363

CHAPTER 12

DIFFERENTIAL ANALYSIS AND

PRODUCT PRICING

CLASS DISCUSSION QUESTIONS

1. a. Differential revenue is the amount of

increase or decrease in revenue ex-

pected from a particular course of action

compared with an alternative.

2. This decision is an example of a make-or-buy

decision. Exabyte is focusing on its compara–

tive advantages, which include marketing and

distribution, while building partnerships with

others to actually manufacture key elements

of the product.

3. The differential income and costs of the

lease option should be compared against

selling the building. The differential revenue

4. Assuming there is demand for the premium-

grade product, this would assume the differ-

ential price (premium less commodity) ex-

ceeded the differential cost to process the

product to premium grade.

5. A business should only accept business at a

special price if the lower price will not con-

taminate the regular pricing for other cus-

offering discount business to a customer

that may wish to order in the future.

6. It would be reasonable to purchase from the

the profitability of the store, including all the

revenues, variable costs, and fixed costs

associated with the store, since they would

all be differential to the decision. In addition,

any costs of closing the store and preparing

the store for disposal would need to be con-

sidered (legal costs, demolition costs, em-

ployee severance costs). Lastly, the oppor-

tunity cost of the value of the equipment and

fixed and variable) and provide a reasonable

amount for profit.

9. The use of ideal standards might not allow

for such factors as normal spoilage or nor-

mal periods of idle time, with the result that

these costs might not be covered by the

product price. In such cases, the product

price could be too low to earn a desired prof-

364

12. The target cost concept begins with a price

that can be sustained in the marketplace,

then subtracts a target profit, thus determin-

ing the target cost. The cost is made to con-

14. A production bottleneck is a point in the

production process where demand exceeds

the ability to produce (i.e., the segment is

operating at full capacity). As a result, the

365

EXERCISES

E12–1

a. YAMADA INDUSTRIES

Proposal to Lease or Sell Machinery

Differential revenue from alternatives:

E12–2

a. COLA BEVERAGES INC.

Proposal to Discontinue Kiwi Cola

Differential revenue from annual sales of Kiwi Cola:

Revenue from sales ……………………………………………… $4,000,000

Differential cost of annual sales of Kiwi Cola:

Variable cost of goods sold ………………………………….. $1,905,000*

366

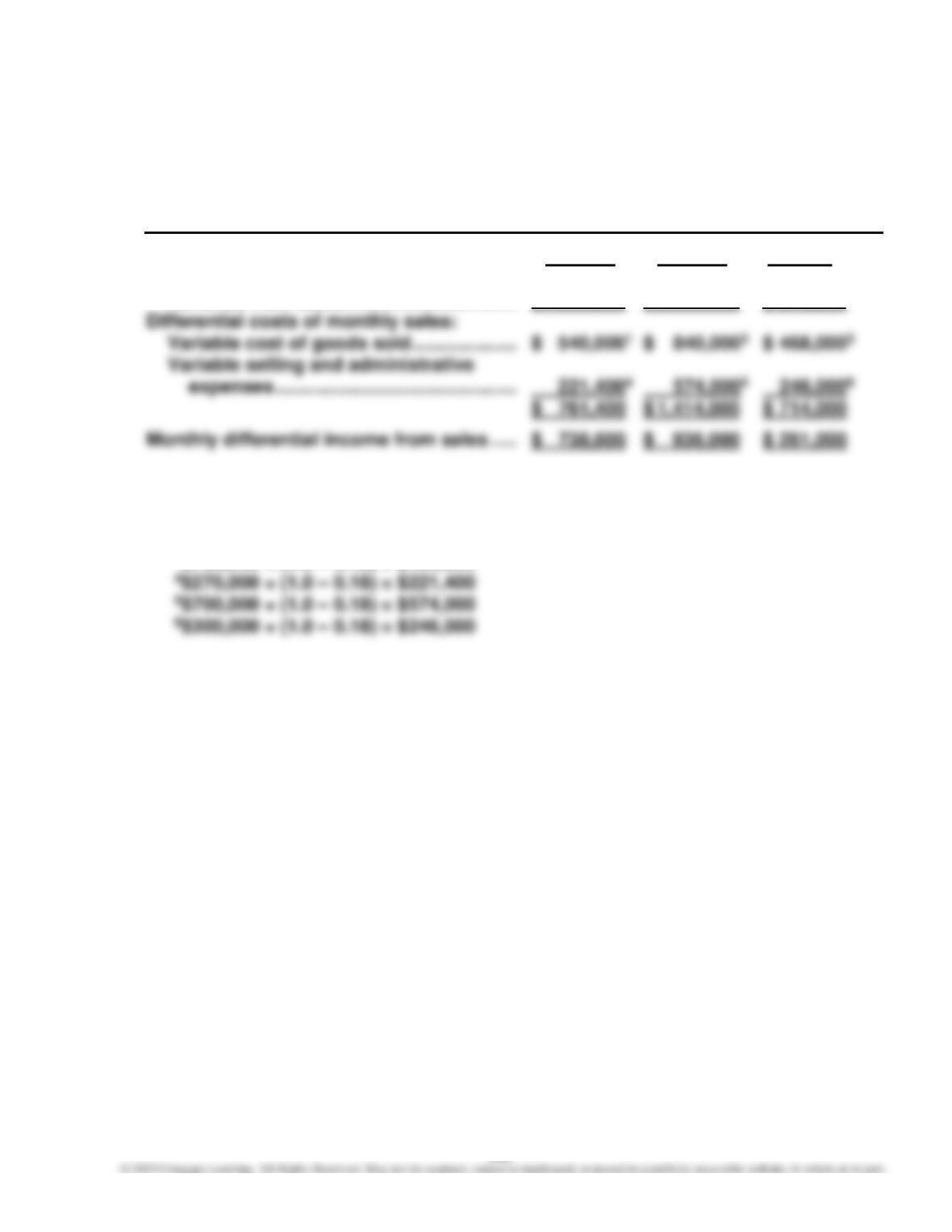

E12–3

a.

DINNER WARE COMPANY

Differential Product Analysis Report

Bowls Plates Cups

Differential revenue from monthly sales:

Revenue from sales …………………………... $ 1,500,000 $ 2,350,000 $ 975,000

Computations:

1$900,000 × (1.0 – 0.40) = $540,000

2$1,400,000 × (1.0 – 0.40) = $840,000

3$780,000 × (1.0 – 0.40) = $468,000

b. The Cups line should be retained. As indicated by the differential analysis in part

(a), the income would decrease by $261,000 (excess of differential revenue over

differential cost) if the Cups line is discontinued.

367

E12–4

Note to Instructors: Many students may be unfamiliar with the financial services in-

dustry. This exercise provides an opportunity to introduce students to some basic

terms and concepts used within the industry.

a. The “Individual Investor” segment serves the retail customer, you and me. These

b. Variable costs in the “Individual Investor” segment include:

1. Commissions to brokers

2. Fees paid to exchanges for executing trades

c.

Individual Institutional

Investor Investor

Income from operations before taxes …….. $ 928 $463

Plus depreciation and amortization ……….. 108 47

Estimated contribution margin ………………. $1,036 $510

368

E12–5

The flaw in the decision was the failure to focus on the differential revenues and costs,

which indicate that operating income would be reduced by $85,000 if Children’s San-

dals is discontinued. This differential income from sales of Children’s Sandals can be

determined as follows:

Differential revenue from annual sales of Children’s

Sandals:

E12–6

a. BALBOA TECHNOLOGIES COMPANY

Proposal to Manufacture Carrying Case

Purchase price of carrying case ……………………………. $20.00

Differential cost to manufacture carrying case:

Direct materials …………………………………………………. $9.00

369

E12–7

a. WISCONSIN ARTS OF MILWAUKEE

Proposal to Purchase Outside Page Layout Services

Differential revenue:

Salvage of computer equipment …………………………... $ 6,500

Differential expenses:

Purchase price of layout work:

Number of pages ……………………………………………… 30,000

b. The benefit from using an outside service is shown to be $91,500 greater than per-

forming the layout work internally. The fixed costs (depreciation expenses) in the

budget are irrelevant to the decision. Thus, the work should be purchased from

the outside on a strictly financial basis. In addition, the decision to purchase from

the outside would be further favored if the need for administrative expansion

space were great. If more administrative space were needed immediately, then any

avoided lease costs would become a differential benefit to the decision to out-

source.

370

E12–8

a. Annual variable costs—present equipment ……………. $ 75,000

Annual variable costs—new equipment…………………. 39,000

Annual differential decrease in cost ………………………. $ 36,000

b. The sunk cost is the $235,000 book value ($350,000 cost less $115,000 accumulat-

ed depreciation) of the present equipment. The original cost and accumulated de-

preciation were incurred in the past and are irrelevant to the decision to replace

the machine.

371

E12–9

a. SIDNEY TECHNOLOGIES

Proposal to Replace Machine

Annual costs and expenses—present machine …………………………. $267,000

Annual costs and expenses—new machine ………………………………. 227,000

Annual differential decrease in costs and expenses ………………….. $ 40,000*

Number of years applicable ……………………………………………………… × 5

Total differential decrease in costs and expenses ……………………… $200,000

b. The proposal should not be accepted.

c. In addition to the factors given, consideration should be given to such factors as:

Do both present and proposed operations provide the same capacity? What are

E12–10

a. Differential revenue: $520 – $400 = $120

b. Differential cost: $360 – $275 = $85

372

E12–11

a. SPOKANE COFFEE COMPANY

Proposal to Process Columbian Coffee Further

Differential revenue from further processing per batch:

Revenue from sale of Decaf Columbian [(5,000

pounds – 400* pounds evaporation) × $12.50] …………… $ 57,500

b. The differential revenue from processing further to Decaf Columbian is less than

the differential cost of processing further. Thus, Spokane Coffee Company should

sell Columbian coffee and not process further to Decaf Columbian.

c. The price of Decaf Columbian would need to increase to $12.85 per pound in order

for the differential analysis to yield neither an advantage nor a disadvantage (indif-

ference). This is determined as follows:

(5,000 pounds × $9.00) …………………………………………….. 45,000

Differential revenue ………………………………………………………… $ 14,110

Differential cost per batch:

Additional cost of producing Decaf Columbian …………….. 14,110

Differential income from further processing:

Decaf Columbian per batch …………………………………………. $ 0

373

E12–12

a. TOSCA INDUSTRIES INC.

Proposal to Sell to DynaX Company

Differential revenue from accepting the offer:

Revenue from sale of 50,000 additional units at $32 ……………… $1,600,000

Differential cost of accepting the offer:

Variable costs from sale of 50,000 additional units at $29 ……… 1,450,000

Differential income from accepting the offer ……………………………… $ 150,000

E12–13

a.

Budgeted cost per battery for June = Total manufacturing costs ÷ Budgeted pro-

duction

Budgeted cost per battery for June = $1,434,000 ÷ 60,000 batteries = $23.90 per

battery

374

E12–14

a. MIRAMAR TIRE AND RUBBER COMPANY

Proposal to Sell to Rio Motors

Per Unit Total

Differential revenue from accepting special offer …. $20.00 $800,000*

Differential costs from accepting special offer:

Direct materials ……………………………………………….. $10.00

Direct labor……………………………………………………… 5.00

*$20 × 40,000 tires = $800,000

**4% × $40. The avoided sales commission should not be computed on the basis

of the $20 price to Rio Motors, but on the existing domestic sales price of $40.

***$18.95 × 40,000 tires = $758,000

b.

tires 40,000

$778,000

= $19.45

or

375

E12–15

a. $3,000,000 ($15,000,000 × 20%)

b. Total costs:

Variable ($465 × 100,000 units) …………………………………………….. $46,500,000

Fixed ($2,400,000 + $1,100,000)…………………………………………….. 3,500,000

Total ………………………………………………………………………………………… $50,000,000

Cost amount per unit: $50,000,000 ÷ 100,000 units = $500.00

E12–16

a. Total manufacturing costs:

Variable ($420 × 100,000 units) …………………………………………….. $42,000,000

Fixed factory overhead ………………………………………………………… 2,400,000

Total ………………………………………………………………………………………… $44,400,000

Cost amount per unit: $44,400,000 ÷ 100,000 units = $444.00

c. Cost amount per unit………………………………………………………………… $444

Markup ($444.00 × 19.37%) ……………………………………………………….. 86

Selling price …………………………………………………………………………….. $530

376

E12–17

a. Total variable costs: $465 × 100,000 units …………………………………. $46,500,000

c. Cost amount per unit………………………………………………………………… $465

Markup ($465 × 13.98%) ……………………………………………………………. 65

Selling price …………………………………………………………………………….. $530

E12–18

a. The price will be set at the estimated average market price required to remain

competitive, or $24,000. Under the target cost concept, the market dictates the

price, not the markup on cost.

b. The required profit margin of 20% of the estimated $24,000 price implies a $17,600

target product cost as follows:

377

E12–19

a. Historical markup percentage on product cost:

$160

$160 –– $200

= 25% or

b. Required cost reduction: $160.00 – $145.60 = $14.40

c.

1. Direct labor reduction:

min. 60

min. 6

× $20 =

$ 2.00

2. Additional inspection:

min. 60

min. 9

× $20 =

$(3.00)

378

E12–20

Determine the contribution margin per furnace hour as follows:

Type A1 Type B3 Type E6

Revenue ………………………………………………. $ 400,000 $ 578,000 $ 300,000

Variable cost ………………………………………… 250,000 380,000 270,000

Contribution margin ……………………………… $ 150,000 $ 198,000 $ 30,000