PROBLEM 12-42 (CONTINUED)

3.

A variety of responses are reasonable for this question. Since the data given in the

problem do not include the individual variances over several months, it is not possible

to condition the investigation on trends. The largest variances in the performance

report are the most likely to warrant an investigation. The following variances for

August would likely catch the attention of the hospital administrator:

General Medicine Division ………………………………………………………………..

$12,000

F

Administrative Division …………………………………………………………………….

U

Nursing Department ………………………………………………………………………….

U

Maintenance Department ………………………………………………………………….

F

Food servers’ wages …………………………………………………………………………

U

hospital.

PROBLEM 12-43 (45 MINUTES)

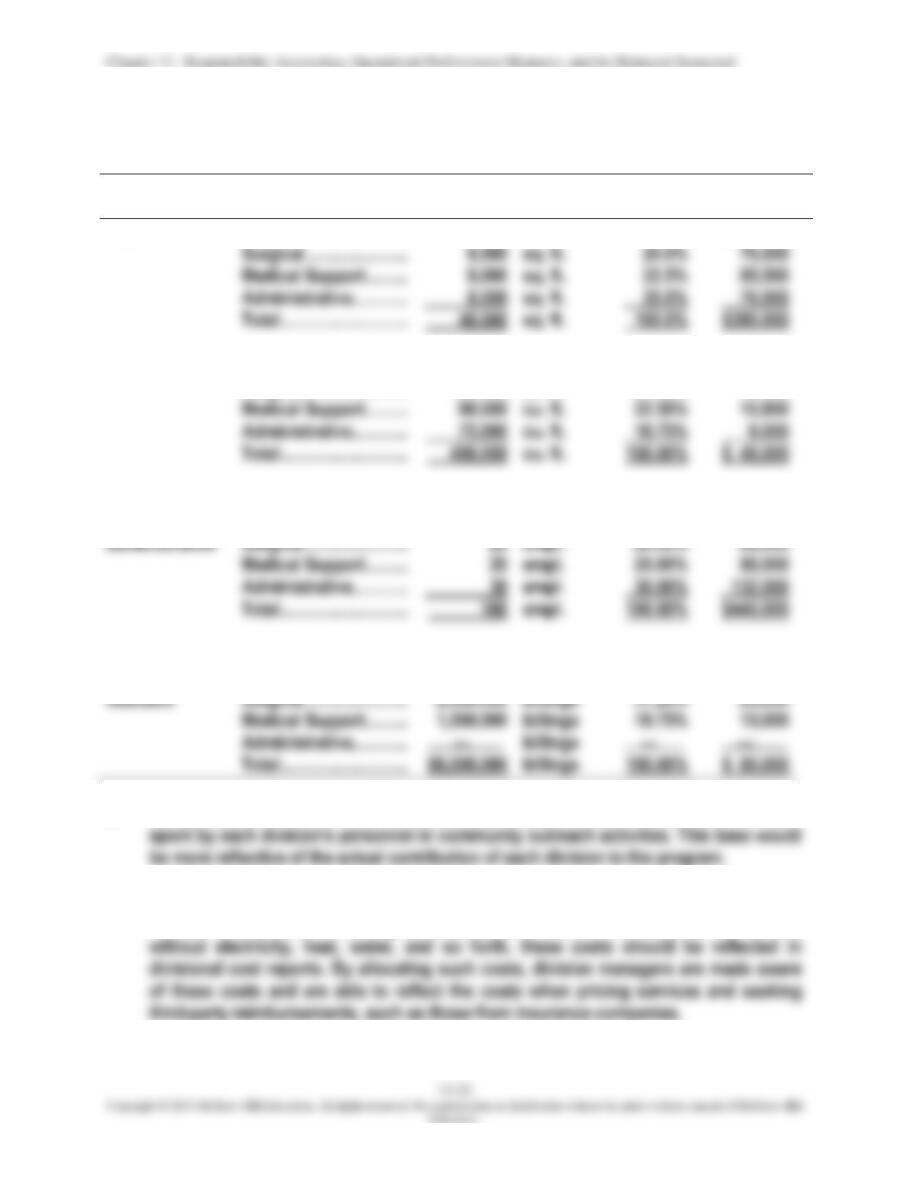

1.

Cost

Pool

Division

Allocation

Base

Percentage

of Total

Costs

Distributed

Facilities

General Medicine ……….

15,000

sq. ft.

37.5%

$142,500

Surgical …………………….

sq. ft.

20.0%

76,000

Medical Support …………

sq. ft.

22.5%

85,500

Administrative ……………

sq. ft.

76,000

Total ………………………….

sq. ft.

$380,000

Utilities

General Medicine ……….

135,000

cu. ft.

33.75%

$ 16,200

Surgical …………………….

100,000

cu. ft.

25.00%

12,000

Medical Support …………

90,000

cu. ft.

22.50%

10,800

Administrative ……………

cu. ft.

9,000

cu. ft.

$ 48,000

General

General Medicine …….

30

empl.

30.00%

$132,000

administration

Surgical …………………….

empl.

20.00%

88,000

Medical Support …………

empl.

20.00%

88,000

Administrative ……………

empl.

Total ………………………….

empl.

$440,000

Community

General Medicine ……….

$4,000,000

billings

50.00%

$ 40,000

outreach

Surgical …………………….

billings

31.25%

25,000

Medical Support …………

billings

18.75%

15,000

Administrative ……………

billings

2.

An alternative allocation base for community outreach costs is the number of hours

3.

The reason for allocating utility costs to the divisions is so that each division’s cost

reflects the total cost of running the division. Since none of the divisions can operate

PROBLEM 12-43 (CONTINUED)

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-44 (75 MINUTES)

1. SEGMENTED INCOME STATEMENTS: BUCKEYE DEPARTMENT STORES, INC. (IN THOUSANDS)

Segments of Company

Segments of Columbus Division

Buckeye

Department

Stores, Inc.

Cleveland

Division

Columbus

Division

Olentangy

Store

Scioto

Store

Downtown

Store

Not Allocated

Cost of merchandise sold ……………………

$ 69,000

Sales personnel—salaries ……………………

Utilities ……………………………………………….

Other …………………………………………………..

Segment contribution margin ……………………

$ 35,745

$ 4,230

$ (105)

Less: Fixed expenses controllable by

segment manager:

Depreciation—furnishings …………………..

$ 1,680

$ 870

$ 810

$ 240

$ 150

$ 420

Computing and billing …………………………

Insurance ……………………………………………

Security ………………………………………………

Less: Fixed expenses, traceable to

segment, but controllable by others: ……….

Depreciation—buildings ………………………

$ 2,790

$ 1,410

$ 1,380

$ 360

$ 270

$ 750

Property taxes …………………………………….

Supervisory salaries …………………………...

Total …………………………………………………………

$ 8,955

$ 4,920

$ 4,035

$ 915

$ 630

$ 2,190

Profit margin traceable to segment ……………

$ 19,440

$ 8,490

$ 2,535

Less: Common fixed expenses …………………

Income before taxes …………………………………

$ 19,080

Less: Income tax expense …………………………

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-44 (CONTINUED)

2.

The segmented income statement would help the president of Buckeye Department

PROBLEM 12-45 (30 MINUTES)

Responsibility-accounting system:

1. Two potential behavioral advantages if RELY’s managers accept the philosophy of

2. Two potential problems that could arise if the managers do not accept the change in

philosophy are as follows:

3. If the managers support the new system, and most of the disadvantages pointed out

above are avoided, the responsibility-center system will enhance the alignment of

PROBLEM 12-45 (CONTINUED)

Participatory budgeting system:

1. Two potential behavioral benefits are the following:

• RELY’s managers are likely to accept the system and be motivated to attain the

2. Two potential problems that could arise are as follows:

• The managers could be motivated to “pad” their budgets, putting slack in the plan to

3. Participatory budgeting can contribute to an organization’s goals by encouraging buy-

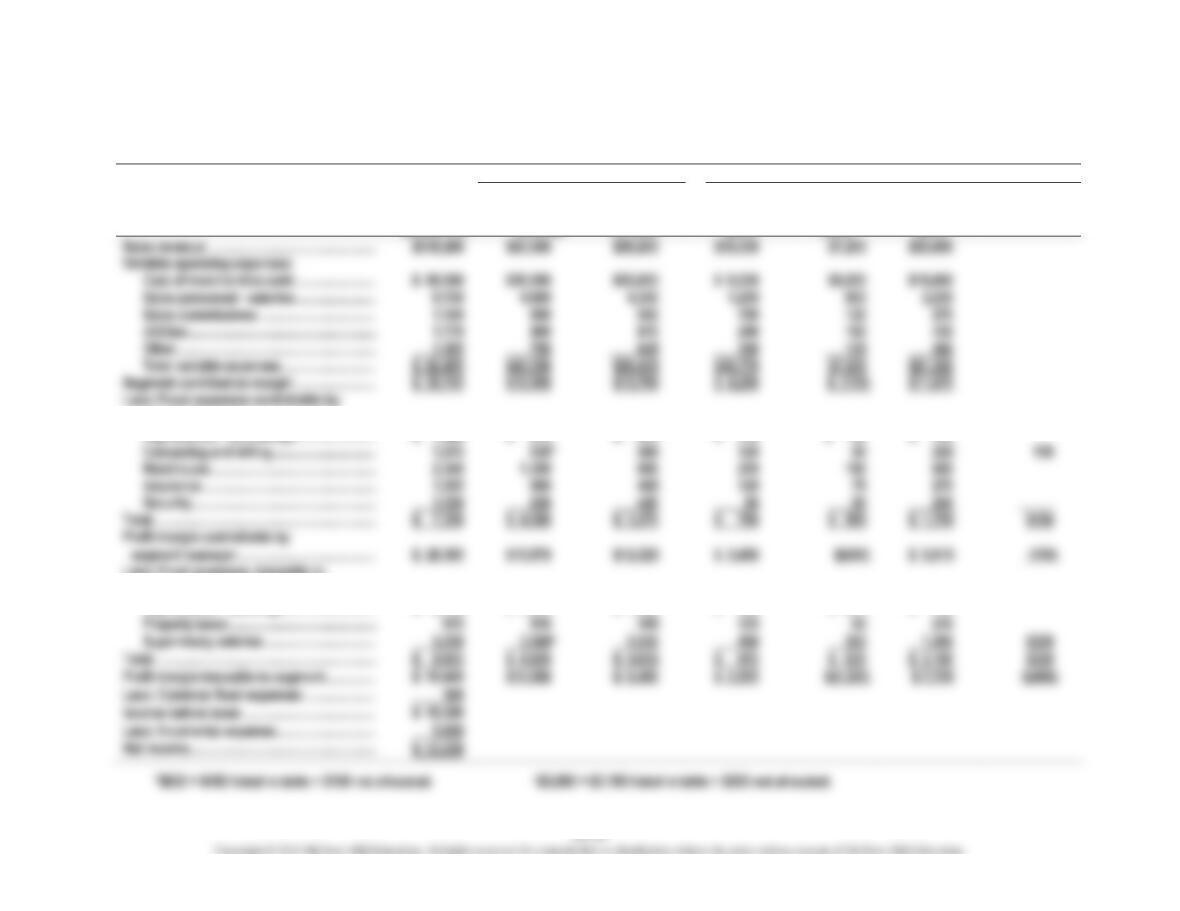

PROBLEM 12-46 (35 MINUTES)

1. Segmented income statement:

Piedmont

Novelties

Raleigh

Charlotte

Savannah

Sales revenue……………………………….

$1,998,000

$666,000

$676,500

$655,500

Variable operating expenses:

Cost of goods sold……………………

$1,057,500

$305,250

$338,250

$414,000

Sales commissions……………………

Segment contribution margin…………….

$ 820,620

$320,790

$297,660

$202,170

Less: Fixed expenses controllable by

segment manager:

Local advertising………………………

$ 121,500

$ 16,500

$ 33,000

$ 72,000

Sales manager salary…………………

48,000

—-

48,000

$ 169,500

$ 16,500

$ 33,000

$120,000

Profit margin controllable by segment

Less: Fixed expenses traceable to

segment, but controllable by

others:

Local property taxes…………………..

$ 18,750

$ 6,750

$ 3,000

$ 9,000

Store manager salaries……………….

162,000

46,500

58,500

57,000

$ 223,050

$ 61,950

$ 68,400

$ 92,700

Less: Common fixed expenses………….

Net income……………………………………

$ 139,620

Supporting calculations:

Sales revenue: Raleigh, 37,000 units x $18.00; Charlotte, 41,000 units

PROBLEM 12-46 (CONTINUED)

2. Savannah is the weakest segment because of several factors:

• Despite being the only store that has a sales manager, and spending

3. Piedmont Novelties uses a responsibility accounting system, meaning that managers

and centers are evaluated on the basis of items under their control. Since this is a

PROBLEM 12-47 (45 MINUTES)

Memorandum

Date:

Today

To:

Mathew Basler, President of Ujvari Equipment Company

From:

I. M. Student

Subject:

Ujvari Equipment Company’s critical success factors are as follows:

1.

Cost-efficient production: The firm must meet the market price, which implies

producing in a cost-efficient manner.

Responsibility-Accounting System

2.

High product quality: Stated by the company president as necessary for success.

3.

On-time delivery: Also noted by the company president as critical to the firm’s

success.

Note that the product price is not a critical success factor, since it is largely beyond the

company’s control. The price is determined by the market.

The sales districts should be revenue centers, in which the sales district managers are

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-47 (CONTINUED)

In conclusion, I recommend that the plants be designated as profit centers and the

If the plants are profit centers, then each plant manager is encouraged to consider both

the costs and the benefits of a rush order. The cost is increased production cost, and the

PROBLEM 12-48 (45 MINUTES)

1.

Categories of measures:

Area of Production

Performance

Cycle time (days) ………………………………………………………………

a

Number of defective finished products ………………………………

b

Manufacturing-cycle efficiency ………………………………………….

a

Customer complaints ………………………………………………………..

b,c

Unresolved complaints ……………………………………………………..

c

Products returned …………………………………………………………….

b,c

Warranty claims ……………………………………………………………….

b,c

In-process products rejected …………………………………………….

d

Aggregate productivity ……………………………………………………..

a,e

Number of units produced per day per employee ……………….

a,e

Percentage of on-time deliveries ……………………………………….

Percentage of orders filled ………………………………………………..

Inventory value/sales revenue …………………………………………..

g,h

Machine downtime (minutes) …………………………………………….

Bottleneck machine downtime (minutes) …………………………...

Overtime (minutes) per employee ………………………………………

a,e

Average setup time (minutes) ……………………………………………

a

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-48 (CONTINUED)

2.

Memorandum

Date:

Today

To:

Management, Diagnostic Technology, Inc.

From:

I. M. Student

Subject:

Performance of Albany plant during 1st quarter

The performance of the Albany plant is evaluated in nine key areas:

a.

Production processing:

b.

Product quality:

c.

Customer acceptance:

d.

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-48 (CONTINUED)

e.

Productivity:

f.

Delivery performance:

Raw material and scrap; inventory:

Machine maintenance:

Overall evaluation:

PROBLEM 12-49 (40 MINUTES)

Memorandum

Date:

Today

To:

President, Southern Plastics Corporation

From:

I. M. Student

Subject:

Performance of Baton Rouge Plant

1.

The Baton Rouge Plant’s performance for the period January through June is

summarized as follows:

a.

Production processing and productivity:

demand late in the period. Power consumption has remained stable.

The plant’s cycle time (or throughput time) has improved over the period

from 19 hours to 16 hours (average of 17.8 hours). This indicates that the

b.

Product quality and customer acceptance:

c.

Delivery performance:

Chapter 12 – Responsibility Accounting, Operational Performance Measures, and the Balanced Scorecard

PROBLEM 12-49 (CONTINUED)

d.

Raw material, scrap and inventory:

e.

Machine maintenance:

2.

Recommended actions:

a.

Investigate the reasons behind the decline in manufacturing-cycle