Case 12-52 Student Name:

Class:

1.

NORTH AMERICAN INDUSTRIES

Segmented Income Statement by Geographic Areas

For the Fiscal Year Ended April 30, 20×4

Geographic Areas

United States Canada Mexico Unallocated Total

Sales in unitsa

Furniture * * * *

Sports * * * *

Housewares * * * *

Total unit sales * * * *

Revenueb

Furniture * * * *

Sports * * * *

Housewares * * * *

Total revenue * * * *

Variable costsc

Furniture * * * *

Sports * * * *

Housewares * * * *

Total variable costs * * * *

Contribution margin * * * *

Fixed costs

Manufacturing overheadd* * * *

Depreciatione* * * *

Administrative and selling expenses * * * * *

Total fixed costs * * * * *

Operating income (loss) * * * * *

SUPPORTING CALCULATIONS:

aSales in units

Total units x % of Sales = Units Sold

United States

Furniture * * *

Sports * * *

Housewares * * *

Canada

Furniture * * *

Sports * * *

Housewares * * *

Mexico

Furniture * * *

Sports * * *

Housewares * * *

bRevenue

Units Sold Unit Price Revenue

United States

Furniture * * *

Sports * * *

Housewares * * *

Canada

Furniture * * *

Sports * * *

Housewares * * *

Mexico

Furniture * * *

Sports * * *

Housewares * * *

cVariable costs

Variable Variable Total

Production Selling Variable

Units Sold Cost/Unit Cost/Unit Cost

United States

Furniture * * * *

Sports * * * *

Housewares * * * *

Canada

Furniture * * * *

Sports * * * *

Housewares * * * *

Mexico

Furniture * * * *

Sports * * * *

Housewares * * * *

dManufacturing overhead

Total Area Proportion Allocated

Production Variable of Production

Overhead Costs Total Cost

United States * * * *

Canada * * * *

Mexico * * * *

Total * *

eDepreciation Expense

Area Proportion

Total Units of Allocated

Depreciation

Sold Total Depreciation

United States * * * *

Canada * * * *

Mexico * * * *

Total * *

2. Areas where the company’s management should focus its attention in order

to improve corporate profitability include the following:

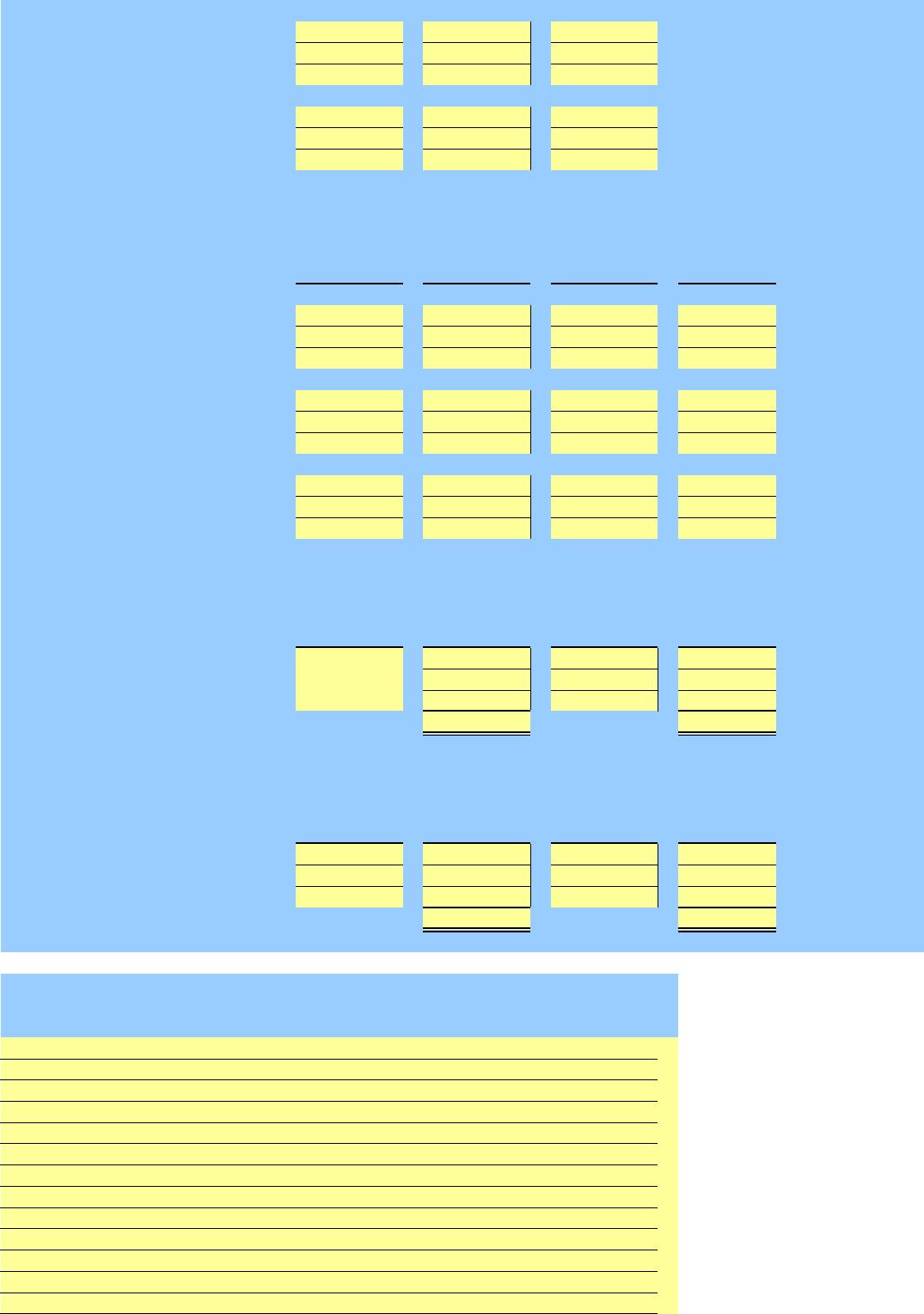

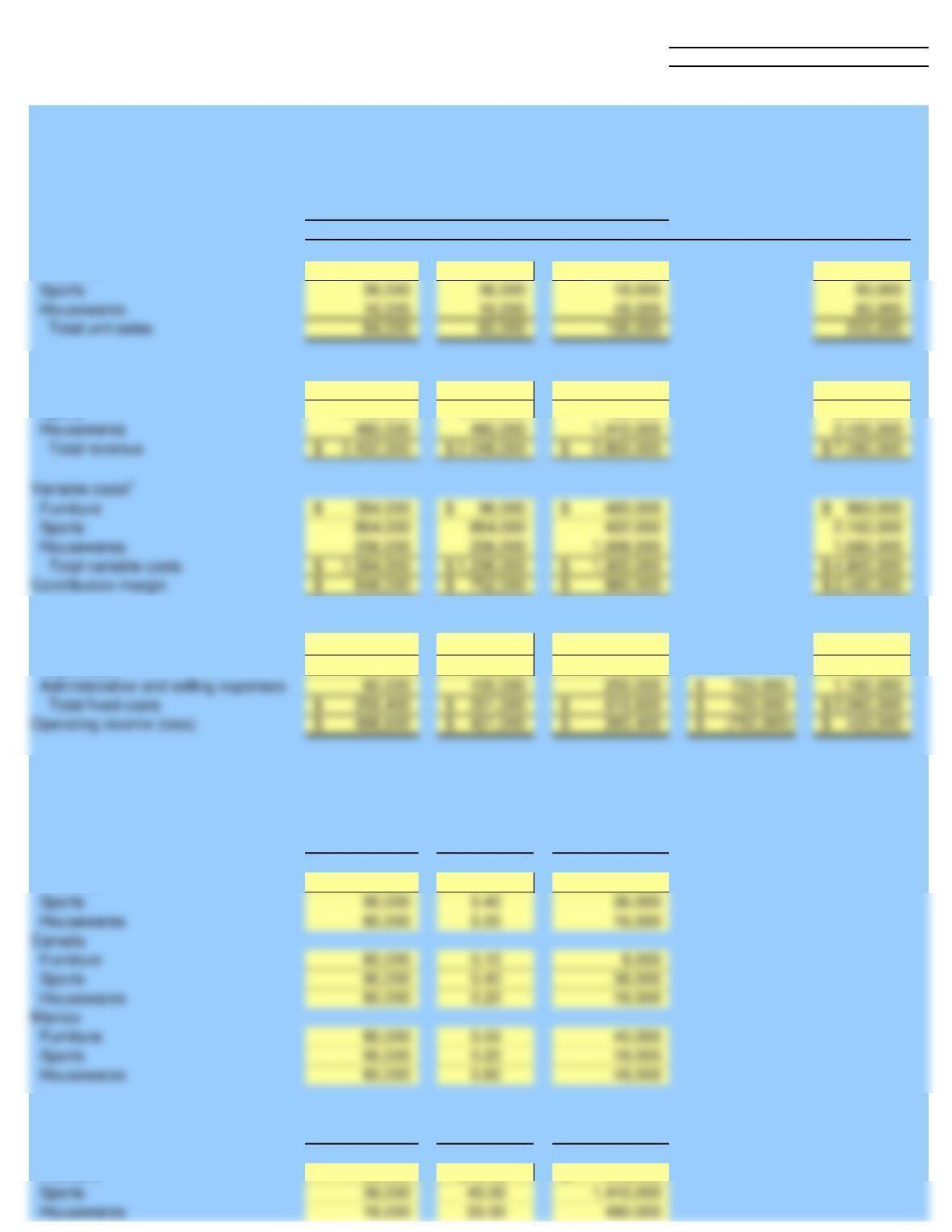

Case 12-52 Student Name:

Class:

1.

NORTH AMERICAN INDUSTRIES

Segmented Income Statement by Geographic Areas

For the Fiscal Year Ended April 30, 20×4

Geographic Areas

United States Canada Mexico Unallocated Total

Sales in unitsa

Furniture 32,000 8,000 40,000 80,000

Revenueb

Variable costsc

Furniture 512,000$ 128,000$ 640,000$ 1,280,000$

Sports 1,440,000 1,440,000 720,000 3,600,000

Fixed costs

Manufacturing overheadd165,000$ 135,000$ 200,000$ 500,000$

Depreciatione134,400 96,000 169,600 400,000

SUPPORTING CALCULATIONS:

aSales in units

Total units % of Sales Units Sold

United States

Furniture 80,000 0.40 32,000

bRevenue

Units Sold Unit Price Revenue

United States

Furniture 32,000 $16.00 512,000$

Instructor

McGraw-Hill/Irwin

Canada

Furniture 8,000 16.00 128,000

cVariable costs

Variable Variable Total

Production Selling Variable

Units Sold Cost/Unit Cost/Unit Cost

United States

Furniture 32,000 8.00$ 4.00$ 384,000$

Sports 36,000 19.00 5.00 864,000

dManufacturing overhead

Total Area Proportion Allocated

Production Variable of Production

Overhead Costs Total Cost

United States 500,000$ 1,584,000$ 33% 165,000$

eDepreciation Expense

Area Proportion

Total Units of Allocated

Depreciation Sold Total Depreciation

United States 400,000$ 84,000$ 33.6% 134,400$

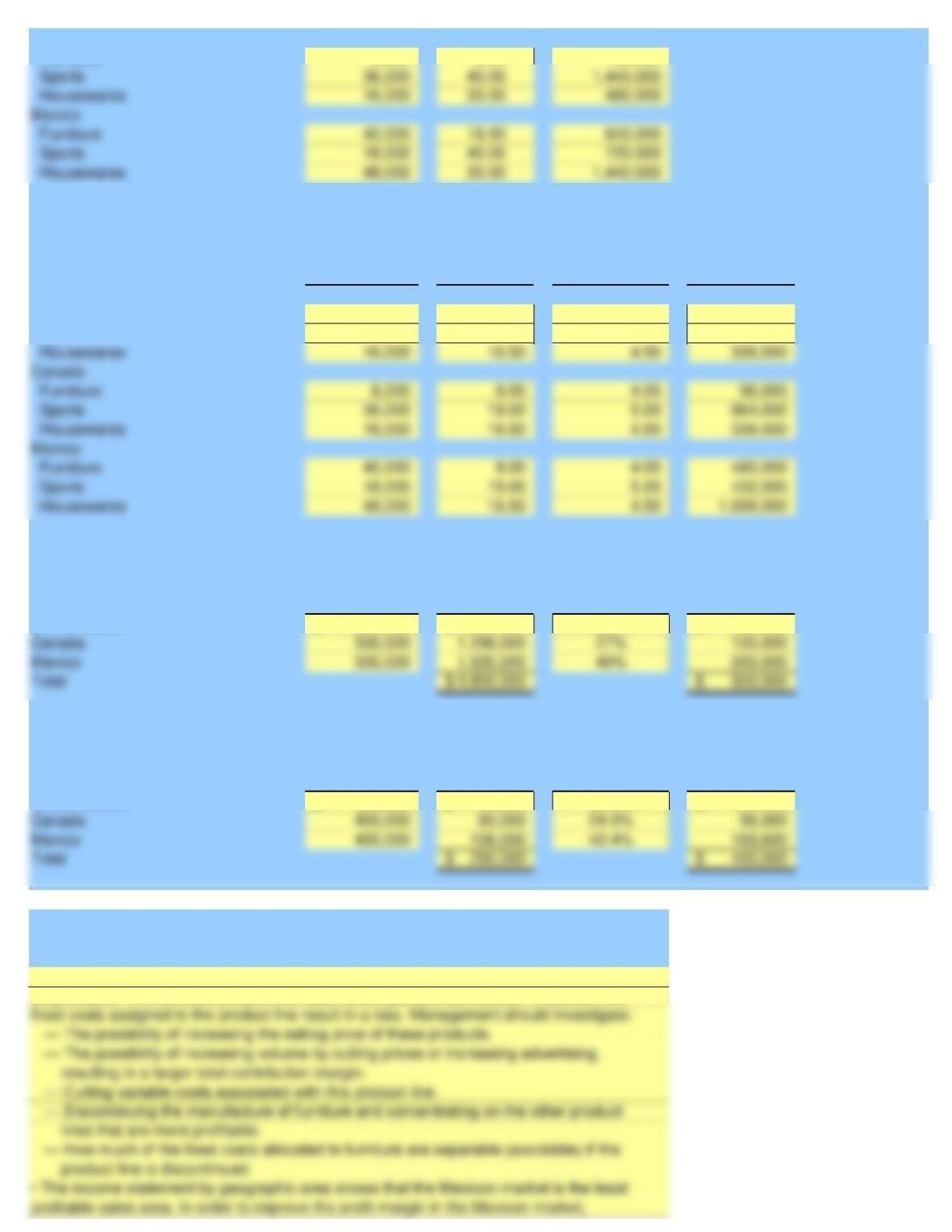

2. Areas where the company’s management should focus its attention in order

to improve corporate profitability include the following:

fixed costs assigned to the product line result in a loss. Management should investigate:

profitable sales area. In order to improve the profit margin in the Mexicon market,

• The income statement by product line shows that the furniture product line may not

be profitable. The furniture product line does have a positive contribution. However, the

considerably higher than those in other areas.

management should:

— Investigate the selling and administrative expenses in this area as they are

— Consider increasing the sales of product lines other than furniture as this product

line makes the smallest contribution to profit.

costs and improve overall profitability.