368 Chapter 12

Trendlines have been added to the graph to illustrate the steeper slope

P12-5 A.

Dell (In millions)

80% of 120% of

Current Sales Current Sales Current Sales

Net revenue $ 33,155.2 $ 41,444.0 $ 49,732.8

B. Hilfiger (In millions)

80% of 120% of

Current Sales Current Sales Current Sales

Net revenue $1,500.8 $ 1,876.0 $2,251.2

C. At 80% of current sales, Hilfiger’s operating income decreases 54%

P12-6 A. Expected cost of goods sold for 2007 = $508

Analysis of Investing Activities 369

B. 2007

(In millions) Expected

C. Because a portion of cost of goods sold is fixed, these costs do not

increase with sales. Therefore, cost of goods sold is lower if the pro-

lower net income.

P12-7 A. Jekyll Hyde

Sales $33,600 $90,000

Operating expenses* 23,000 62,000

Operating income 10,600 28,000

B. Jekyll Hyde

2007: $5,040 ÷ $30,000 = 16.8%

370 Chapter 12

C. Jekyll’s return on assets increased from 16.8% to 22.9% as a result

of the 20% increase in sales. Hyde’s return on assets more than

P12-8 Both companies had positive, steadily increasing cash flows from operat-

ing activities during the three-year period. Both also continued to invest

during this period, although the two firms had different patterns of in-

P12-9 Ratios that could be calculated include the following:

Widgets Inc.

Gizmos Inc.

2007

2006

2007

2006

Accumulated depreciation ÷ plant

and equipment

25.0%

26.4%

51.2%

43.2%

Depreciation rate (depreciation ÷

plant and equipment)

13.3%

13.2%

12.1%

12.3%

44.5%

43.5%

58.5%

Analysis of Investing Activities 371

P12-10 The two companies have had different patterns of cash flows over the

three years presented.

Operating activities: Sara Lee increased its cash flow from operating ac-

tivities during each of the three years reported, while Campbell Soup

P12-11 Ratios that can be computed include the following:

PepsiCo

Coca-Cola

Plant assets ÷ total assets

Intangible assets ÷ total assets

0.291

0.194

0.194

0.122

The two company’s financial results are strikingly similar. For example,

ROA and ROE approximates 15% and 30%, respectively, for the two com-

372 Chapter 12

PepsiCo’s profit margin of 14% is lower than Coca-Cola’s profit margin of

each dollar of book value, the market is willing to pay about $6.50.

P12-12 A. Faucett

2007 2006

Asset turnover 40.7 ÷ 33.8 = 1.20 30.5 ÷ 26.8 = 1.138

Danson

2007 2006

Asset turnover 95.5 ÷ 84.4 = 1.132 71.6 ÷ 71.0 = 1.008

B. Faucett’s return on assets increased from 2006 to 2007, while Dan-

son’s return on assets decreased. Faucett’s return on assets is high-

P12-13

2004

2003

2002

Profit margin (net income ÷ sales)

Asset turnover (sales ÷ total assets)

0.14

1.05

0.13

1.06

0.12

1.07

Analysis of Investing Activities 373

PepsiCo’s profit margins increased annually from 2002 to 2004; however,

P12-14 A.

Griffith Inc.

Johnson Inc.

2008

2007

2008

2007

Asset turnover

113.4%

113.1%

113.0%

112.6%

B. Asset turnover is similar for the two companies. However, a decline

C. The market to book figures suggest that the stock market perceives

P12-15 Pro forma income statements and calculations of return on total assets

follow:

A. Current Expansion Add Add

Operations of Current Dragons Games

Sales $ 9,860 $ 11,832 $ 13,160 $ 12,760

374 Chapter 12

C. Although net income is lower under the addition of the game line

P12-16 Possible ratios to calculate include the following:

2007

2006

2005

2004

2003

Until 2006, the company’s return on assets consistently improved each

year. In 2006, the return on assets decreased to its lowest level since

Two points are important in this analysis. One is that actual return often

differs from expected return. Therefore, the company’s management was

P12-17 A.

Hilfiger

Nike

2004

2003

2004

2003

Asset turnover:

0.91

0.93

1.55

1.57

Analysis of Investing Activities 375

B. As measured by asset turnover, Nike (averaging about 1.6) was more

C.

Hilfiger

Nike

2004

2004

Change in investing cash flows

0.17

3.38

P12-18 A. From the information available, Sporting Life Inc. has improved dra-

matically its ability to meet its interest payments and repayments of

2007

2006

2005

Return on total assets

(NI ÷ total assets)

4.9%

3.9%

1.9%

376 Chapter 12

Other measures that could be of interest are shown below.

2007

2006

2005

Net income ÷ interest ex-

pense

2.2 times

1.3 times

0.5 times

Debt as a percentage of assets has declined significantly, reducing

the risk of investing in its notes. The ability to cover interest pay-

B. Additional information to be examined before making a final decision

could include the following:

• Schedules of debt due in each of the next five years, available in

P12–19 Cobb seems to be more of a credit risk than Speaker. First, Cobb had to

write down some assets due to decline in value ($18 million) and appar-

Analysis of Investing Activities 377

does Speaker.

P12-20 The Book Wermz

Income Statement

For the Year Ended December 31, 2008

Current High Variable High Fixed

Sales $ 6,230,000 $ 7,000,000 $ 7,500,000

Cost of goods sold 3,426,500 4,200,000 3,750,000

P12-21

1

2

3

4

5

6

7

8

9

10

CASES

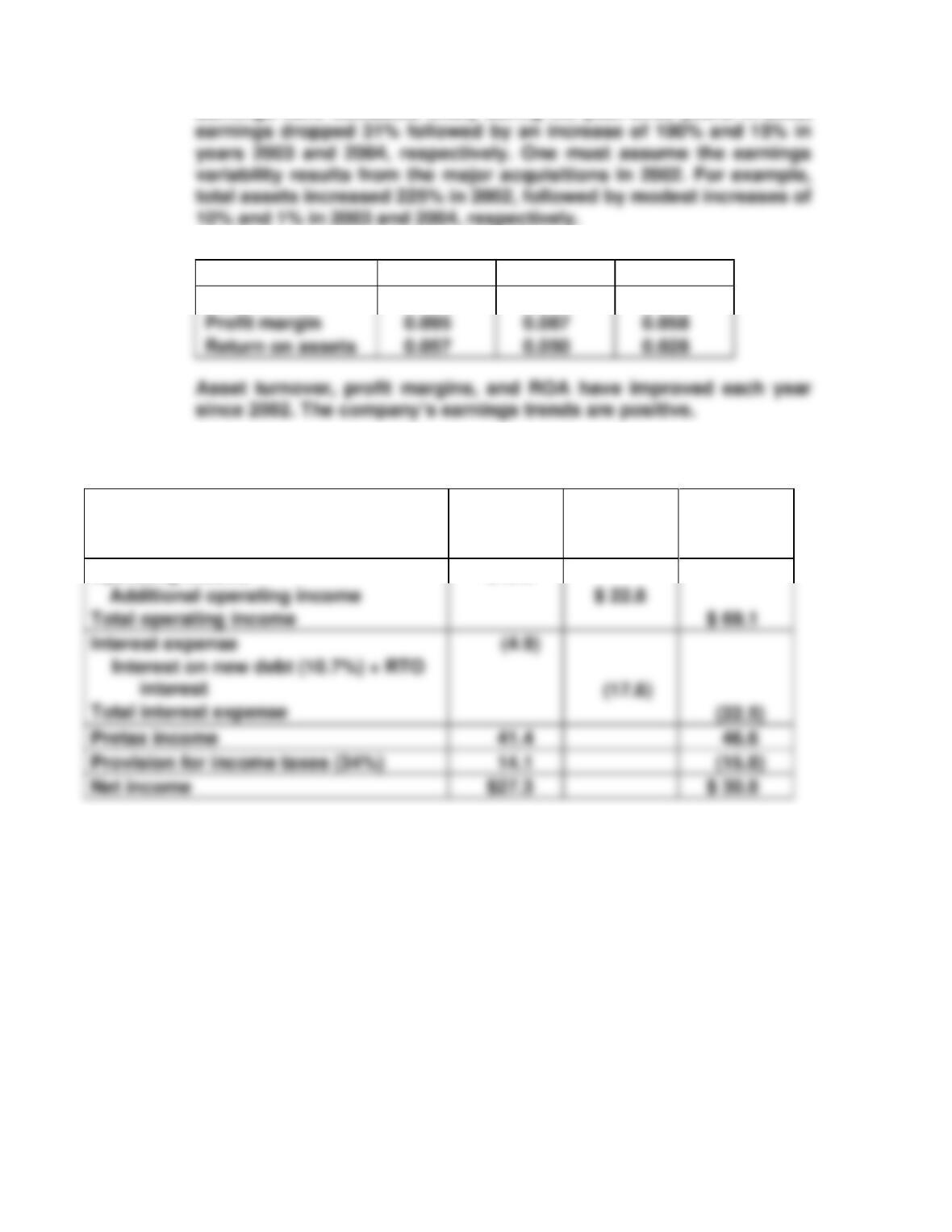

C12-1 A. Note #2 describes a significant investment in fiscal 2002 resulting

B. Growth rates:

2004

2003

2002

Total assets

0.012

0.102

2.249

378 Chapter 12

Earnings have fluctuated wildly during the past three years. In 2002,

C.

2004

2003

2002

Turnover

0.600

0.576

0.481

C12-2 A pro forma analysis would indicate the following:

PRO FORMA INCOME STATEMENT

(In millions)

Before

Acquisi-

tion

Effect of

Acquisi-

tion

After

Acquisi-

tion

Interest on new debt (10.7%) + RTO

Operating income

$46.3

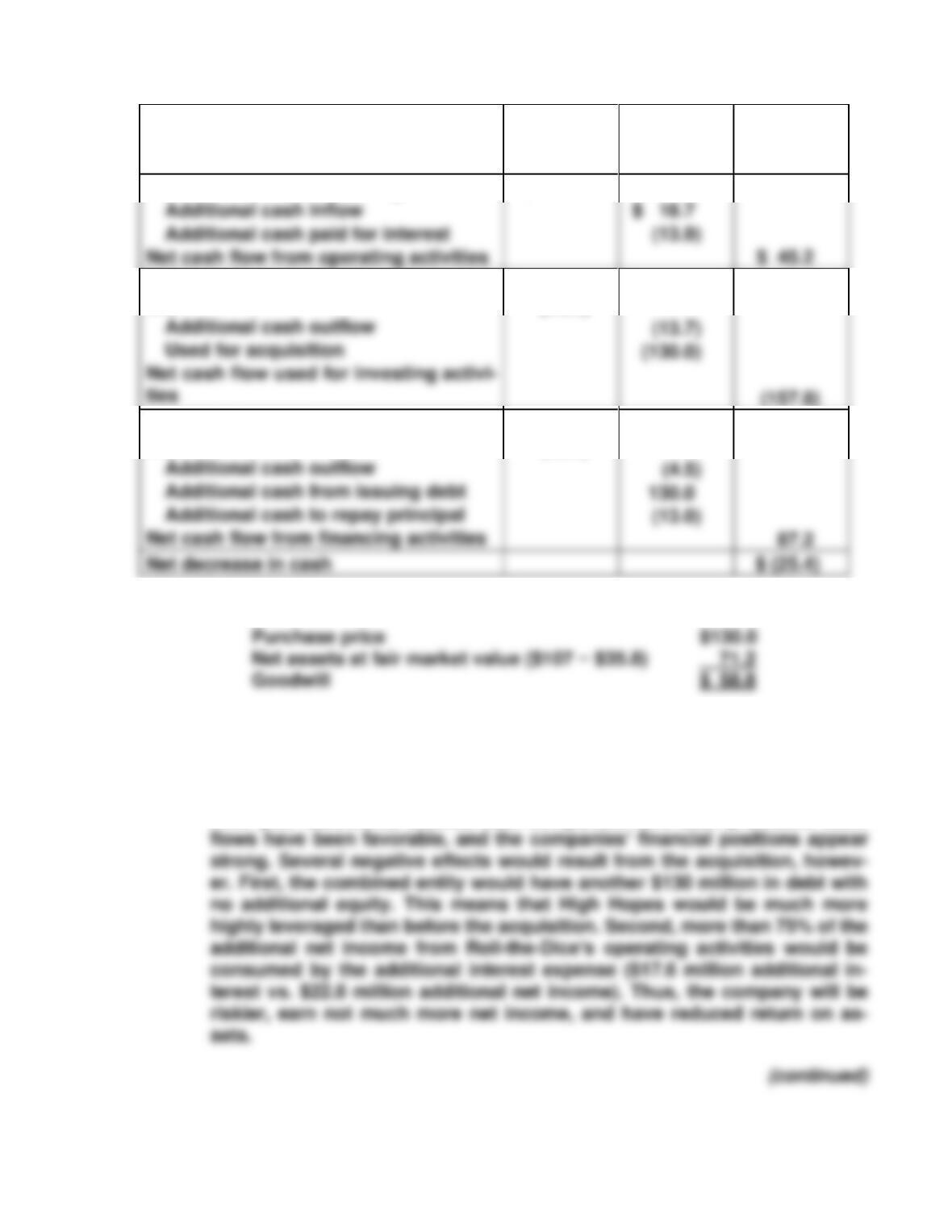

Analysis of Investing Activities 379

PRO FORMA STATEMENT OF CASH

FLOWS

(In millions)

Before

Acquisi-

tion

Effect of

Acquisi-

tion

After

Acquisi-

tion

Net cash flow from operating activities

$ 40.4

Net cash flow used for investing activi-

ties

(14.1)

Net cash flow used for financing activi-

ties

(25.3)

Goodwill is computed as follows:

The $130 million cash used for acquisition and $130 million cash obtained

from issuing debt is a wash and could be omitted from the pro forma

cash flow statement above. Either way, the net decrease in cash is $25.4

million.

Prior year statements indicate both companies have been profitable. Cash

380 Chapter 12

High Hopes Company

Before

After

value of identifiable assets acquired) + $58.8 (goodwill) = $471.5

The biggest problem with the acquisition is the need for additional cash

flow. The added operating cash flow from Roll-the-Dice ($18.7) is not suf-

The pro forma statements for 2008 are only a part of the information to be

Note to instructor: The above analysis has ignored any change in depre-

C12-3 Under the current projections, return on assets would be 9.4% (net in-

come of $150,000 divided by total assets of $1,590,000). The effect on

ROA of each suggestion is as follows:

Analysis of Investing Activities 381

(4) The writedown of old equipment reduces both net income and total

(5) If the accounting department has projected the inclusion of the new

If we adopt only those options that are both in accordance with GAAP

and raise ROA, the results would be as follows.

Net income (as previously projected) $150,000

Unfortunately, however, we must also writedown the carrying value of the

old forming machine. The writedown will be $15,000 [($60,000 × 30%) −