CHAPTER 12

UNDERSTANDING THE ISSUES

1. Viewing an interim period as an integral

part of a larger annual period has several

benefits. The allocation of expense under

this viewpoint provides information that al-

2. A number of factors are necessary in order

to determine the estimated effective annual

tax rate. First of all, the rate should reflect

conditions to be experienced for the entire

year. Therefore, in addition to year-to-date

pretax income/loss, such amounts must be

projected for the balance of the year. Statu-

tory tax rates are applied to these annual

amounts after considering the presence of

possible annual permanent differences

tax credit carrybacks and carryforwards.

3. Several factors may explain this situation. If

the third-quarter loss were greater than the

to the loss may not be recognized. How-

ever, if this were the case, one would

consider any known pretax income in the

carryback period and any “more likely than

tax income in the carryforward period.

4. There are a number of reasons why the

total operating profit of the reportable seg-

ments does not normally equal the consoli-

dated operating profit. First of all, not all

operating segments are reportable and yet

such amounts are included in consolidated

amounts. Second, there are a number of

intersegment transactions whose effect

luating segment performance and/or

because allocation is not possible on a rea-

sonable basis. Finally, the accounting

Ch. 12—Exercises 12–2

EXERCISES

EXERCISE 12-1

(1) Generally speaking, research and development (R&D) costs are expensed in the year in

which they are incurred. Therefore, absent contrary evidence, all of the $360,000 of costs

(2) A likely explanation for an effective tax rate less than the statutory rate is that there are dif-

ferences between how items of revenue and/or expense are recognized for tax purposes

(3) If the tax benefit associated with the net operating loss in the prior year was not fully recog-

nized in the year of loss, it is possible that an additional amount of benefit traceable to the

(4) In order to estimate the annual effective tax rate applicable to an interim period, it is neces-

sary to estimate the amount of annual taxable income. Therefore, the estimated amount of

(5) The effective tax rate for the first quarter of the current year suggests several things. First,

not all of the estimated current-year tax loss could be carried back against the prior two

years. If this had been the case, the effective tax rate would have been at least 25%.

Exercise 12-1, Concluded

(6) If the current year-to-date LIFO liquidation will not exist at year-end because it is estimated

that current-year purchases will exceed current-year sales, then the interim cost of sales

EXERCISE 12-2

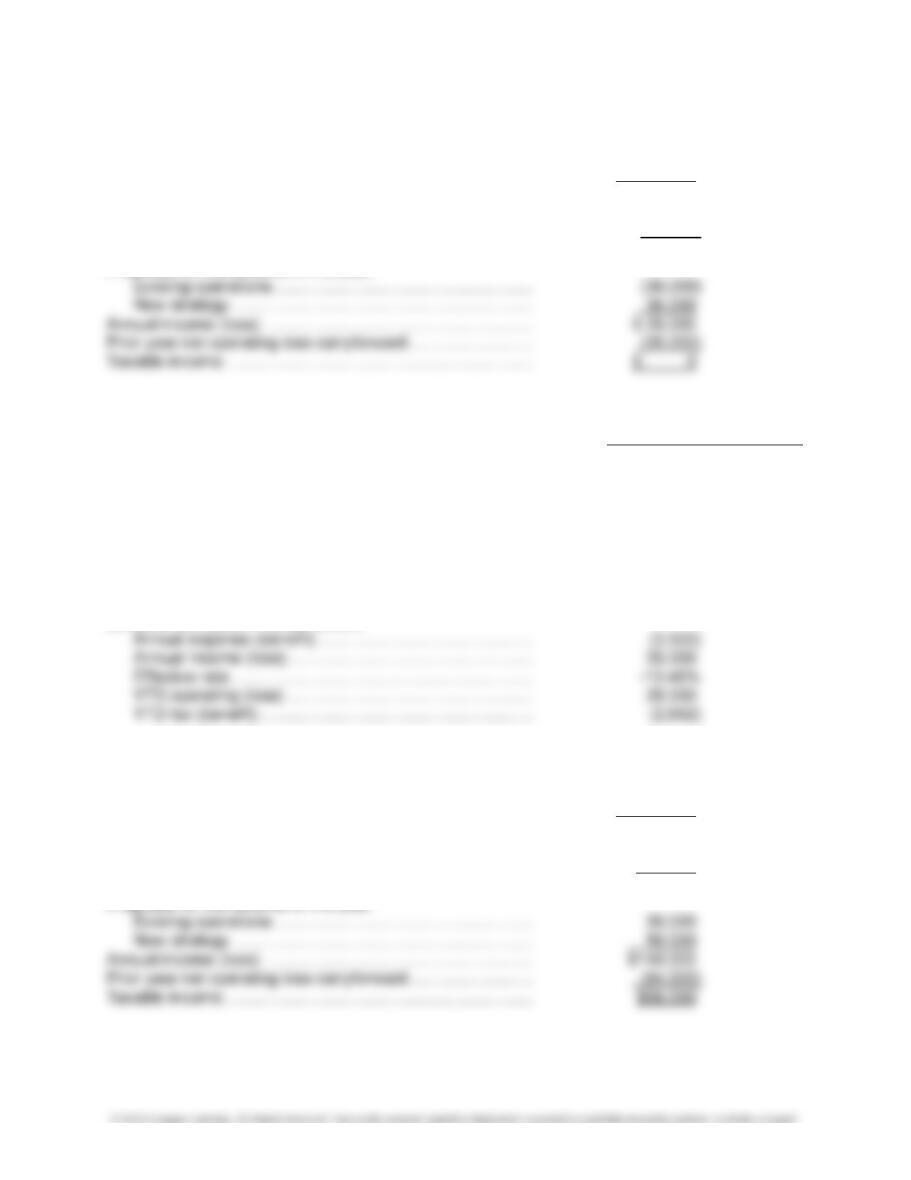

Strategy A

Quarter 2

2015

YTD income (loss):

Existing operations ………………………………………………… $60,000

New strategy ………………………………………………………… (85,000)

Subtotal ……………………………………………………………….. (25,000)

Projected for the balance of the year:

2015 2014

DR (CR) CR (DR)

Annual entry:

Taxes receivable (payable) ……………………………………..

Deferred tax asset (15% x $40 K) ……………………………. 6,000

Deferred tax asset …………………………………………………. 4,000

Tax expense (benefit) ……………………………………………. (4,000) (6,000)

Note: The deferred tax asset balance is $10,000 (15% × $50K + 25% × $10 K)

Ch. 12—Exercises 12–4

Strategy B

Quarter 2

2015

YTD income (loss):

Existing operations ………………………………………………… $60,000

New strategy ………………………………………………………… (40,000)

Subtotal ……………………………………………………………….. 20,000

Projected for the balance of the year:

2015 2014

DR(CR) CR(DR)

Annual entry:

Taxes receivable (payable) ……………………………………..

Deferred tax asset (15% x $40 K) ……………………………. 6,000

Deferred tax asset …………………………………………………. 3,500

Tax expense (benefit) ……………………………………………. (3,500) (6,000)

Note: The deferred tax asset balance is $9,500 (15% × $50K + 25% × $8 K) represented by the

remaining $58 K ($84 K – $26 K) of 2014 loss

Effective tax rate & YTD tax benefit:

Strategy C

Quarter 2

2015

YTD income (loss):

Existing operations ………………………………………………… $60,000

New strategy …………………………………………………………

Subtotal ……………………………………………………………….. 60,000

Projected for the balance of the year:

12–5 Ch. 12—Exercises

2015 2014

DR(CR) CR(DR)

Annual entry:

Taxes receivable (payable) …………………………………….. (4,000)

(15% x $50 K + 25% x $6 – $5 tax credit)

Deferred tax asset (15% x $40 K) ……………………………. 6,000

Note: That there is no longer a deferred tax balance because all of the $84,000 prior year loss

has been used against current year income.

Effective tax rate & YTD tax benefit:

Annual expense (benefit) ……………………………………….. 10,000

The estimated tax expense of $10,000 can also be calculated as follows:

The tax expense on $140,000 after the tax credit would be:

$50,000 at 15% …………………………………………………….. $7,500

The $84,000 prior year operating loss had additional benefit of:

$40,000 at 30% …………………………………………………….. 12,500

$44,000 at 25% …………………………………………………….. 11,000

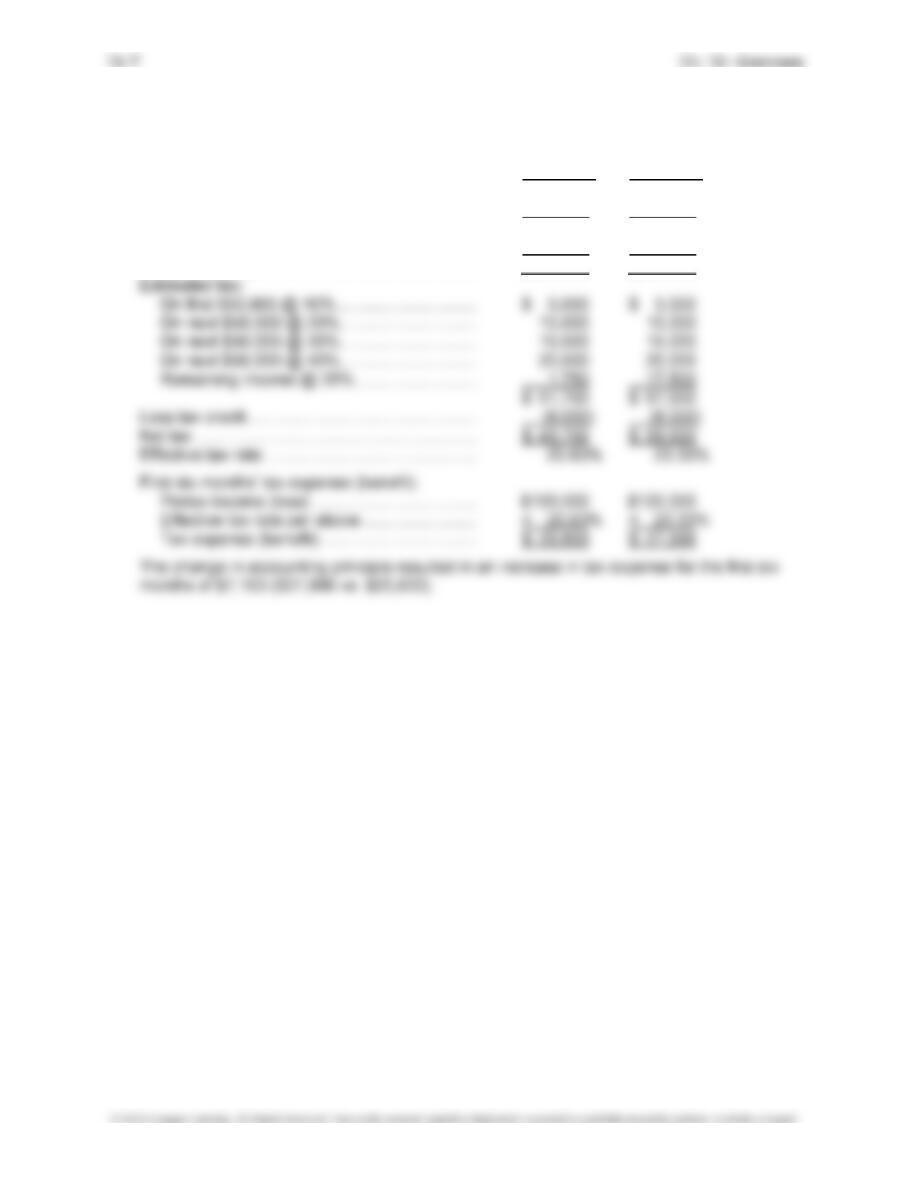

EXERCISE 12-3

Granger Supply, Inc.

Interim Income Statements

For the Periods Ending Quarter 1 and 2 of the Current Year

Quarter 1

Quarter 2

Net sales …………………………………………………………………… $12,000,000 $9,000,000

Cost of sales (See Schedule A) ……………………………………. 7,900,000 7,805,000

Gross profit ……………………………………………………………….. $ 4,100,000 $1,195,000

Schedule A—Cost of Sales

Quarter 1

Quarter 2

As stated:

Cost of sales—industrial supplies ……………………………. $4,300,000 $4,700,000

Cost of sales—cleaning equipment ………………………….. 3,000,000 3,200,000

Adjustment for replacement cost:

Schedule B—Income Tax Schedule

Quarter 1

Quarter 2

YTD income before tax ……………………………………………….. $2,000,000 $1,395,000

Projected income ……………………………………………………….. 5,100,000 4,000,000

Estimated annual income …………………………………………….. $7,100,000 $5,395,000

Ordinary Pretax Income (Loss) Tax Expense (Benefit)

Interim Current Effective Tax Previously Current

EXERCISE 12-4

(1) Before After

Change

Change

YTD income (loss) …………………………………….. $100,000 $120,000

Projected income (loss) ……………………………… 110,000 135,000

Total annual ……………………………………………… $210,000 $255,000

Less exempt income ………………………………….. (5,000) (5,000)

Taxable income ………………………………………… $205,000 $250,000

(2) Total Total

Excluding Excluding

Ordinary Total Nonordinary Nonordinary

Income

Income Loss Gain

First six months continuing ……….. $120,000 $120,000 $120,000 $120,000

Third quarter continuing ……………. 80,000 80,000 80,000 80,000

Projected continuing ………………… 20,000 20,000 20,000 20,000

Incremental tax expense (benefit) traceable to:

All nonordinary items ($57,600 – $50,600) …………………….. $ 7,000

All nonordinary losses ($71,600 – $57,600) ……………………. $ (14,000)

All nonordinary gains [$7,000 – ($14,000)] …………………….. $ 21,000

Taxable income:

Pretax accounting income …….. $220,000 $240,000 $280,000 $180,000

Less exempt income ……………. (4,000) (4,000) (4,000) (4,000)

12–9 Ch. 12—Exercises

EXERCISE 12-5

Tax rates 30% 25% 15%

Case A 2015 2014 2013

YTD income (loss) ……………………………………………….. $ (80,000)

Projected for the balance of the year ……………………….. 120,000

Effective rate ………………………………………………………… 26.25%

YTD operating (loss) …………………………………………….. (80,000)

YTD tax (benefit) ………………………………………………….. (21,000)

Case B 2015 2014 2013

YTD income (loss) ……………………………………………….. $ (80,000)

Annual income (loss) ……………………………………………. (80,000)

Effective rate ………………………………………………………… 8.13%

YTD operating (loss) …………………………………………….. (80,000)

YTD tax (benefit) ………………………………………………….. (6,500)

Ch. 12—Exercises 12–10

Deferred tax asset (30% x $20 K) …………………………… 3,500

Tax expense (benefit) …………………………………………… (3,500) (2,500)

NOTE: The deferred tax asset at year-end 2015 is

$6,000.

Effective tax rate & YTD tax benefit:

Loss carryback to prior 2 years ……………………………….. 30,000

Taxable income …………………………………………………….. $(60,000) $ (10,000) $30,000

Annual entry: DR (CR) DR (CR) DR (CR)

Taxes receivable (payable) ………………………………. 4,500 (4,500)

Deferred tax asset (25% x $5 K) ……………………….. 1,250

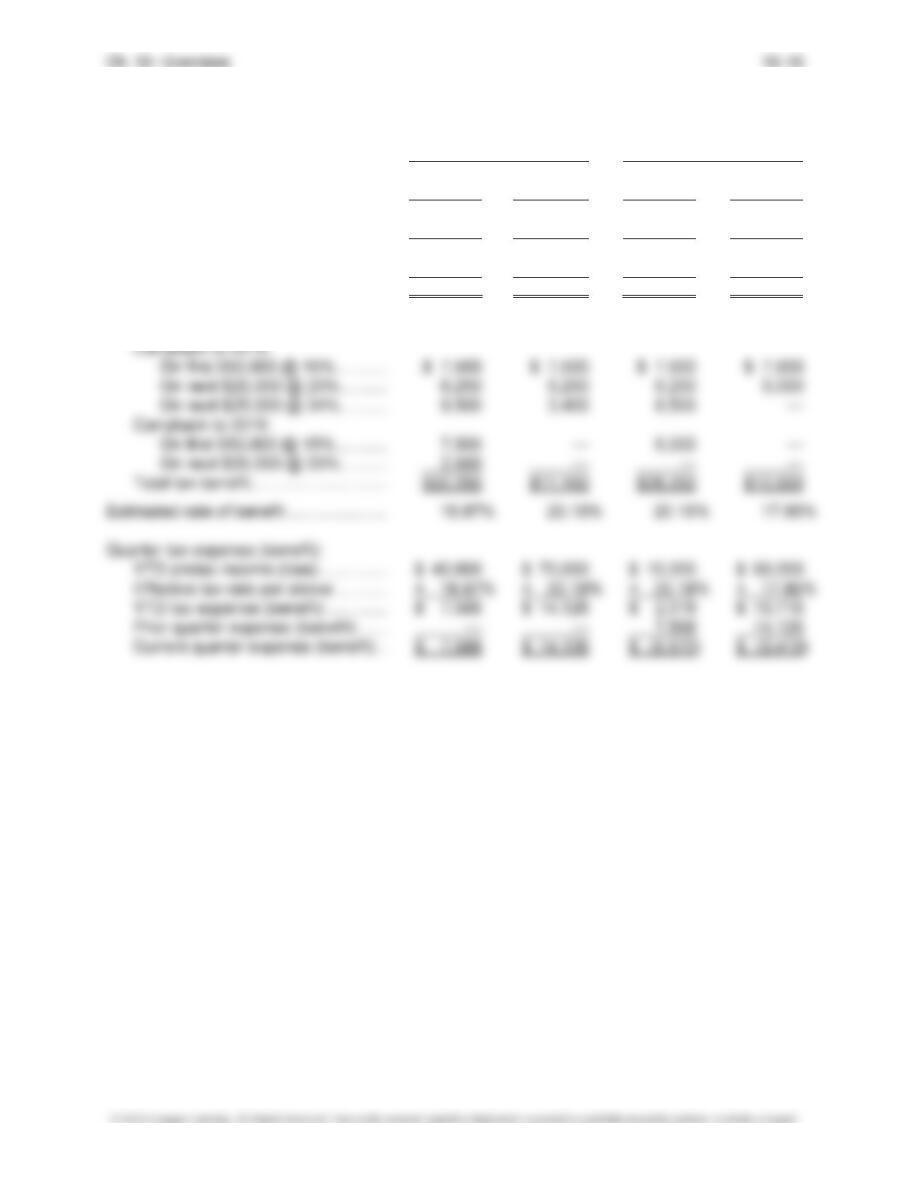

EXERCISE 12-6

Quarter 1

Quarter 2

Originally

Stated

Continuing Discontinued Continuing Discontinued

YTD pretax income (loss) ……………………….. $ 800,000 $1,020,000 $(220,000) $1,545,000 $(700,000)

Projected pretax income (loss) ………………… 1,100,000 1,420,000 (320,000) 1,050,000 —

Estimated annual income ………………………… $1,900,000 $2,440,000 $(540,000) $2,595,000 $(700,000)

Pretax Income (Loss) Tax Expense (Benefit)

Type of Current Effective Previously Current

Interim Quarter Income Period Year-to-Date Tax Rate Year-to-Date Reported Period

First Continuing Op. $ 800,000 $ 800,000 29.50% $ 236,000 $ — $ 236,000

First—Restated Continuing Op. 1,020,000 1,020,000 30.72% 313,344 — 313,344

First—Restated Discontinued (220,000) (220,000) Note A (77,344) — (77,344)

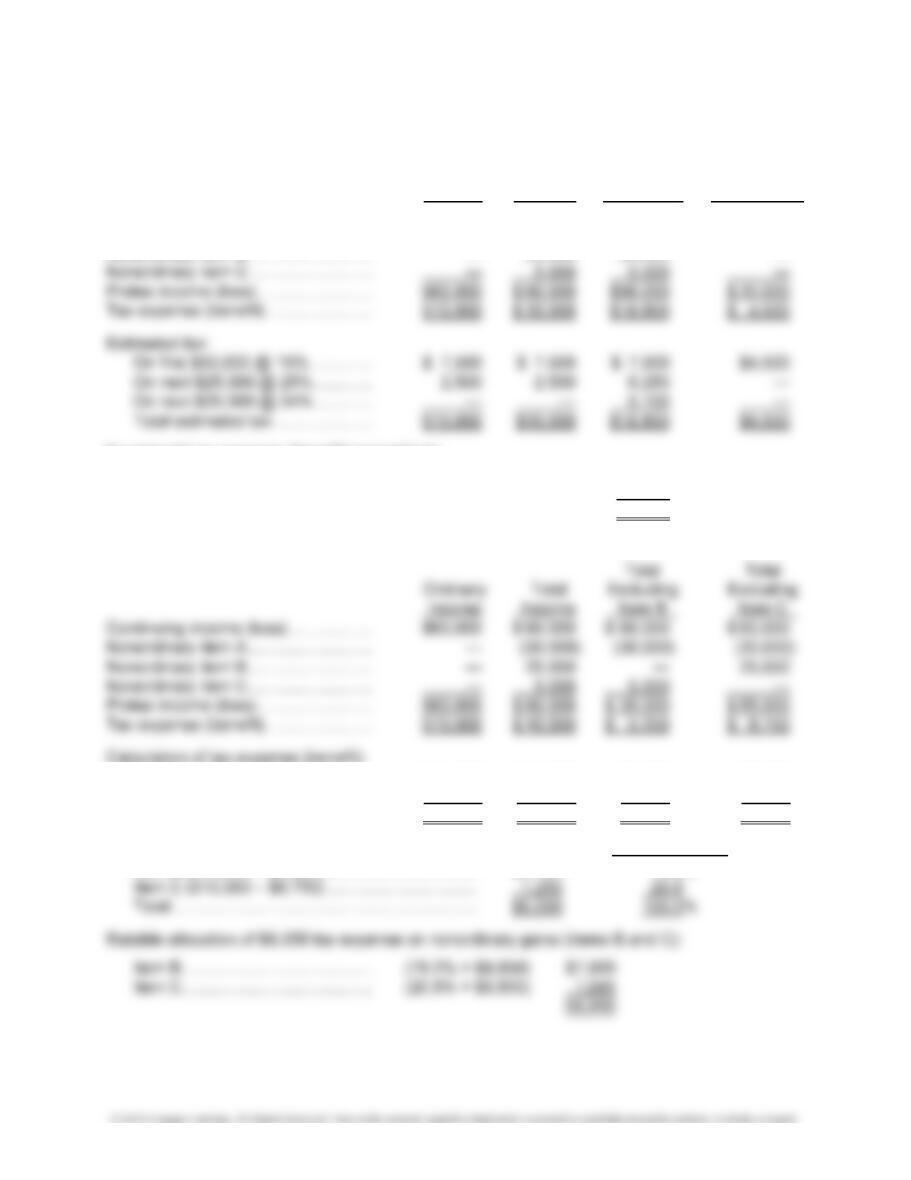

EXERCISE 12-7

Quarter 1, 2017 Quarter 2, 2017

Before After Before After

Change

Change Change Change

First-quarter income (loss) ………………. $ 40,000 $ 70,000 $ 40,000 $ 70,000

Second-quarter income (loss) ………….. — — (30,000) (10,000)

YTD income (loss) …………………………. $ 40,000 $ 70,000 $ 10,000 $ 60,000

Projected income (loss) ………………….. (210,000) (155,000) (150,000) (130,000)

Total annual ………………………………….. $(170,000) $ (85,000) $(140,000) $ (70,000)

Estimated tax benefit:

12–13 Ch. 12—Exercises

EXERCISE 12-8

Total Total

Excluding Excluding

Ordinary Total Nonordinary Nonordinary

Income Income Loss (A) Gain (B & C)

Continuing income (loss) ……………… $60,000 $ 60,000 $60,000 $ 60,000

Nonordinary item A ……………………… — (30,000) — (30,000)

Nonordinary item B ……………………… — 25,000 25,000 —

Incremental tax expense (benefit) traceable to:

All nonordinary items ($10,000 – $10,000) ………………………….. $ 0

All nonordinary losses ($10,000 – $18,850) …………………………. (8,850)

All nonordinary gains [$0 – ($8,850)] ………………………………….. $ 8,850

On first $50,000 @ 15% ………….. $ 7,500 $ 7,500 $5,250 $7,500

On next $25,000 @ 25% …………. 2,500 2,500 — 1,250

Total estimated tax …………………. $10,000 $10,000 $5,250 $8,750

Incremental tax expense (benefit) traceable to: Percent of Total

Item B ($10,000 – $5,250) …………………………… $4,750 79.2%

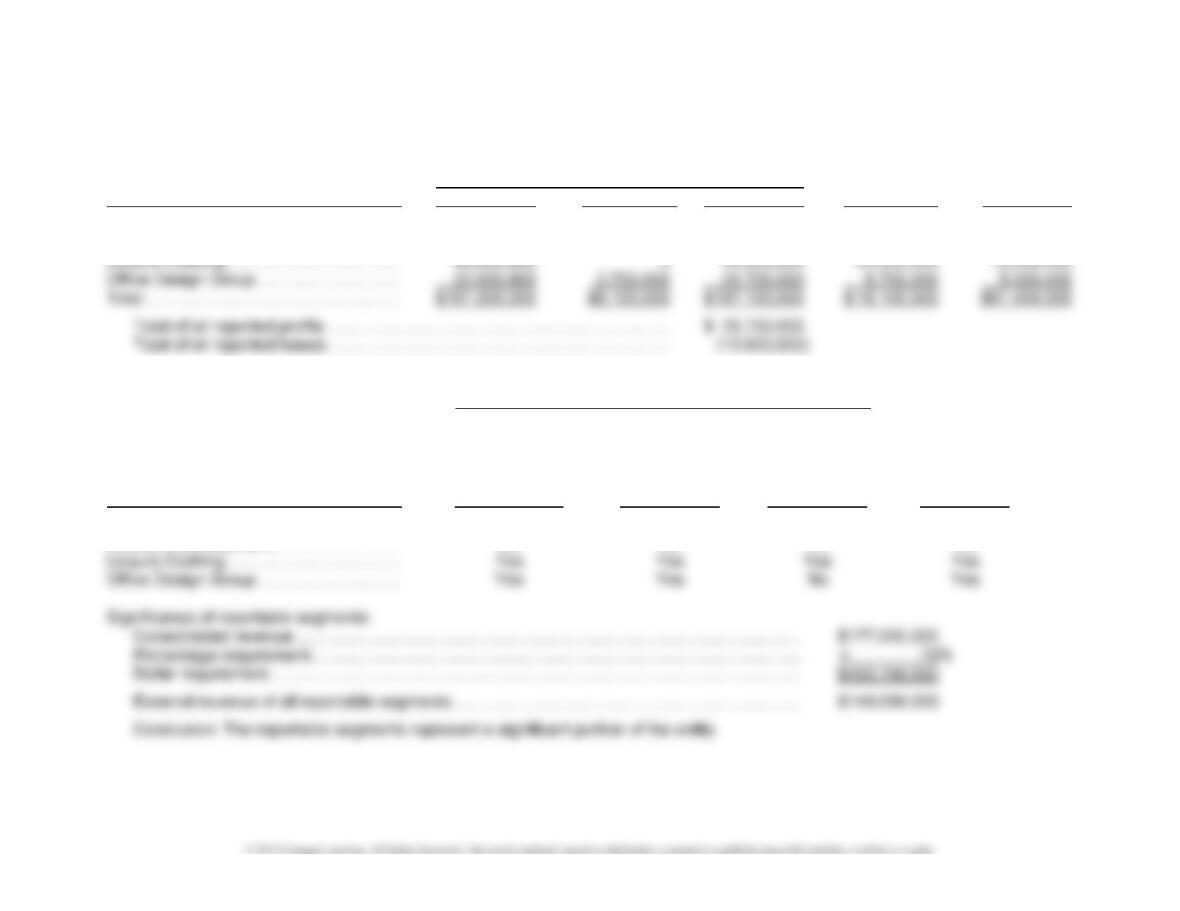

EXERCISE 12-9

(1) It seems most likely that the area of oils and lubricants could be combined with the distribu-

tion of specialized tools. Both areas share a number of similarities including serving the

(2) Determination of whether segments are reportable:

Is Segment’s

Absolute

Value of

Revenue Profit/Loss Assets Is

10% or More of 10% or More of 10% or More of Segment

Segment $30,750,000? $4,514,200? $32,660,000? Reportable?

(3) Items that may comprise the reconciliation of segment totals to companywide totals may

include the following:

• Not all segments are reportable.

• Corporate-level components of other income such as interest income, extraordinary

12–15 Ch. 12—Exercises

EXERCISE 12-10

Determination of whether segments are reportable:

Revenues

Reported

Segment External Intersegment Total Profit (Loss) Assets

Film Studios …………………………………….. $ 82,000,000 $ 0 $ 82,000,000 $(11,000,000) $38,000,000

Software Development ………………………. 12,000,000 3,400,000 15,400,000 (2,600,000) 5,400,000

Is Segment’s

Absolute Value

Revenue of Profit or Assets

10% or Loss 10% or 10% or

More of More of More of Is Segment

Segment $167,100,000? $29,700,000? $61,400,000? Reportable?

Film Studios …………………………………….. Yes Yes Yes Yes

Software Development ………………………. No No No No

Ch. 12—Problems 12–16

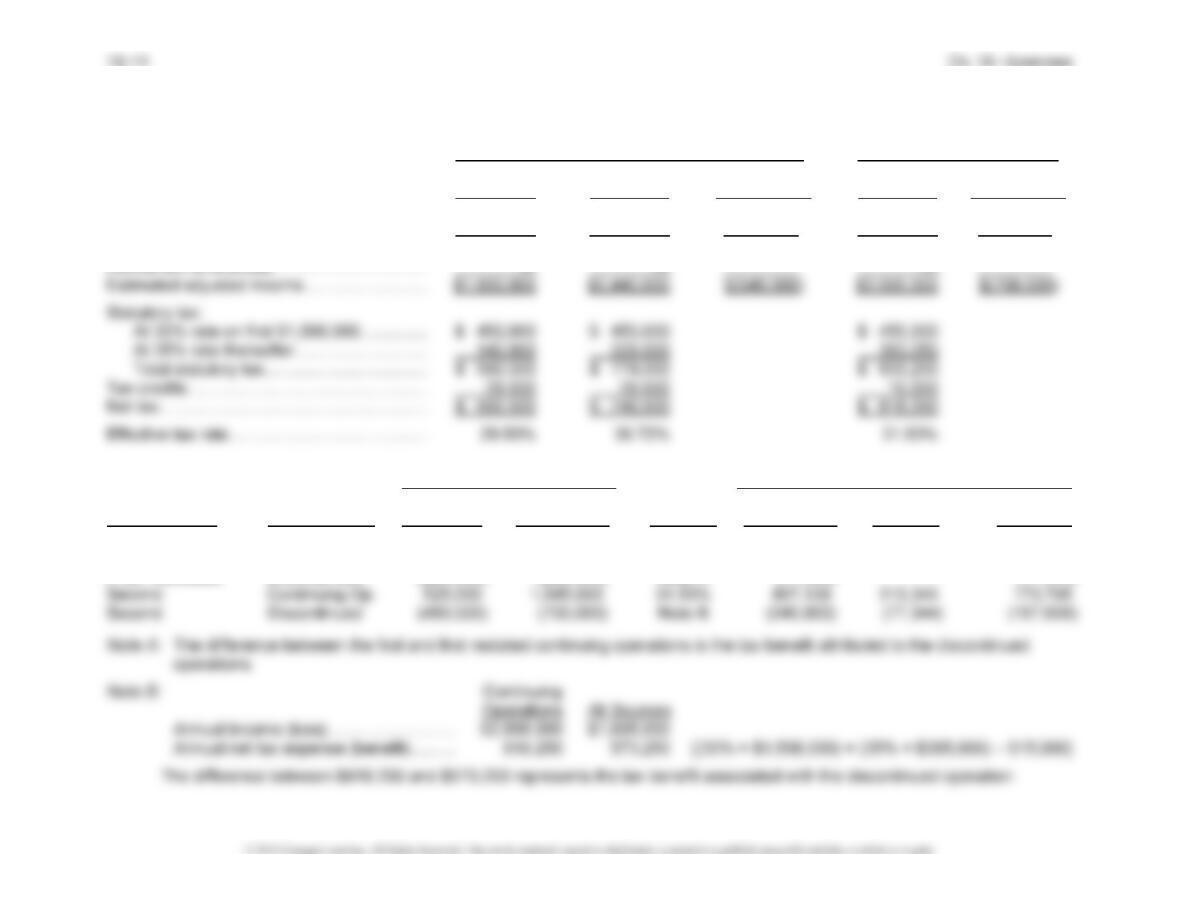

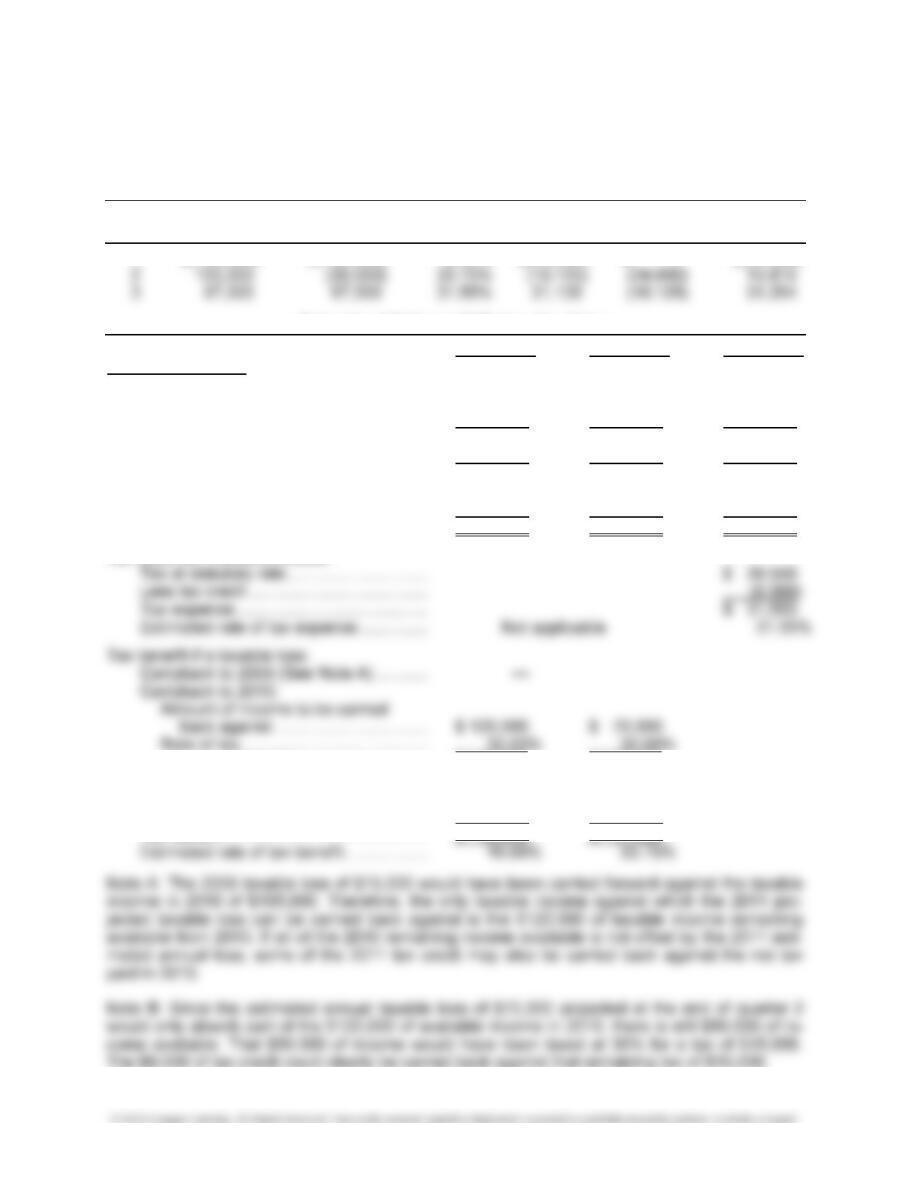

PROBLEMS

PROBLEM 12-1

Pretax Income (Loss) Tax Expense (Benefit)

Current Year-to- Effective Year-to- Previously Current

Quarter Period Date Tax Rate Date Reported Period

1 $(150,000) $(150,000) 16.00% $(24,000) $ — $(24,000)

Schedule of Estimated Effective Tax Rates

Quarter 1 Quarter 2 Quarter 3

YTD income (loss):

First quarter ……………………………………. $(150,000) $(150,000) $(150,000)

Second quarter ……………………………….. 120,000 120,000

Third quarter …………………………………… — 97,000

Total ………………………………………………. $(150,000) $ (30,000) $ 67,000

Projected income (loss) ………………………….. (75,000) (50,000) 33,000

Total annual income (loss) ………………………. $(225,000) $ (80,000) $ 100,000

Plus nondeductible expenses ………………….. 22,000 15,000 20,000

Less nontaxable income …………………………. — (5,000) (7,000)

Taxable income (loss) …………………………….. $(203,000) $ (70,000) $ 113,000

Tax expense if taxable income:

Amount of benefit ………………………… $ 36,000 $ 21,000

Plus tax credit carryback:

Carryback to 2009 ……………………….. — —

Carryback to 2010 (Note B) ………….. — 6,000

Tax benefit ……………………………………… $ 36,000 $ 27,000

PROBLEM 12-2

Quarter 1 Quarter 1 Quarter 1 Quarter 2 Quarter 3

Original

Continuing DISCO Continuing Continuing

YTD income ……………………………………………….. $(45,000) $(30,000) $(15,000) $28,000 $ 68,000

Projected income ………………………………………… (25,000) 15,000 (40,000) 62,000 42,000

Pretax Income (Loss) Tax Expense (Benefit)

Interim Period Type of Current Year- Effective Year- Previously Current

(quarter) Income Period to-Date Tax Rate to-Date Reported Period

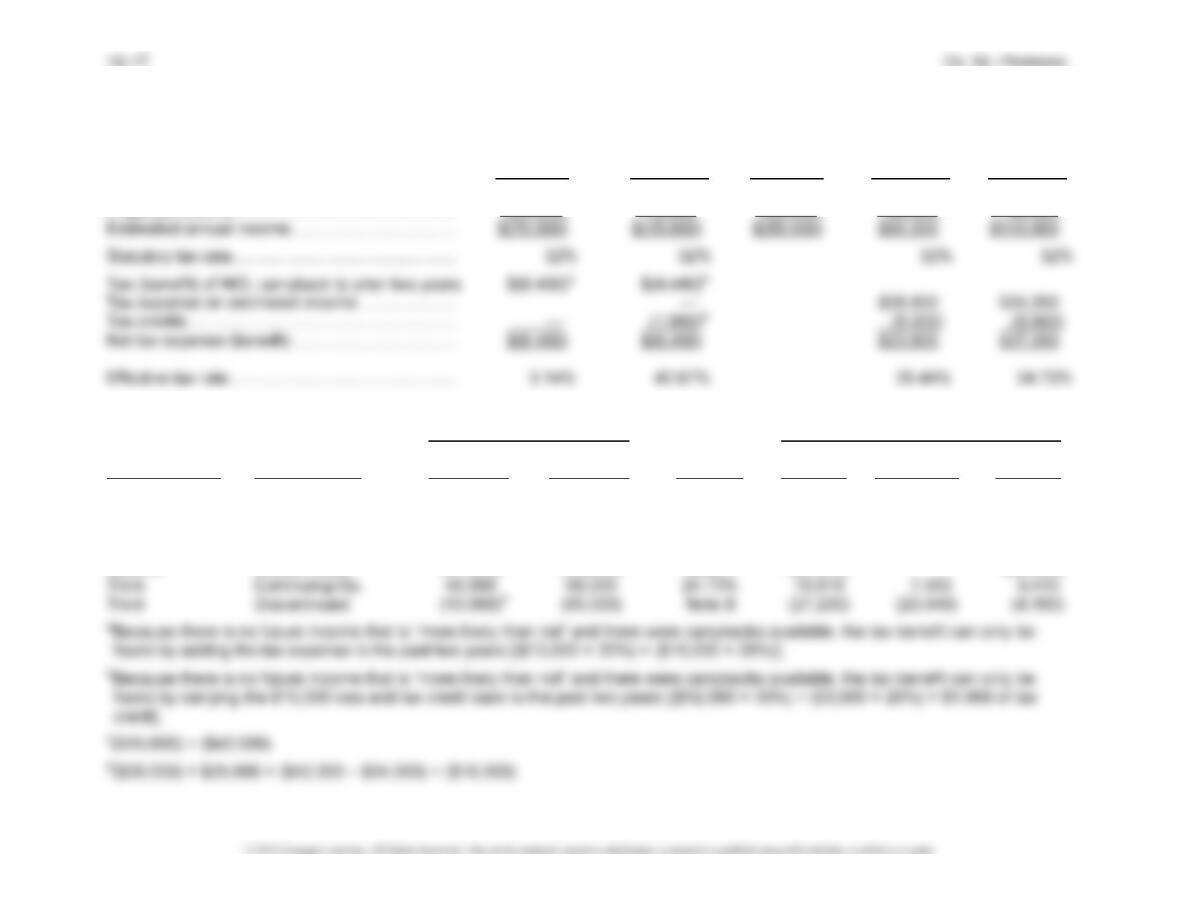

First Continuing Op. $(45,000) $(45,000) See a $ (6,400) $ — $ (6,400)

First—Restated Continuing Op. (30,000) (30,000) See b (6,400) — (6,400)

First—Restated Discontinued (15,000) (15,000) See b — — —

Second Continuing Op. 58,000 28,000 26.44% 7,403 (6,400) 13,803

Second Discontinued (57,000)c (72,000) Note A (23,040) — (23,040)

Problem 12-2, Concluded

Note A: Ordinary

Income

All Sources

Annual income (loss) ………………….. $90,000 $18,000