CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN)

CAPITAL INVESTMENT ANALYSIS

DISCUSSION QUESTIONS

1. The principal objections to the use of the average rate of return method are its failure to

consider the expected cash flows from the proposals and the timing of these flows.

2. The principal limitations of the cash payback method are its failure to consider cash flows

occurring after the payback period and its failure to use present value concepts.

4. A one-year payback will not equal a 100% average rate of return because the payback period

is based on cash flows, while the average rate of return is based on income. The depreciation

on the project will prevent the two methods from reconciling.

7. The $7,900 net present value indicates that the proposal is desirable because the proposal is

expected to recover the investment and provide more than the minimum rate of return.

9. The computations for the net present value method are more complex than those for the

methods that ignore present value. Also, the method assumes that the cash received from the

proposal during its useful life will be reinvested at the rate of return used to compute the

present value of the proposal. This assumption may not always be reasonable.

10. The computations for the internal rate of return method are more complex than those for the

methods that ignore present value. Also, the method assumes that the cash received from the

proposal during its useful life will be reinvested at the internal rate of return. This assumption

may not always be reasonable.

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

BASIC EXERCISES

BE 26–1 (FIN MAN); BE 12–1 (MAN)

Estimate average annual income

$117,000 ($936,000 ÷ 8 years)

BE 26–2 (FIN MAN); BE 12–2 (MAN)

8.8 years ($374,000 ÷ $42,500)

BE 26–3 (FIN MAN); BE 12–3 (MAN)

BE 26–4 (FIN MAN); BE 12–4 (MAN)

20%

[($463,565 ÷ $115,000) = 4.031, the present value of an annuity factor for nine

periods at 20%, from Exhibit 5]

BE 26–5 (FIN MAN); BE 12–5 (MAN)

a.

Present value of $50,000 per year at 12% for 8 years* ……………………..

$ 248,400

Present value of $8,000 at 12% at the end of 8 years** …………………….

3,232

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

EXERCISES

Ex. 26–1 (FIN MAN); Ex. 12–1 (MAN)

Project A

Project Z

Average annual income:

$57,600 ÷ 12 ………………………………………………………………………….

$ 4,800

$63,000 ÷ 15 ………………………………………………………………………….

$ 4,200

Average investment:

($55,000 + $5,000) ÷ 2 ……………………………………………………………

($50,000 + $6,000) ÷ 2 ……………………………………………………………

Average rate of return:

$4,800 ÷ $30,000 ……………………………………………………………………

$4,200 ÷ $28,000 ……………………………………………………………………

Ex. 26–2 (FIN MAN); Ex. 12–2 (MAN)

Average Rate Average Annual Income

=Average Investment

of Return

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–3 (FIN MAN); Ex. 12–3 (MAN)

Average Rate Average Annual Income

=Average Investment

of Return

Ex. 26–4 (FIN MAN); Ex. 12–4 (MAN)

Year 1

Years 2–9

Last Year

Initial investment ………………………………………..

$(120,000)

Operating cash flows:

Annual revenues (5,000 units × $18) ………

$ 90,000

$ 90,000

$ 90,000

Selling expenses (3% × $90,000) ……………

(2,700)

(2,700)

(2,700)

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–5 (FIN MAN); Ex. 12–5 (MAN)

Location 1: $975,000 ÷ $150,000 = 6.5-year cash payback period.

Location 2: 5-year cash payback period, as follows:

Net Cash

Flow

Cumulative

Net Cash

Flows

Year 1 ………………………………………………………………………………..

$275,000

$275,000

Ex. 26–6 (FIN MAN); Ex. 12–6 (MAN)

a. The Liquid Soap product line is recommended, based on its shorter cash

payback period. The cash payback period for both products can be determined

using the following schedule:

Initial investment: $540,000

Liquid Soap

Body Lotion

Cumulative

Cumulative

Net Cash

Net Cash

Net Cash

Net Cash

Flow

Flows

Flow

Flows

Year 1 …………………………….

$170,000

$170,000

$90,000

$ 90,000

Liquid Soap has a four-year cash payback period, and Body Lotion has a six-

year cash payback.

b. The cash payback periods are different between the two product lines because

Liquid Soap earns cash faster than does Body Lotion. Even though both

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–7 (FIN MAN); Ex. 12–7 (MAN)

Present Value

Net Cash

Present Value of

a.

Year

of $1 at 15%

Flow

Net Cash Flow

1

0.870

$ 80,000

$ 69,600

b. Yes. The $24,520 net present value indicates that the return on the proposal is

greater than the minimum desired rate of return of 15%.

Ex. 26–8 (FIN MAN); Ex. 12–8 (MAN)

a.

20Y1

20Y2

20Y3

20Y4

20Y5

Revenues ………………………

$ 65,000

$ 65,000

$ 65,000

$ 65,000

$ 65,000

Net Cash Flow

Present Value

Present Value of

b.

Year

[from part (a)]

of $1 at 12%

Net Cash Flow

20Y1

$19,000

0.893

$ 16,967

20Y2

17,000

0.797

13,549

20Y4

13,000

0.636

c. The total present value of cash flows from the delivery truck investment is

less than the total purchase price of the truck. That is, the net present value

is negative. Thus, this analysis does not support investment in the truck.

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–9 (FIN MAN); Ex. 12–9 (MAN)

a.

(in millions)

Annual revenues ……………………………………………………………….

$ 30

Annual cash expenses ……………………………………………………….

b.

(in millions

except present

value factor)

Annual cash flows ……………………………………………………………..

$ 9

Present value of an annuity of $1 at 14% for 25 periods ……….

× 6.87293*

Present value of hotel project cash flows, rounded ……………..

$ 62

Hotel construction costs ……………………………………………………

Net present value of hotel project ……………………………………….

$ 12

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

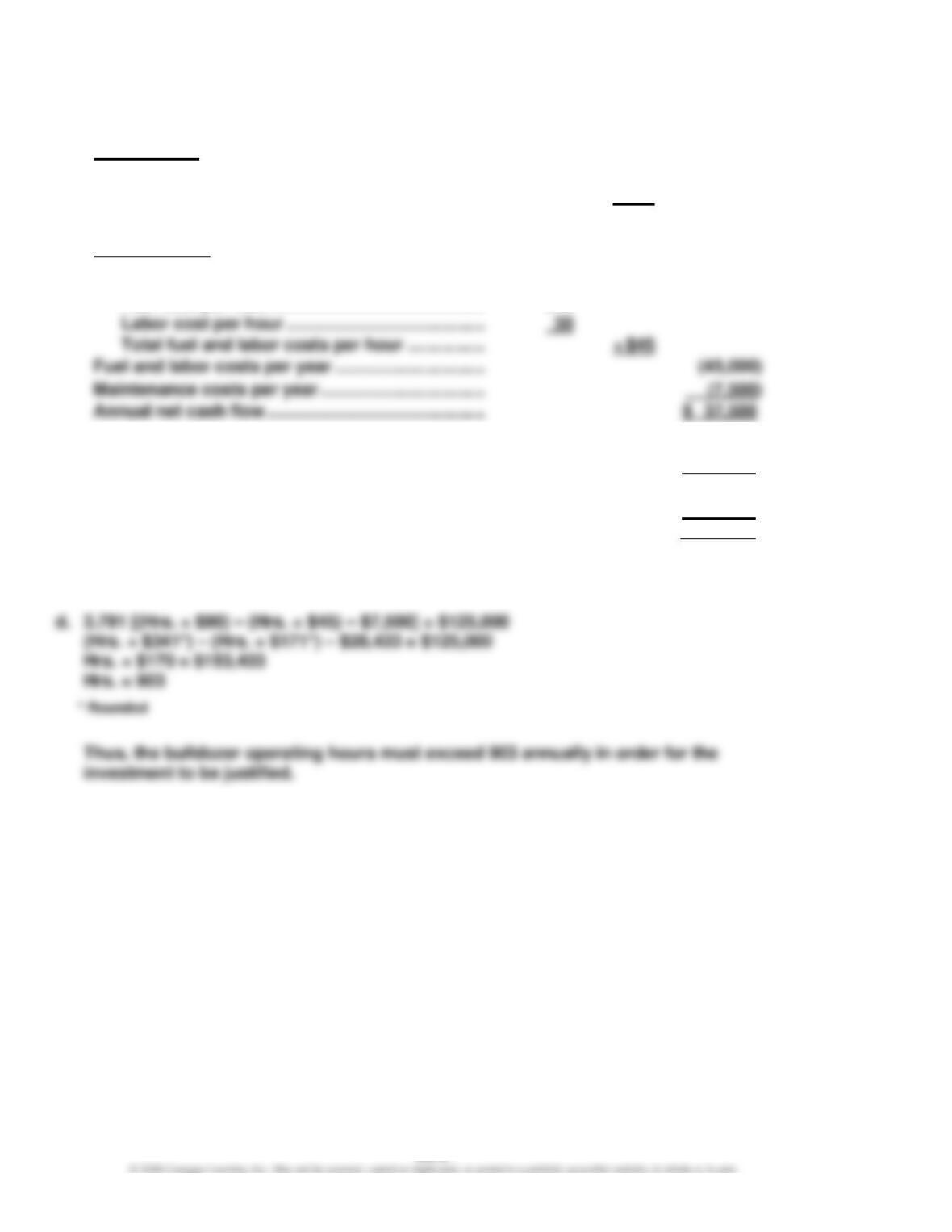

Ex. 26–10 (FIN MAN); Ex. 12–10 (MAN)

a.

Cash inflows:

Hours of operation ………………………………………….

1,000

Revenue per hour …………………………………………..

× $90

Revenue per year ……………………………………………

$ 90,000

Cash outflows:

Hours of operation ………………………………………….

1,000

Maintenance costs per year …………………………….

Annual net cash flow ………………………………………

$ 37,500

Fuel cost per hour ……………………………………..

$15

b.

Annual net cash flow (at the end of each of five years) …….

$ 37,500

Present value of annuity of $1 at 10% for five periods ………

× 3.791

Present value of annual net cash flows …………………………..

$ 142,163

Amount to be invested …………………………………………………..

(125,000)

Net present value …………………………………………………………..

$ 17,163

c. Yes. Jones should accept the investment because the bulldozer cost is less than the

present value of the cash flows at the minimum desired rate of return of 10%.

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–11 (FIN MAN); Ex. 12–11 (MAN)

a.

Revenues (3,600 × 340 days × $280) ………………………………………….

$ 342,720,000

Variable expenses (3,600 × 340 days × $100) ……………………………..

(122,400,000)

Fixed expenses (other than depreciation) ………………………………….

(90,000,000)

Annual net cash flow ………………………………………………………………..

$ 130,320,000

Ex. 26–12 (FIN MAN); Ex. 12–12 (MAN)

a.

Total Present Value of Net Cash Flow

Present Value Index = Amount to Be Invested

Des Moines:

$712,500 = 0.95

$750,000

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–13 (FIN MAN); Ex. 12–13 (MAN)

a. Annual net cash flow—Sewing Machine:

$80,640 = 1,800 hours × (290 baseballs – 150 baseballs) × $0.32 per baseball

Annual net cash flow—Packing Machine:

$29,400 = 1,400 hours × $21 labor cost saved per hour

Sewing Machine:

Annual net cash flow (at the end of each of 8 years) ……………………….

$ 80,640

Present value of annual net cash flows ………………………………………….

Packing Machine:

Annual net cash flow (at the end of each of 8 years) ……………………….

$ 29,400

Present value of an annuity of $1 at 15% for 8 years (Exhibit 5) ……….

b.

Total Present Value of Net Cash Flow

Present Value Index = Amount to Be Invested

c. The present value index indicates that the packing machine would be the

preferred investment, assuming that all other qualitative considerations are

equal. Note that the net present value of the sewing machine is greater than

the packing machine’s. However, the sewing machine requires more than triple

the investment than the packing machine ($260,000 vs. $85,000), for barely

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–14 (FIN MAN); Ex. 12–14 (MAN)

a.

$156,250 *

Average rate of return on investment : = 25%

($1,250,000 + $0) ÷ 2

* The annual earnings are equal to the cash flow less the annual depreciation expense,

shown as follows:

$312,500 – ($1,250,000 ÷ 8 years) = $156,250

Ex. 26–15 (FIN MAN); Ex. 12–15 (MAN)

a.

$1, 400,000

Payback period : = 4 years

$350,000

b. Net present value:

Present value factor for an annuity of $1, 10 periods at 10%: 6.145

Net present value = (6.145 × $350,000) – $1,400,000 = $750,750

c. Some critical elements that are missing from this analysis are:

• The manager is viewing the acquisition of automated assembly equipment as

a labor-saving device. This is probably a limited way to view the investment.

• The cost of the automated assembly equipment does not stop with the initial

purchase price and installation costs. The equipment will require the company

to hire engineers and support personnel to keep the machines running, to

• The analysis fails to account for taxes.

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–16 (FIN MAN); Ex. 12–16 (MAN)

Present Value Factor for an Amount to Be Invested

b. 15% Row 6 in Exhibit 5. The column associated with the factor 3.785 is 15%.

Ex. 26–17 (FIN MAN); Ex. 12–17 (MAN)

Present Value Factor for an Amount to Be Invested

=Annual Net Cash Flow

Annuity of $1 for 10 Periods

b. There are many uncertainties that could adversely impact a project of this scale

and scope. There are uncertainties affecting the initial investment and the annual

cash flow assumptions. Regarding the initial investment, the construction cost

could be higher than $415 million, due to delays, labor issues, and other

construction site problems. The annual cash flow assumptions could be adversely

impacted by uncertainties such as:

1. Warm weather conditions, or no snow

2. Recessionary economic conditions that reduce the demand for ski holidays

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–18 (FIN MAN); Ex. 12–18 (MAN)

a.

Delivery Truck

Cash received from additional delivery (95,000 bags × $0.45) …………..

$ 42,750

Cash used for operating expenses (24,000 miles × $1.35) ………………..

Internal Rate of Return = 15% (from text Exhibit 5 for 7 periods)

Bagging Machine

Direct labor savings (3 hrs./day × $18/hr. × 250 days/yr.) …………………

$13,500

Present Value Factor for an Annuity Amount to Be Invested

b. To: Management

Re: Investment Recommendation

An internal rate of return analysis was performed for the delivery truck and

bagging machine investments. The internal rate of return for the bagging

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–19 (FIN MAN); Ex. 12–19 (MAN)

a.

Present value of annual net cash flows ($35,000 × 4.968*) ……………….

$ 173,880

Amount to be invested ………………………………………………………………….

(186,725)

Net present value ………………………………………………………………………….

$ (12,845)

*

Present value of an annuity of $1 at 12% for 8 periods from text Exhibit 5.

b. The rate of return is less than 12% because there is a negative net present

value.

Ex. 26–20 (FIN MAN); Ex. 12–20 (MAN)

With an expected useful life of five years, the cash payback period cannot be

greater than five years. This would indicate that the cost of the initial investment

would not be recovered during the useful life of the asset. In addition, there would

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

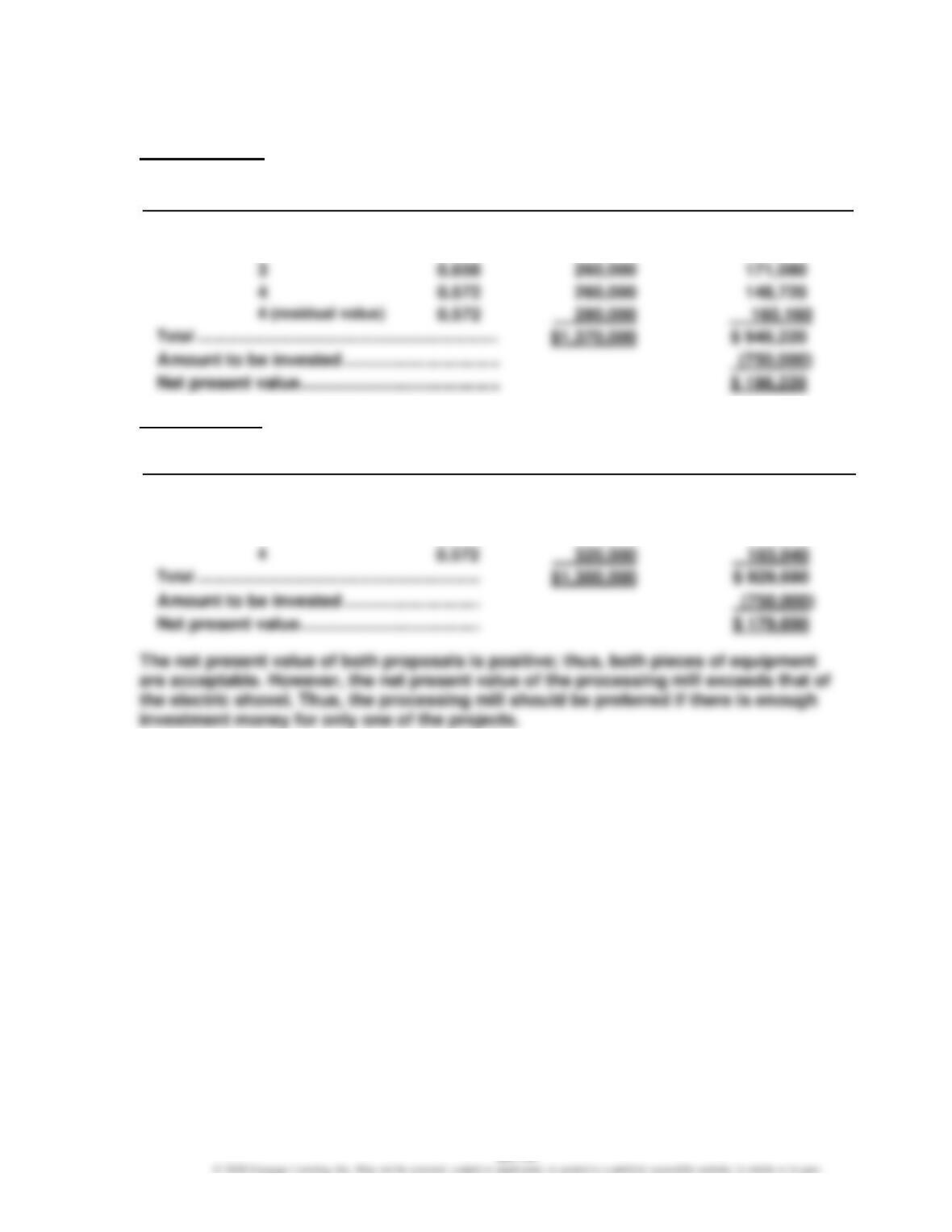

Ex. 26–21 (FIN MAN); Ex. 12–21 (MAN)

Processing Mill

Present Value

Net Cash

Present Value of

Year

of $1 at 15%

Flow

Net Cash Flow

1

0.870

$ 310,000

$ 269,700

2

0.756

260,000

196,560

0.658

0.572

Electric Shovel

Year

Present Value

of $1 at 15%

Net Cash

Flow

Present Value of

Net Cash Flow

1

0.870

$ 330,000

$ 287,100

2

0.756

325,000

245,700

3

0.658

325,000

213,850

0.572

Note to Instructors: Because the investment amount is the same, the net present value

can be compared to determine preference. That is, the present value index will show

the same preference ordering.

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Ex. 26–22 (FIN MAN); Ex. 12–22 (MAN)

a. Blending Equipment

Equal annual cash flows for Years 1–5 …………………………

$ 19,000

Present value of a $1 annuity at 10% for five

periods (Exhibit 5) …………………………………………………….

× 3.791

Residual value at end of fifth year ………………………………..

Computer System

Equal annual cash flows for Years 1–5 …………………………

$ 27,000

Present value of a $1 annuity at 10% for five

periods (Exhibit 5) …………………………………………………….

× 3.791

b. Present value index of blending equipment:

$81,344 = 1.08

$75,000

Present value index of computer system:

$102,357 = 1.14

$90,000

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

PROBLEMS

Prob. 26–1A (FIN MAN); Prob. 12–1A (MAN)

1. a. Average annual rate of return for both projects:

$56,250 ÷ 5 $11,250

= = 30.0%

($75,000 + $0) ÷ 2 $37,500

b. Net present value analysis:

Present Value of

Present

Net Cash Flow

Net Cash Flow

Value of

Front-End

Front-End

Year

$1 at 12%

Loader

Greenhouse

Loader

Greenhouse

1

0.893

$ 40,000

$ 26,250

$ 35,720

$ 23,441

2

0.797

35,000

26,250

27,895

20,921

4

0.636

16,695

(75,000)

$ 24,941

2. The report to the capital investment committee can take many forms. The report

should, as a minimum, present the following points:

a. Both projects offer the same average annual rate of return.

b. Although both projects exceed the selected rate established for discounted cash

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Prob. 26–2A (FIN MAN); Prob. 12–2A (MAN)

1. a. Cash payback period for both projects: 2 years (the year in which accumulated

net cash flows equal $900,000), shown as follows:

Plant Expansion

Retail Store Expansion

Net Cash

Cumulative

Net Cash

Cumulative

Year

Flow

Net Cash Flow

Year

Flow

Net Cash Flow

1

$450,000

$450,000

1

$500,000

$500,000

2

2

b. Net present value analysis:

Present Value of

Present

Net Cash Flow

Net Cash Flow

Value of

Plant

Retail Store

Plant

Retail Store

Year

$1 at 15%

Expansion

Expansion

Expansion

Expansion

1

0.870

$ 450,000

$ 500,000

$ 391,500

$ 435,000

2

0.756

450,000

400,000

340,200

302,400

3

0.658

340,000

350,000

223,720

230,300

4

0.572

143,000

2. The report can take many forms and should include, as a minimum, the following

points:

a. Both projects offer the same total net cash flow.

b. Both projects offer the same cash payback period.

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Prob. 26–3A (FIN MAN); Prob. 12–3A (MAN)

1.

Maintenance Equipment

Present Value

Net Cash

Present Value of

Year

of $1 at 20%

Flow

Net Cash Flow

1

0.833

$ 4,000,000

$ 3,332,000

3

0.579

2,500,000

1,447,500

Ramp Facilities

Present Value

Net Cash

Present Value of

Year

of $1 at 20%

Flow

Net Cash Flow

1

0.833

$12,000,000

$ 9,996,000

2

0.694

10,000,000

6,940,000

$31,000,000

Net present value ………………………………………

$ 2,147,000

Computer Network

Present Value

Net Cash

Present Value of

Year

of $1 at 20%

Flow

Net Cash Flow

1

0.833

$ 6,000,000

$ 4,998,000

2

0.694

5,000,000

3,470,000

3

0.579

4,000,000

2,316,000

CHAPTER 26 (FIN MAN); CHAPTER 12 (MAN) Capital Investment Analysis

Prob. 26–3A (FIN MAN); Prob. 12–3A (MAN) (Concluded)

2.

Total Present Value of Net Cash Flow

Present Value Index = Amount to Be Invested

$7,208,500

Maintenance equipment : = 0.90 *

$8,000,000

* Rounded

3. The computer network has the largest present value index. Although ramp

facilities has the largest net present value, it returns less present value per dollar