Accounting Information Systems

12-21

Step 5: Click the “Design Mode” option in the tool bar to exit Design Mode. You can now click on the spin button and change the

value of the sales growth rate. Notice how all of the values in the spreadsheet change simply by clicking the spin button arrows – no

need to repeatedly type in the new sales growth rate value.

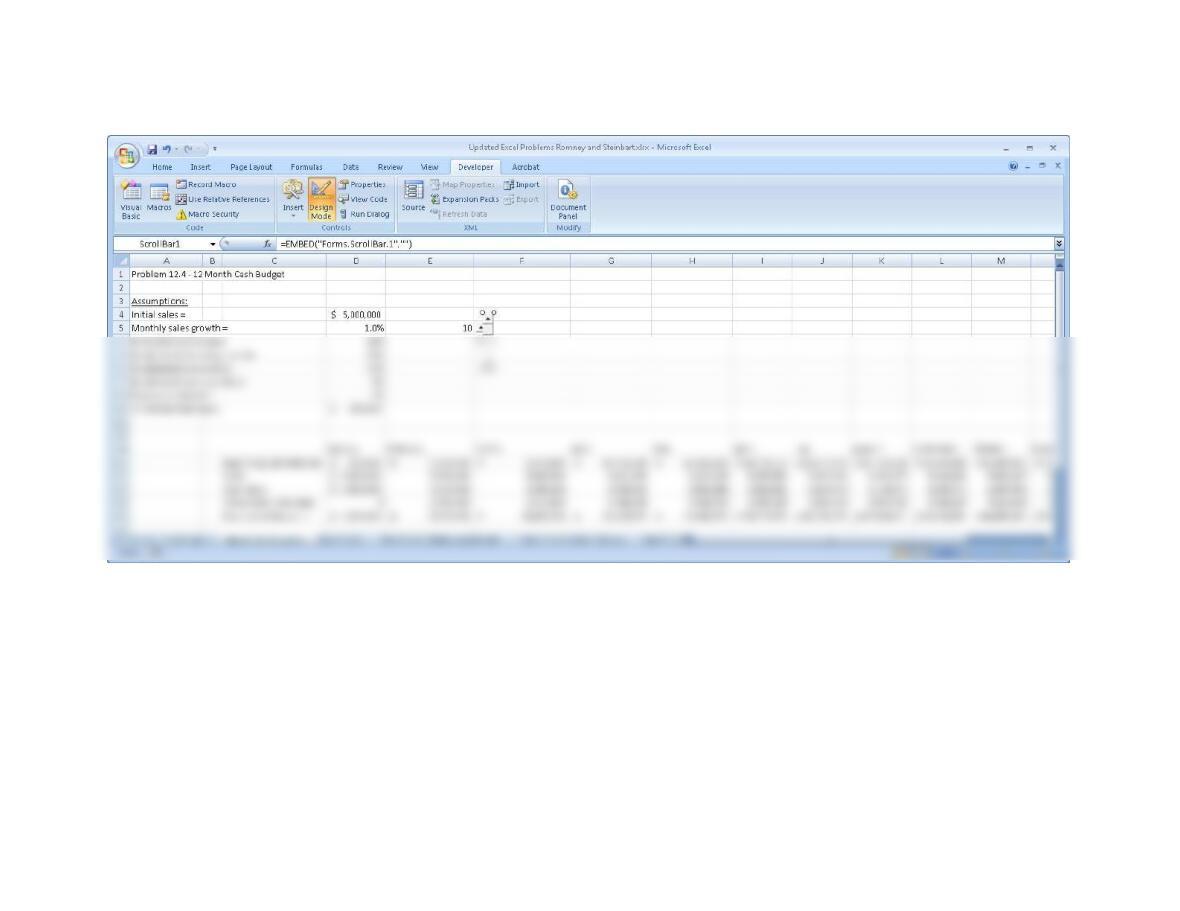

c. Add a scroll bar to your spreadsheet that will let you modify the amount of initial sales to vary from $4,000,000 to

$6,000,000 in increments of $100,000.

A scroll bar is another spinner tool. The difference between a scroll bar and a spin button is that a scroll bar has a space between its

Ch. 12: The Revenue Cycle: Sales and Cash Collections

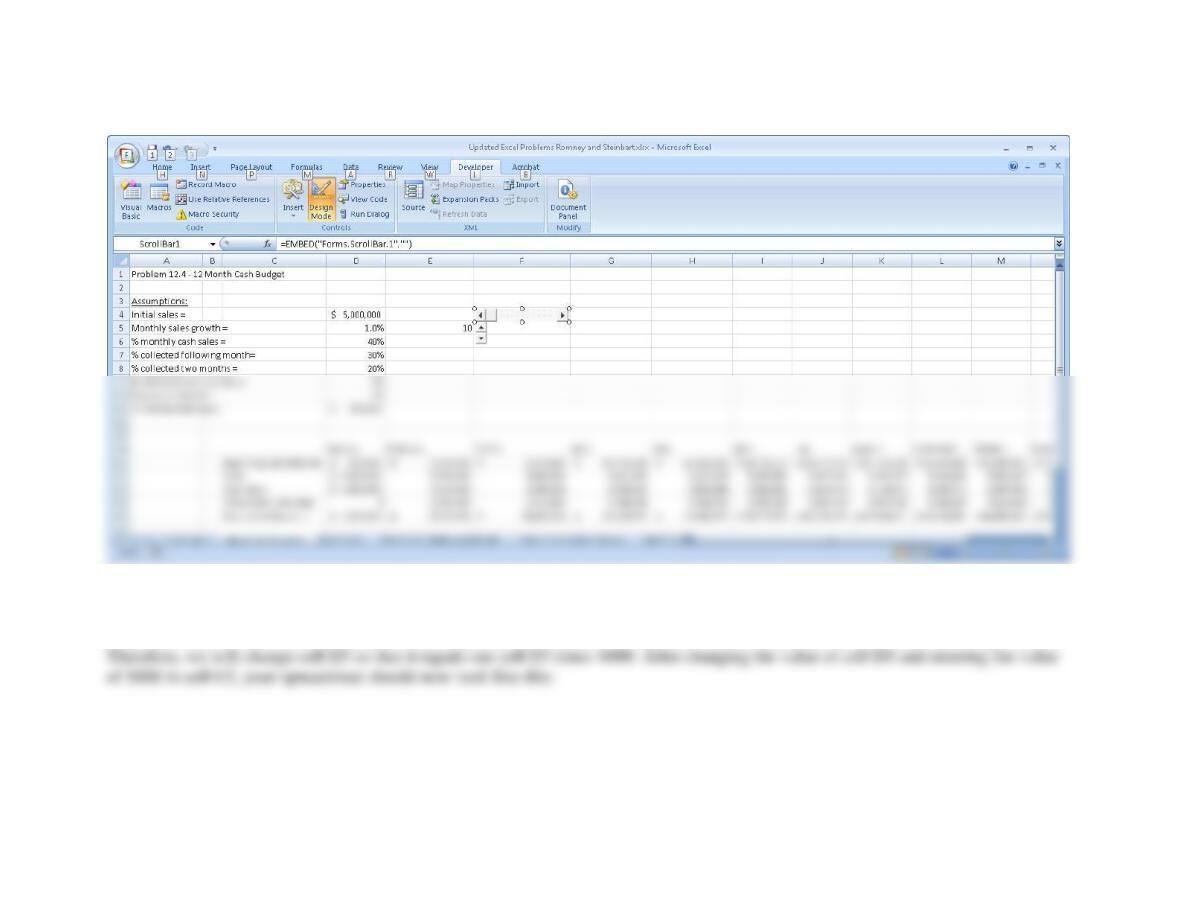

Step 2: Click on one corner of the scroll bar and drag it so that it fills cell F5 horizontally. Your spreadsheet should now look like this:

Accounting Information Systems

12-23

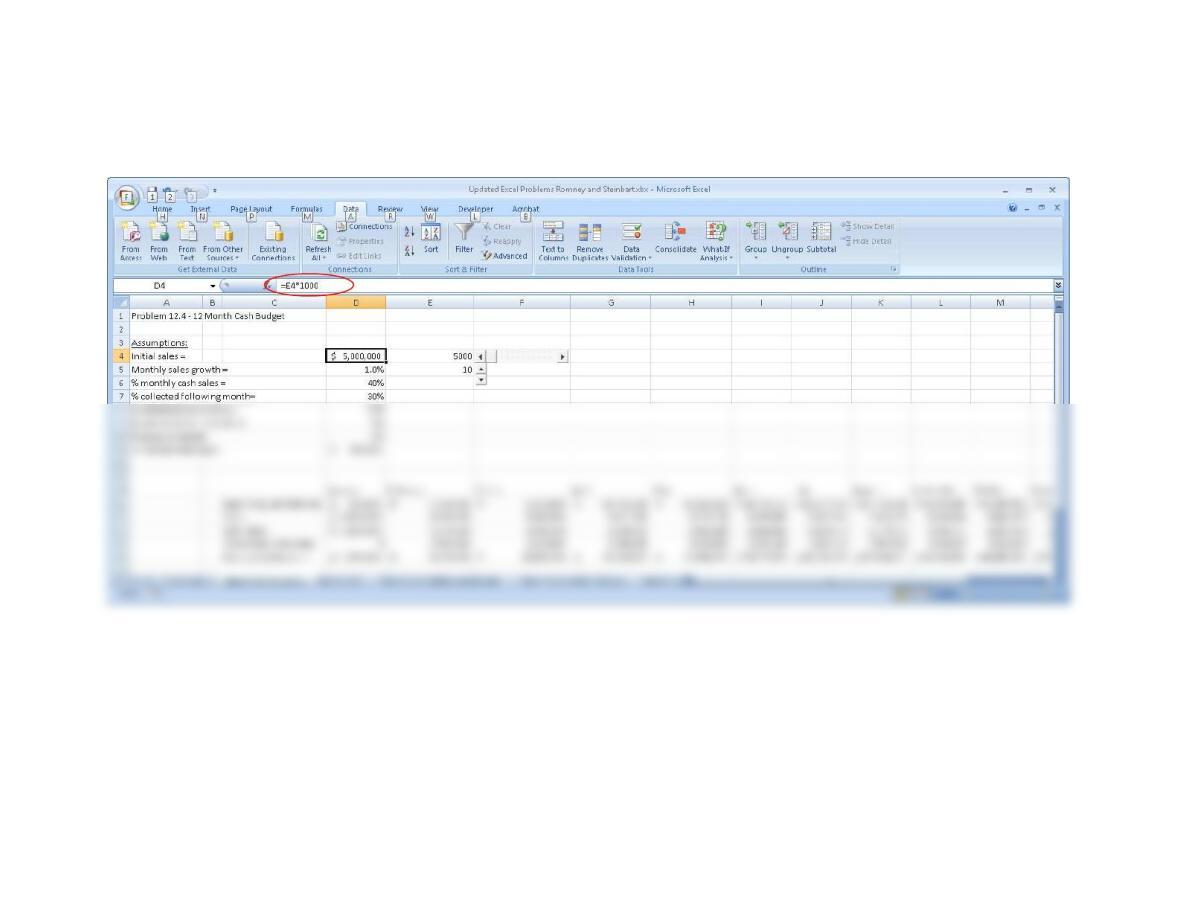

Step 3: As with the spin button, we have to link the scroll bar to the cell that will display the values we wish to vary. Our goal is to

vary sales from $4,000,000 to $6,000,000 in increments of $100,000. The spinner tool, however, cannot work with such large values.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

Accounting Information Systems

12-25

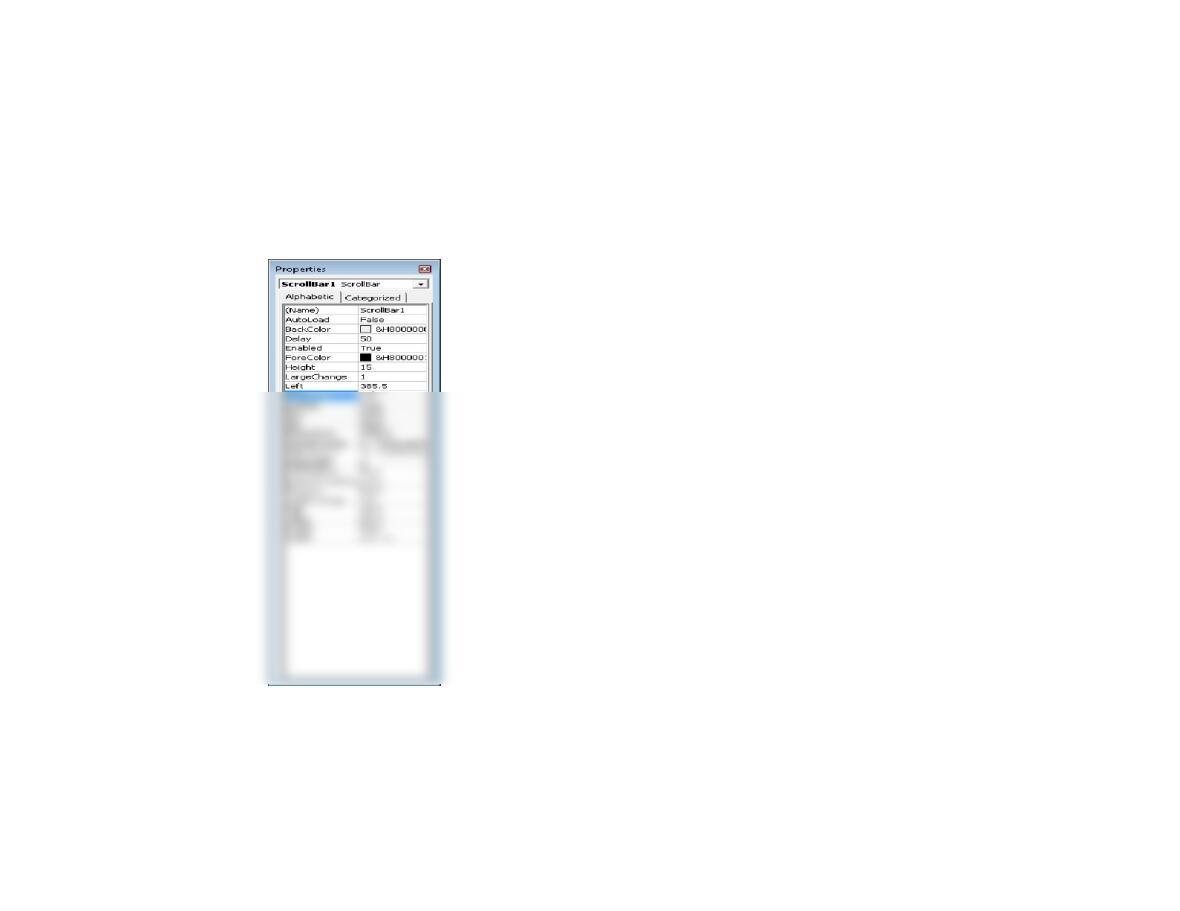

Step 4: Now right-click on the scroll bar tool in cell F5, select properties, and enter the following values:

LinkedCell = E4

Max = 6000

Min = 4000

SmallChange = 100

Step 5: You can now click on the left and right arrows in the scroll bar to vary the amount of initial sales and see the effects ripple

through the spreadsheet – without having to retype new initial sales values.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

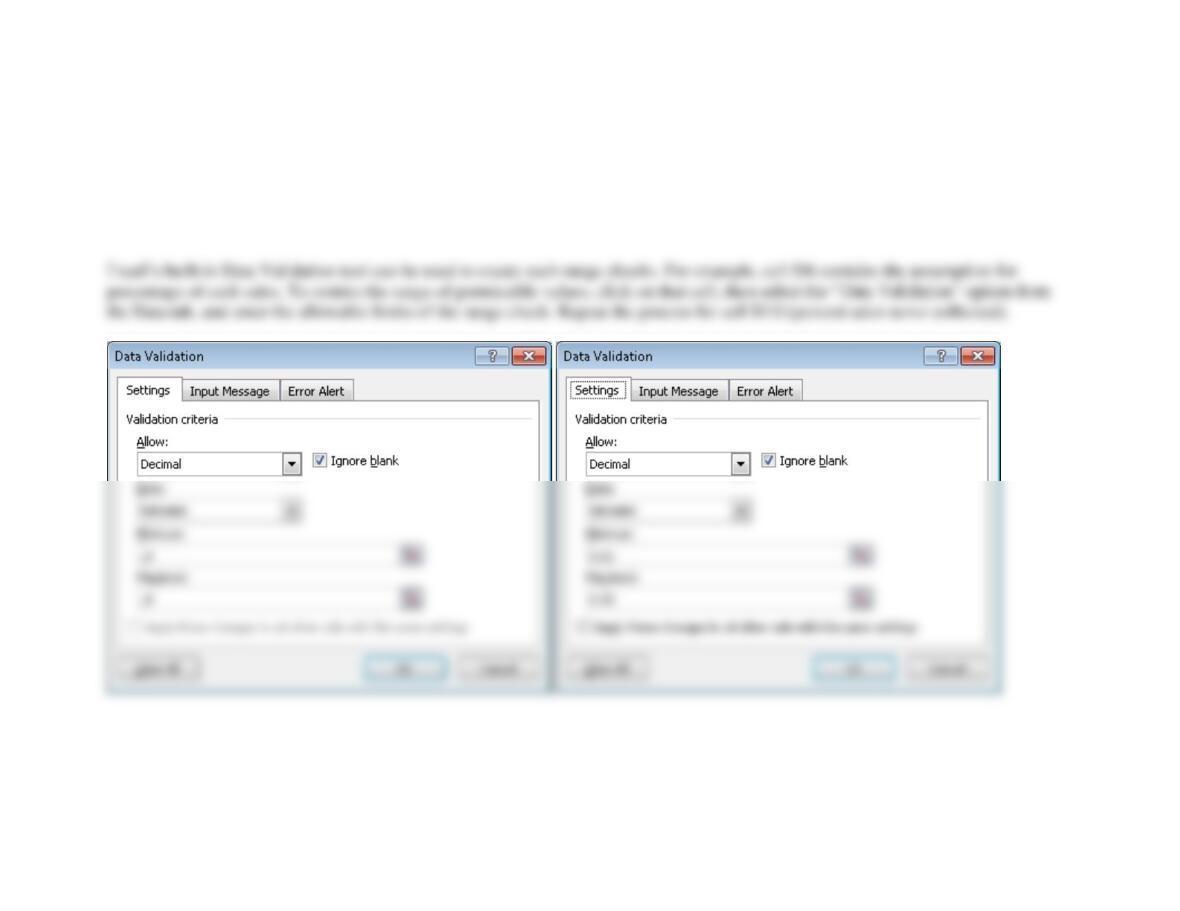

d. Design appropriate data entry and processing controls to ensure spreadsheet accuracy.

Chapter 10 describes the various data input validation controls that can be used. In this problem, students should be instructed to set

reasonable range checks on the allowable values for the percentage of sales that are cash sales and what percentage of credit sales is

never collected.

In addition, user data entry should be restricted to the cells that contain the initial assumptions. All other cells in the spreadsheet

should be locked.

12.5 For each of the following activities identify the data that must be entered by the

employee performing that activity and list the appropriate data entry controls:

a. Sales order entry clerk taking a customer order

Data that must be entered

Appropriate Data Entry Edit Controls

User ID

Validity check

Compatibility test (is user authorized to perform this task?)

Completeness check (cannot be null)

Password

Validity check

Compatibility test (is user authorized to perform this task?)

Completeness check (cannot be null)

Note: All other fields on the sample sales order entry screen (see Figure 12-6) can be

completed by the system.

Delivery method

Choose from pull-down list of options

Desired delivery date

Field check (date)

Item number

Field check

Validity check

Check digit

Ch. 12: The Revenue Cycle: Sales and Cash Collections

b. Shipping clerk completing a bill of lading for shipment of an order to a customer

Data that must be entered

Appropriate Data Entry Edit Controls

User ID

Validity check

Compatibility test (is user authorized to perform this task?)

Completeness check (cannot be blank)

Password

Validity check

Compatibility test (is user authorized to perform this task?)

Completeness check (cannot be blank)

Carrier name

Choose from pull-down list of approved carriers

Note: All other fields on the sample bill of lading (see Figure 12-11) can be completed by

the system.

Customer name (consigned to)

Choose from pull-down list of customers

Completeness check (cannot be blank)

Number of packages

Field check (numeric only)

Sign check (>0)

Completeness check (cannot be blank)

Description

Completeness check (cannot be blank)

Weight

Field check (numeric only)

Completeness check (cannot be blank)

Class or rate

Choose from pull-down menu of options

Completeness check (cannot be blank)

Accounting Information Systems

12-29

12.6 Create a questionnaire checklist that can be used to evaluate controls for each of the

four basic activities in the revenue cycle (sales order entry, shipping, billing, and

cash collections).

a. For each control issue, write a Yes/No question such that a “No” answer

represents a control weakness. For example, one question might be “Are

customer credit limits set and modified by a credit manager with no sales

responsibility?”

A wide variety of questions is possible. Below is a sample list:

Question

Yes

No

1. Is access to master data restricted?

8. Are physical counts of inventory taken regularly and used to adjust the

perpetual inventory records?

9. Are the credit approval and sales order entry tasks performed by

separate individuals?

10. Are picking list quantities compared to sales orders?

11. Is physical access to inventory controlled?

12. Are reports of open sales orders regularly created and reviewed?

13. Are shipping documents reconciled with sales orders?

14. Are the shipping and billing functions performed by different

individuals?

15. Are monthly statements mailed to customers?

16. Are the functions of processing customer payments and maintaining

accounts receivable performed by separate individuals?

17. Is the bank account reconciled by someone other than the person who

processes customer payments?

18. Are lockbox arrangements used?

19. Are customer credit limits set and modified by a credit manager with no

sales responsibility?

2. Is the master data regularly reviewed and all changes investigated?

3. Is sensitive data encrypted while stored in the database?

4. Does a backup and disaster recovery plan exist?

5. Have backup procedures been tested within the past year?

6. Are appropriate data entry edit controls used?

7. Are digital signatures required for online orders?

Ch. 12: The Revenue Cycle: Sales and Cash Collections

b. For each Yes/No question, write a brief explanation of why a “No” answer

represents a control weakness.

Question

Reason a “No” answer represents a weakness

1

Unrestricted access to master files could facilitate fraud by allowing employees to

5

If the backup plan is not regularly tested, it may not work.

6

Without proper data entry edit controls, errors in sales order entry may occur

resulting in shipments that are not billed, sending the wrong items, etc.

7

Without a digital signature, orders may be processed and sent that the customer later

refuses, resulting in increased costs

8

Without periodic physical counts, the perpetual inventory records are likely to be

incorrect, creating problems in filling customer orders on time

9

If the same individual approves changes in credit and takes customer orders, they can

increase credit limits for friends which may result in sales that are not collected.

10

Not comparing picking lists to sales orders can result in shipping the wrong

merchandise or the wrong quantities to customers.

11

If physical access to inventory is not restricted, theft may occur.

12

Failure to monitor sales orders may result in delays in filling customer orders

13

Failure to compare shipping documents to sales orders may result in errors in filling

customer orders

14

Not segregating the billing and shipping functions increases the risk of deliberately

not billing for shipments

15

Not mailing monthly statements to customers increases the risk of not detecting

errors or fraud in maintaining accounts receivable

16

Not segregating handling of customer payments and maintenance of accounts

receivable creates the possibility of lapping

17

If the bank account is reconciled by the same person who processes customer

payments, theft can occur and be covered up by adjusting the bank balance on the

bank reconciliation

18

Not using lockboxes, where feasible, creates delays in receiving customer payments

which could result in cash flow problems

bonuses earned) without regard to the risk of having to write off the sales as

uncollectible.

change account balances to conceal theft

2

Failure to investigate all changes to customer master data may allow fraud to occur

because unauthorized changes to credit limits may not be detected.

3

Failure to encrypt sensitive data can result in unauthorized disclosure of personal

information about customers

4

If a backup and disaster recovery plan does not exist, the organization may suffer

loss of important data.

Accounting Information Systems

12-31

12.7 O’Brien Corporation is a midsize, privately owned, industrial instrument

manufacturer supplying precision equipment to manufacturers in the Midwest. The

corporation is 10 years old and uses an integrated ERP system. The administrative

offices are located in a downtown building and the production, shipping, and

receiving departments are housed in a renovated warehouse a few blocks away.

receiving the merchandise.

Customer orders are picked and sent to the warehouse, where they are placed near

the loading dock in alphabetical sequence by customer name. The loading dock is

used both for outgoing shipments to customers and to receive incoming deliveries.

There are ten to twenty incoming deliveries every day, from a variety of sources.

The system is configured to prepare the sales invoice only after shipping employees

enter the actual quantities sent to a customer, thereby ensuring that customers are

billed only for items actually sent and not for anything on back order.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

Identify at least three weaknesses in O’Brien Corporation’s revenue cycle activities.

Describe the problem resulting from each weakness. Recommend control

procedures that should be added to the system to correct the weakness.

(CMA Examination, adapted)

Weaknesses and Potential Problem(s)

Recommendation(s) to Correct

Weaknesses

1. Orders from new customers do not

require any form of validation, resulting in

Require digital signatures on all online

orders from new customers.

2. Customer credit histories are not

checked before approving orders, resulting

in excessive uncollectible accounts.

Customers’ credit should be checked and

no sales should be made to those that do

not meet credit standards.

3. Outgoing shipments are placed near the

loading dock door without any physical

Separate the shipping and receiving docks.

accounts for the inaccuracies in the

perpetual inventory records and may also

prevent timely detection of theft.

4. Physical counts of inventory are not

made at least annually. This probably

Physical counts of inventory should be

made at least once a year.

5. Shipments are not reconciled to sales

orders, resulting in sending customers the

wrong items.

The system should be configured to match

shipping information to sales orders and

alert the shipping employees of any

discrepancies.

unanticipated shortages that result in delays

in filling customer orders.

they are discovered.

6. The perpetual inventory records are only

updated weekly. This contributes to the

The warehouse staff should enter

information about shortages as soon as

Accounting Information Systems

12.8 Parktown Medical Center, Inc. is a small health care provider owned by a publicly

held corporation. It employs seven salaried physicians, ten nurses, three support

staff, and three clerical workers. The clerical workers perform such tasks as

reception, correspondence, cash receipts, billing, and appointment scheduling. All

are adequately bonded.

The servicing physician prepares a charge slip that is given to one of the clerks for

pricing and preparation of the patient’s bill. At the end of the day, one of the clerks

uses the bills to prepare a revenue summary and, in cases of credit sales, to update

the accounts receivable subsidiary ledger.

The clerks take turns preparing and mailing monthly statements to patients with

unpaid balances. One of the clerks writes off uncollectible accounts only after the

physician who performed the respective services believes the account will not pay

and communicates that belief to the office manager. The office manager then issues

a credit memo to write off the account, which the clerk processes.