CHAPTER 13

Operating Activities

THINKING BEYOND THE QUESTION

How do we account for operating activities?

Estimation methods can have a major effect on a company’s reported rev-

enues and expenses. If appropriate methods are used, the revenues and

QUESTIONS

Q13-1 Both the income statement and the statement of cash flows report the re-

sults of operating activities. The difference is that the income statement

Q13-2 The income statement is organized to highlight certain information that is

useful to financial statement users. By breaking out specific items sepa-

rately, additional information about the workings of the organization are

revealed. For example, if the company has material amounts of both sales

384 Chapter 13

Q13-3 Your friend is partially right—the income statement is full of estimates,

and it does not reveal either the current cash position or the cash flows of

Q13-4 Title to goods transfers to the buyer at the point named in the freight

terms. Therefore, if goods are sold FOB shipping point, the goods become

the property of the buyer when they are loaded onto the truck (or rail car)

Q13-5 There is a large conceptual difference between a reduction of revenue and

an expense. While it is true that the effect on net income would be identi-

cal, there is more to the issue. Revenue can be defined as the reward that

is earned from serving customers. Sales discounts and sales returns are

Q13-6 Gross profit is affected by two types of transactions: sales and the transac-

tions that create inventory cost. For a merchandiser, inventory cost derives

from just one transaction, a purchase. For a manufacturer, it is more com-

Operating Activities 385

Q13-7 Neither receiving nor paying for the raw materials will affect the current–

year income statement. The materials will be expensed as part of cost of

Q13-8 These goods should not be included as part of Hadley’s inventory at De-

cember 31 because the firm does not own the goods. The ownership of

Q13-9 Yes and no. It depends on what is meant by the “amount” of inventory. If

the issue is the quantity of inventory on hand, such as number of cases,

number of tons, etc., the answer is “no.” GAAP require a physical count at

fiscal year-end to confirm the quantity of goods in inventory. On the other

Q13-10 Most corporations attempt to maximize reported earnings and cash flows

from operating activities. Inventory estimation methods affect reported

earnings directly and cash flows indirectly through taxes on corporate

profits. If a company’s unit inventory costs increase over time, LIFO nor-

mally will result in a greater amount of cost of goods sold than FIFO be-

od, it will sell units out of inventory layers that have a lower unit cost than

current costs. The unit cost of these earlier layers may be much lower if

LIFO has been used than if FIFO has been used because they represent

much earlier acquisitions. Therefore, the company may actually record

lower cost of goods sold using LIFO than using FIFO, resulting in higher

Q13-11 This is because of the mechanics of the LIFO and FIFO methods. Under

LIFO, the most recent costs of inventory purchases are charged off to cost

of goods sold. Older costs are reported as ending inventory. When prices

Q13-12 The lower of cost or market rule requires companies to estimate the re-

placement cost of their inventories. If the replacement cost is below cost,

the inventory must be written down to the lower value. The purpose of this

Operating Activities 387

Q13-13 It is difficult to argue that research and development costs don’t provide

any benefit to future accounting periods. If this were true, companies

would be foolish to make such expenditures. Even casual observation of

Q13-14 The existence of a difference between the two amounts indicates that the

company has preferred stock outstanding. Because of the nature of pre-

Q13-15 Earnings per share numbers can be confusing, with both basic and diluted

earnings presented and with computations based on income before and af-

ter items like discontinued segments, extraordinary items, and effects of

388 Chapter 13

EXERCISES

E13-1 Definitions of all terms are listed in the glossary.

E13-2 Hoffman Electric

Income Statement

Year Ending December 31, 2007

Sales revenue $ 260,772

E13-3 Sales are revenues generated from the sale of goods and services during

a fiscal period.

Other income is income generated by other miscellaneous operating activ-

ities.

Research and development expenses are those associated with the crea-

tion and improvement of products and production processes. GAAP

require these costs to be expensed in the period in which they occur.

Provision for depreciation, depletion, and amortization is the expense

associated with the use of plant assets, natural resources, and intan-

Operating Activities 389

Provision for taxes on income is the amount of tax a company would owe

on its pretax income if this amount of income were reported for tax

(Based on the “Other Topics” section at the end of the chapter)

Minority interests is the portion of income of consolidated subsidiar-

ies attributable to minority stockholders of these subsidiaries. Thus,

Earnings per share is the amount of net income available to common

stockholders divided by the average number of common shares out-

standing during the fiscal period. Alcoa reports earnings per share as

basic and diluted. The diluted value represents earnings available to

common shareholders if all convertible securities were exchanged for

common stock.

E13-4 a. In general, San Miguel should not recognize revenue until:

i. It has completed most of the activities necessary to produce and

sell the goods or services,

390 Chapter 13

In other words, revenue cannot be recognized until the company

has performed those activities that earn it the right to receive pay-

b. San Miguel’s service contracts provide for service over a period of

time. Therefore, service revenue should be recognized as time pass-

E13-5 Amount of gross sales $30,000,000

Sales discounts 900,000

Amount billed 29,100,000

Operating Activities 391

E13-6 a.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

Accounts Receivable

18,600,000

Calculation of doubtful accounts expense:

Allowance for doubtful accounts,

beginning of 2008 $ 450,000

Account written off (165,000)

Balance after write-off $ 285,000

E13-7 a. The entire amount should be recognized as a sale in April, when the

machine is delivered to the customer and the earnings process is

completed.

b. The cost of the components should be recognized in April, as part of

Sales Revenue

18,600,000

Cash

18,750,000

Accounts Receivable

Accounts Receivable

392 Chapter 13

E13-8 Year 2007 Year 2008

a. Accounts Receivable:

b. Doubtful Accounts Expense:

2007: $4,000,000 × 0.05 $ 200,000

2008: Proof $ 191,600*

c. Allowance for Doubtful Accounts:

E13-9 a. Revenue = $700,000 ($2,000,000 × 35%)

E13-10 a. Revenue = $16,000,000 ($40 million × 40%)

Operating Activities 393

E13-11

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

2/27

Merchandise

400

E13-12 a.

ASSETS

=

LIABILITIES

+

OWNERS’ EQUITY

Date

Accounts

Cash

Other

Assets

Contributed

Capital

Retained

Earnings

1

Merchandise Inventory

600,000

Accounts Payable

600,000

2

Accounts Receivable

855,000

Sales

3

Merchandise Inventory

Cost of Goods Sold

–491,000

4

Merchandise Inventory

–35,000

Accounts Payable

5

Cash

Accounts Receivable

6

Cash

–565,000

Accounts Payable

–565,000

7

Accounts Receivable

–22,000

Sales Discounts

–22,000

8

–16,000

–16,000

9

Accounts Receivable

–12,000

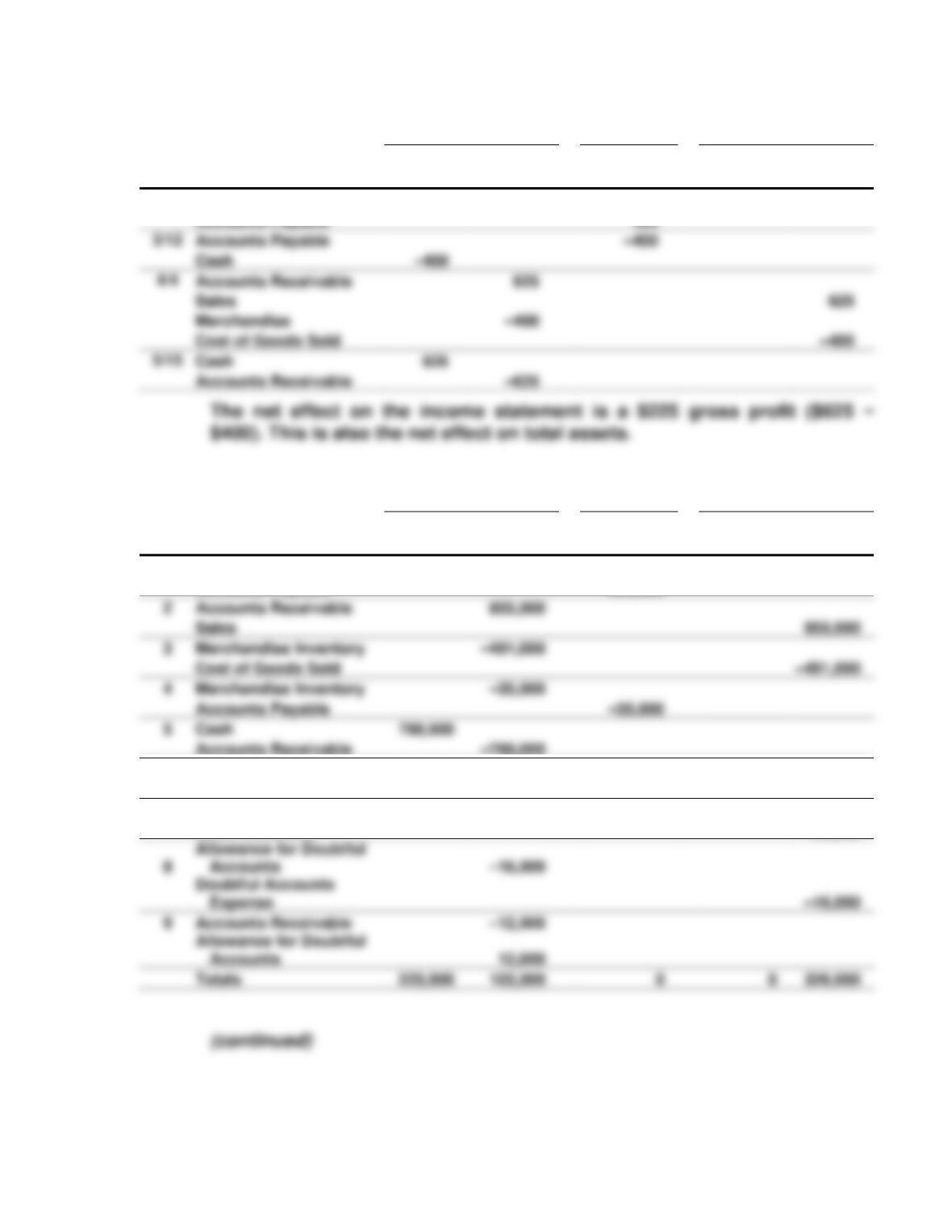

Totals

103,000

Accounts Payable

Accounts Payable

Cash

Accounts Receivable

625

Sales

Merchandise

Cost of Goods Sold

Cash

Accounts Receivable

394 Chapter 13

b. Net Income

Gross sales revenue $ 855,000

Sales discounts (22,000)

E13-13 The income statement recognition of the events would be in March, when

the sale took place; the income statement effect in the other months is ze-

ro. Both the purchase and the sale should be recorded net of the discount.

Sale—invoice price $ 75,000

E13-14 a. Always false. Sales discounts are not an expense. They do not repre-

sent the use or consumption of resources in generating revenue. In-

stead, sales discounts are a reduction in the amount of revenue that

has been earned. They are similar to other price reductions. In es-

sence, it is revenue that the company never had.

Operating Activities 395

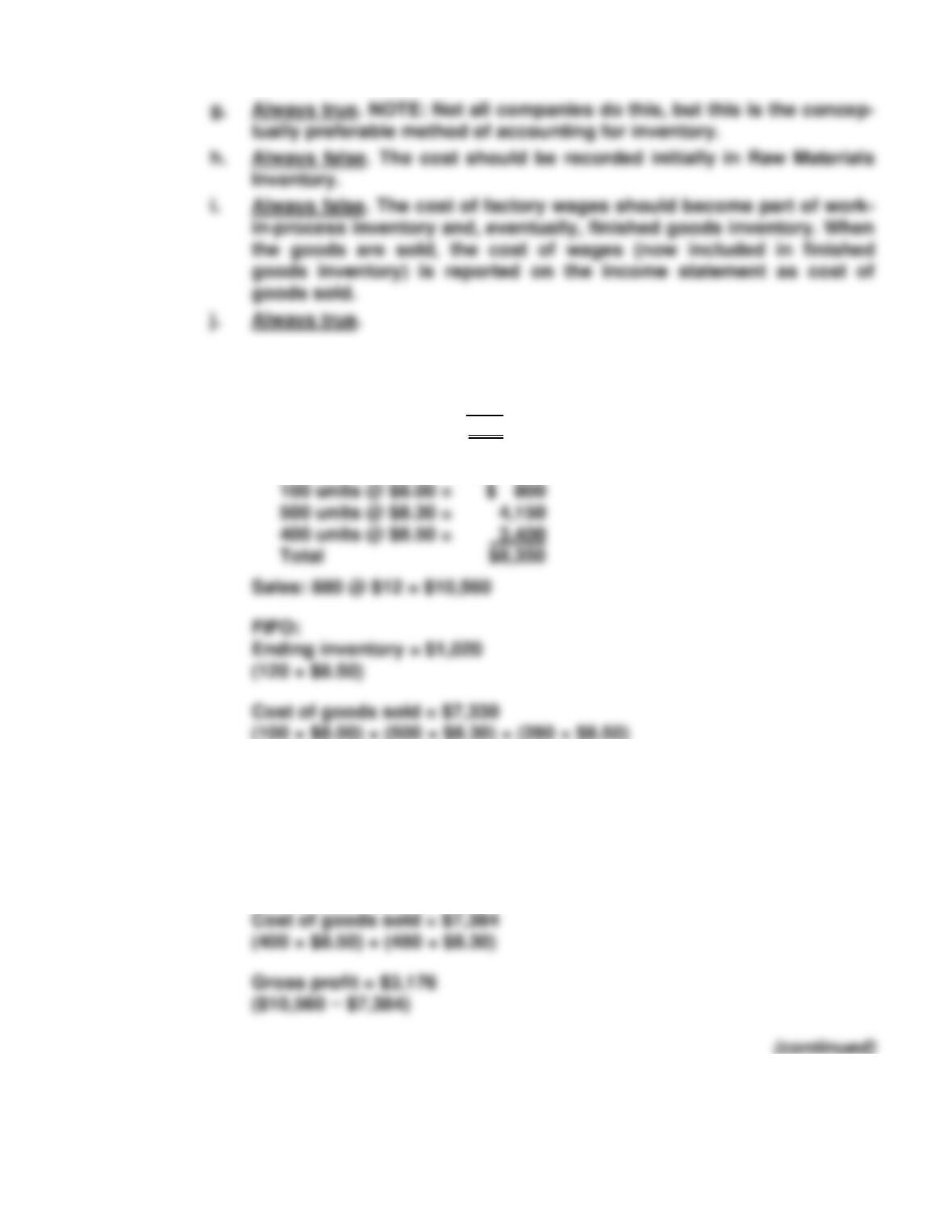

E13-15 a. Beginning inventory 100 units

Purchased (500 + 400) 900

Sold (880)

Ending inventory 120 units

Cost of goods available for sale:

Gross profit: $3,230

($10,560 − $7,330)

LIFO:

Ending inventory = $966

(100 × $8.00) + (20 × $8.30)

396 Chapter 13

b. The highest gross profit results from FIFO because the oldest, lowest

E13-16

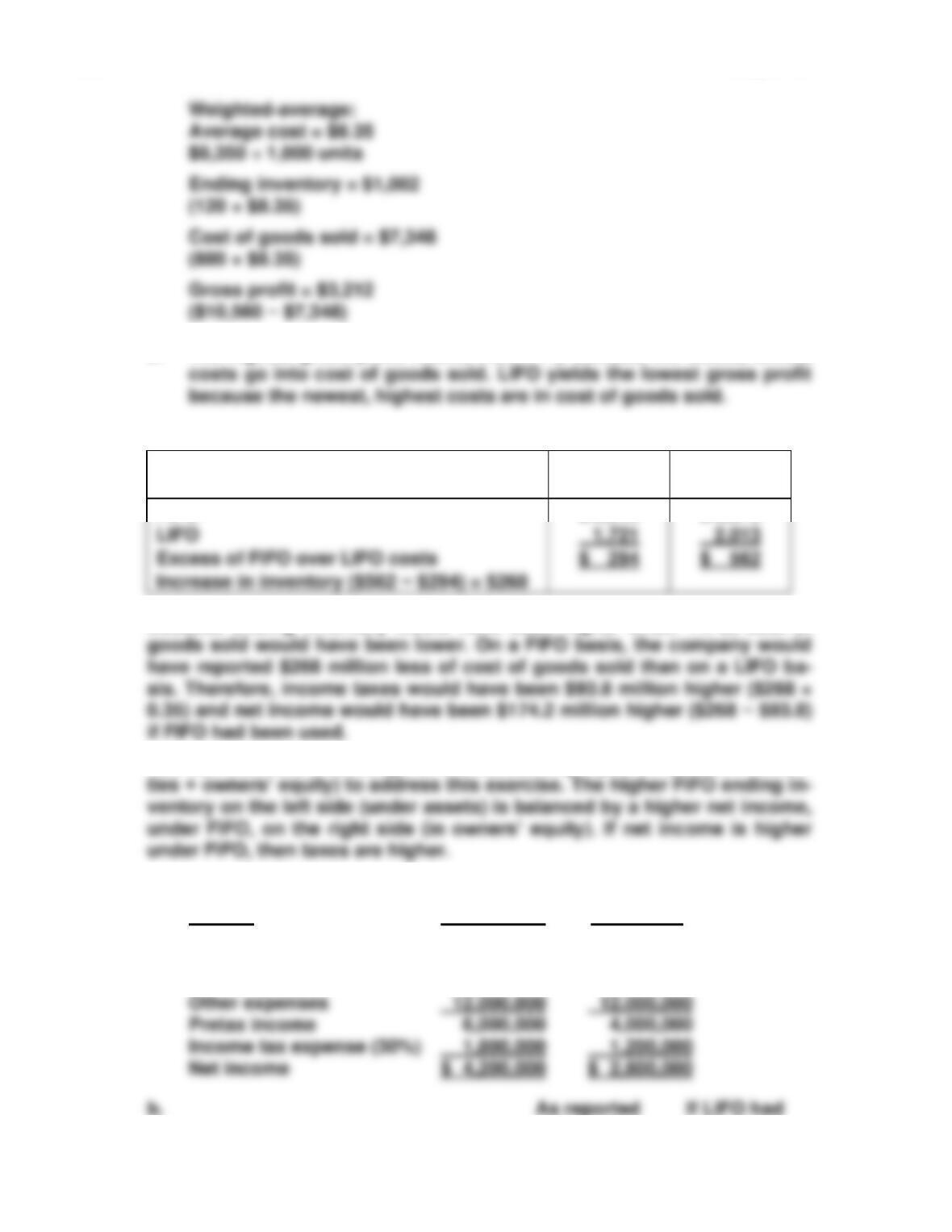

(In millions)

Beginning

Inventory

Ending

Inventory

FIFO

$ 2,015

$ 2,575

Because ending inventory would have been higher under FIFO, cost of

You can also use knowledge of the accounting equation (assets = liabili-

E13-17 a. As reported If LIFO had

Income via FIFO been used

Sales revenue $ 60,000,000 $ 60,000,000

Less:

Cost of goods sold 42,000,000 44,000,000

Operating Activities 397

Cash flow via FIFO been used

c. No. Cost of goods sold would have been $2 million higher using LIFO

rather than FIFO. As a result, the company’s net income would have

E13-18 a. Goods were sold to customers on credit.

b. Company records cost of goods sold and decrease of inventory.

c. Cash was collected from customers’ credit purchases.

d. Inventory was purchased on credit.

e. Some of the inventory purchased on credit was returned to the ven-

398 Chapter 13

c. Total cost of goods available for sale = 1,200 + 700 + 1,500 = $3,400

E13-20 a. Total units sold = 8,000 + 2,000 + 5,000 = 15,000

c. Total cost of goods available for sale = 90,000 + 36,000 + 140,000 =

$266,000

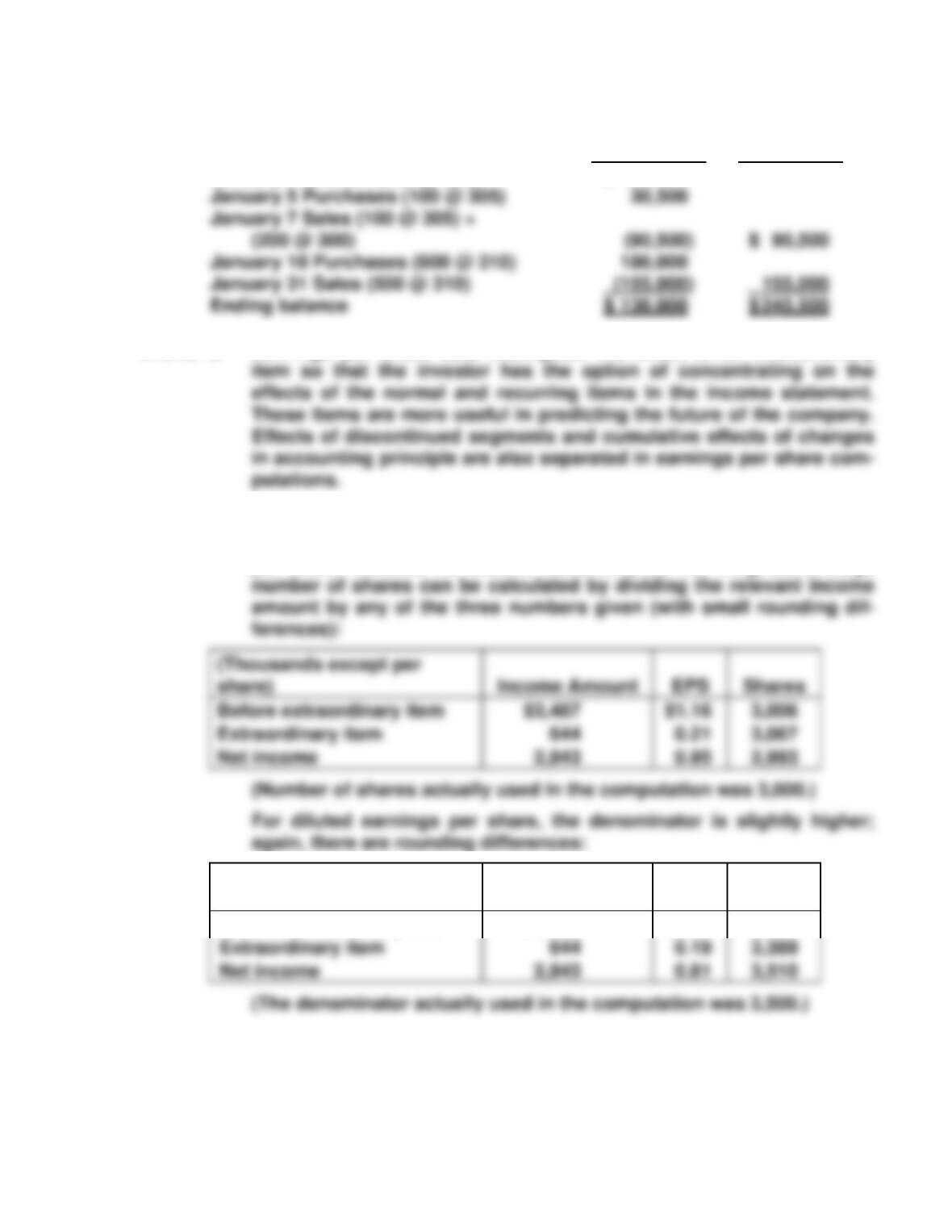

E13-21 Merchandise Cost of

Inventory Goods Sold

January 1 balance (550 @ 300) $ 165,000

Operating Activities 399

E13-22

Merchandise Cost of

Inventory Goods Sold

January 1 balance (550 @ 300) $ 165,000

E13-23 a. Earnings per share data distinguish the effect of an extraordinary

b. Basic and diluted earnings per share are the categories specified by

Statement of Financial Accounting Standards No. 128. Basic earnings

per share includes no dilutive securities, so the weighted-average

Income Amount

EPS

Shares

$3,487

$1.16

3,006

(Thousands except per

share)

Income Amount

EPS

Shares

Before extraordinary item

$3,487

$1.00

3,487

c. The extra 500 would come from some kind of security that could turn

into common stock, such as convertible preferred stock, convertible

bonds, or employee stock options.

400 Chapter 13

E13-24 A complete income statement is shown below with each of the require-

ments keyed by letter.

Net operating revenues $ 956,000

Cost of goods sold (312,000)

Selling and administrative expenses (245,000)

E13-25 a. Income from continuing operations, before taxes $ 250,000

Income tax expense (provision for taxes) (75,000)

Income before special items 175,000

Discontinued operations:

Operating Activities 401

E13-26 a. Inventory is expensed as cost of goods sold when it is sold; so this

would be expensed in 2008 rather than 2007.

b. Estimated warranty costs should be expensed in the year of sale, to

PROBLEMS

P13-1 Leafy Green Corp.

Income Statement

For the Month of January 2007

Sales $16,500

Expenses:

Salad ingredients $8,500

P13-2 In general, revenues are recognized in the income statement when the fol-

lowing four criteria have been met:

1. The selling company has completed most of the activities necessary to

produce and sell the goods or services.

402 Chapter 13

b. Each month 1/24 of the subscription price would be recognized.

P13-3 Revenue recognition involves decisions about when revenue is recorded

for financial reporting purposes. This is an important decision because it

affects the amount of revenue reported in specific fiscal years. Revenue

should be recognized when it has been earned. The earnings process typ-

P13-4 A. Accounts receivable, 1/1/2008

($16.5 million + $1.8 million) $ 18,300,000

Sales on credit 56,500,000

Collected from customers (57,900,000)

B. Allowance for doubtful accounts, beginning of 2008 $ 1,800,000

Accounts written off as uncollectible (1,980,000)