Chapter 12 – Financial Statement Analysis

12-1

Chapter 12

Financial Statement Analysis

INSTRUCTOR’S MANUAL

Authors’ Perspectives

PART A: Comparison of Financial Accounting Information

LO12-1 Perform vertical analysis.

Vertical and Horizontal Analysis – We can first remind students that ratios are used to make

comparisons every day. Batting averages provide feedback in baseball about how well a player is

hitting. Basketball and football fans use points per game to compare teams’ offensive and

defensive performance. The cost per ounce of meat at the grocery store matters to shoppers. In

PART B: Using Ratios to Assess Risk and Profitability

LO12-3 Use ratios to analyze a company’s risk.

LO12-4 Use ratios to analyze a company’s profitability.

Risk Ratios – Part B begins with a detailed assessment of risk for Under Armour, comparing the

company’s risk ratios to the sports apparel industry leader, Nike. The coverage includes eight

risk ratios, distinguished by liquidity and solvency.

Chapter 12 – Financial Statement Analysis

12-2

causes investors to bid the price of a stock upward. At the same time, as risk increases, stock

prices generally decline. Most investors are risk averse. This risk aversion decreases the demand

for riskier stocks, lower the price. So, risk and profitability are key factors in the investment

decision, and accounting ratios provide important insights into those factors.

Common Mistake: For computing risk and profitability ratios, students get confused as to

whether to use (1) the average of ending and beginning amounts or (2) the ending amounts

an equivalent time basis.

Flexibility in Coverage – Some instructors prefer to cover ratios with each chapter as they move

through the topics in the course. This chapter-by-chapter approach allows instructors to reinforce

immediately how the chapter’s measurement/communication topics lead to decision-making.

Other instructors prefer to cover ratios in a final summary chapter, such as Chapter 12’s

PART C: Earnings Persistence and Earnings Quality

LO12-5 Distinguish persistent earnings from one-time items.

LO12-6 Distinguish between conservative and aggressive accounting practices.

Earnings Persistence – Part C begins with the concept of earnings persistence. Discontinued

Conservative versus Aggressive – The final section on earnings quality reinforces the idea that

Chapter 12 – Financial Statement Analysis

12-3

assumptions and estimates are inherent in financial accounting. As a result, management can

affect amounts reported in the financial statements by applying conservative or aggressive

accounting practices. Major topics from Chapters 5, 6, 7, and 8 are used as examples of both

• Illustration 12-28 shows the impact of conservative versus aggressive accounting choices

in the income statement.

• Illustration 12-29 shows the impact of conservative versus aggressive accounting choices

in the balance sheet.

One potentially enlightening aspect of this topic is that conservative versus aggressive

Self-Study Materials

■ Let’s Review—Horizontal analysis (p. 604).

■ Let’s Review—Risk ratios (p. 611).

Chapter 12 – Financial Statement Analysis

12-4

Key Points by Learning Objective

Throughout the chapter, Key Points provide quick synopses of the critical pieces of information

LO12-1 Perform vertical analysis.

For vertical analysis, we express each item as a percentage of the same base amount, such as a

percentage of sales in the income statement or as a percentage of total assets in the balance sheet.

LO12-2 Perform horizontal analysis.

LO12-3 Use ratios to analyze a company’s risk.

We divide risk ratios into liquidity ratios and solvency ratios. Liquidity ratios focus on the

company’s ability to pay current liabilities, whereas solvency ratios include long-term liabilities.

LO12-4 Use ratios to analyze a company’s profitability.

LO12-5 Distinguish persistent earnings from one-time items.

LO12-6 Distinguish between conservative and aggressive accounting practices.

Changes in accounting estimates and practices alter the appearance of amounts reported in

Chapter 12 – Financial Statement Analysis

12-5

A

As

ss

si

ig

gn

nm

me

en

nt

t

C

Ch

ha

ar

rt

ts

s

Questions

Learning

Objective(s)

Topic

Time

(Min.)

1

LO12-1, 12-2

financial statement analysis

LO12-1, 12-2

Explain the difference between vertical and

horizontal analysis

5

3

LO12-1

Describe the base amounts commonly used in

vertical analysis

5

size of its common stock and retained earnings

balances

amount and percentage change in horizontal

analysis

Identify types of comparisons commonly used in

5

6

LO12-3

Explain why some ratios use average rather than

ending balance sheet amounts

5

7

LO12-3

Describe the difference between liquidity and

solvency

5

8

LO12-3

Relate risk ratios with financial questions

5

9

LO12-3

Determine whether each of the following changes in

risk ratios is good news or bad news about a

company

5

10

LO12-3

Describe the effect of a transaction on the current

ratio

5

LO12-4

Relate profitability ratios with financial questions

5

profitability ratios is good news or bad news about a

company

LO12-4

Explain why the return on assets and the return on

equity differ

5

LO12-5

Explain how earnings persistence relate to the

reporting of discontinued operations

5

LO12-5

Examine a trend in earnings per share before and

after discontinued operations

5

LO12-6

Explain the difference between conservative and

aggressive accounting practices

5

LO12-6

Explain why an accounting practice is conservative

5

LO12-6

Explain why an accounting practice is aggressive

5

LO12-6

Examine year-end adjustments for a common trend

5

20

LO12-6

Provide an example of a change in accounting

practice that has no effect on cash flows

5

Chapter 12 – Financial Statement Analysis

12-6

Brief

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

BE12-1

LO12-1

Prepare vertical analysis

15

BE12-2

LO12-2

Prepare horizontal analysis

15

BE12-3

LO12-1

Understand vertical analysis

10

BE12-4

LO12-2

Understand horizontal analysis

5

BE12-5

LO12-2

Understand percentage change

5

BE12-6

LO12-3

Calculate receivables turnover

5

BE12-7

LO12-3

Calculate inventory turnover

5

BE12-8

LO12-3

Understand inventory turnover

5

BE12-9

LO12-3

Understand the current ratio

10

LO12-4

Calculate profitability ratios

15

LO12-4

Calculate profitability ratios

10

LO12-5

10

LO12-5

Classify income statement items

10

accounting practices

accounting practices

Exercises

Learning

Objective(s)

Topic

Time

(Min.)

E12-1

LO12-1, 12-2,

12-3, 12-4,

12-5, 12-6

Match terms with their definitions

20

E12-2

LO12-1

Prepare vertical analysis

15

E12-3

LO12-2

Prepare horizontal analysis

15

E12-4

Prepare vertical and horizontal analyses

30

E12-5

LO12-3

Evaluate risk ratios

30

E12-6

LO12-4

Evaluate profitability ratios

30

E12-7

LO12-3

Calculate risk ratios

30

E12-8

LO12-4

Calculate profitability ratios

30

E12-9

LO12-4

Calculate profitability ratios

30

LO12-4

Calculate profitability ratios

20

LO12-5

Classify income statement items

15

LO12-5

20

LO12-5

15

accounting practices

accounting practices

Chapter 12 – Financial Statement Analysis

12-7

Problems

Learning

Objective(s)

Topic

Time

(Min.)

P12-1A

LO12-1

Perform vertical analysis

20

P12-2A

LO12-2

Perform horizontal analysis

20

P12-3A

LO12-1, 12-2

Perform vertical and horizontal analyses

30

P12-4A

LO12-3

Calculate risk ratios

30

P12-5A

LO12-4

Calculate profitability ratios

20

P12-6A

LO12-3, 12-4

Use ratios to analyze risk and profitability

45

LO12-1

Perform vertical analysis

20

P12-2B

LO12-2

Perform horizontal analysis

20

P12-3B

LO12-1, 12-2

Perform vertical and horizontal analyses

30

P12-5B

LO12-4

Calculate profitability ratios

20

P12-6B

LO12-3, 12-4

Use ratios to analyze risk and profitability

45

Additional

Perspectives

Topic

Time

(Min.)

AP12-1

Continuing Problem: Great Adventures

45

AP12-2

Financial Analysis: American Eagle Outfitters, Inc.

45

AP12-3

Financial Analysis: The Buckle, Inc.

45

Buckle, Inc.

AP12-5

Ethics

20

AP12-6

Internet Research

20

AP12-7

Written Communication

20

AP12-8

Earnings Management

20

Chapter 12 – Financial Statement Analysis

12-8

Alternate Let’s Review

Problem #1

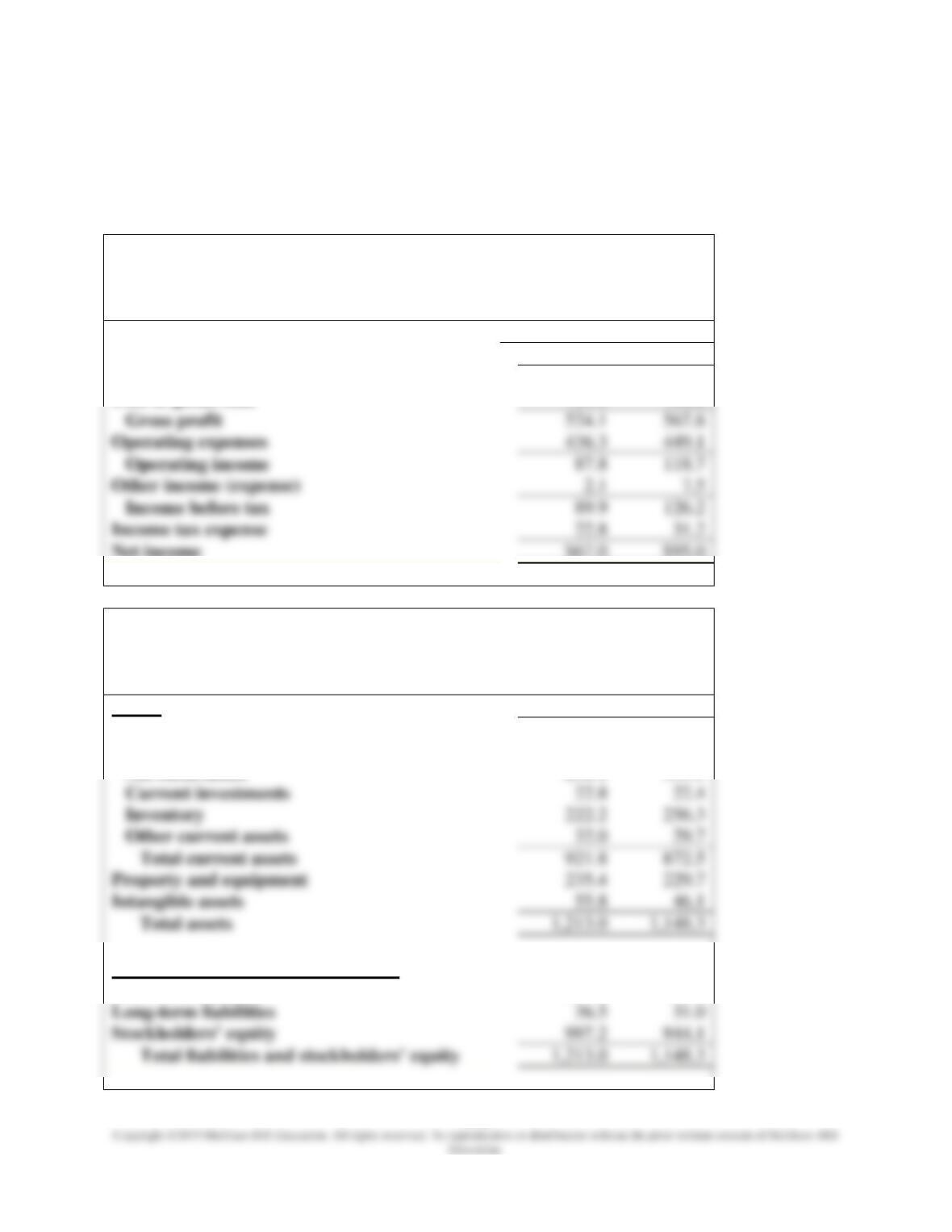

The income statements and balance sheets for Incredible Sports are as follows:

Incredible Sports

Income Statements

For the Years Ended December 31

(in millions)

2021

2020

Sales revenue

$1,244.0

$1,317.8

Cost of goods sold

719.9

750.0

Gross profit

524.1

567.8

Operating expenses

436.3

449.1

Operating income

118.7

Other income (expense)

Income before tax

126.2

Income tax expense

Net income

$67.0

$95.0

Incredible Sports

Balance Sheets

December 31

(in millions)

Assets

2021

2020

Current assets:

Cash

$386.7

$230.6

Net receivables

258.1

333.5

Current investments

Inventory

222.2

256.3

Other current assets

Total current assets

921.8

872.5

Property and equipment

235.4

229.7

Total assets

Liabilities and Stockholders’ Equity

Current liabilities

179.3

173.2

Long-term liabilities

Stockholders’ equity

997.2

944.1

Chapter 12 – Financial Statement Analysis

12-9

Required:

Calculate the following risk ratios for the year ended December 31, 2021.

Solution:

Risk Ratios

Calculations

Liquidity

Receivables turnover ratio

$1,244.0

($258.1 + $333.5) / 2

= 4.2 times

Average collection period

= 86.9 days

Inventory turnover ratio

($222.2 + $256.3) / 2

= 3.0 times

Average days in inventory

= 121.7 days

Current ratio

$179.3

= 5.1 to 1

Acid-test ratio

$179.3

= 3.7 to 1

Solvency

Debt to equity ratio

$179.3 + $36.5

$997.2

= 21.6%

Chapter 12 – Financial Statement Analysis

12-10

Problem #2

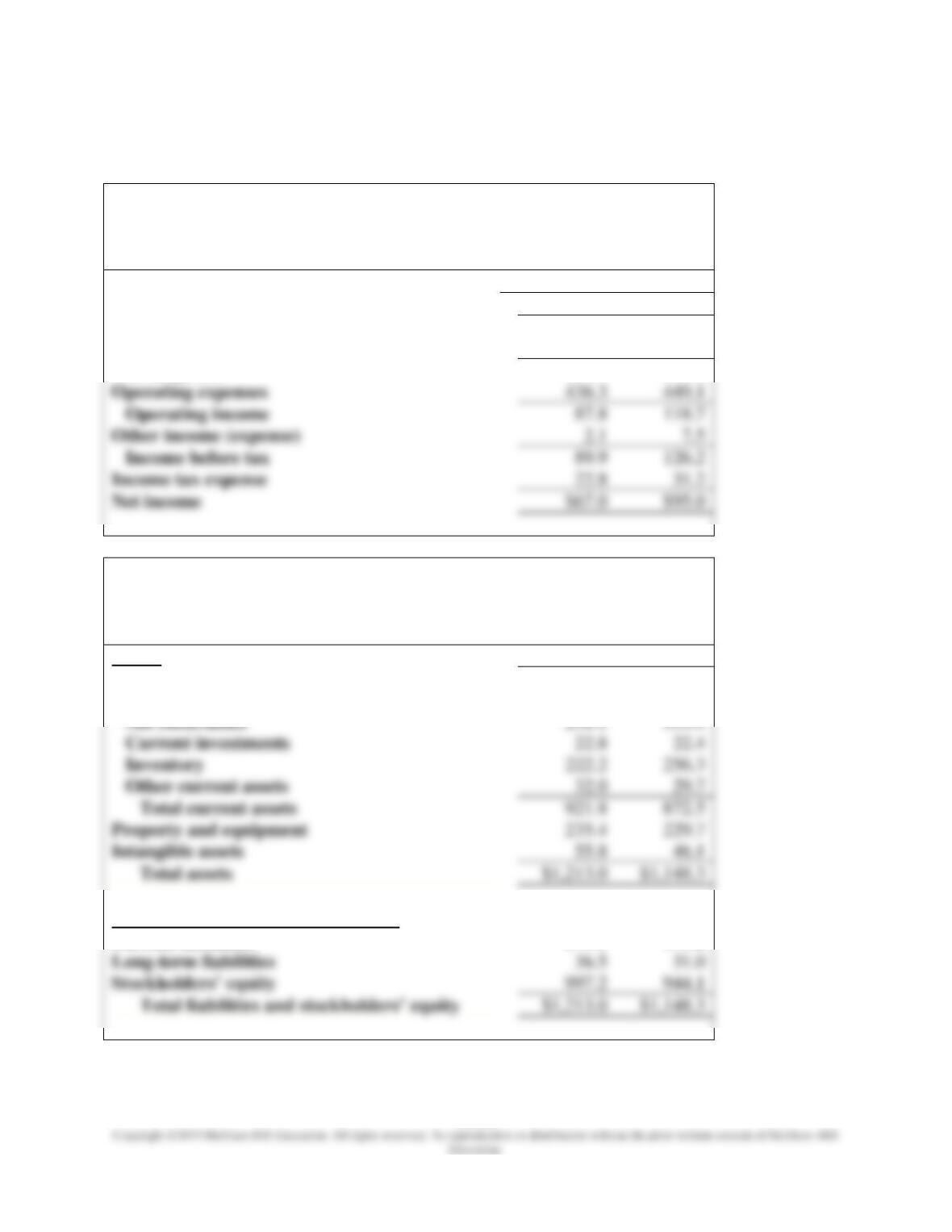

The income statements and balance sheets for Incredible Sports are as follows:

Incredible Sports

Income Statements

For the Years Ended December 31

(in millions)

2021

2020

Sales revenue

$1,244.0

$1,317.8

Cost of goods sold

719.9

750.0

Gross profit

524.1

567.8

Operating expenses

436.3

449.1

Operating income

118.7

Other income (expense)

Income before tax

126.2

Income tax expense

Net income

$67.0

$95.0

Incredible Sports

Balance Sheets

December 31

(in millions)

Assets

2021

2020

Current assets:

Cash

$386.7

$230.6

Net receivables

258.1

333.5

Current investments

Inventory

222.2

256.3

Other current assets

Total current assets

921.8

872.5

Property and equipment

235.4

229.7

Intangible assets

Total assets

$1,213.0

$1,148.3

Liabilities and Stockholders’ Equity

Current liabilities

179.3

173.2

Long-term liabilities

Stockholders’ equity

997.2

944.1

$1,213.0

$1,148.3

In addition, the company reported earnings per share of $2.02 for the year ended December 31,

2021, and the closing stock price on December 31, 2021, was $39.04.

Chapter 12 – Financial Statement Analysis

Required:

Solution:

Profitability Ratios

Calculations

Gross profit ratio

$524.1

$1,244.0

= 42.1%

Return on assets

$67.0

($1,213.0 +$1,148.3) / 2

= 5.7%

Profit margin

$1,244.0

= 5.4%

Asset turnover

= 1.1 times

Return on equity

= 6.9%

Price-earnings ratio

$39.04

= 19.3

Chapter 12 – Financial Statement Analysis

12-12

Problem #3

Required:

Classify each of the following accounting practices as conservative or aggressive.

1. Decrease the allowance for uncollectible accounts.

2. Decrease the useful life for calculating depreciation.

3. Reduce the amount of a contingent liability reported for litigation.

4. Record a larger expense for warranties.

5. When costs are going up, change from LIFO to FIFO.

Solution:

Chapter 12 – Financial Statement Analysis

12-13

Common Mistakes

Common Mistakes made by students are highlighted in each of the chapters. With greater

awareness of the potential pitfalls, student can avoid making the same mistakes and gain a deeper

understanding of the chapter material.

Common Mistake

In comparing an income statement account with a balance sheet account, some students

Chapter 12 – Financial Statement Analysis

12-14

Decision Points and Decision Maker’s Perspective

Decision Points and Decision Maker’s Perspectives are provided throughout each chapter to give

insight into how measurement and communication of financial accounting information help

decision makers.

Decision Points

Question

Accounting Information

Analysis

Question

Accounting Information

Analysis

How do we compare

Common-size income

A vertical analysis using common-

Chapter 12 – Financial Statement Analysis

12-15

Decision Maker’s Perspective

How Warren Buffett Interprets Financial Statements

Warren Buffett is one of the world’s wealthiest individuals, with investments in the billions. As

founder and CEO of Berkshire Hathaway, an investment company located in Omaha,

Nebraska, he is also highly regarded as one of the world’s top investment advisors. So, what’s

the secret to his success? Warren Buffett is best known for his attention to details, carefully

examining each line in the financial statements.

Does Location in the Income Statement Matter?

As manager of a company, would you prefer to show an expense as part of continuing operations

or as a part of discontinued operations? Your first response might be that it really doesn’t matter,

since the choice affects only the location in the income statement and has no effect on the final

Look Out for Earnings Management at Year-End

Let’s assume you’re an auditor and all four of the final changes to the accounting records near

year-end increase income. Wouldn’t you be just a little concerned? It may be that all four

Chapter 12 – Financial Statement Analysis

12-16

Ethical Dilemma

Michael Hechtner was recently hired as an assistant controller for Athletic Persuasions, a

recognized leader in the promotion of athletic events. However, the past year has been a difficult

one for the company’s operations. In order to help with slowing sales, the company has extended

credit to more customers and accepted payment over longer time periods, resulting in a

significant increase in accounts receivable. Similarly, with slowing sales, its inventory of

do in this situation? Is it acceptable for Michael just to keep quiet?

Key Issues

• When does putting a positive spin on a situation become unethical?

• What action, if any, should Michael take in this situation?

Option 1: Keep quiet and give full support to his boss, J.P. Sloan

• This is the easiest alternative.