CHAPTER 12

Analysis of Investing Activities

THINKING BEYOND THE QUESTION

How do assets create value for our business?

A company can improve its return on assets by increasing its revenues,

QUESTIONS

Q12-1 Investing activities are important because they provide a basis for future

earnings and cash flows. A company invests in resources that provide a

Q12-2 Additional investment in resources, including plant assets and current

assets, is a basis for company growth. This investment provides re-

Q12-3 Investing activities involve the acquisition or disposal of long-term as-

sets. This includes assets such as productive equipment, investments in

other companies, and intangible assets. The choice to acquire equipment

with certain capabilities rather than other equipment having different ca-

352 Chapter 12

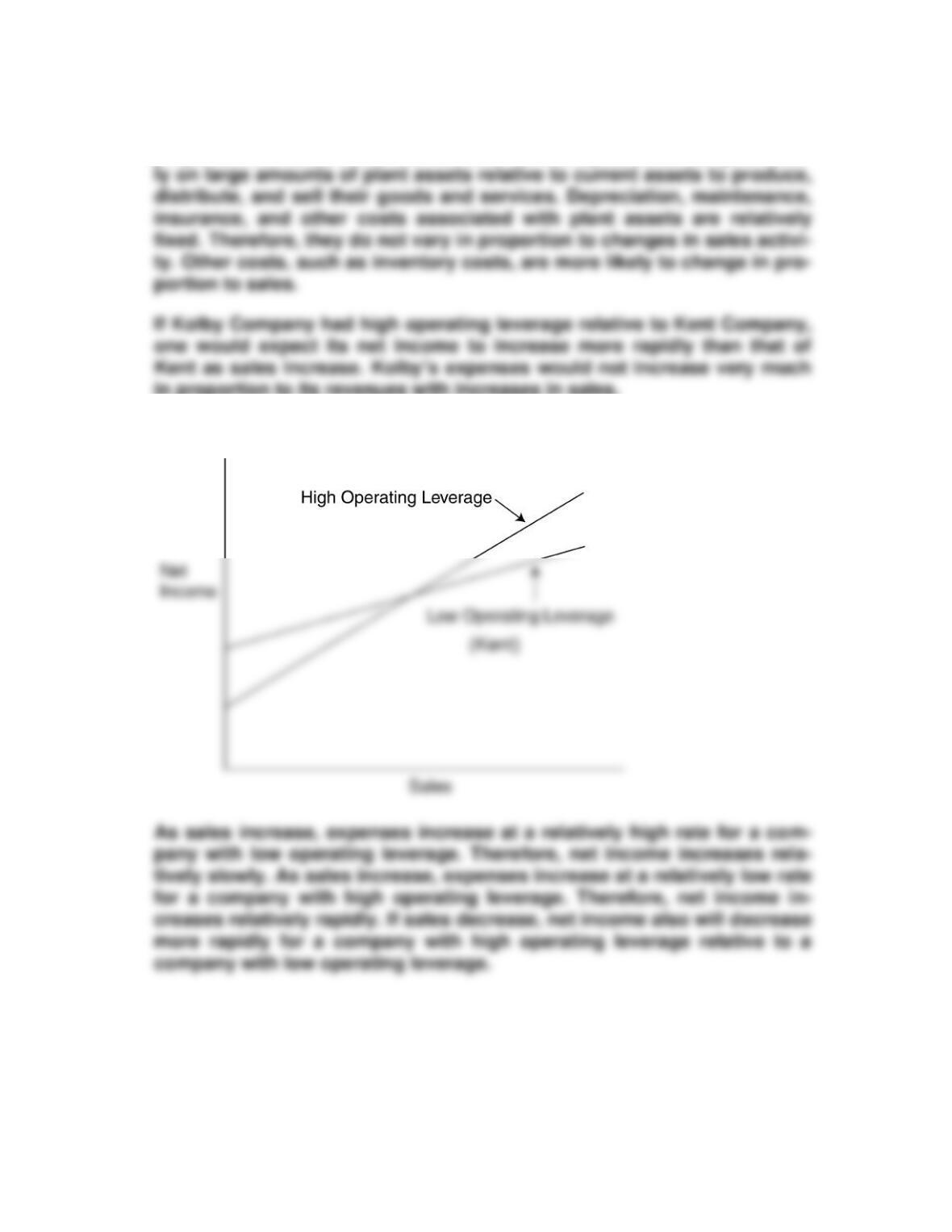

Q12-4 Investments in companies with high fixed costs involve more rather than

less risk. Companies with high fixed costs can be described as having

Q12-5 The balance sheet of a financially strong company will show that it main-

tains sufficient cash to meet its ongoing cash requirements. It should not

maintain an excess of cash, however, because cash does not earn a re-

turn until it is invested. Other than the cash balance at the end of a fiscal

year, the balance sheet does not provide much information about cash.

Q12-6 These facts suggest that the company has well-established products in

mature markets but that there is not much opportunity for growth or ex-

pansion. It is encouraging that profits are being earned and that cash flow

from operations is also positive. It is interesting, however, that the scale

Analysis of Investing Activities 353

Q12-7 It depends on the nature of the business involved. Some businesses, by

their very nature, require huge and costly investments in facilities and

equipment. Oil refineries or auto manufacturers would be good examples

Q12-8 Both amounts are stated in terms of cost. Therefore, the portion of cost

that has been depreciated already yields information about the general

age of the assets. Depending on the nature of the business, this can be

Q12-9 Asset turnover is a function of two components: sales and total assets.

Clearly, if the acquisition of new assets had no effect on sales, the pres-

ence of the additional assets would cause asset turnover to fall. But

Q12-10 Generally, companies become more valuable because of growth in sales

and profits. One way to increase sales and profits is by expanding the

scale of operations. This means making new investments in assets that

354 Chapter 12

Q12-11 Return on assets is a reflection of investing decisions made in the past.

Because of past investing decisions, the company has a certain collec-

tion of assets available today for use in generating profits. If wise (or

Q12-12 The formula to compute asset turnover is sales divided by total assets.

Therefore, any strategy that increases the numerator proportionately

more than the denominator will generate higher asset turnover. Similarly,

Q12-13 Revenues and expenses do not always increase proportionately. Consid-

er grocery stores, for example. If sales increase during a certain week

over prior weeks, there are many costs that do not increase at all. For ex-

ample, the costs related to the store building and equipment do not in-

Q12-14 Investing activities often require financing. As new assets are acquired,

new liabilities are created that may increase the risk of liabilities already

in place. Therefore, creditors (particularly long-term creditors) monitor

Analysis of Investing Activities 355

Q12-15 A company’s balance sheet identifies the costs of its assets and the

sources of finances used to acquire them. Financial assets and liabilities

may be adjusted for changes in market value, but the balance sheet does

EXERCISES

E12-2 a. Sales $ 8,000,000 $10,000,000 $ 12,000,000

b. Sales $ 8,000,000 $10,000,000$ 12,000,000

Net income (loss) $ (400,000) $ 1,000,000 $ 2,400,000

c. Operating leverage has a positive effect on net income when sales in-

356 Chapter 12

E12-3 Operating leverage can be measured as the percentage of a company’s

total costs accounted for by fixed costs. Some companies have higher

proportions of fixed costs than others. For example, some companies re-

in proportion to its revenues with increases in sales.

The following diagram illustrates the relationship:

(Kolby)

Analysis of Investing Activities 357

E12-4 a. Co. A Co. B

Sales $10,000 $10,000

c. Co. A Co. B

Sales $ 9,000 $ 9,000

d. Co. A Co. B

Sales $ 11,000 $11,000

E12-5

Change in total assets from prior year

2004

2003

0.13

(continued)

358 Chapter 12

Capital expenditures to total assets

2004

2003

2002

Capital expenditures to total assets are remarkably similar for both com-

Capital expenditures to

depreciation and amortization

2004

2003

2002

Both companies reported declining capital expenditures relative to de-

preciation expense during the periods reported. However, with the excep-

E12-6 The effect of the sales on the company’s accounts would be as follows:

A. Total assets would increase by $115,000, as would net income and

retained earnings.

B. Total assets would decrease by $110,000, as would net income and

retained earnings.

The sale of investment A or B has a noticeable effect on the company’s

net income and return on assets. Historical costs conceal a company’s

Analysis of Investing Activities 359

E12-7 2004 2003 2002

Profit margin (net income ÷ net revenue) 0.064 0.060 0.040

Change in capital expenditures 0.079 0.007

E12-8 2004 2003 2002

Profit margin (net income ÷ net revenue) 0.120 0.086 0.058

Asset turnover (revenues ÷ total assets) 0.685 0.663 0.643

E12-9 2004 2003 2002

Cash flow from operating activities to assets 0.140 0.127 0.121

McDonald’s Corporation’s cash flow to assets ratio increased in 2003 and

360 Chapter 12

E12-10

Lucy’s Lockets

Desi’s Delights

2008

2007

2008

2007

Asset turnover

126.0%

122.2%

74.3%

76.7%

ates a higher return.

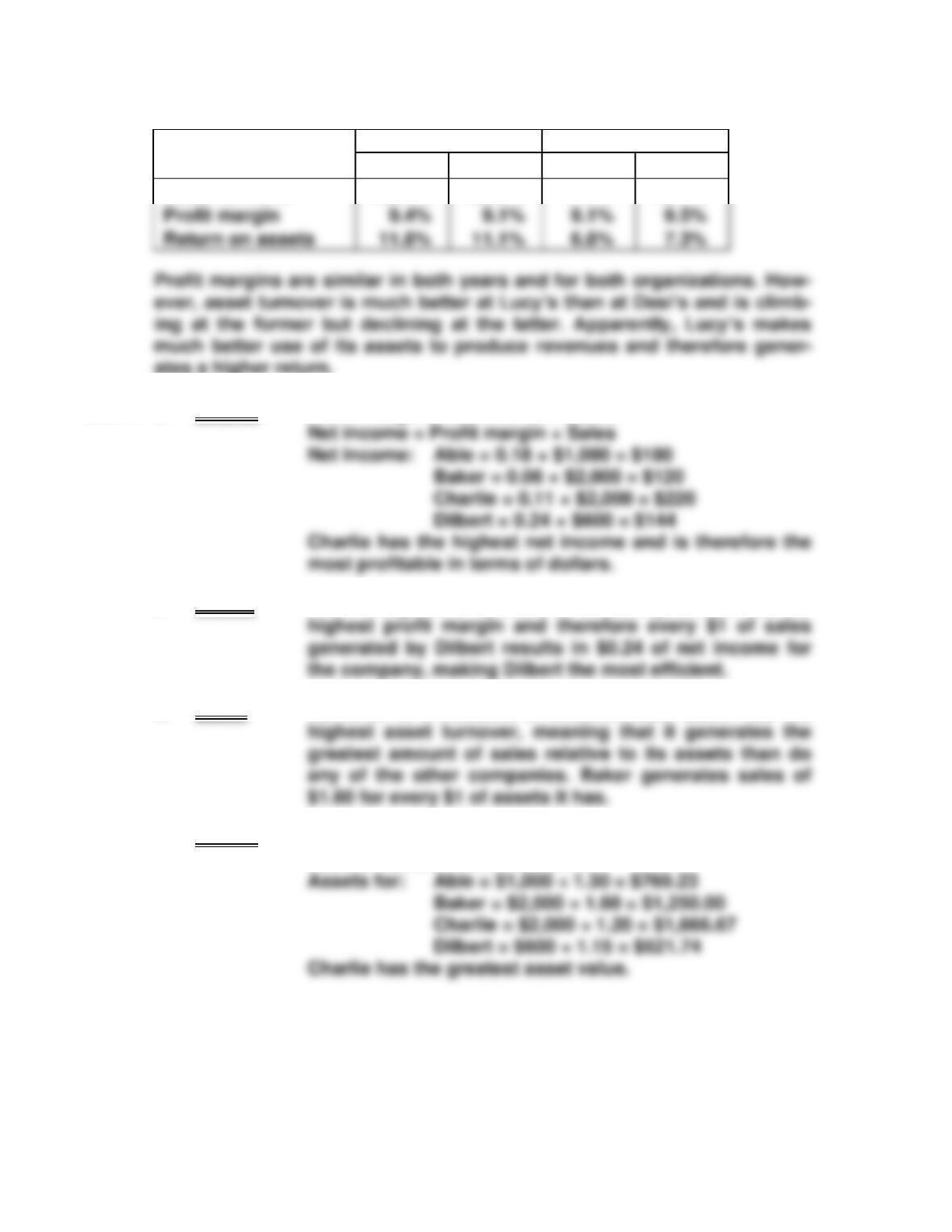

E12-11 a. Charlie Profit margin = Net income ÷ Sales

b. Dilbert Profit margin is a measure of efficiency. Dilbert has the

c. Baker Turnover is a measure of effectiveness. Baker has the

d. Charlie Asset turnover = Sales ÷ Assets

Assets = Sales ÷ Asset turnover

Analysis of Investing Activities 361

E12-12 a. 20% Sales 20% Sales

Decrease Increase

b. Current Decrease Increase

Sales of 20% of 20%

1. ROA 1.2 0.88 1.52

2. Change in ROA (26.7%) 26.7%

If sales change, then net income, ROA, profit margin, and asset turnover

change in the same direction. However, a percentage change in sales (in

E12-13 Each strategy could have a positive effect on return on assets. In the right

combination with other factors, each also has its risks as follows:

• Increased sales without an increase in assets will improve return on

assets unless the increase causes more expenses than revenues.

E12-14 Effectiveness refers to a company’s ability to use its assets to generate

sales; it can be measured by calculating asset turnover (sales total as-

362 Chapter 12

E12-15 Return-related ratios with and without the new product line can be calcu-

lated as follows:

Last Year

Pro Forma

Effectiveness: Asset turnover

86.7%

86.6%

E12-16

Year 2008

Year 2007

Year 2006

ROA

5,250 ÷ 30,000

= 0.175

2,800 ÷ 20,000

= 0.14

1,200 ÷ 10,000

= 0.12

Profit margin

5,250 ÷ 15,000

E12-17 These impaired assets should be written down to their current market

value. The amount involved for each machine is the book value of $3,600

($6,000 less depreciation of $600 per year for four years) less the resale

Analysis of Investing Activities 363

E12-18 Return on equity should increase because of decreased outstanding eq-

uity and decreased interest expense. However, if the reduced debt de-

creased leverage, this effect may not occur. The increase in cash flow

E12-19 Cash flow from operations has increased by 19% during the three-year

period [($3,195 − $2,688) ÷ ($2,688)]. It appears that the investing activities

have been successful in generating additional operating cash flow.

At this point, cash flow from operating activities is sufficient to cover in-

vesting and financing activities. In fact, 29% of the operating cash flow

364 Chapter 12

PROBLEMS

P12-1 (student name, address, date)

Ivan Steeger

1352 Bull Run Road

Milltown, OR 97111

Dear Ivan:

You asked about issues to consider in your decisions about equipment

for the new cookie business. Given your own background with small

businesses, I’m sure you already have a number of topics for discussion.

But I do have a few suggestions.

If you purchase the automated equipment, you will have higher operat-

ing leverage. Your fixed costs will be higher, but you will avoid the varia-

ble cost of employees used to shape cookies by hand. The automated

equipment could bring higher cash flow if sales are high. However, the re–

lated fixed costs would increase possible losses if revenues were small.

The larger-capacity equipment would take care of your projected sales

for several years, at a lower total price than a purchase of smaller equip-

ment now and additional equipment later. On the other hand, your risk of

Analysis of Investing Activities 365

P12-2 A. Risk: It appears that Strategy B is riskier because it leads to more

B. Operating leverage: The apparent fixed costs are as follows:

Sales of Sales of Sales of

C. Investment strategy: It appears that Strategy B involves a greater

amount invested in plant assets, because depreciation is higher and

fixed. Under Strategy A, depreciation expense increases at each

P12-3 (In thousands)

A.

Old equipment

Outlying

Rural Areas

Only

Outlying

Rural Areas

Plus Two

Towns

Outlying

Rural Areas

Plus Four

Towns

Revenues

$ 3,000

Fixed expenses

Net income (loss)

$ 600

B.

New equipment

Only

Revenues

$ 3,000

Fixed expenses

Net income (loss)

$ 900

Outlying

Rural Areas

Outlying

Rural Areas

Plus Two

Outlying

Rural Areas

Plus Four

C. In this case, under the current revenue conditions, changing to the

new equipment has no effect on the projected net income from the

garbage removal service, which is $200,000 with or without the

Analysis of Investing Activities 367

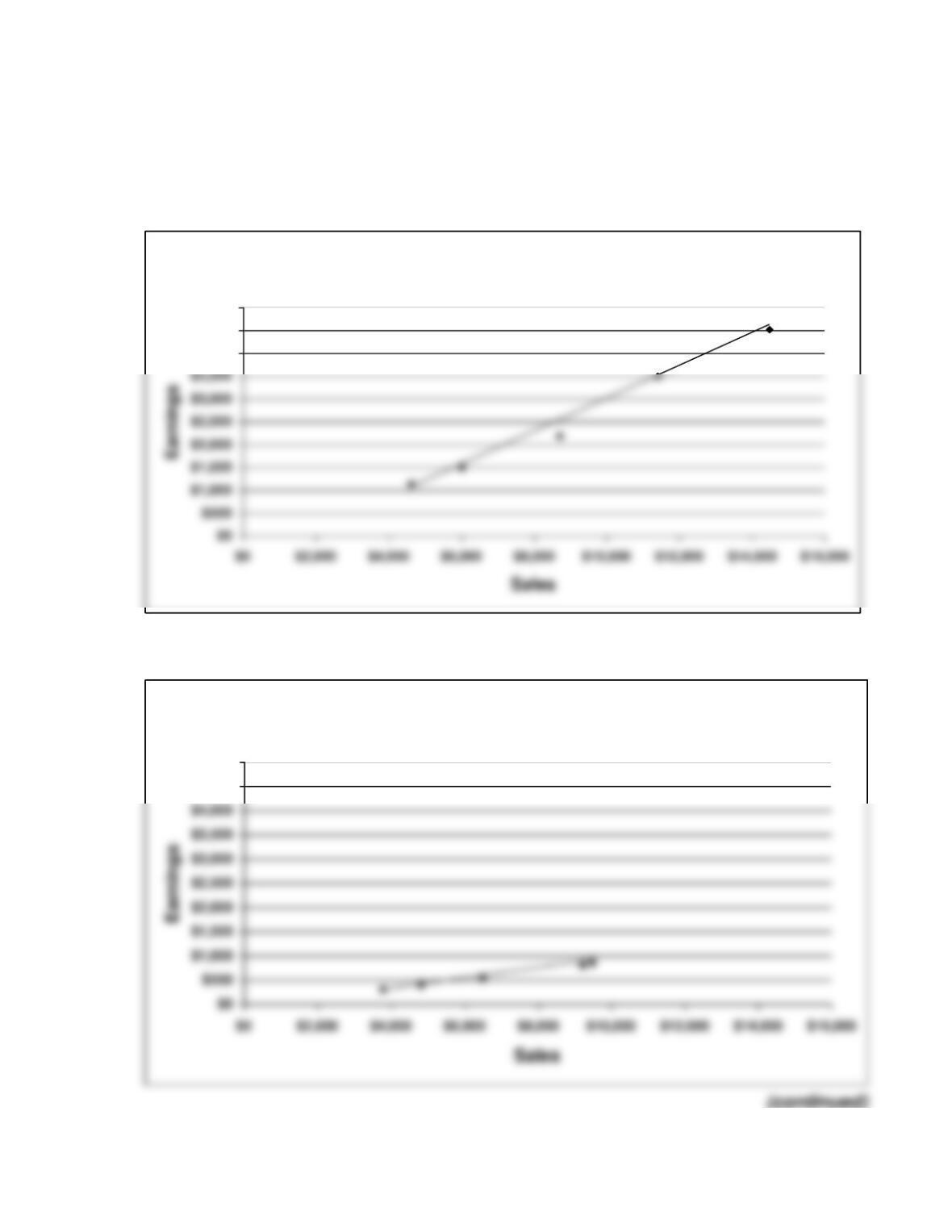

P12-4 A graph of the relationship between sales and earnings for each company

shows the following:

Solution Software, Inc.

$4,000

$4,500

$5,000

Fashion Clothing Co.

$4,500

$5,000