Ch. 12: The Revenue Cycle: Sales and Cash Collections

Identify at least three control weaknesses at Parktown. Describe the potential threat

and exposure associated with each weakness, and recommend how to best correct

them. (CPA Examination, adapted)

1. Weakness: The employees who perform services are permitted to approve credit

without an external credit check.

Threat: Sales could be made that turn out to be uncollectible.

2. Weakness: The physician who approves credit also approves the write-off of

uncollectible accounts.

Threat: Accounts receivable could be understated and bad debts expense overstated

because write-offs of accounts could be approved for accounts that are, in fact,

3. Weakness: The employee who initially handles cash receipts also prepares billings

and maintains accounts receivable.

Threat: Theft by lapping could occur. Fees earned and cash receipts or accounts

receivable could be understated because of omitted or inaccurate billing.

4. Weakness: The employee who makes bank deposits also reconciles bank statements.

Threat: The cash balance per books may be overstated because all cash is not

deposited (i.e. theft).

5. Weakness: The employee who makes bank deposits also issues credit memos.

Accounting Information Systems

Threat: The office manager could steal cash and cover up the shortage by issuing a

credit memo for the amount stolen.

6. Weakness: Trial balances of the accounts receivable subsidiary ledger are not

prepared independently of, or verified and reconciled to, the accounts receivable

control account in the general ledger.

Threat: Any of fees earned, cash receipts, and uncollectible accounts expense could

be either understated or overstated because of undetected differences between the

Ch. 12: The Revenue Cycle: Sales and Cash Collections

12.9 Figure 12-18 depicts the activities performed in the revenue cycle by the Newton

Hardware Company. (CPA Examination, adapted)

a. Identify at least 7 weaknesses in Newton Hardware’s revenue cycle. Explain the

resulting threat and suggest methods to correct the weakness.

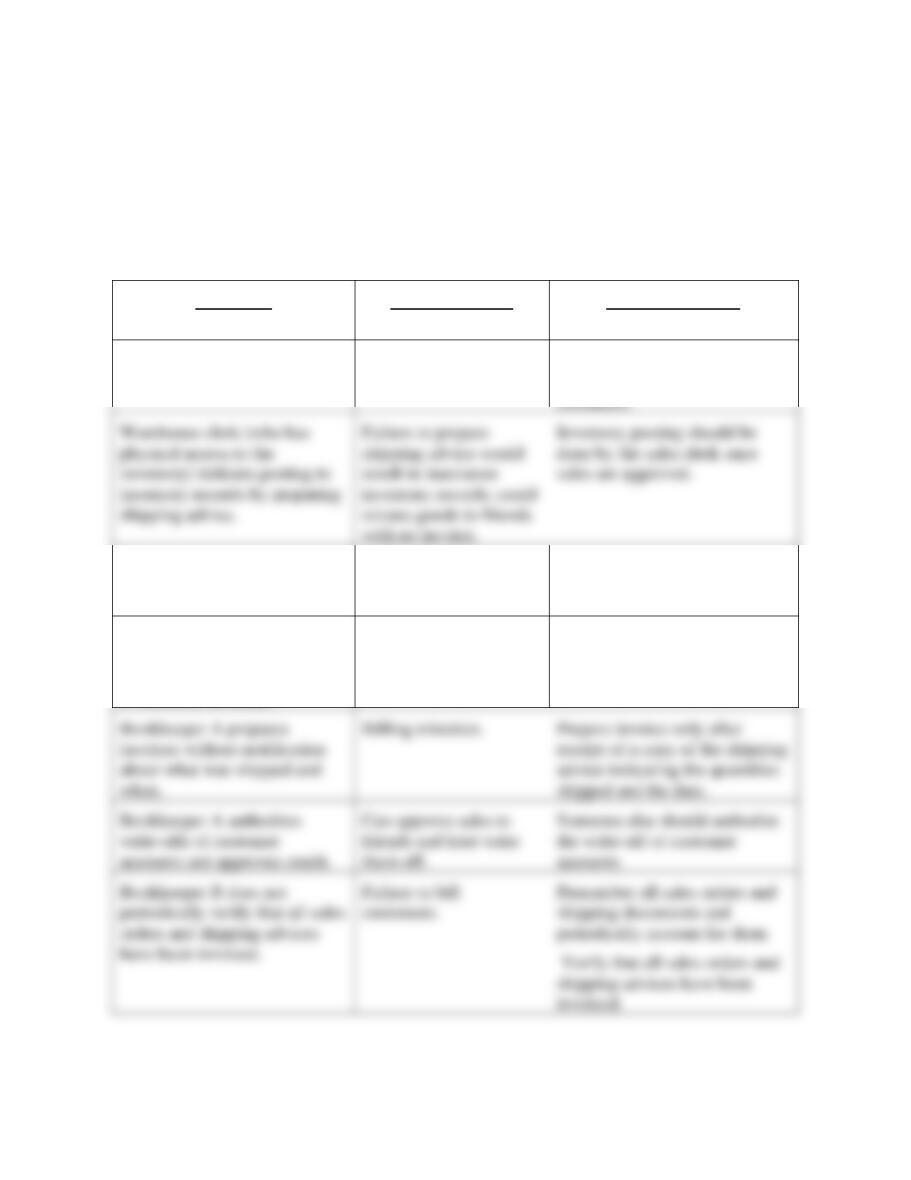

Weakness

Threat/Problem

Recommendation

Credit approval by bookkeeper

A has no effect on shipping.

Uncollectible sales.

Credit approval must occur

prior to shipping merchandise to

Warehouse clerk does not

retain copy of the shipping

advice.

Cannot easily identify

loss if the carrier has

accident.

Use a 4-copy shipping advice

and retain one copy in the

warehouse.

Bookkeeper A authorizes

customer credit and prepares

source documents for posting

to customer accounts.

Sales to friends that

exceed credit limit.

Credit manager should approve

all credit.

Bookkeeper A prepares

invoices without notification

about what was shipped and

when.

Billing mistakes.

Prepare invoice only after

receipt of a copy of the shipping

advice indicating the quantities

shipped and the date.

Bookkeeper A authorizes

write-offs of customer

accounts and approves credit.

Can approve sales to

friends and later write

them off.

Someone else should authorize

the write-off of customer

accounts.

Verify that all sales orders and

shipping advices have been

invoiced.

inventory) initiates posting to

inventory records by preparing

shipping advice.

result in inaccurate

inventory records; could

release goods to friends

with no invoice.

sales are approved.

Accounting Information Systems

12-37

Collections Clerk does not

deliver postdated checks and

checks with errors to an

employee independent of the

bank deposit for review and

disposition.

Possible theft of checks.

Deliver all checks not deposited

to another employee who has no

bank deposit/reconciliation

duties.

Collection Clerk initiates

posting of receipts to

subsidiary accounts receivable

ledger and has initial access to

cash receipts.

Theft by lapping.

Checks should be opened by

someone who does not have

bookkeeping or accounting

duties. That person should then

send a list of cash receipts to the

collections clerk to be used to

record cash receipts.

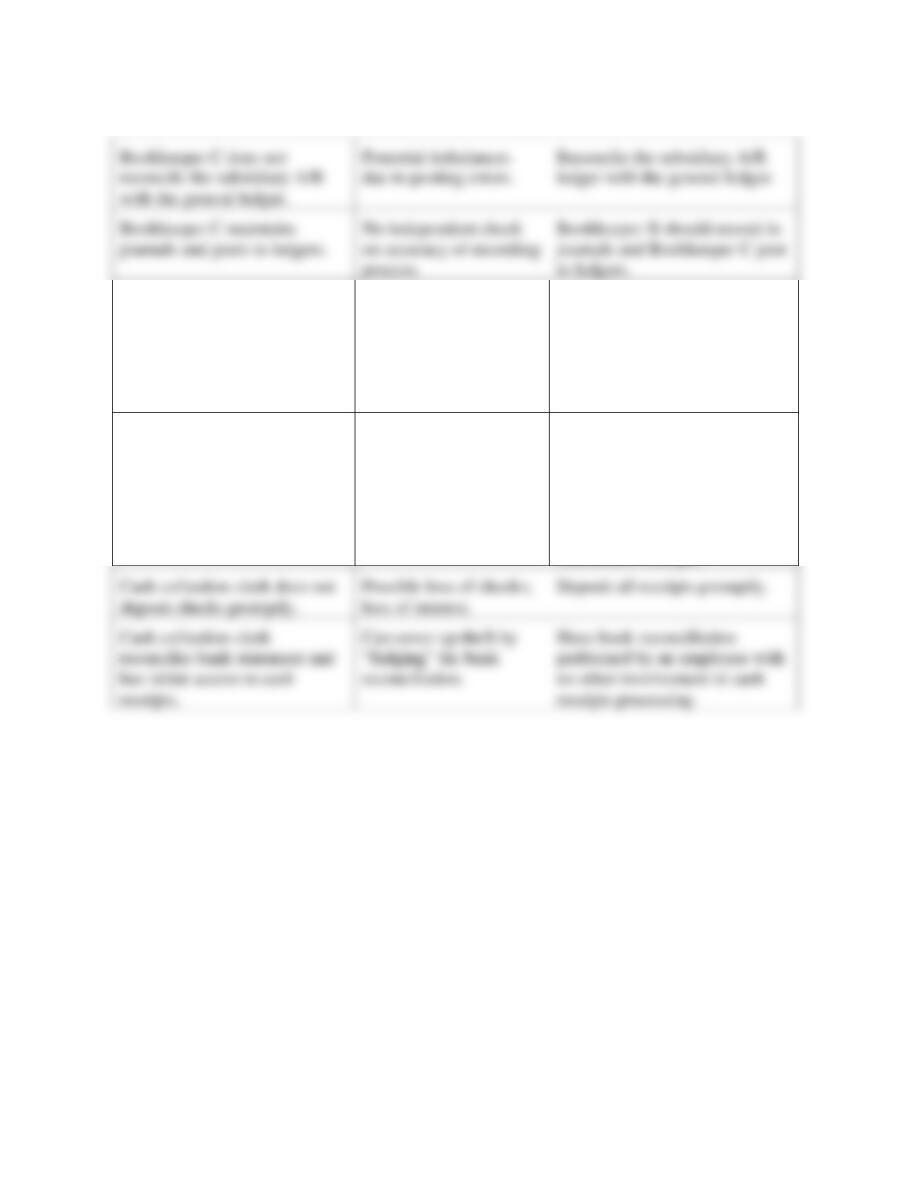

Cash collection clerk does not

deposit checks promptly.

loss of interest.

Deposit all receipts promptly.

Cash collection clerk

reconciles bank statement and

has initial access to cash

receipts.

Can cover up theft by

reconciliation.

Have bank reconciliation

performed by an employee with

no other involvement in cash

receipts processing.

Bookkeeper C does not

reconcile the subsidiary A/R

with the general ledger.

Potential imbalances

due to posting errors.

Reconcile the subsidiary A/R

ledger with the general ledger.

process.

to ledgers.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

b. Identify ways to use IT to streamline Newton’s revenue cycle activities. Describe

the control procedures required in the new system.

Some ways that Newton could use IT to improve efficiency include:

• On-line data entry by sales staff. The system should include credit checks on

customers as well as check inventory availability

Accounting Information Systems

12-39

12.10 The Family Support Center is a small charitable organization. It has only four full-

time employees: two staff, an accountant, and an office manager. The majority of its

funding comes from two campaign drives, one in the spring and one in the fall.

Donors make pledges over the telephone. Some donors pay their pledge by credit

card during the telephone campaign, but many prefer to pay in monthly

installments by check. In such cases, the donor pledges are recorded during the

telephone campaign and they are then mailed pledge cards. Donors mail their

contributions directly to the charity. Most donors send a check, but occasionally

some send cash. Most donors return their pledge card with their check or cash

donation, but occasionally the Family Support Center receives anonymous cash

donations. The procedures used to process donations are as follows:

The accountant enters the information from the list into the computer to

update the Family Support Center’s files. The accountant then prepares a

deposit slip (in duplicate) and deposits all cash and checks into the charity’s

bank account at the end of each day. No funds are left on the premises

overnight. The validated deposit slip is then filed by date. The accountant

also mails an acknowledgment letter thanking each donor. Monthly, the

accountant retrieves all deposit slips and uses them to reconcile the Family

Support Center’s bank statement. At this time, the accountant also reviews

the pledge files and sends a follow-up letter to those people who have not yet

fulfilled their pledges.

1. Weakness – Sarah opens all mail and prepares a list of donations (cash and

checks). Sarah could misappropriate anonymous cash donations.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

2. Weakness – The donations and donation list are sent to the accountant for

recording and to prepare the bank deposit. Therefore, the accountant has custody

of the donation and records the donation.

3. Weakness – Each employee has full access (create, read, update, delete) to the

accounting system.

Control – Only the accountant and the office manager should have full access to

the accounting system.

b. Describe the IT control procedures that should exist in order to protect the

Family Support Center from loss, alteration, or unauthorized disclosure of data.

• The weekly back-up should be stored off-site, not in the manager’s office.

Accounting Information Systems

12.11 Match the threats in the first column to the appropriate control procedures in the

second column (more than one control may address the same threat).

Threat

Applicable Control Procedures

1. _a,p__ Uncollectible sales

a. Restrict access to master data.

3. __o_ Crediting customer

account.

2. _g,i__ Mistakes in shipping

b. Encrypt customer information while in

5. _e,j,k__ Theft of inventory

by employees.

e. Physical access controls on inventory

6. __l_ Excess inventory.

f. Segregation of duties of handling cash

and maintaining accounts receivable.

7. _a__ Reduced prices for sales

to friends.

g. Reconciliation of packing lists with sales

orders.

placing them.

8. _d__ Orders later repudiated

h. Reconciliation of invoices with packing

9. _h,q__ Failure to bill

customers.

i. Use of bar-codes or RFID tags.

10. _h__ Errors in customer

invoices

j. Periodic physical counts of inventory

11. _m,n_ Cash flow problems

k. Perpetual inventory system.

12. _c__ Loss of accounts

receivable data

l. Use of either EOQ, MRP, or JIT

inventory control system.

personal information.

13. __a,b_ Unauthorized

m. Lockboxes or electronic lockboxes.

14. _g,r__ Failure to ship orders

to customers.

n. Cash flow budget

o. Mail monthly statements to customers.

q. Segregation of duties of shipping and

billing.

documents.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

12.12 EXCEL PROBLEM

Use EXCEL’s regression tools to analyze and forecast future sales.

(Hint: The article “Forecasting with Excel,” by James A. Weisel in the February

2009 issue of the Journal of Accountancy (available at www.aicpa.org) explains how

to perform the following tasks using either Excel 2003 or Excel 2007).

a. Create a spreadsheet with the following data about targeted emails, click ads,

and unit sales:

Emails

Clicks

Unit Sales

150000

100

12000

155000

105

12500

125000

75

10000

130000

150

14000

135000

125

12500

120000

100

10000

125000

125

10900

130000

135

11500

130000

110

12500

120000

95

10500

100000

75

10750

110000

100

10000

100000

80

9500

140000

130

13500

120000

110

11500

130000

125

13000

100000

85

12000

110000

100

9000

120000

135

10000

130000

140

13500

140000

125

13400

130000

115

12750

120000

105

12750

100000

95

10000

130000

145

9000

150000

150

15000

140000

120

12000

125000

100

13500

110000

95

11000

130000

140

13500

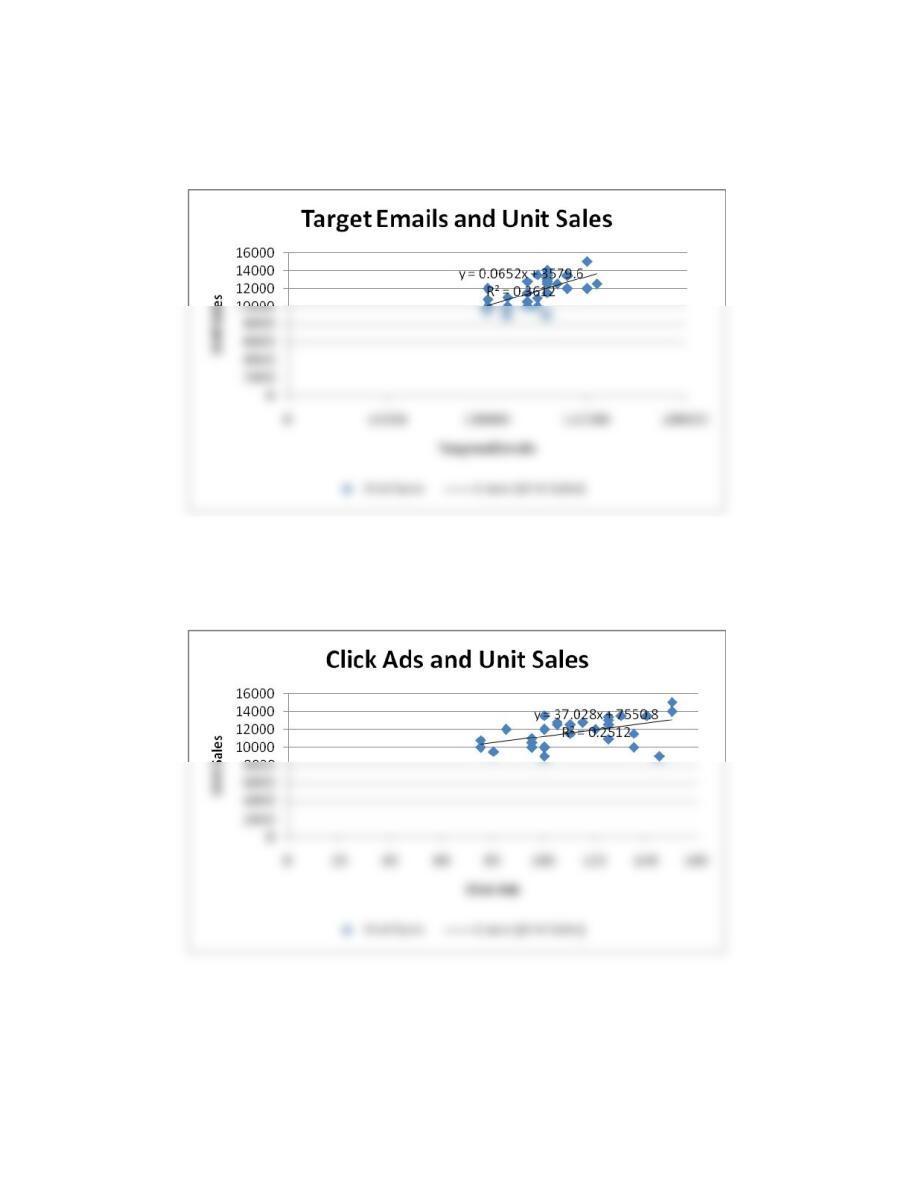

b. Create a scattergraph to illustrate the relationship between targeted emails and

unit sales. Display the regression equation and the R2 between the two variables

on the chart.

c. Create a scattergraph to illustrate the relationship between click ads and unit

sales. Display the regression equation and the R2 between the two variables on

the chart.

Accounting Information Systems

12-45

d. Which variable (targeted emails or click ads) has the greater influence on unit

sales? How do you know?

Targeted emails have a greater effect on unit sales than do click ads as shown by the

higher R2 for the regression formula.

e. Use the “ =Forecast “function to display the forecasted sales for 200,000 targeted

emails and for 200 click ads.

12.13 Give two specific examples of nonroutine transactions that may occur in processing

cash receipts and updating accounts receivable. Also specify the control procedures

that should be in place to ensure the accuracy, completeness, and validity of those

transactions.

Nonroutine Transaction

Control Procedure

1. Change of customer name or

address

1. Log of who initiated change and date.

2. Credit memos for sales

2. Approval by credit manager

3. Adjustments to customer credit

rating or credit limit.

3. Review and approval by credit manager

both prior to event and after recording.

4. Correction of errors in amounts,

dates, etc.

4. Review and approval by department

manager prior to resubmission.

5. New customers added to master

file.

5. Review and approval by credit manager

prior to submission.

6. Account write-offs (bad debts).

6. Review and approval by credit manager

both before event and after recording.

Ch. 12: The Revenue Cycle: Sales and Cash Collections

SUGGESTED ANSWERS TO THE CASES

Case 12.1: RESEARCH PROJECT: IMPACT OF IT ON REVENUE

CYCLE ACTIVITIES, THREATS, AND CONTROLS

Search popular business and technology magazines (Business Week, Forbes,

Fortune, CIO, etc.) to find an article about an innovative use of IT that can be used

to improve one or more activities in the revenue cycle. Write a report that:

a. Explains how IT can be used to change revenue cycle activities

b. Discusses the control implications. Refer to Table 12-1 and explain how the new

procedure changes the threats and appropriate control procedures for

mitigating those threats.