Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

CHAPTER 12

Responsibility Accounting, Operational

Performance Measures, and the Balanced

Scorecard

ANSWERS TO REVIEW QUESTIONS

12-1 Goal congruence results when the managers of subunits throughout an organization

strive to achieve objectives that are consistent with the goals set by top

management. In order for the organization to be successful, the managers and

12-2 (a) Cost center: A responsibility center, the manager of which is accountable for the

subunit’s costs. (An example is a production department in a manufacturing

firm.)

12-3 It would be appropriate to change a particular hotel from a profit center to an

12-4 Flexible budgeting allows a performance report to be constructed in a meaningful

way. The performance report should compare actual expenses incurred with the

12-5 Under activity-based responsibility accounting, management’s attention is directed

toward activities, rather than being focused primarily on cost, revenue, and profit

12-6 Attention to the following two factors may yield positive behavioral effects from a

responsibility-accounting system.

(a) When properly used, a responsibility-accounting system does not emphasize

12-7 Rarely does a single individual completely control a result in an organization. Most

results are caused by the joint efforts of several people and the joint impact of

12-8 (a) Cost pool: A collection of costs to be assigned to a set of cost objects. (An

(b) Cost object: A responsibility center, product, or service to which a cost is

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

12-9 An example of a common resource in an organization is a computer department. The

resource includes the computer itself, the software, and the computer specialists

12–10 A computer system has a limited capacity at any one time. Allocating the cost of

12–11 A cost allocation base is a measure of activity, physical characteristic, or economic

characteristic associated with the responsibility centers, which are the cost objects

12–12 Marketing costs are distributed to the hotel’s departments on the basis of budgeted

sales dollars so that the behavior of one department does not affect the costs

12–14 Many managers and accountants believe that it is misleading to allocate common

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

12–15 It is important in responsibility accounting to distinguish between segments and

segment managers, because some costs that are traceable to a segment may be

12–16 Three key features of a segmented income statement are as follows: contribution

12–17 A common cost for one segment can be a traceable cost for another segment. For

example, the salary of the general manager of a hotel is traceable to that segment of

12–18 Customer profitability analysis refers to using the concepts of activity-based costing

to determine how serving particular customers causes activities to be performed and

12–19 Seven areas in which nonfinancial operational performance measures are being

used are as follows:

(a) Raw material and scrap

12–20 Manufacturing cycle efficiency (MCE) is defined as processing time divided by the

12–21 Examples of customer-acceptance measures include the number of customer

12–22 An aggregate productivity measure is defined as total output divided by total input.

Such a measure is limited because it is expressed in dollars, rather than in physical

12–23 An airline could measure the frequency and cost of customer complaints about lost

12–24 Responses will vary widely on this question. Here are some possibilities for a bank:

• Financial: (a) profit; (b) cost of back-office (i.e., administrative) operations.

12–25. Lead measures, such as market share or new financial products, show how well the

bank is doing now in areas that will affect financial performance in the future. Lag

12–26. Improvement in employee retention could lead to improvement in internal business

processes, such as better product or service quality, faster manufacturing cycle

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

SOLUTIONS TO EXERCISES

EXERCISE 12-27 (10 MINUTES)

The Maintenance Department should not be charged for the excess wages of the skilled

EXERCISE 12-28 (10 MINUTES)

(1)

Orange juice factory: Cost center or profit center.

(2)

College of engineering at a university: Profit center.

(By designating the college of engineering as a profit center, this subunit is

(4)

Outpatient clinic in a profit-oriented hospital: Profit center.

Mayor’s office of a city: Cost center.

(6)

Movie theater: Cost center or profit center.

(7)

Radio station: Profit center.

Claims department: Cost center.

(9)

Ticket sales division of an airline: Revenue center.

Bottling plant: Cost center.

EXERCISE 12-29 (50 MINUTES)

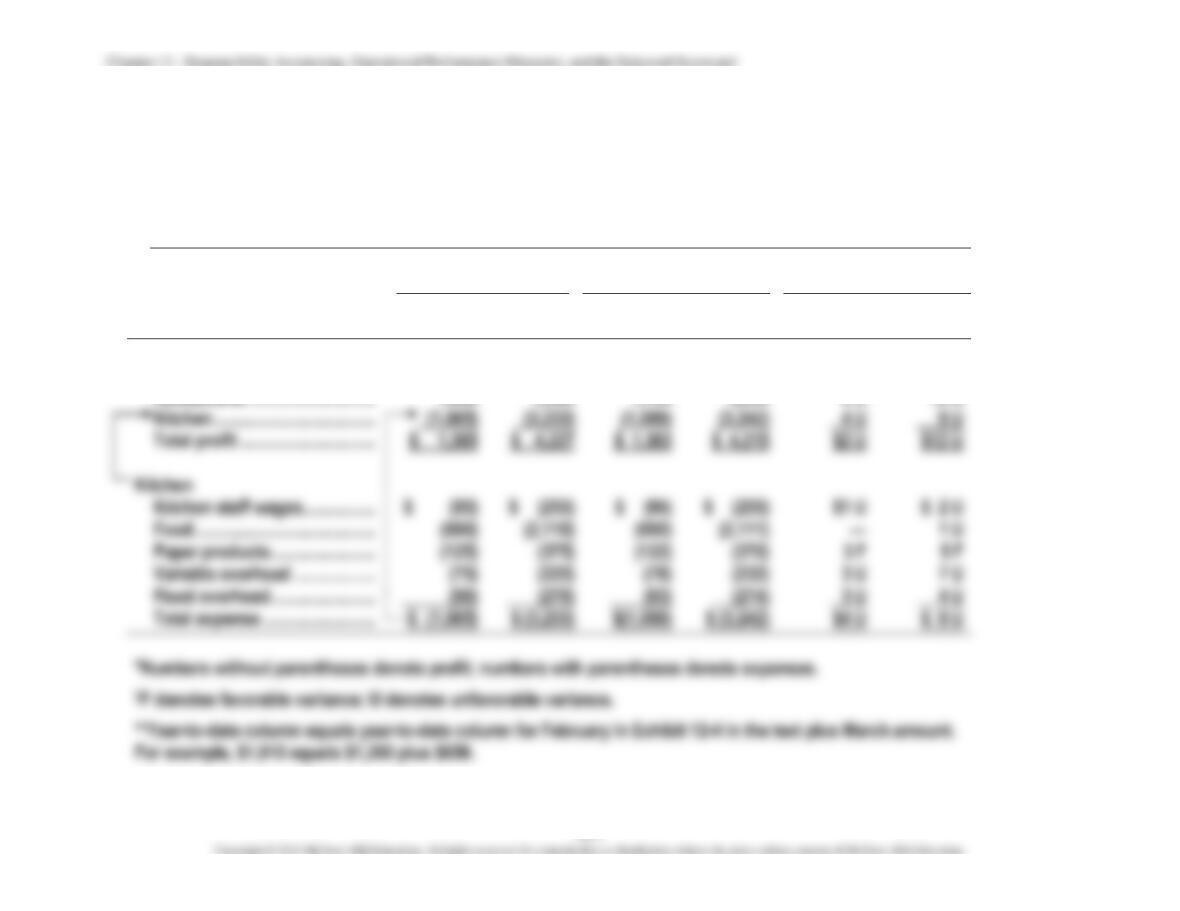

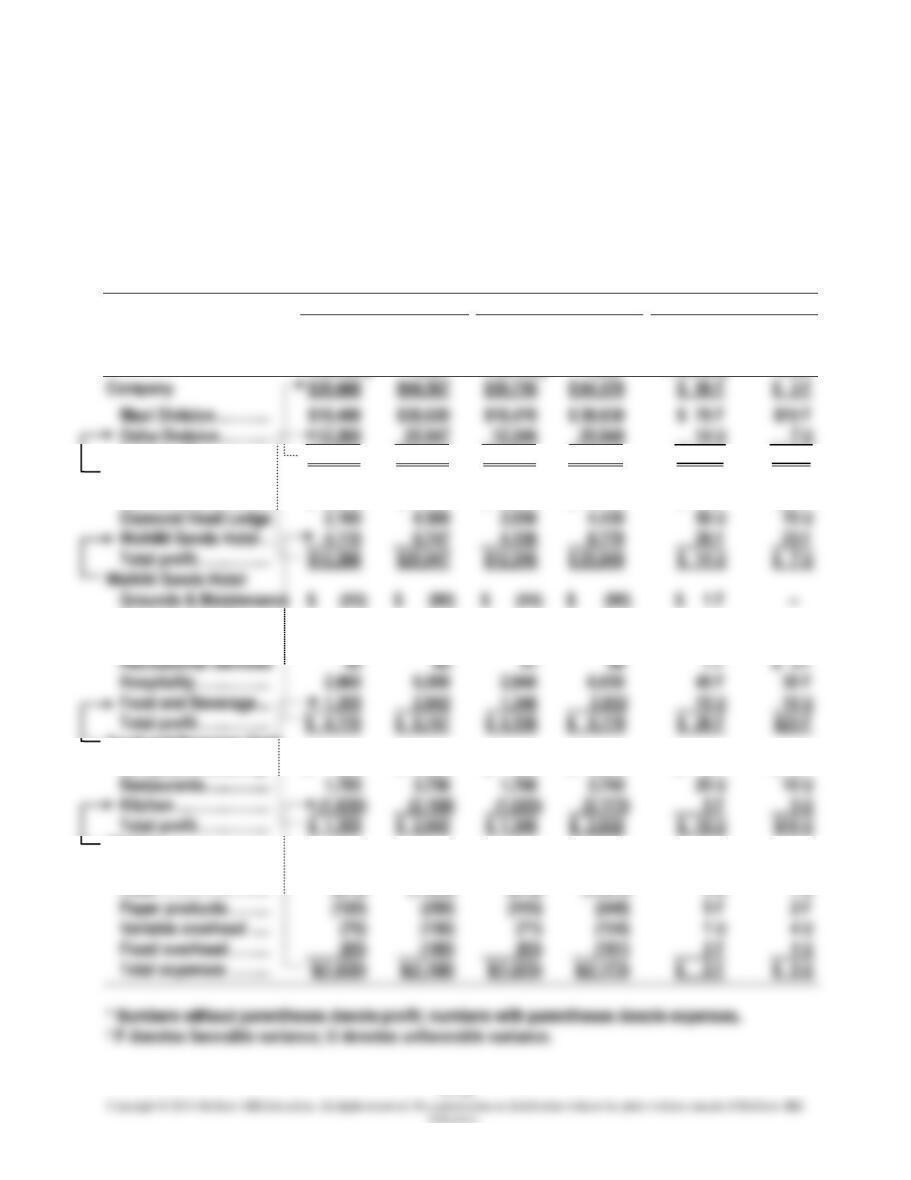

PERFORMANCE REPORTS FOR MARCH:

SELECTED SUBUNITS OF ALOHA HOTELS AND RESORTS

(IN THOUSANDS)

Flexible Budget*

Actual Results*

Variance†

March

Year to

Date**

March

Year to

Date**

March

Year to

Date**

Food and Beverage Department

Banquets & Catering …………..

$ 650

$ 1,910

$ 658

$ 1,923

$ 8 F

$ 13 F

Restaurants ……………………….

1,800

5,550

1,794

5,534

6 U

16 U

Kitchen ………………………………

Total profit …………………………

$ 1,383

$ 4,215

$2 U

Kitchen

Kitchen staff wages …………….

$1 U

Food ………………………………….

(690)

(690)

1 U

Paper products …………………..

(125)

(375)

(122)

(370)

Variable overhead ………………

(225)

(232)

3 U

7 U

Fixed overhead …………………..

(90)

*Numbers without parentheses denote profit; numbers with parentheses denote expenses.

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

EXERCISE 12-30 (10 MINUTES)

The appropriate responsibility-accounting treatment for each of the scenarios is the

following:

(1)

Since the cost of idle time incurred in Department B was due to the breakdown of

(2)

If the machinery had been properly maintained, it would be more appropriate not to

charge the cost due to idle time in Department B back to Department A. This cost

EXERCISE 12-31 (10 MINUTES)

A profit center such as this might not be free to sell its services outside the company.

By designating this department as a profit center, the corporation has given the managers

of the department an opportunity to manage their operation just like a full-fledged business.

EXERCISE 12-32 (30 MINUTES)

1.

Allocation of costs:

Division

Department

and

Allocation Base

Liberal Arts

Sciences

Business

Administration

Total

Cost

Allocated

Admissions

(enrollment)

$46,800

(1,000/2,500)

$37,440

(800/2,500)

$32,760

(700/2,500)

$117,000

$73,125

$68,250

The Admissions Department costs are allocated on the basis of enrollment. The more

students enrolled in a division, the more admissions there are to process.

The Registrar’s costs are allocated on the basis of credit hours. The greater the

number of credit hours, the more course registrations there are to process.

The Computer Services Department’s costs are allocated on the basis of the

2.

The estimated amount of computer time required would probably be a better

allocation base for the Computer Services Department. Two different courses

The number of courses would probably be a better allocation base for the Registrar’s

costs. Costs in this department are driven by processing course registrations, not

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

EXERCISE 12-33 (40 MINUTES)

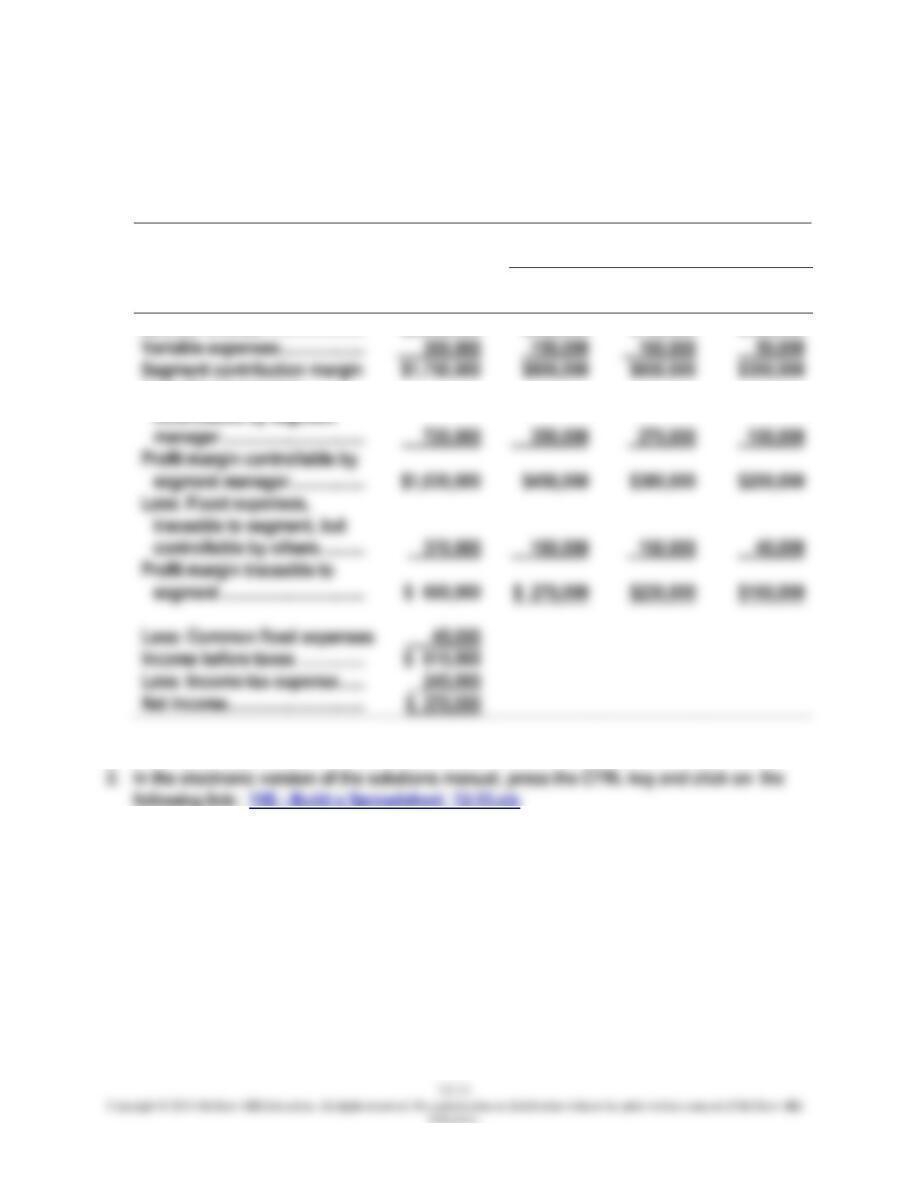

1. Segmented income statement:

SEGMENTED INCOME STATEMENTS: TRI-COUNTY CABLE SERVICES, INC.

Tri-County

Segments of Company

Cable

Services

Metro

Suburban

Outlying

Service revenue ………………….

$2,050,000

$950,000

$750,000

$350,000

Variable expenses ……………….

50,000

Segment contribution margin

$1,750,000

$800,000

$650,000

$300,000

Less: Fixed expenses,

40,000

Less: Common fixed expenses

Income before taxes ……………

Less: Income tax expense ……

Less: Fixed expenses

EXERCISE 12-34 (30 MINUTES)

Answers will vary widely, depending on the company. Some examples are as follows:

Marriott Hotels: Company-owned hotel, profit center

McDonald’s Corporation: Company-owned restaurant, profit center

EXERCISE 12-35 (15 MINUTES)

1.

Aggregate (or total) productivity

=

input total

output total

2.

This summary financial measure does not convey much information to management

or other users of the data. A preferable approach would be to record multiple physical

measures that capture the most important determinants of the bank’s productivity.

Examples include the following:

a.

Clerk time per bank window customer

Errors per 1,000 transactions handled

c.

Checks miscoded per 1,000 checks processed

Customers per day

e.

Customers per employee

Square feet of space in bank per 1,000 customers

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

EXERCISE 12-36 (10 MINUTES)

1.

Manufacturing cycle efficiency (MCE):

MCE

=

timemove time waiting timeinspection timeprocessing

timeprocessing

+++

=

EXERCISE 12-37 (10 MINUTES)

1.

Manufacturing cycle efficiency

=

timemove time waiting

timeinspection timeprocessing

timeprocessing

++

+

=

2.

Manufacturing cycle time

=

batch per units

batch per timeproduction total

=

.25 hour (or 15 minutes) per unit

3.

Velocity

=

batch per timeproduction total

batch per units

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

EXERCISE 12-38 (30 MINUTES)

1. The overall long-term goal for a profit-seeking enterprise generally is profitability.

This means that the key long-term goal in a profit-seeking business’s balanced

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

SOLUTIONS TO PROBLEMS

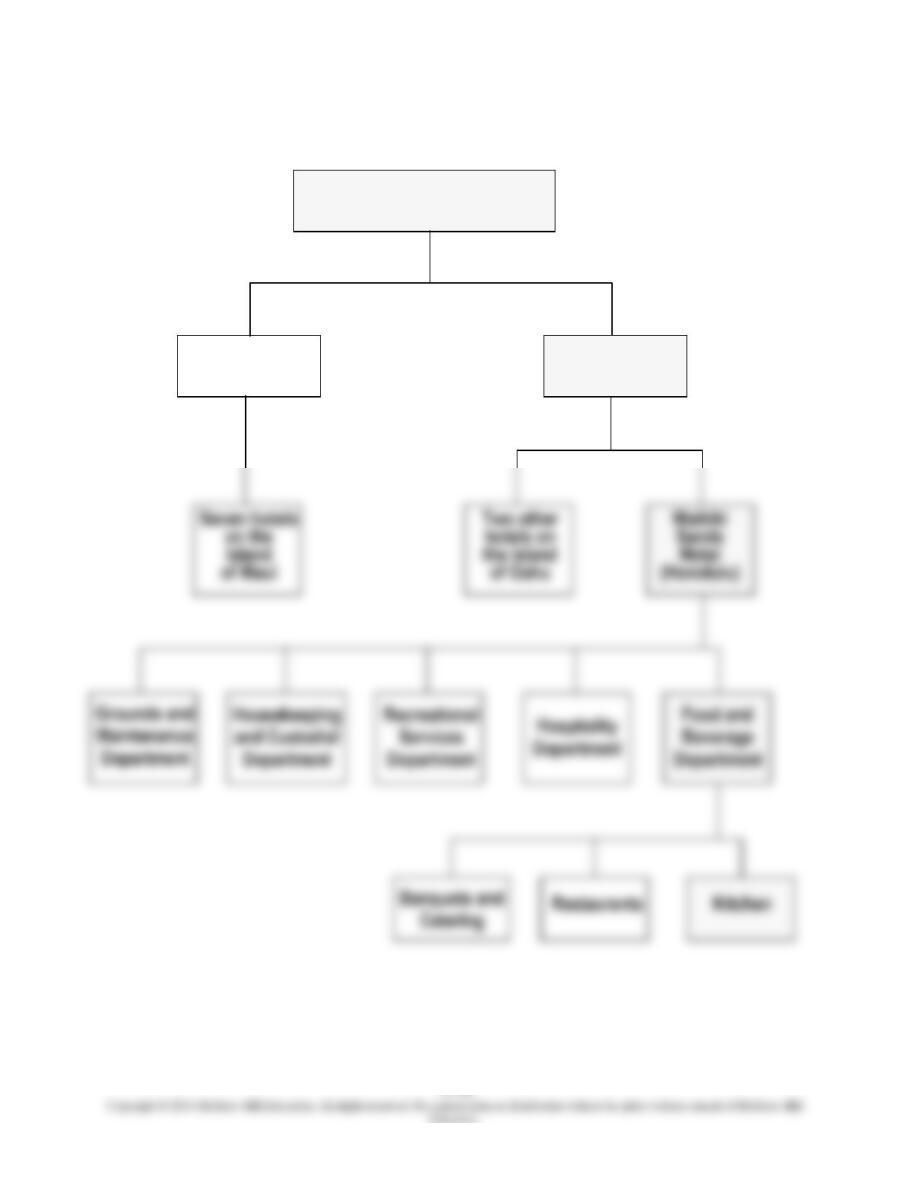

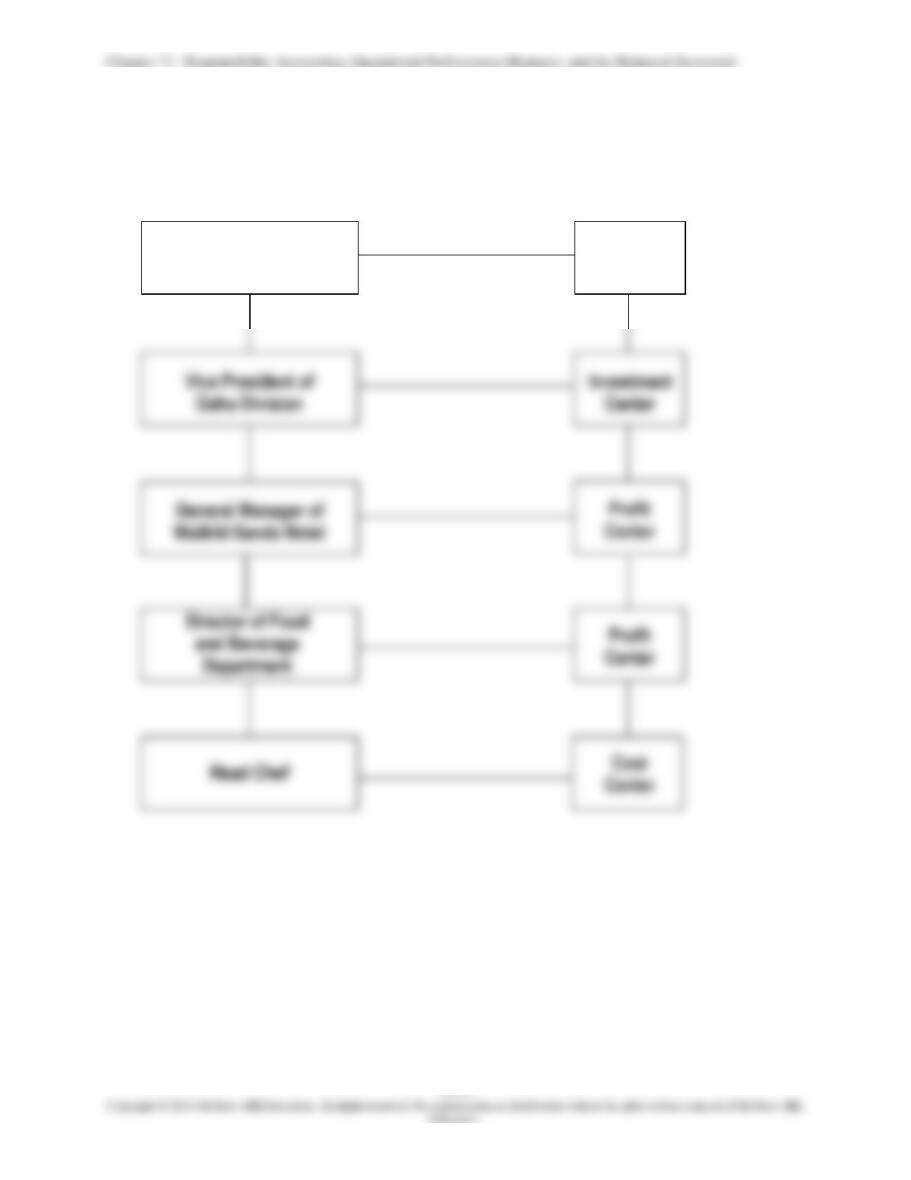

PROBLEM 12-39 (30 MINUTES)

A wide range of responses is possible for this problem. The organization chart and

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-39 (CONTINUED)

Maui Division

Aloha Hotels and Resorts, Inc.

Oahu Division

PROBLEM 12-39 (CONTINUED)

MANAGER

RESPONSIBILITY

CENTER

President of Aloha

Hotels and Resorts, Inc.

Investment

Center

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-40 (40 MINUTES)

Once again, a wide range of responses is possible, depending on the organization designed

in the preceding problem. The format for the performance reports is given in Exhibit 12-4 for

Aloha Hotels and Resorts. This exhibit is repeated here for convenience.

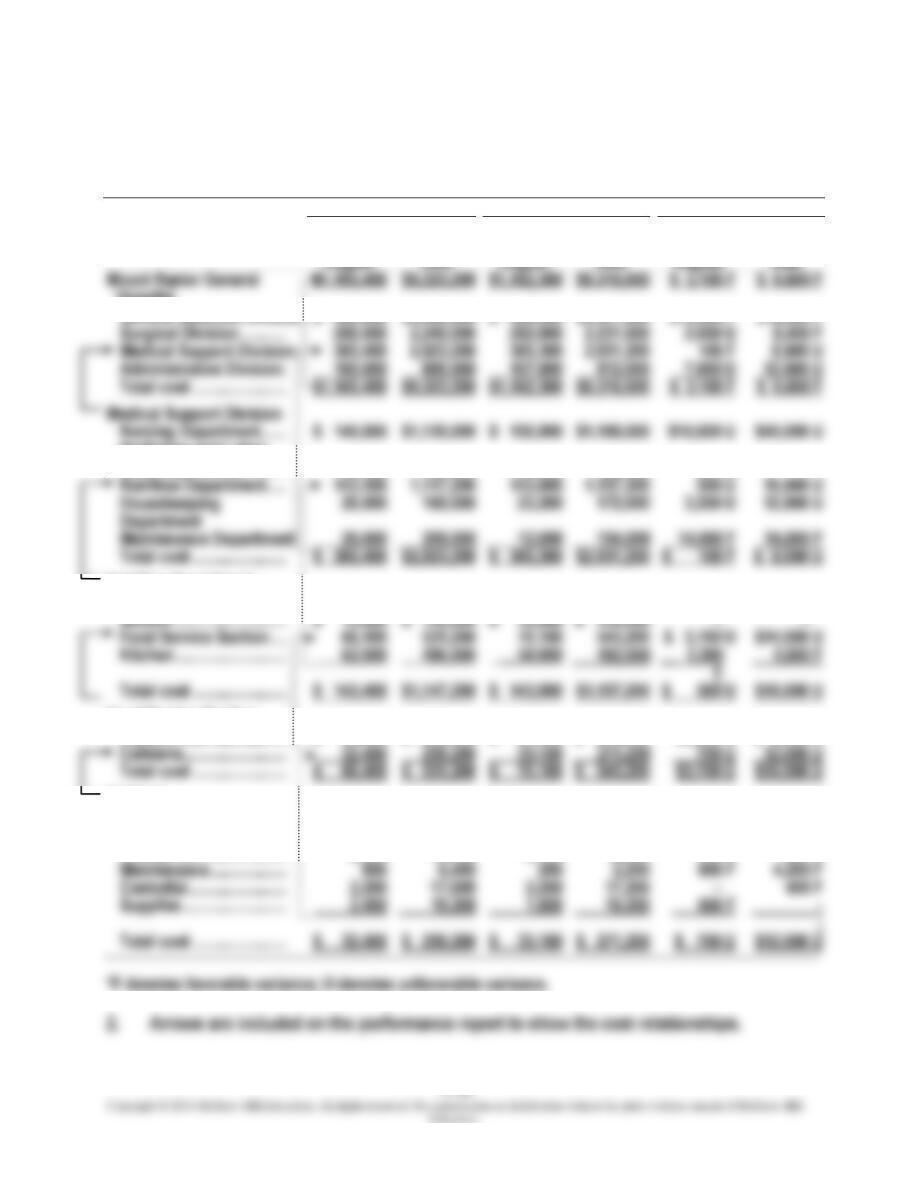

PERFORMANCE REPORTS FOR FEBRUARY:

SELECTED SUBUNITS OF ALOHA HOTELS AND RESORTS

(IN THOUSANDS)

Flexible Budget*

Actual Results*

Variance†

Year

Year

Year

to

to

to

February

Date

February

Date

February

Date

Maui Division ………….

$18,400

$38,620

$18,470

$ 38,630

$ 70 F

$10 F

Oahu Division …………

Total profit ………………

$30,660

$64,567

$30,716

$ 64,570

$ 56 F

$ 3 F

Oahu Division

Waimea Beach Resort

$ 6,050

$12,700

$ 6,060

$ 12,740

$ 10 F

$40 F

Diamond Head Lodge

Waikiki Sands Hotel ..

Total profit ………………

$12,260

$25,947

$12,246

$ 7 U

Waikiki Sands Hotel

Grounds & Maintenance

$ (45)

$ (90)

$ 1 F

—

Housekeeping &

Custodial

(40)

(90)

(41)

(90)

1 U

—

Recreational Services

$ 3 F

Hospitality ………………

Food and Beverage …

Total profit ………………

$ 4,136

Food and Beverage Dept.

Banquets & Catering

$ 600

$ 1,260

$ 605

$ 1,265

$ 5 F

$ 5 F

Restaurants …………….

Kitchen …………………..

Total profit ………………

$ 1,355

$ 2,842

$ 1,340

$ 2,832

$ 15 U

$10 U

Kitchen

Kitchen staff wages …

$ (80)

$ (168)

$ (78)

$ (169)

$ 2 F

$ 1 U

Food ………………………

(675)

(1,420)

(678)

(1,421)

3 U

1 U

Paper products ……….

Variable overhead …..

(70)

(150)

(71)

(154)

1 U

4 U

Fixed overhead ……….

* Numbers without parentheses denote profit; numbers with parentheses denote expenses.

PROBLEM 12-41 (35 MINUTES)

Memorandum

Date:

Today

To:

Sandy Beach, General Manager of Waikiki Sands Hotel

From:

I.M. Student

Subject:

Responsibility Centers

recommendations, staff scheduling, and use of materials and equipment.

The Waikiki Sands Hotel is a profit center as specified by the corporation’s top

management. The hotel’s general manager does not have the authority to make significant

investment decisions, so an investment-center designation would be inappropriate for the

hotel.

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-42 (60 MINUTES)

1.

Performance Report for August: Selected Subunits of Mount Ranier General Hospital

Flexible Budget

Actual Results

Variance*

Year

Year

Year

to

to

to

August

Date

Date

Date

Hospital

General Medicine Division

$ 420,000

$3,360,000

$ 408,000

$3,341,800

Surgical Division ………..

280,000

282,000

Medical Support Division

365,400

365,300

100 F

8,000 U

Administrative Division .

100,000

800,000

107,000

812,000

Total cost …………………..

$1,165,400

$9,323,200

$1,162,300

$9,316,600

Medical Support Division

Nursing Department ……

$ 140,000

$1,120,000

$ 150,000

$1,160,000

$10,000 U

$40,000 U

Radiology and Labor-

atory Department ………..

36,000

288,000

36,200

288,000

200 U

—

Nutrition Department…..

143,400

143,900

500 U

10,000 U

Housekeeping

Department

Maintenance Department

26,000

Total cost …………………..

$ 365,400

$2,923,200

$ 365,300

$2,931,200

$ 100 F

$ 8,000 U

Nutrition Department

$ 15,000

$ 120,000

$ 15,000

—

—

Food Service Section ….

66,400

531,200

70,100

545,200

$ 3,700 U

$14,000 U

Kitchen ………………………

Total cost …………………..

$ 143,400

$1,147,200

$ 143,900

$1,157,200

$10,000 U

Registered Dietitians’

Food Service Section

Patient Food Service …..

$ 34,000

$ 272,000

$ 37,000

$ 274,000

$3,000 U

$ 2,000 U

Cafeteria …………………….

32,400

259,200

33,100

271,200

Total cost …………………..

$ 66,400

$ 531,200

$ 70,100

$ 545,200

$3,700 U

Cafeteria

Food servers’ wages …..

$ 16,000

$ 128,000

$ 18,000

$ 144,000

$2,000 U

$16,000 U

Paper products …………..

9,000

72,000

8,800

72,400

200 F

400 U

Utilities ………………………

2,000

16,000

2,100

16,200

100 U

200 U

Maintenance ……………….

6,400

600 F

Custodial ……………………

2,200

17,600

2,200

—

400 F

*F denotes favorable variance; U denotes unfavorable variance.