,575,000

Retained earnings …………………………….. 2,268,000

Total paid-in capital and

retained earnings ………… 5,376,000

PROBLEM 13-4A

(a) Feb. 1 Land ………………………………………………. 120,000

Preferred Stock (2,000 X $50) ……. 100,000

Paid-in Capital in Excess of

Par—Preferred Stock

($120,000 – $100,000) ……………. 20,000

July 1 Cash (16,000 X $7) ………………………….. 112,000

Common Stock (16,000 X $5) ……. 80,000

Sept. 1 Patent (400 X $70) …………………………... 28,000

Preferred Stock (400 X $50) ………. 20,000

Paid-in Capital in Excess of

Par—Preferred Stock

(400 X $20) …………………………... 8,000

Dec. 1 Cash (8,000 X $7.50) ……………………….. 60,000

Dec. 31 Income Summary ……………………………. 260,000

Retained Earnings …………………… 260,000

PROBLEM 13-4A (Continued)

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Feb. 1

Balance

J2

100,000

500,000

600,000

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

350,000

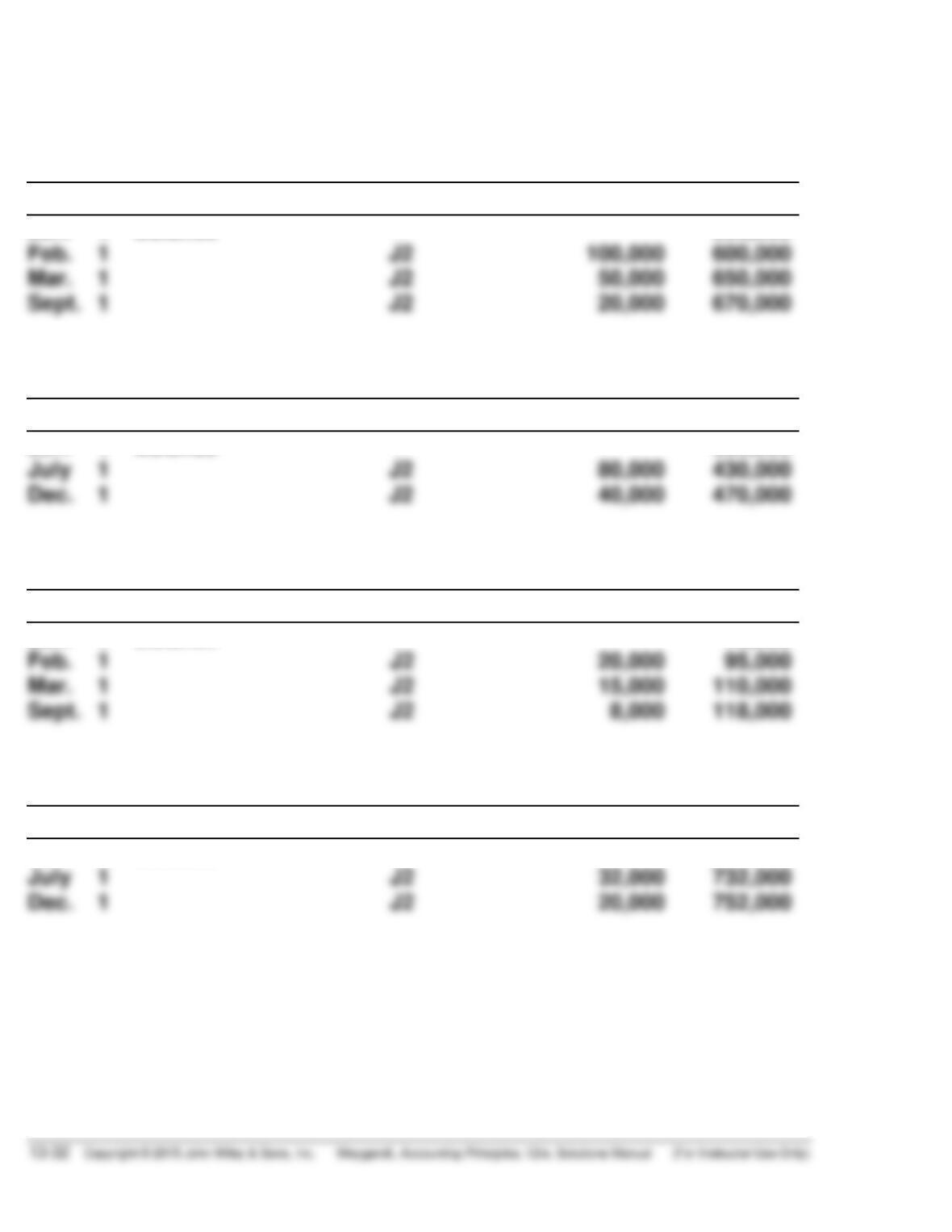

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Feb. 1

Balance

J2

20,000

75,000

95,000

Paid-in Capital in Excess of Par—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

700,000

PROBLEM 13-4A (Continued)

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

300,000

(c) PECK CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

10% Preferred stock,

$50 par value,

20,000 shares authorized,

13,400 shares issued

Additional paid-in capital

In excess of par—

preferred stock ………………………. $118,000

In excess of par—

common stock ……………………….. 752,000

PROBLEM 13-5A

GALINDO CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock,

$50 par,

16,000 shares issued

and outstanding………………… $ 800,000

Total capital stock ………….. 2,800,000

Additional paid-in capital

In excess of par—

preferred stock …………………. $ 679,000

In excess of stated value—

common stock ………………….. 1,600,000

Total paid-in capital ………… 5,089,000

Retained earnings …………………………….. 1,748,000

Total paid-in capital and

retained earnings ………… 6,837,000