Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 12

Chapter 12

Accounting for Partnerships

QUESTIONS

1. Under the circumstances described, the death, bankruptcy, or legal inability of a

partner to execute a contract ends a partnership. In addition, if a partnership is

3. All partners in a general partnership have unlimited liability. A limited partnership

4. Yes, partners can limit the right of a partner. Such an agreement is binding on

9. George’s claim is not valid unless the previously agreed upon method of sharing net

incomes and losses granted George an annual salary allowance of $25,000. Unless

2,000

5,000

11. At all times in the accounting history of a partnership (or any organization), assets

must equal liabilities plus equity. When the assets are converted to cash, any gains

QUICK STUDIES

Quick Study 12-1 (10 minutes)

a. The partnership will need to pay because it is a merchandising firm.

Quick Study 12-2 (10 minutes)

Quick Study 12-3 (10 minutes)

Cash ……………………………………………………………………………….

1,000

717

Quick Study 12-4 (15 minutes)

Stolton

Bright

Total

Net income ………………………………………

52,000

Salary allowances

Stolton ………………………………………….

Balance of income …………………………..

17,000

Balance allocated equally

Stolton ………………………………………….

Balance of income …………………………..

Quick Study 12-5 (10 minutes)

Quick Study 12-6 (10 minutes)

Quick Study 12-7 (10 minutes)

Choi, Capital ……………………………………………………….…………..

Amal, Capital …………………………………………………………………..

718

Quick Study 12-8 (10 minutes)

1.

Jan. 31

Perez, Capital ……………………………………………………

1,200

2.

Jan. 31

Perez, Capital ……………………………………………………

1,200

3.

Jan. 31

Perez, Capital ……………………………………………………

1,200

Quick Study 12-9 (30 minutes)

1.

Field

Brown

Snow

Total

Allocation of all losses

2. a)

May 31

b)

May 31

Snow, Capital ……………………………………………………

719

Quick Study 12-9 (concluded)

3. a)

Snow, Capital ……………………………………………………

b)

Snow, Capital ……………………………………………………

Quick Study 12-10 (15 minutes)

Total partnership return on equity = Net Income/Average equity

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 12

720

EXERCISES

Exercise 12-1 (15 minutes)

Characteristic

General Partnerships

1.

Duration of life

h. Limited

3.

c. Not separate entity from partners

5.

e. Mutual agency

6.

a. Requires only an agreement

721

Exercise 12-2 (20 minutes)

a. Recommended Organization: Sharif, Henry, and Korb might first

consider organizing their business as a general partnership. However, a

problem for these new graduates is that they do not have funds and with

b. Recommended Organization: The two doctors should form a

partnership. A general partnership will have the disadvantage of

c. Recommended Organization: Munson should consider setting up a

limited partnership. Given his real estate expertise he can manage the

722

Exercise 12-3 (25 minutes)

1.

Jan. 1

Cash ………………………………………………………………..

17,500

Equipment ……………………………………………………….

82,500

2.

Jan. 1

Cash ………………………………………………………………..

31,250

Exercise 12-4 (30 minutes)

Cash ………………………………………………………………..

1,000

2,000

3,000

4,000

10,000

Exercise 12-5 (30 minutes)

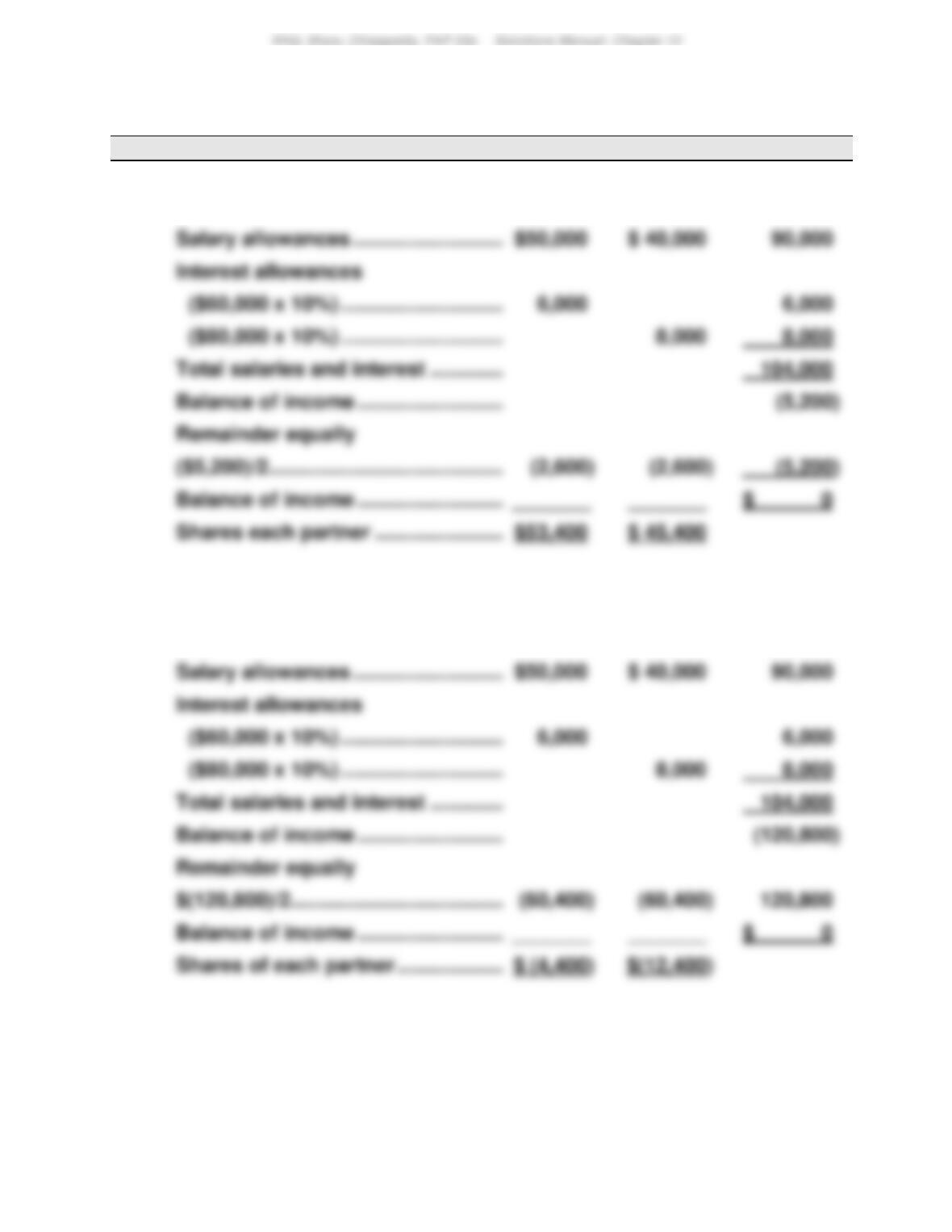

Ramer

Knox

Total

$160,000 x 1/2 …………………………..

($60,000/$140,000) x $160,000 …………………

Salary allowances …………………………..

Total salary and interest …………………………

Balance of income …………………………..

Balance allocated equally

($56,000)/2 ……………………………………………..

28,000

723

Exercise 12-6 (35 minutes)

Ramer

Knox

Total

1.

Net income …………………………………………….

$ 98,800

Salary allowances …………………………..

Total salaries and interest ……………………..

Balance of income …………………………..

Remainder equally

($5,200)/2 ……………………………………………….

Balance of income …………………………..

_______

Shares each partner …………………………..

2.

Net income …………………………………………….

$ (16,800)

Salary allowances …………………………..

Total salaries and interest ……………………..

Balance of income …………………………..

Remainder equally

$(120,800)/2 ……………………………………………

Balance of income …………………………..

_______

$ 0

724

Exercise 12-7 (25 minutes)

1a. 2017

Mar. 1

Cash ………………………………………………………………..

82,500

60,000

Building …………………………………………………………..

34,000

20,000

34,000

20,000

Income Summary ……………………………………………..

90,000

2.

Capital account balances

Eckert

Kelley

Initial investment …………………………..

$ 82,500

$ 67,500

Withdrawals ………………………………….

Share of income* …………………………..

*Supporting calculations

Eckert

Kelley

Total

Net income ……………………………………………………….

$90,000

Salary allowance

Total salary allowance …………………………..

Balance of income …………………………..

Total interest allowances…………………………..

Balance of income …………………………..

Balance allocated equally

Total allocated equally …………………………..

$ 0

725

Exercise 12-8 (10 minutes)

Exercise 12-9 (25 minutes)

1.

Nov. 1

Cash …………………………………………………………………

90,000

2.

Nov. 1

Cash ………………………………………………………………..

3.

Nov. 1

Cash ………………………………………………………………..

80,000

726

Exercise 12-10 (15 minutes)

1.

2.

3.

727

Exercise 12-11 (30 minutes)

a. Loss from selling assets

Total book value of assets ………………………………………

$126,000

Total liabilities (before liquidation)…………………………..

Cash proceeds from sale of assets ………………………….

b. Loss allocation

Turner

Roth

Lowe

Total

Capital balances before

loss liquidation

$ 2,500

$ 14,000

$ 31,500

$ 48,000

(30,400)

$(5,100)

Exercise 12-12 (30 minutes)

a. Loss from selling assets

Total book value of assets ………………………………………

Total liabilities before liquidation …………………………..

$78,000

Cash proceeds from sale of assets ………………………….

b. Loss and deficit allocation

Turner

Roth

Lowe

Total

Capital balances before loss

$ 2,500

$ 14,000

$ 31,500

$ 48,000

Exercise 12-13 (20 minutes)

Rugged Sports Enterprises LP:

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 12

729

PROBLEM SET A

Problem 12-1A (30 minutes)

Cash ………………………………………………………………………………

1,000

3,000

5,000

8,000

730

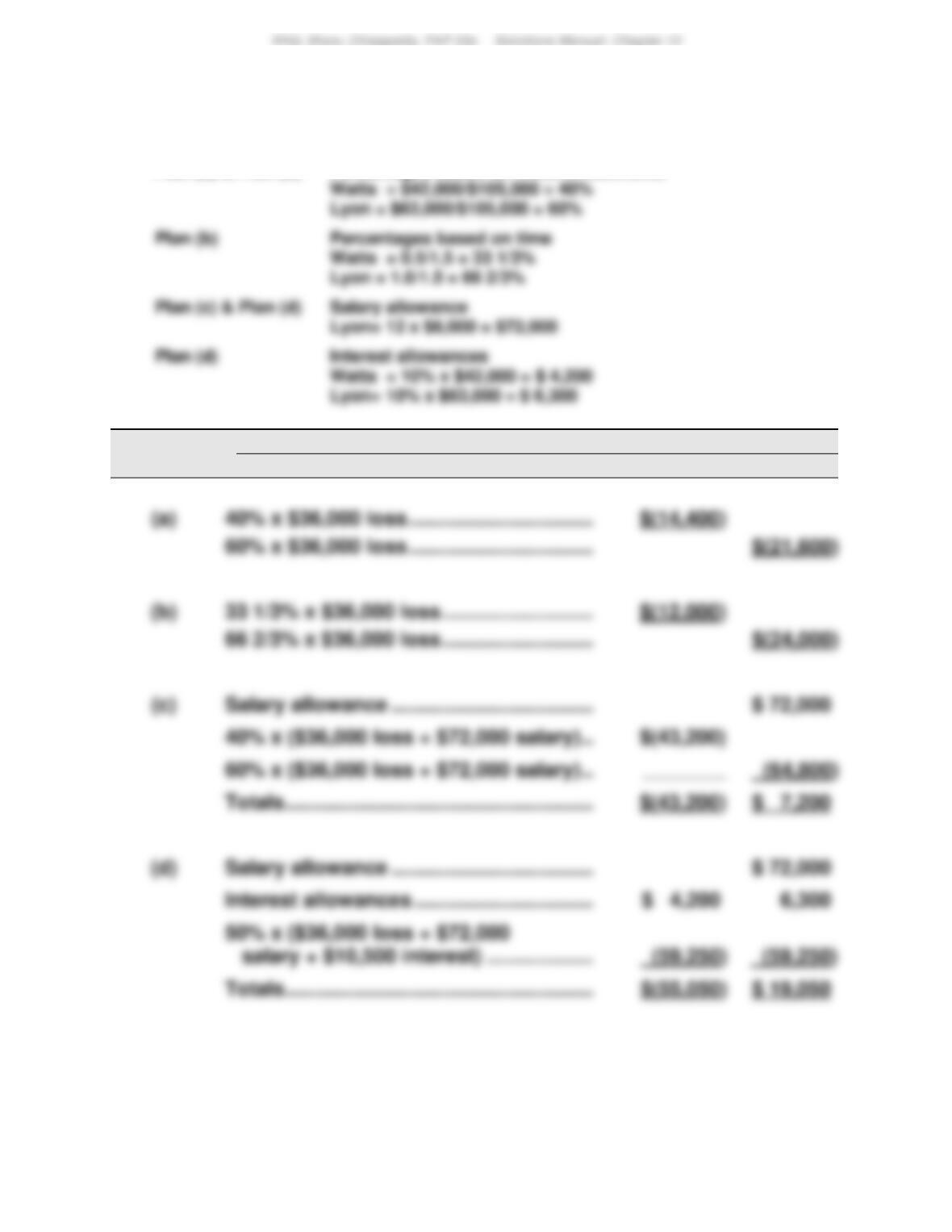

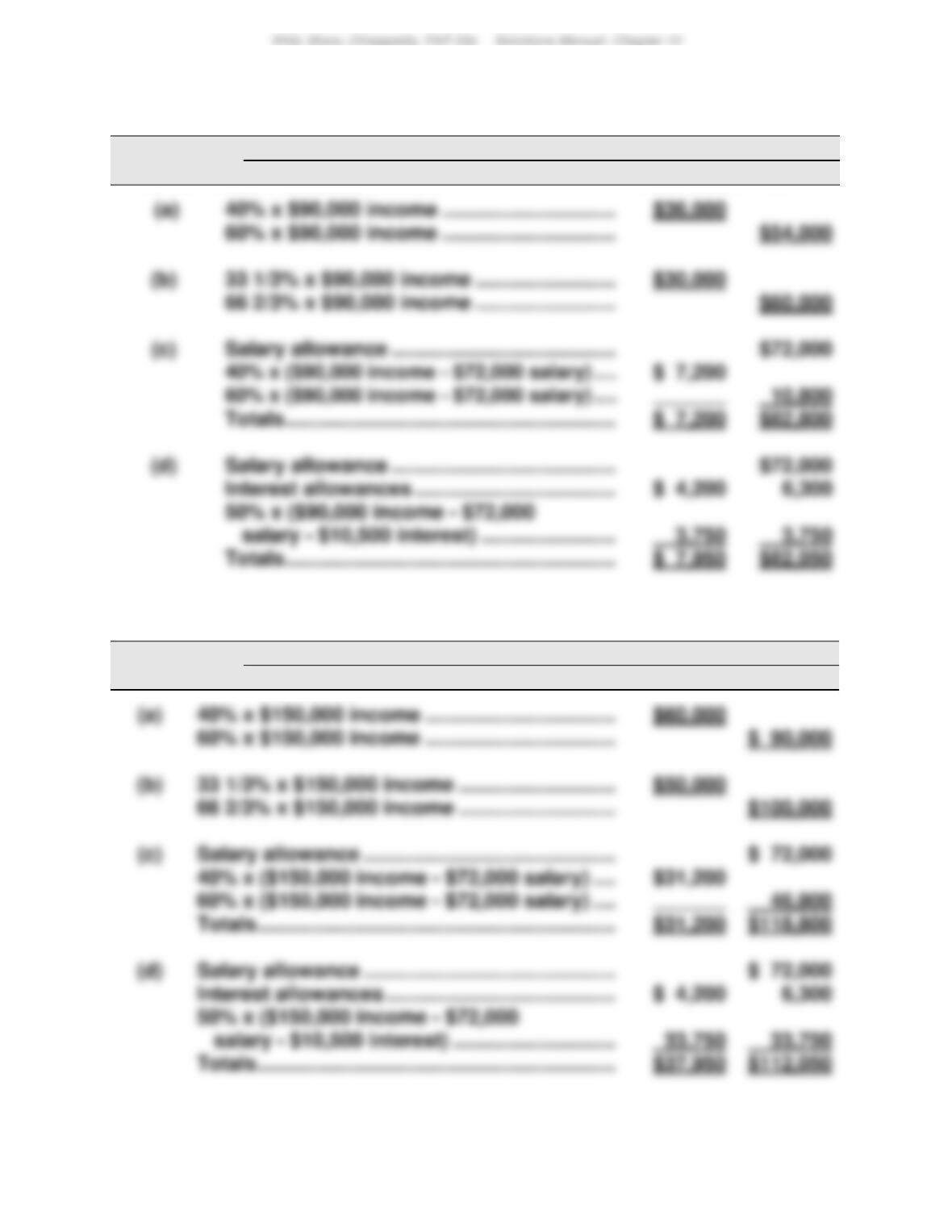

Problem 12-2A (45 minutes)

Preliminary calculations

Plan (a) & Plan (c)

Percentages based on initial investments

Lyon = $63,000/$105,000 = 60%

Plan (b)

Percentages based on time

Watts = 0.5/1.5 = 33 1/3%

Plan (c) & Plan (d)

Salary allowance

Lyon= 12 x $6,000 = $72,000

Watts = 10% x $42,000 = $ 4,200

Lyon= 10% x $63,000 = $ 6,300

Income (Loss)

Year 1

Sharing Plan

Calculations

Watts

Lyon

40% x $36,000 loss ……………………………………………

60% x $36,000 loss ……………………………………………

33 1/3% x $36,000 loss …………………………..

66 2/3% x $36,000 loss …………………………..

Salary allowance ………………………………………………

40% x ($36,000 loss + $72,000 salary) ………………..

60% x ($36,000 loss + $72,000 salary) ………………..

Totals ……………………………………………………….

Salary allowance ………………………………………………

Totals ……………………………………………………….

731

Problem 12-2A (Concluded)

Income (Loss)

Year 2

Sharing Plan

Calculations

Watts

Lyon

Income (Loss)

Year 3

Sharing Plan

Calculations

Watts

Lyon

732

Problem 12-3A (50 minutes)

1.

Dec. 31

Income Summary ……………………………………………..

249,000

2.

Dec. 31

Income Summary ……………………………………………..

249,000

3.

Dec. 31

Income Summary ……………………………………………..

249,000

733

Problem 12-4A (40 minutes)

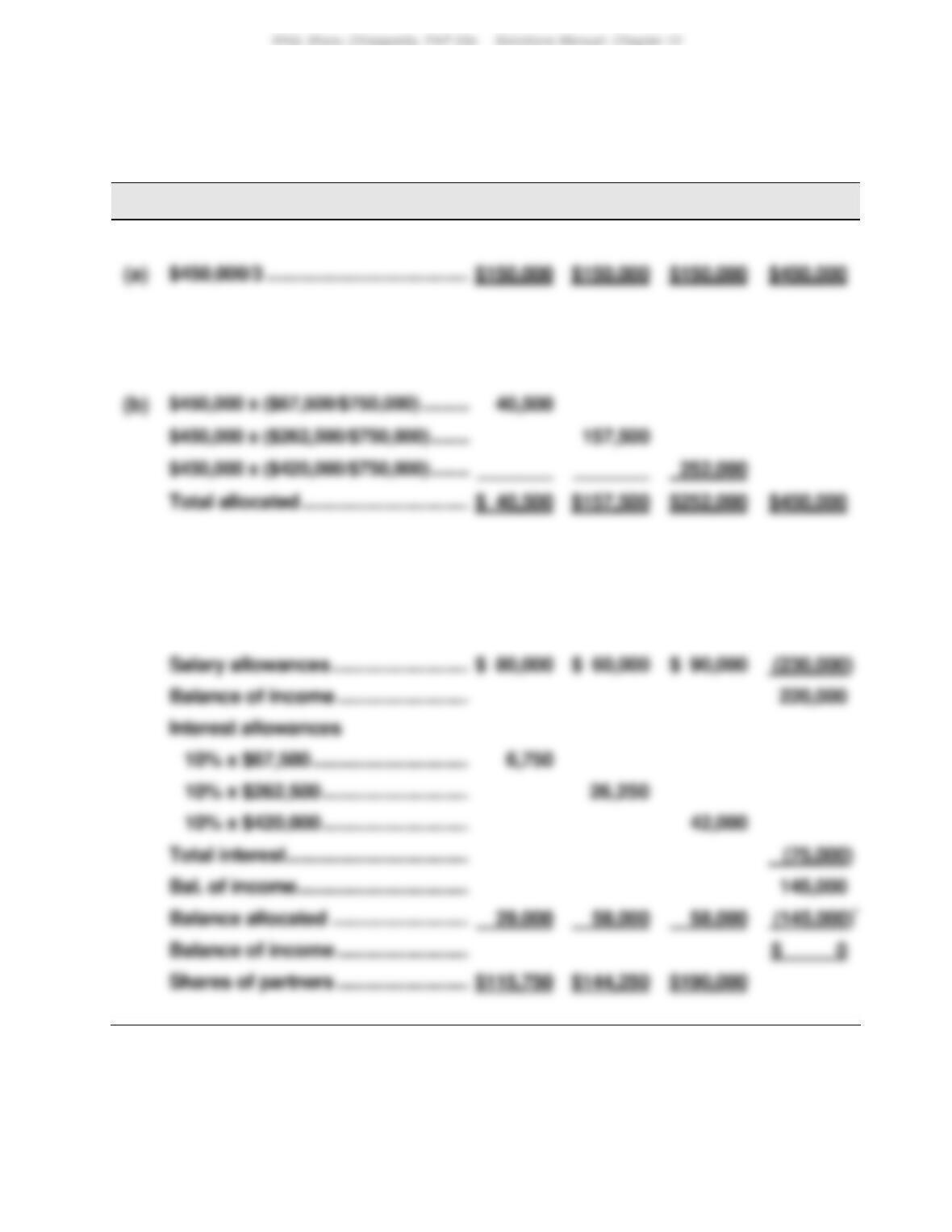

Part 1

Income (Loss)

Sharing Plan

Calculations

Mo

Lu

Barb

Total

(a)

$450,000/3 ……………………………………………………….

$450,000

Total allocated ……………………………………………………….

$450,000

(c)

Net income ……………………………………………………….

$450,000

734

Problem 12-4A (Concluded)

Part 2

MLB PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Mo

Lu

Barb

Total

Beginning capital balances …………..

$ 0

$ 0

$ 0

$ 0

Part 3

Dec. 31

Income Summary ……………………………………………..

209,000

Mo Meek, Capital ………………………………………………

Barb Beck, Capital …………………………………………….